The Charlotte driver sitting in I-77 traffic, the homeowner watching a summer storm roll in over SouthPark, and the contractor trying to insure a work truck parked in a tight urban ZIP code all face the same problem. Insurance in Charlotte isn't generic. The risks are local, the pricing is local, and the mistakes get expensive fast.

That matters even more when a household budget is already stretched. Over 1 million North Carolina residents, or 10.7% of the population, are uninsured for healthcare because of affordability pressures, and that strain can push families to skip auto or home coverage too, leaving major assets exposed, according to Charlotte Legal Advocacy's overview of healthcare access in North Carolina. In practice, that means many people aren't underinsured by choice. They're juggling too many bills at once.

If you're trying to sort out Charlotte NC insurance without getting buried in policy language, this guide is built for real life. It focuses on what Charlotte residents and business owners deal with: heavy commuter traffic, hurricane remnants, tree damage, neighborhood pricing differences, and the trade-off between cheaper premiums now and bigger costs later.

For readers comparing vehicle protection options first, this overview of local auto insurance options in Charlotte and nearby NC cities is a useful starting point.

Table of Contents

- Your Guide to Smart Insurance in Charlotte NC

- NC Insurance Requirements What You Legally Need

- Beyond the Basics Coverages Charlotteans Should Consider

- How Much Does Charlotte NC Insurance Cost in 2026

- Five Smart Strategies for More Affordable Insurance

- Why an Independent Agency Is Your Best Ally

- Get Your Free Charlotte NC Insurance Quote Today

Your Guide to Smart Insurance in Charlotte NC

Charlotte moves fast. A normal weekday can include a long commute, a pop-up downpour, a cracked windshield from highway debris, and a call from your mortgage company asking for updated proof of insurance. Individuals often lack the time to decode exclusions, compare deductibles, and determine whether a low premium is a good deal.

That's where smart Charlotte NC insurance decisions start. Not with chasing the cheapest number on a screen, but with matching coverage to the way you live here. If you drive Uptown, through I-485, or across I-77 every week, your risks are different from someone who barely uses a car. If you own a home near a creek, mature tree line, or older roof stock, your pressure points are different too.

Local risk changes what counts as good coverage

A policy can look fine until something local happens. In Charlotte, that often means storm damage from wind and heavy rain, neighborhood-specific underwriting, or a liability claim that gets bigger than expected because repair and replacement costs have gone up.

Practical rule: If a policy only meets the legal minimum, it may satisfy the state and still leave you paying out of pocket after a serious claim.

Business owners see the same pattern. A NoDa shop, a contractor with vehicles on the road, and a landlord with a duplex don't need the same setup. The right answer depends on property exposure, payroll, vehicle use, and whether one uncovered loss would interrupt income.

What works better than guesswork

Strong insurance planning in Charlotte usually comes down to a few habits:

- Know the legal floor: Minimum required coverage matters, but it isn't the same as real protection.

- Build around local exposures: Traffic corridors, storm patterns, flood zones, and property age all affect coverage choices.

- Review the policy every year: A policy that fit two years ago may not fit after a move, renovation, teen driver, or new business vehicle.

People usually regret two things. Buying too little liability, and assuming a standard policy covers every kind of water loss.

NC Insurance Requirements What You Legally Need

North Carolina sets a legal baseline, not a promise that you'll be fully protected after a loss. If you own a car or run a business with employees, it's worth knowing exactly where that baseline starts.

The legal baseline for drivers

For personal auto coverage, North Carolina requires liability insurance. Drivers often hear the shorthand numbers and never get a plain-English explanation of what they mean. The easier way to read them is this: part of the coverage pays for injuries you cause to other people, and part pays for damage you cause to someone else's property.

For a detailed breakdown from a local agency resource, review North Carolina auto insurance requirements.

| Coverage Type | Requirement | What It Means |

|---|---|---|

| Bodily Injury Liability | 30/60 | Pays for injuries you cause to others. The first number is the limit for one person. The second is the total limit for one accident. |

| Property Damage Liability | 25 | Pays for damage you cause to another person's vehicle or other property. |

| Workers' Compensation for Businesses | Required for businesses with three or more employees | Helps cover medical costs and lost wages for employees hurt on the job, subject to policy and claim rules. |

A lot of Charlotte drivers stop at the minimum because it's the fastest way to become legal. That's understandable. But if you cause a serious wreck on a busy corridor, low liability limits can get used up quickly.

A legal policy keeps you compliant. It doesn't guarantee that it keeps you financially safe.

What businesses need to watch

Business insurance law catches owners off guard more often than auto rules do. Many small companies start with a handful of workers, grow fast, and don't realize when workers' compensation becomes mandatory. That's a problem because a payroll change can create a coverage gap if the policy doesn't keep up.

Three common trouble spots show up in Charlotte:

- Growing crews: A small service business hires quickly and doesn't update coverage in time.

- Vehicle use drift: A personal vehicle starts being used for deliveries, tools, or jobsite travel.

- Subcontractor confusion: Owners assume another party's policy covers everyone on a job, then find out the contract says otherwise.

If you're a sole proprietor with no employees, your setup may look different. If you have staff, leased drivers, or field crews, the details matter. The state requirement is the floor. Contracts, landlords, lenders, and jobsite agreements often require more.

A practical reading of the law

The cleanest way to approach NC insurance requirements is to treat them as your starting checklist:

- Confirm what's mandatory for your situation

- Match policy use to real use

- Raise limits before a claim forces the lesson

That approach avoids the most expensive mistake in insurance. Being technically insured, but functionally uncovered.

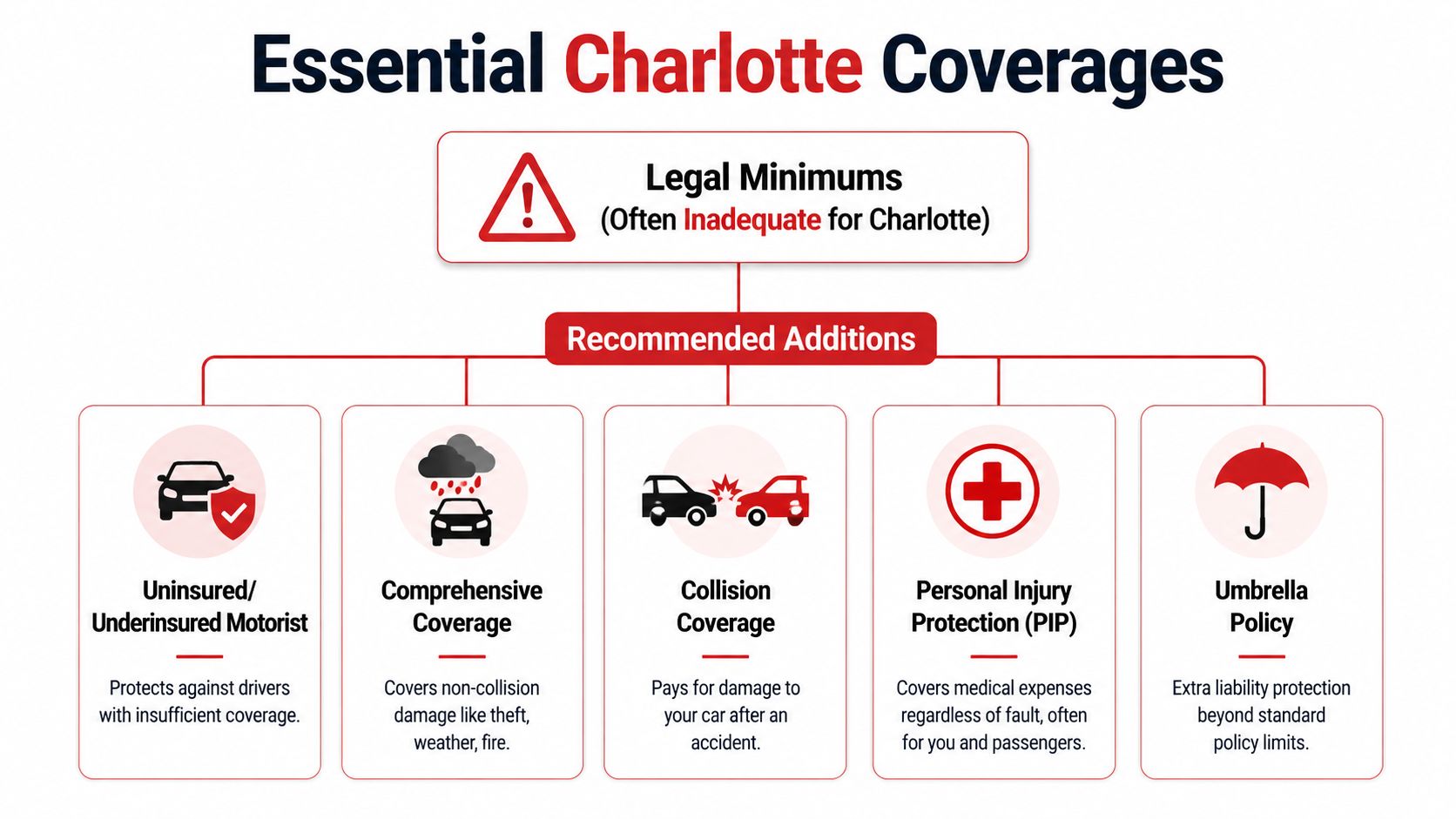

Beyond the Basics Coverages Charlotteans Should Consider

The legal minimum may let you register a vehicle and get on the road. It doesn't account for Charlotte's storm season, crowded interstates, or the cost of repairing newer vehicles and homes.

Why minimum coverage falls short in Charlotte

Start with traffic. If you drive I-77, I-85, or I-485 often, the true risk isn't just causing damage to someone else. It's getting hit by a driver who doesn't have enough insurance, then finding out your own policy doesn't do much to help with the gap.

Then add weather. Charlotte doesn't have to take a direct coastal hit to see damage from hurricane remnants. Heavy rain, wind-driven debris, hail, and falling limbs can wreck a roof or dent a vehicle in one afternoon. Non-collision coverage is what answers many of those non-collision losses.

A separate flood policy deserves its own mention. Standard homeowners insurance typically doesn't cover flood damage. That catches people every year, especially when water backs up, creeks rise, or drainage systems get overwhelmed after repeated storms.

The coverages that usually matter most

These are the additions that often make the biggest difference in Charlotte:

- Uninsured and underinsured motorist coverage: Useful when another driver causes a loss and their limits aren't enough.

- Coverage for damage from non-collision events: Helps with theft, weather damage, fire, and falling objects.

- Collision coverage: Pays for damage to your own vehicle after an accident, even if the repair bill is painful.

- Higher liability limits: Important for households with assets to protect.

- Flood insurance: Critical if your property has any water exposure that goes beyond routine rain runoff.

- A Business Owner's Policy: Often a practical fit for small businesses that need property and liability protection in one package.

If your car sits under trees and your home sits near water, cheap insurance can become expensive insurance very quickly.

One overlooked detail after an auto claim is parts quality and repair language. If you want to understand the replacement parts conversation better before you approve a repair, this guide to CAPA certified parts for repairs gives helpful context.

Common misconceptions that cost people money

Two mistakes show up again and again.

First, people assume "full coverage" is a technical policy type. It isn't. It's just a casual phrase, and it often hides gaps because different people mean different things by it.

Second, homeowners assume all water damage is covered. It isn't. A burst pipe claim and rising floodwater are not the same issue under many policies.

The strongest Charlotte NC insurance plans are built around exposures, not labels.

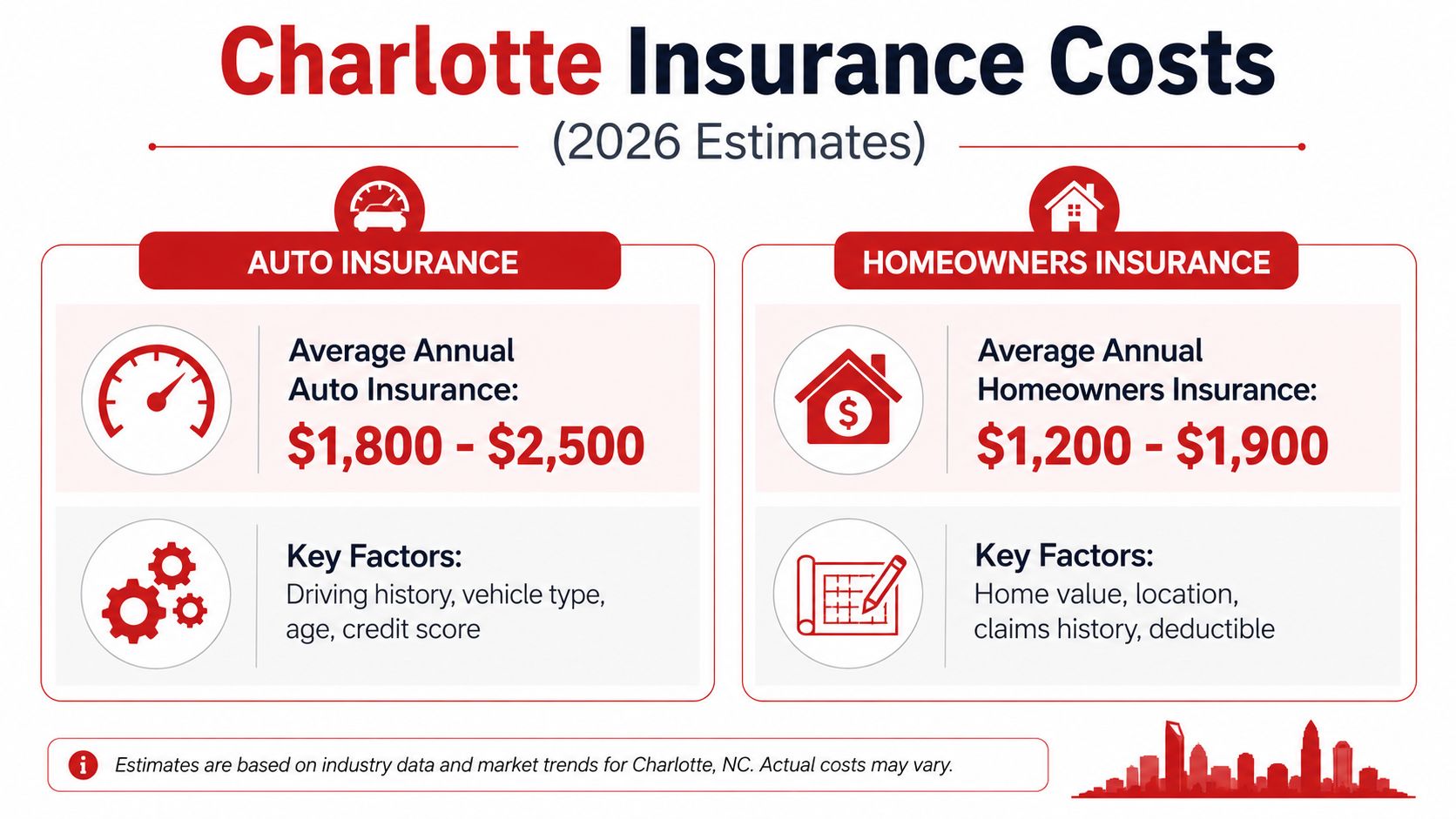

How Much Does Charlotte NC Insurance Cost in 2026

Charlotte insurance pricing frustrates people because the premium can change sharply even when the customer feels like nothing changed. That's because the price isn't built from one factor. It reflects your risk profile, your property, your ZIP code, and the shape of the insurance market itself.

What is pushing premiums upward

One of the biggest cost pressures is market concentration. The top five property and casualty insurers in North Carolina control over 58% of the market, and average homeowners renewal premiums in Charlotte rose 12.3% annually from 2023 through 2025, driven by concentration, rising rebuilding costs, and skilled labor shortages, according to the North Carolina Department of Insurance market share and premium information.

That matters on the ground. When labor is tight and materials take longer to source, every roof, kitchen, siding, or framing claim becomes more expensive to settle. Carriers respond with stricter underwriting, higher deductibles in some cases, and less flexibility on homes or vehicles that already look risky on paper.

Why two Charlotte households can get very different quotes

Charlotte isn't one uniform rating environment. A driver in a dense traffic corridor and a driver in a quieter suburban pocket may see very different offers. The same goes for homeowners. Roof age, property updates, prior claims, proximity to water, and local loss patterns all influence the premium.

Charlotte's wedge and crescent development patterns also matter in practical ways. Neighborhood-level differences in wealth, infrastructure, and access to services can line up with how carriers assess risk. That doesn't mean every household in a given area gets the same outcome. It does mean location can shape pricing and even carrier appetite.

Three broad cost drivers show up most often:

- Property rebuild difficulty: Older homes, specialized materials, and labor delays can push replacement costs up.

- Vehicle repair complexity: Newer cars carry more sensors, pricier parts, and calibration costs after crashes.

- Local underwriting signals: ZIP code, claims activity, and neighborhood characteristics can influence whether a carrier prices aggressively or cautiously.

A high premium isn't always a sign that you're overpaying. Sometimes it's a sign that the risk was priced broadly and not reviewed carefully enough.

The most useful question isn't "Why is insurance expensive?" It's "Which part of my profile is driving the price, and is there a better way to structure the policy?"

Five Smart Strategies for More Affordable Insurance

Lowering your premium without wrecking your protection takes judgment. Some savings moves help. Some only make the policy look cheaper until a claim shows what was removed.

Savings that help without gutting coverage

Start with the changes that usually create real value.

- Bundle where it makes sense: Combining auto with home, renters, or another personal line often provides one of the strongest discounts available.

- Raise deductibles carefully: A higher deductible can reduce premium, but only if you can afford that amount after a loss.

- Clean up policy errors: Garaging address mistakes, outdated mileage, old lienholder information, and wrong vehicle use classifications can all distort pricing.

- Review drivers and vehicles annually: Remove cars you no longer own, update commuting patterns, and ask whether older vehicles still justify physical damage coverage.

- Protect your credit profile: In many cases, stronger credit helps support better pricing.

- Ask about approved training discounts: Defensive driving courses can help some drivers.

What usually backfires

People trying to cut costs fast often make two expensive moves. They slash liability limits, or they drop coverage without looking at the replacement cost of the vehicle or home.

A better approach is to cut waste before cutting protection. If your deductible is too low, if your home policy endorsements don't match the property, or if you're carrying coverage for an old situation, fix that first.

Here's a simple annual checklist:

- Pull your current declarations pages

- Mark anything that changed in the last year

- Check deductibles against your emergency savings

- Review whether every listed driver and vehicle still belongs there

- Compare the package, not just the premium

The cheapest quote wins only if it still works on the day you file a claim.

Good Charlotte NC insurance shopping isn't about chasing the smallest number. It's about spending less on the wrong things so you can keep the protection that matters.

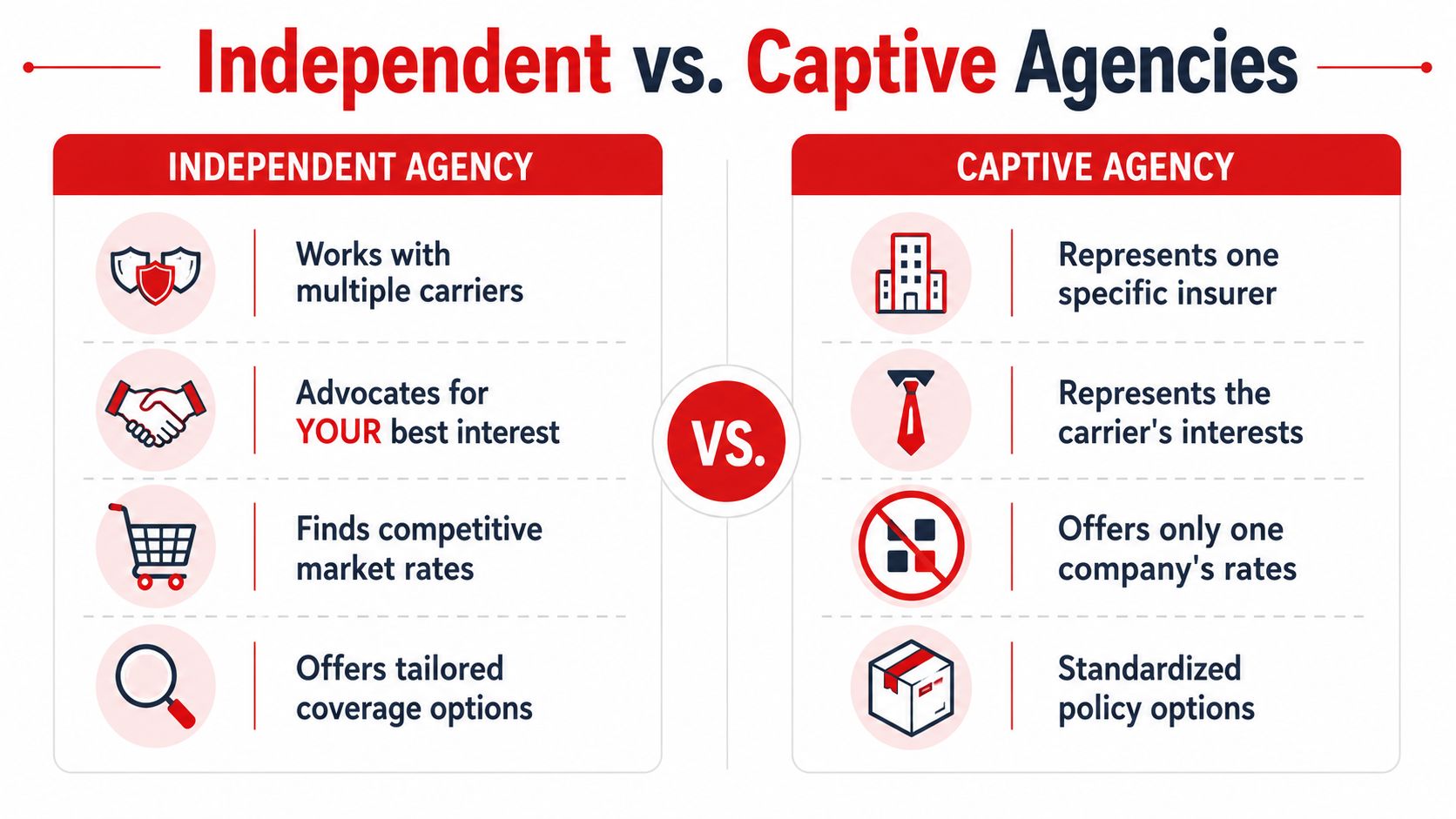

Why an Independent Agency Is Your Best Ally

Charlotte insurance shoppers have more than one way to buy coverage. The important difference isn't just convenience. It's whether the person helping you can look across multiple options or only offer one path.

Choice matters more in a tight market

When markets tighten, limited choice gets expensive. Charlotte's wedge and crescent wealth patterns can correlate with insurance denial rates, and an independent agent can add context and help interpret carrier pricing in underserved zones where automated systems may fall short, based on the UNC Charlotte review of unequal healthcare access and neighborhood patterns.

That local context matters because automated quoting systems don't always tell the full story. A household may look unusual to a rating model for reasons that have little to do with how carefully the property is maintained or how responsibly the vehicle is used.

If you want a plain-language explanation of the model, this article on what an independent insurance agency is breaks it down well.

Where local judgment beats automation

Independent agents tend to be most helpful when the risk isn't perfectly clean. That includes:

- Mixed-use households: A personal vehicle that occasionally supports side work.

- Older homes with updates: The wiring, roof, or plumbing may have improved even if the home age triggers concern.

- Contractors and small fleets: Usage details matter, and direct online forms often oversimplify them.

- Underserved areas: Pricing models can read a ZIP code first and the full household story second.

A captive setup may still work for some shoppers. But if you want broader options, more negotiation room, and advice that isn't limited to a single company's appetite, independence usually gives you a better shot.

Good agency work isn't just quoting. It's translating your real risk into a policy structure carriers can evaluate fairly.

That advocacy matters for business owners especially. A company with vehicles, employees, tools, or jobsite exposure doesn't just need a certificate. It needs someone who can spot the gap before a claim does.

Get Your Free Charlotte NC Insurance Quote Today

At some point, the best move is to stop guessing and get the policy reviewed. That's especially true for Charlotte drivers and business owners whose rates jumped at renewal or whose coverage hasn't been revisited in a while.

A simple way to get started

For businesses, the need for review is even stronger. With 82% of North Carolina's commercial insurance market controlled by a single carrier, businesses need an expert advocate to explore limited competitive options and help secure fair pricing, according to the Health System Tracker analysis of commercial health insurance market concentration.

A clean quote process usually looks like this:

Gather your current policy information

Have your declarations page, driver details, vehicle information, or business operations summary ready.Share the actual use of the risk

Mention commute patterns, work vehicle use, prior claims, recent renovations, payroll changes, or anything else that affects underwriting.Review the quote for structure, not just price

Compare deductibles, exclusions, endorsements, and liability limits. That's where good value shows up.

If you want Charlotte NC insurance that matches the way you drive, own property, or run a business, don't settle for a quick quote that skips the details.

Select Insurance Group, Inc. makes that process easier with fast, no-obligation insurance quotes for personal and commercial coverage. Their independent agency model compares options from multiple carriers, and their bilingual team helps Charlotte-area customers by phone or online with auto, home, renters, business, commercial auto, and more.