You're probably dealing with one of three situations right now. Your auto policy just renewed and the premium jumped. You're looking at a house and suddenly realizing “home insurance in Florida” is its own full-time subject. Or you're opening something local, maybe a food truck, a contractor operation, or a small office, and you need coverage that matches how you work in Orlando.

That's where people usually get stuck. The ads make insurance sound simple. Real life in Central Florida isn't simple. Storm exposure, daily traffic, rental properties, business vehicles, and changing carrier rules all make the decision more complicated than a quick online quote suggests.

A good local guide helps. If you want a broader look at how independent agencies fit into the local market, this overview of insurance agencies in Orlando is a useful starting point. The short version is that the right Orlando insurance agency should do more than sell a policy. It should help you avoid buying the wrong one.

Table of Contents

- Navigating Your Insurance Needs in Orlando

- What an Orlando Insurance Agency Actually Does

- Comparing Common Insurance Policies for Orlando Residents

- How to Choose the Right Orlando Insurance Agency

- Why Select Insurance Group is a Trusted Local Choice

- Get Protected Today with a Free No-Obligation Quote

Navigating Your Insurance Needs in Orlando

Living in Orlando means your insurance questions usually show up in ordinary moments. You're inching along I-4 after work and wondering whether your limits are high enough if there's a serious crash. You're putting together a hurricane prep list and realizing you're not fully sure what your home policy would and wouldn't respond to. You sign a lease for a small storefront or buy a van for your business, and now personal coverage no longer fits what you're doing.

That confusion is normal. Few individuals wake up wanting to compare endorsements, deductibles, liability limits, and exclusions. They want to know one thing. If something goes wrong, will the policy do what they think it does?

In practice, that's the primary value of working with an Orlando insurance agency that knows the local market. The job isn't just to hand over a quote. It's to ask the questions most buyers miss. Is the home owner-occupied or rented out part time? Is the vehicle used only for commuting, or is it also hauling tools and equipment? Is the property a standard single-family home, or something less straightforward like a triplex or a small rental building?

A cheap policy that sidesteps your real exposure isn't a bargain. It's just a delayed problem.

The strongest coverage plans usually come from a conversation, not a form. Orlando residents often need something more customized than the standard direct-to-consumer path provides. That's especially true when a family's needs overlap, such as home, auto, rental property, and business coverage under one roof.

A good agency makes the process feel manageable again. You bring the practical details. They help sort what matters, what doesn't, and where the gaps are.

What an Orlando Insurance Agency Actually Does

Hearing “insurance agency” can lead to the assumption that every office works the same way. They don't. The biggest difference is whether the agency represents one insurance company or whether it shops across multiple carriers for you.

Independent advice versus single-company sales

An independent Orlando insurance agency works more like a personal shopper. Instead of pulling one product off one shelf, it checks several options and matches coverage to the risk. That matters because Orlando residents don't all fit one clean profile. A teacher commuting daily, a first-time landlord with a triplex, and a mobile food business all need very different answers.

Independent agencies in the Orlando and Tampa market typically compare instant quotes from 20 to 40 leading carriers, and the same source says multi-carrier comparison reduces consumer premiums by 15 percent to 25 percent on average through carrier-specific pricing differences and risk models, according to Select Insurance Group's overview of its quoting approach.

That doesn't mean the cheapest quote is automatically the right one. It means you get a broader field to compare price, coverage details, eligibility, and turnaround time.

If you're shopping for vehicle coverage first, this guide to an auto insurance agency in Florida helps clarify how local drivers can compare policy options without losing sight of coverage quality.

Where an agency earns its keep

An agency proves its value in the parts of insurance that don't fit neatly into an ad.

- Matching use to policy type. A lot of claim problems start with a bad fit. A personal auto policy may not line up with business use. A standard home policy may not fit a multi-unit rental setup.

- Explaining trade-offs clearly. Lower premium often means higher out-of-pocket exposure, narrower protection, or stricter limitations on certain losses.

- Finding carrier appetite. Some insurers like straightforward owner-occupied homes. Others are more open to small commercial risks, unusual property types, or specialized vehicles.

- Helping when the claim is messy. Not every loss is a broken windshield or a simple roof issue. If a property loss involves contamination or hazardous conditions, outside specialists may become part of the claim process. In those cases, practical resources on understanding biohazard remediation claims can help property owners understand what to document and how cleanup work may intersect with insurance.

Practical rule: Buy insurance for the claim you hope never happens, not for the monthly payment you hope stays low.

The strongest agencies also translate insurance into normal language. They don't hide behind jargon. They tell you when a lower quote is lower for a reason. They tell you when your deductible changes the conversation. They tell you when your business has outgrown the policy you started with.

That's what people are really paying for. Not paperwork. Judgment.

Comparing Common Insurance Policies for Orlando Residents

Most Orlando households and small businesses don't need every policy on the market. They need the right mix. The easiest way to think about it is by matching the policy to the property, vehicle, or operation you're trying to protect.

Orlando Insurance Coverage at a Glance

| Coverage Type | What It Protects | Ideal For |

|---|---|---|

| Auto | Your vehicle, liability for accidents, and related driving exposures based on the policy terms | Daily commuters, families with multiple drivers, delivery or business owners who need to sort out vehicle use |

| Homeowners | The home structure, personal belongings, liability, and certain covered property losses | Owner-occupied homes, newly purchased houses, long-time Florida homeowners reviewing storm-related exposure |

| Commercial | Business liability, buildings, contents, operations, and business-owned vehicles depending on policy design | Retail shops, contractors, offices, restaurants, food trucks, and other local operators |

| Trucking | Commercial vehicle exposure tied to heavier use, cargo, operations, and driver activity depending on the account | Owner-operators, fleets, contractors hauling equipment, and businesses with road-heavy operations |

That table is the high-level view. The details are where Orlando buyers need to slow down.

Auto insurance looks straightforward until a household has a teen driver, a work truck, or a vehicle used for more than commuting. Homeowners insurance seems simple until you ask whether the home is primary, seasonal, rented, or partially occupied by others. Commercial coverage gets complicated fast because one business may need general liability, commercial auto, and workers' compensation all at once.

Where residents usually get tripped up

Auto coverage is often under-reviewed. People focus on premium, then forget to revisit limits after a move, a new job, or an added driver. In Orlando traffic, that can be a mistake. If your car is also part of your workday, the conversation needs to start there. Personal and business use aren't interchangeable.

Homeowners coverage causes the most confusion when buyers assume “covered” means every kind of property problem is automatically included. It doesn't. Ownership type, occupancy, property condition, and loss cause all matter. If you want a plain-English refresher on the basics, this piece on understanding homeowners insurance is a helpful companion read before you compare policy forms.

One issue I see overlooked too often is the small multi-family property. A lot of Orlando-area content talks only about single-family homes, but some residents own or want to insure a triplex or a small rental building. Direct carriers often reject those risks, while independent agencies can sometimes place them through markets built for that kind of property. That's a major difference in practice, because “non-standard” doesn't mean “uninsurable.”

If you own a property that doesn't fit the standard suburban template, don't assume the answer is no. It may just mean you're asking the wrong channel.

Commercial insurance is where one-size-fits-all breaks down fastest. A food truck, for example, isn't just a vehicle. It can involve liability, equipment, property, and business interruption concerns depending on the operation. The same goes for a contractor whose tools live in a truck, a retail tenant with inventory on site, or a small office with employees coming and going.

Trucking coverage deserves its own category because the exposure is different from ordinary commercial auto. More road time, heavier equipment, and operational demands create a different underwriting conversation. Buyers who try to squeeze trucking into a standard vehicle framework usually end up frustrated.

A practical approach is to group your risk by how you live and work:

- Personal life risks such as your home, condo, rental unit, or family vehicles

- Income-producing property risks such as a triplex, duplex, or small apartment building

- Business operation risks such as customer injuries, property damage, mobile operations, or employee-related exposure

- Vehicle-intensive business risks such as delivery, contracting, hauling, or trucking

The cleaner you are about those categories, the easier it is for an agency to put together coverage that makes sense.

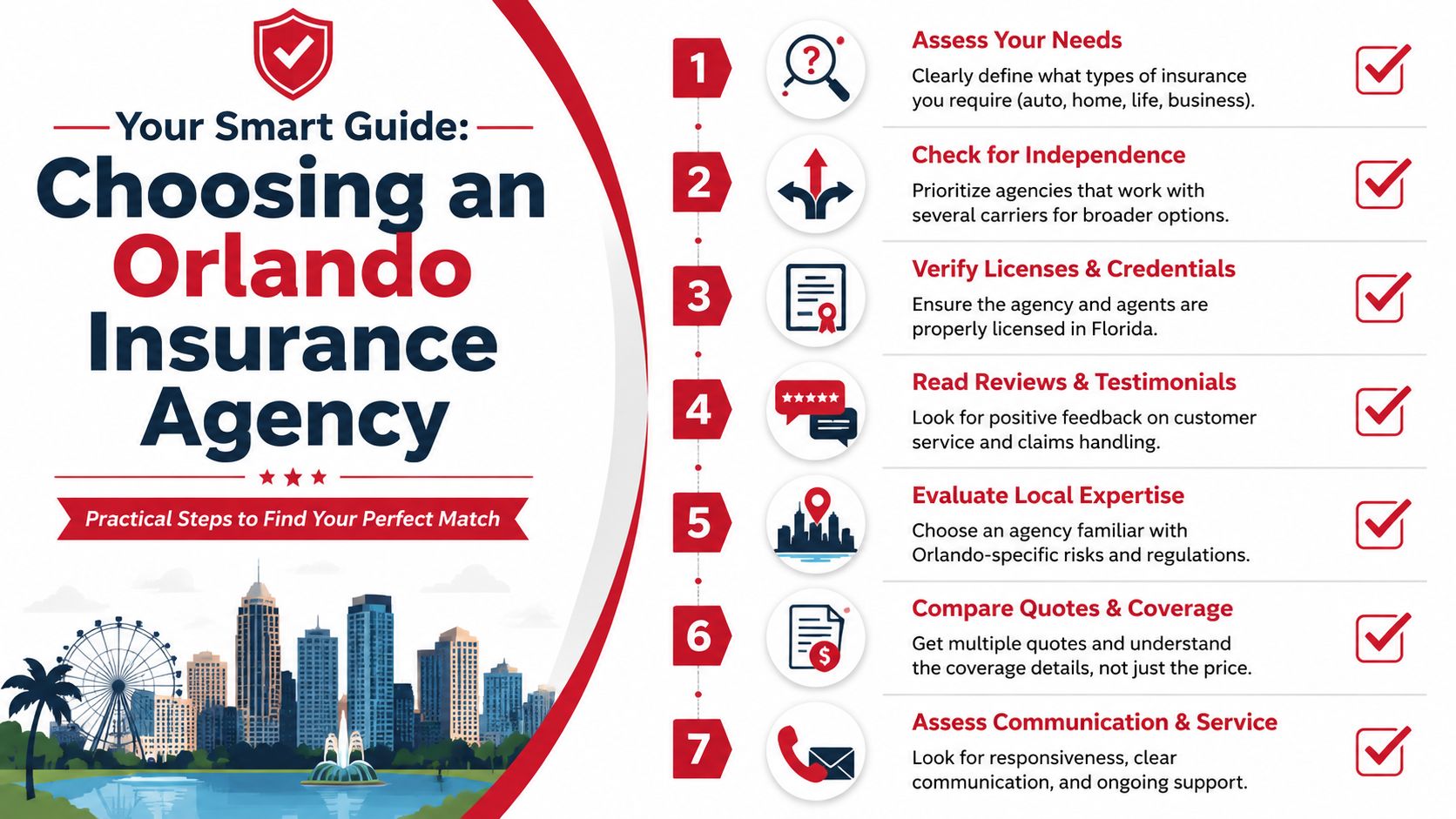

How to Choose the Right Orlando Insurance Agency

A lot of buyers ask the wrong opening question. They ask, “Who's cheapest?” A better question is, “Who's going to help me avoid a bad fit?” Price matters. Service, clarity, and follow-through matter more when something goes wrong.

Questions worth asking before you commit

Start with questions that reveal how the agency works, not just what it sells.

- How many carriers do you work with for my type of risk? You're trying to learn whether the agency has real market access for your situation or only a narrow lane.

- What details would make this policy ineligible or less appropriate? A good agent should be able to identify the facts that change the recommendation.

- How do you handle claims support? You want to know whether they just hand you a carrier phone number or stay involved when the issue gets complicated.

- Can you help with unusual properties or operations? This matters if you own a multi-family rental, run a mobile business, or use vehicles in a way that goes beyond ordinary personal driving.

- How do you communicate after the sale? Some agencies are responsive when quoting and difficult to reach once the policy is bound.

There's one question consumers ask all the time and local agency content often avoids: what do you do if your agency won't answer you? The Patient Advocate Foundation notes that 60 percent of consumers struggle to get timely answers from insurers and may need assertive follow-up, reference tracking, supervisor requests, and contact with advocacy offices, according to its guidance on what to do when you can't get answers from your insurance company.

That matters because responsiveness isn't a soft skill in insurance. It's part of the product.

Red flags that should slow you down

Some warning signs show up before you buy.

One is vague answers. If you ask whether a policy fits a triplex, business vehicle, or food truck and the response stays fuzzy, that's a problem. Complex risks need direct answers.

Another is pressure to bind quickly without a real review. Fast isn't always efficient. Sometimes it just means important facts are being skipped.

A third is poor documentation habits. If nobody encourages you to save emails, note reference numbers, or confirm changes in writing, you're being trained into a future headache.

Keep a simple claim and service paper trail. Dates, names, reference numbers, and summary notes save time when a conversation has to be escalated.

Watch for these practical issues too:

- Sales-first language. If every answer circles back to monthly payment and never to exclusions, deductibles, or use restrictions, you're not getting full guidance.

- No appetite for exceptions. Some agencies do fine with standard accounts but stumble the moment your property or business is even slightly outside the box.

- Inconsistent follow-up. If calls and messages already drift into silence during quoting, don't expect smoother communication during a claim.

- Unclear service boundaries. You should know who handles changes, billing questions, certificates, and claim check-ins.

The right Orlando insurance agency doesn't need to promise perfection. It needs to be reachable, candid, and competent when the details matter.

Why Select Insurance Group is a Trusted Local Choice

For Orlando buyers who want an independent option, Select Insurance Group, Inc. is one agency operating in this space. According to its BBB business profile, the company was founded in 2002, claims 30+ years of industry experience, operates across seven Southeastern states, and has bilingual specialists who provide free, no-obligation quotes across personal and commercial lines by comparing 20 to 40 carriers.

That combination matters because it lines up with what local shoppers usually ask for. They want choices, not a single preset answer. They want someone who can talk through both family coverage and business coverage. They want a process that doesn't become harder just because the risk is less standard.

What local buyers usually want from an agency

In day-to-day practice, people usually care about four things.

First, they want range. If a standard home, auto, or commercial quote isn't the right fit, they don't want the conversation to stop there.

Second, they want clarity. Bilingual service helps in a market as diverse as Orlando because coverage decisions are too important to leave half-understood.

Third, they want speed with context. Fast quotes are useful only when someone also explains what's inside them.

Fourth, they want one place for multiple needs. A household may need auto, renters, and homeowners coverage. A small business may need liability, workers' compensation, and commercial auto. The more moving pieces there are, the more useful a coordinated agency relationship becomes.

Why that matters in day-to-day service

A local office should make routine insurance tasks easier, not heavier. That includes getting documents over quickly, updating policies when life changes, and helping clients sort out whether a new purchase, rental arrangement, or vehicle use changes the type of protection they need.

The Orlando market rewards practical agencies. The buyers who do best aren't the ones who chase the lowest number on day one. They're the ones who find a team that can handle normal coverage, tougher edge cases, and ongoing service without making everything feel like a battle.

Get Protected Today with a Free No-Obligation Quote

Insurance gets easier once you stop treating it like a commodity. In Orlando, the right fit depends on how you drive, where you live, what you own, and whether your work creates exposures a basic policy won't touch.

That's why an independent agency approach works so well for so many residents here. It gives you room to compare options, ask better questions, and line up coverage with real life instead of a generic profile.

If you're ready to sort out auto, home, renters, commercial, or trucking coverage, the next step doesn't need to be complicated. Start with a free no-obligation quote request and bring the details that matter most: how the property is used, how the vehicle is used, who needs to be covered, and what worries you most if a claim happens.

Good insurance advice should leave you feeling clearer than when you started. That's the standard to look for.

If you want straightforward help reviewing your current coverage or comparing new options, reach out to Select Insurance Group, Inc.. An independent agency can help you sort through personal and commercial choices, identify gaps, and get a free, no-obligation quote without turning the process into a guessing game.