Florida isn't just another flood insurance state. It holds about 20% of all private residential flood policies in the U.S., according to a Wharton and Resources for the Future analysis. That one fact changes the conversation. In most places, flood insurance means NFIP first and maybe private as an afterthought. In Florida, private flood is a real market, a real option, and for many homeowners, the smarter one.

The mistake I see most often is simple. People shop flood insurance like they're shopping for the cheapest way to satisfy a lender. That's backwards. The critical question is whether the policy gives you enough money and enough usable coverage to rebuild your life after a flood. For a lot of Florida homes, especially higher-value homes, that's where the gap between NFIP and private flood becomes impossible to ignore.

Table of Contents

- Why Florida Is the Epicenter of the Flood Insurance Debate

- Understanding Your Florida Flood Risk

- NFIP vs Private Flood A Detailed Comparison

- Analyzing the Costs and Pricing Models

- Eligibility Lender Requirements and Availability

- When to Choose NFIP vs a Private Policy

- Florida Flood Insurance FAQs

- Can I switch from NFIP to private flood insurance in Florida

- Do I have to wait for my NFIP policy to expire before getting a private quote

- What if my private flood option offers broader coverage but I'm worried about consistency

- Does a condo association's flood coverage protect my unit and belongings

- Is private flood insurance always better than NFIP in Florida

- What's the biggest mistake Florida homeowners make

Why Florida Is the Epicenter of the Flood Insurance Debate

Florida sits at the center of this argument because homeowners here often have a real choice. In many states, flood insurance is mostly a one-lane conversation. In Florida, owners of primary homes, second homes, coastal properties, and higher-value houses often have to decide whether the standard government option is enough or whether private coverage is the only way to protect the actual rebuild cost.

That choice matters more in Florida due to its extensive flood exposure. You have storm surge, inland rain events, canal and drainage issues, and a large number of homes with rebuilding costs that can outrun standard flood limits fast. If your house would cost far more to rebuild than a basic policy will pay, the wrong flood policy leaves you self-insuring the gap.

That is the central debate. Price matters, but coverage adequacy matters more.

I see homeowners make the same mistake over and over. They compare premiums before they compare payout ceilings. A lower premium feels like a win until a major flood turns the policy into a partial payment instead of a full recovery plan. For higher-value Florida homes, that is the difference between rebuilding the house you had and settling for what the policy cap allows.

This also connects to the rest of your property protection. If your home sits in an exposed area, review flood choices alongside homeowners insurance for high-risk Florida zones so you are not solving one coverage gap while ignoring another.

Flood losses also create damage that shows up after the water recedes. Wet insulation, staining, swelling, and hidden deterioration inside exterior and interior walls can turn into a much bigger repair bill, which is why homeowners should understand preventing wall compromise indicators as part of post-flood recovery planning.

Florida gives homeowners more options than many other states. That only helps if you choose the policy that can rebuild your property, not just satisfy a lender file.

Understanding Your Florida Flood Risk

The first rule is simple. Homeowners insurance doesn't cover flood damage. If water rises from the ground, pushes in from storm surge, overflows from nearby water, or enters as general floodwater, you're in flood-policy territory, not standard home-policy territory.

Flood zones tell you something, but not everything

Most homeowners hear a flood zone letter and stop there. That's a mistake.

Flood zones can shape lender requirements and pricing, but they don't tell the whole story of how water behaves around your house. A mapped higher-risk zone may trigger a lender requirement. A lower-risk zone may still flood from heavy rain, overwhelmed drainage, neighborhood grading issues, storm surge reach, or nearby canals and retention areas.

Here's the practical way to think about common zone types:

- Zone A or similar high-risk inland zones: Water exposure is a known issue, and lenders often pay close attention.

- Zone V or coastal high-hazard zones: Wave action and coastal flooding concerns can make protection decisions more serious.

- Zone X or lower-risk areas: Lower risk does not mean no risk. It usually means the lender may not require flood coverage.

Your address matters more than the label

I'd rather know what happens on your street after a hard rain than hear someone say, “I'm not in a flood zone.”

Look at the property like a claims adjuster would:

- Street drainage: Does water back up or sit at the curb?

- Lot shape: Does runoff move toward the house?

- Nearby water: Canal, pond, creek, marsh, or tidal water nearby changes the discussion.

- Neighborhood history: Repeated standing water is a warning sign even when maps look favorable.

- House design: Slab homes, low openings, and enclosed lower areas can change the severity of damage.

If you've already seen moisture intrusion or interior warning signs, learn the preventing wall compromise indicators that often show up before damage becomes more expensive and harder to fix.

Practical rule: Buy flood insurance based on how water can reach your property, not just whether a lender demands it.

The financial question is brutally simple

Ask yourself one thing. If floodwater entered your home this season, could you pay for demolition, drying, repairs, replacement of damaged contents, and temporary disruption out of pocket?

Few can recover financially. That's why flood insurance in Florida is a financial planning tool, not just a mortgage requirement.

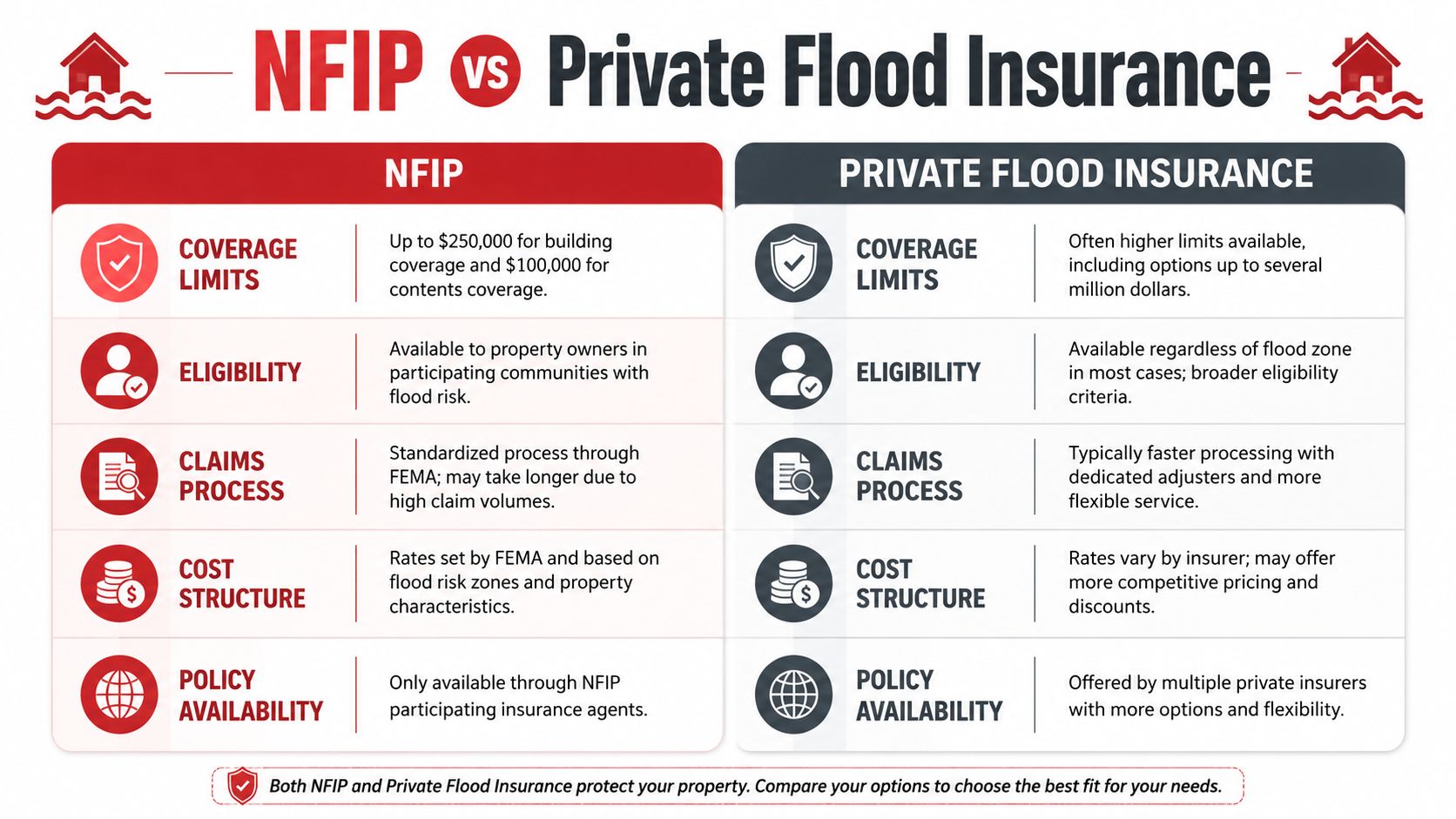

NFIP vs Private Flood A Detailed Comparison

One number drives this decision for many Florida homeowners: $250,000. That is the standard NFIP cap for residential building coverage. For a large share of Florida homes, especially properties with higher rebuild costs, that number is the whole argument.

NFIP vs Private Flood Insurance at a Glance

| Feature | NFIP (National Flood Insurance Program) | Private Flood Insurance |

|---|---|---|

| Coverage limits | Residential building coverage capped at $250,000 and contents at $100,000 | Can offer higher limits for homes that exceed NFIP caps |

| Coverage structure | Standardized policy design | Varies by carrier and underwriting |

| Additional living expenses | Not included in the standard base program | Often included |

| Replacement cost breadth | More limited and standardized | Often broader, depending on policy |

| Waiting period | Generally 30 days before coverage starts | Can vary by insurer |

| Underwriting | Program-based | Property-specific underwriting |

| Best fit | Homes that need standardized access or fit within NFIP limits | Homes that need broader protection or higher limits |

If you are still sorting out lender rules, property location, or whether your mortgage will require a policy at all, review this guide on whether flood insurance is required in Florida.

Coverage limits decide whether you are actually protected

The biggest difference is not branding, convenience, or paperwork. It is whether the policy can realistically pay to put your house back together after a major flood.

NFIP works well for some properties. It gives standardized access to flood coverage, and for lower-value homes or owners mainly trying to satisfy a lender, it may be enough. But for Florida homes with higher reconstruction costs, the NFIP cap can leave a serious gap.

That gap is where homeowners get burned.

A house does not need to be a luxury waterfront property to run past NFIP limits. Rebuild cost rises fast in Florida once you factor in drywall replacement, cabinetry, flooring, insulation, electrical work, labor, and code-related repairs after water damage. If your realistic rebuild number is far above the NFIP ceiling, choosing NFIP alone may solve the mortgage requirement while failing the financial reality test.

My advice is simple. Match flood coverage to rebuild cost, not to the minimum a lender will accept.

Private flood usually offers better recovery after a serious loss

The second major difference is what happens after the floodwater is gone.

As explained in this overview of private flood versus NFIP coverage features, private policies often include additional living expenses or loss-of-use coverage and may offer broader replacement cost options. Standard NFIP coverage does not include loss of use.

That matters in real life. If your kitchen is torn out, flooring is removed, and moisture work keeps the home unlivable for weeks, the claim is not just about drywall and baseboards. It is about where your family lives during repairs and how much of that disruption you pay for yourself.

Private coverage is often the better fit if you want protection for:

- Higher-value structures that would clearly exceed NFIP limits

- Temporary housing costs after a flood loss

- Broader replacement features that better match modern rebuild costs

- A more complete recovery plan, not just a bare-bones payout

Standardized access vs property-specific underwriting

NFIP is predictable. The form is standardized, and that consistency helps homeowners who need a straightforward option.

Private flood is more customized. Underwriting can be more selective, but the upside is a policy that may fit the actual property better. That can mean higher limits, broader benefits, or terms that make more sense for the home you own instead of the average home the program was built around.

For a modest home with rebuild costs that fit comfortably inside NFIP limits, the standardized route can be perfectly reasonable. For a Florida home with expensive finishes, larger square footage, or a rebuild cost that would strain the NFIP cap, private flood deserves first look.

Timing still matters

Waiting periods can affect what you can buy and when coverage starts. NFIP generally has a 30-day waiting period before coverage begins. Private policies may use different rules.

Do not wait until a storm is approaching to make this choice. By then, your options may be limited, and the wrong policy decision gets expensive fast.

Analyzing the Costs and Pricing Models

In Florida, the wrong flood policy can leave a six-figure rebuild gap even when you paid for coverage every year. That is the primary pricing problem.

Why two quotes for the same home can look very different

NFIP and private carriers do not price flood risk the same way. One uses a standardized program structure. The other uses property-level underwriting and its own appetite for risk. That is why one home can get two very different quotes for what looks like the same protection on page one.

Start with the property itself. A newer inland house with better elevation and fewer red flags may get a very competitive private offer. A coastal home, an older slab home, or a property with claim history may price better through NFIP, or may have fewer private options.

The mistake is focusing on premium before you check the coverage ceiling.

For many Florida homes, especially higher-value homes, the bigger question is simple. If this house takes on major flood damage, which policy gives me enough money to rebuild it the way it stands today? If the answer is neither, keep shopping or adjust limits. A lower premium does not fix underinsurance.

Ask these questions before you compare the annual cost:

- What is the building limit, and does it match today's rebuild cost?

- What is the contents limit, and is it enough for what is in the home?

- Do I get payment for temporary housing after a covered flood loss?

- How much am I keeping on my own shoulders through the deductible?

- Will this policy satisfy my lender without delays at closing?

How I'd judge price in real life

For a lower-value home that fits comfortably inside NFIP limits, NFIP can be the practical choice. The pricing may be fair, the form is familiar, and the coverage may be adequate for the structure.

That logic breaks down fast on homes with high rebuild costs.

If your house would cost far more to reconstruct than the policy can pay, the cheaper option is often the more expensive mistake. I see this most often with larger Florida homes, custom interiors, upgraded kitchens, expensive flooring, and homes in areas where labor and material costs spike after a major storm. After a widespread flood event, rebuilding is never cheap, and being short on limits hurts at the worst possible time.

Use a side-by-side comparison like this:

| What to compare | Why it matters |

|---|---|

| Building limit | This determines whether the policy can cover major structural repairs or a near-total rebuild |

| Contents limit | Furniture, electronics, flooring, and personal property add up faster than many owners expect |

| Additional living expenses or loss of use | This decides whether you pay hotel and rental costs out of pocket after a serious loss |

| Deductible | A low premium paired with a deductible you cannot comfortably absorb is a bad trade |

| Waiting period | This affects closings, lender timelines, and when coverage actually starts |

If you have a mortgage, confirm how flood coverage fits into the larger loan picture. The 24hourEDU mortgage insurance guide is a useful primer for homeowners who want to understand how lenders look at property-related insurance requirements.

Business owners should use the same pricing discipline. If you are comparing commercial options, review business flood insurance in Orlando and Florida before you decide on limits.

Cheap flood insurance is only cheap if the payout is big enough to put the property back together.

Eligibility Lender Requirements and Availability

A policy can look great on paper and still fail a practical test if you can't get it, can't keep it, or your lender won't accept it.

Who can usually get what

NFIP is the more standardized option. For many properties, it's the default path because it's familiar and broadly recognized.

Private flood is different. Availability depends on underwriting. That means a private insurer can be selective about the homes it wants to insure. One property may qualify for broad private coverage with strong terms. Another may get declined or offered less attractive options.

That doesn't make private flood bad. It just means private flood behaves like private insurance.

Private policies can also offer broader protection. As noted in the earlier coverage section, private flood often includes additional living expenses and broader replacement features that standard NFIP coverage typically doesn't. That can make private flood attractive for homeowners who care about lifestyle disruption, not just raw building damage.

What to confirm with your lender before you bind anything

Don't assume the lender will sort it out after the fact. Confirm acceptance before you pay for a private policy.

Use this checklist:

- Ask for private flood acceptance requirements: Some lenders want specific documentation.

- Confirm the required building amount: The policy has to satisfy the lender's minimum standard.

- Check the mortgagee clause details carefully: Small paperwork mistakes create closing delays.

- Verify timing: If the policy is for a purchase or refinance, effective date matters.

If you're also trying to understand related loan protections, this plain-English 24hourEDU mortgage insurance guide helps clarify a different coverage concept that borrowers often confuse with property insurance.

A flood policy isn't useful for closing if the lender won't approve it in time.

Availability is part of the risk decision

If your property is difficult to place privately, NFIP may be the practical answer. If you qualify for strong private terms and your lender accepts them, private may give you a much better recovery position.

This is why the right choice isn't ideological. It's property-specific.

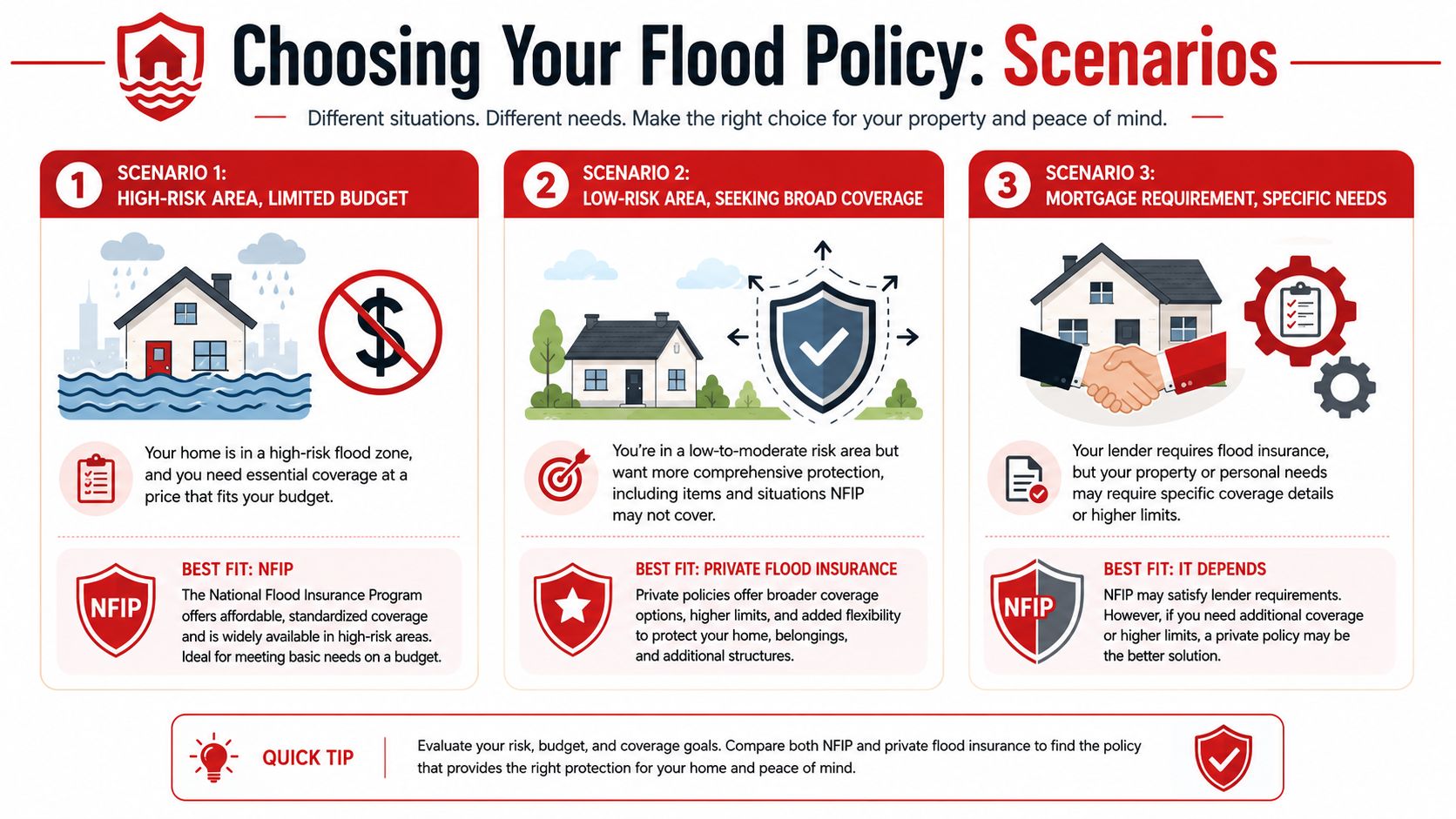

When to Choose NFIP vs a Private Policy

The cleanest way to make this decision is to stop thinking in product categories and start thinking in homeowner profiles.

Florida's regulator makes the key issue plain. Florida is the largest private residential flood market in the country, and one of the main reasons is the limits adequacy problem. With NFIP residential building coverage capped at $250,000, many homeowners need more than the federal program can provide, as explained by the Florida Office of Insurance Regulation flood insurance guidance.

Choose private when coverage adequacy is the issue

If your home's rebuild need clearly exceeds the NFIP cap, private flood should be your first serious look.

That applies especially when:

- Your home has higher rebuild costs: Materials, finishes, and labor can push true exposure well above the federal limit.

- You want broader claim protection: Temporary housing and broader replacement features can matter as much as the building limit.

- You view flood insurance as asset protection: You're trying to preserve savings and equity, not just satisfy a mortgage condition.

If you own a coastal home, a newer custom home, or a property with significant interior value, don't let price distract you from the larger math. A lower premium paired with an inadequate cap is not a bargain.

Choose NFIP when stability or access is the issue

NFIP can be the better answer when broad availability and standardization matter more than custom coverage.

NFIP often makes the most sense when:

- Your home fits within the federal cap reasonably well

- Private underwriting options are limited

- Your lender prefers a straightforward standardized product

- You need a familiar baseline policy rather than broader optional features

For some homeowners, that's enough. Not every home needs a more customized private policy.

Use a layered approach when one policy alone isn't enough

Some Florida homeowners don't fit neatly into one camp. They need the predictability of a standard base policy but still have a meaningful exposure above that base amount.

That's where layered thinking becomes useful. If the home's risk profile and lender situation support it, pairing a primary policy structure with higher-limit protection can make more sense than relying on one policy to do everything.

The right flood policy is the one that leaves you able to rebuild, not the one that looks cheapest on renewal day.

My blunt recommendation is this. If your house would be financially painful to rebuild after a major flood, don't default to NFIP just because it's familiar. Get both paths evaluated, then choose based on whether the coverage is adequate.

Florida Flood Insurance FAQs

Can I switch from NFIP to private flood insurance in Florida

Yes, in many cases you can. The smart way to do it is to compare the effective date, lender acceptance, and coverage terms before making any change. Don't cancel first and ask questions later.

Do I have to wait for my NFIP policy to expire before getting a private quote

No. You can shop before renewal. In fact, that's the best time to do it because you can compare limits, coverage breadth, and lender requirements without creating last-minute pressure.

What if my private flood option offers broader coverage but I'm worried about consistency

That's a fair concern. The answer is to review the policy terms carefully and think beyond premium. If consistency and standardized access matter most, NFIP may still be the better fit. If your bigger concern is rebuilding adequately after a loss, private may still be the stronger choice.

Does a condo association's flood coverage protect my unit and belongings

Not necessarily. Association coverage may protect parts of the building structure, but unit improvements, contents, and use-related costs can be a separate issue. Condo owners should verify exactly where the association's responsibility stops.

Is private flood insurance always better than NFIP in Florida

No. It's often better for homeowners who need broader coverage or higher limits. It's not automatically better for every property. The best policy depends on the home, the lender, and the size of the financial gap you're trying to protect.

What's the biggest mistake Florida homeowners make

They focus on premium before they check adequacy. That's the wrong order. First decide how much protection you need. Then compare the cost of buying it.

If you want help sorting through NFIP and private flood options without guessing, Select Insurance Group, Inc. can compare coverage choices for your Florida property and help you focus on what matters: lender acceptance, usable limits, and whether the policy will protect your finances after a real flood loss.