Cheap car insurance in Florida sounds simple until you look at the numbers. Florida is the third-most-expensive state for full-coverage auto insurance, with average monthly costs of $311 versus the national average of $186, and quoted rates in the state saw a 15% jump in 2023, the largest increase in the country, according to ValuePenguin's average car insurance cost analysis.

If you're frustrated, you're not overreacting. You're shopping in one of the toughest auto insurance markets in the country. The good news is that high prices don't mean you have to accept the first quote you get. The right strategy can still uncover meaningful savings, especially if you understand where Florida premiums come from and which levers move the price.

Table of Contents

- Why Finding Cheap Car Insurance in Florida Feels Impossible

- Decoding Florida's Unique Auto Insurance Requirements

- The Smart Way to Compare Car Insurance Quotes in Florida

- Unlocking Every Available Discount and Telematics Savings

- How to Adjust Coverage and Deductibles for Optimal Savings

- The Most Common and Costly Insurance Mistakes to Avoid

Why Finding Cheap Car Insurance in Florida Feels Impossible

Florida drivers aren't imagining things. Rates are high because the state has structural cost problems, not just individual driver problems.

A lot of online advice treats auto insurance like a coupon hunt. Ask for discounts. Raise your deductible. Shop around. Those steps can help, but in Florida they don't explain why even careful drivers with solid records still get hit with painful premiums. The bigger issue is that carriers price in the state's litigation pressure, high claim activity, and inefficient claim handling costs.

That matters because many shoppers blame themselves for a quote that was expensive before their application was even reviewed.

The problem starts above the driver level

Florida's insurance affordability strain has been tied to a long-running pattern of claim abuse and legal system pressure. The state also carries unusually high claim-related costs that get baked into premiums across the board. In plain English, many drivers are paying for a market problem, not just their own risk profile.

Practical rule: In Florida, the cheapest policy isn't just about discounts. It's about finding a carrier whose pricing model is less exposed to the state's worst cost drivers.

That's why a quote can feel unreasonable even if your car is modest, your mileage is normal, and your record is clean. Some insurers absorb state-level cost drag better than others. Some don't.

If you want a useful legal and consumer-side breakdown of rising premiums, injury claims, and practical ways to respond, this guide on how to save on Florida auto insurance is worth reading alongside your quote search.

What actually works

Drivers usually save the most when they stop shopping by brand familiarity and start shopping by carrier fit. Florida isn't a state where broad, one-size-fits-all advice works well.

A smarter approach looks like this:

- Check the market, not one insurer: A single company can only show you its own rate.

- Look past the sticker price: A low initial premium can hide weaker protection or a pricing model that's more volatile after a claim.

- Match the policy to the actual risk: Florida drivers need to think about uninsured motorists, claim trends, and repair costs, not just minimum legal compliance.

Cheap car insurance in Florida is usually found by navigating the market's inefficiencies, not by pretending those inefficiencies don't exist.

That's the mindset that makes the rest of the search easier. Once you understand why the market is expensive, you can start avoiding the parts of it that hurt you most.

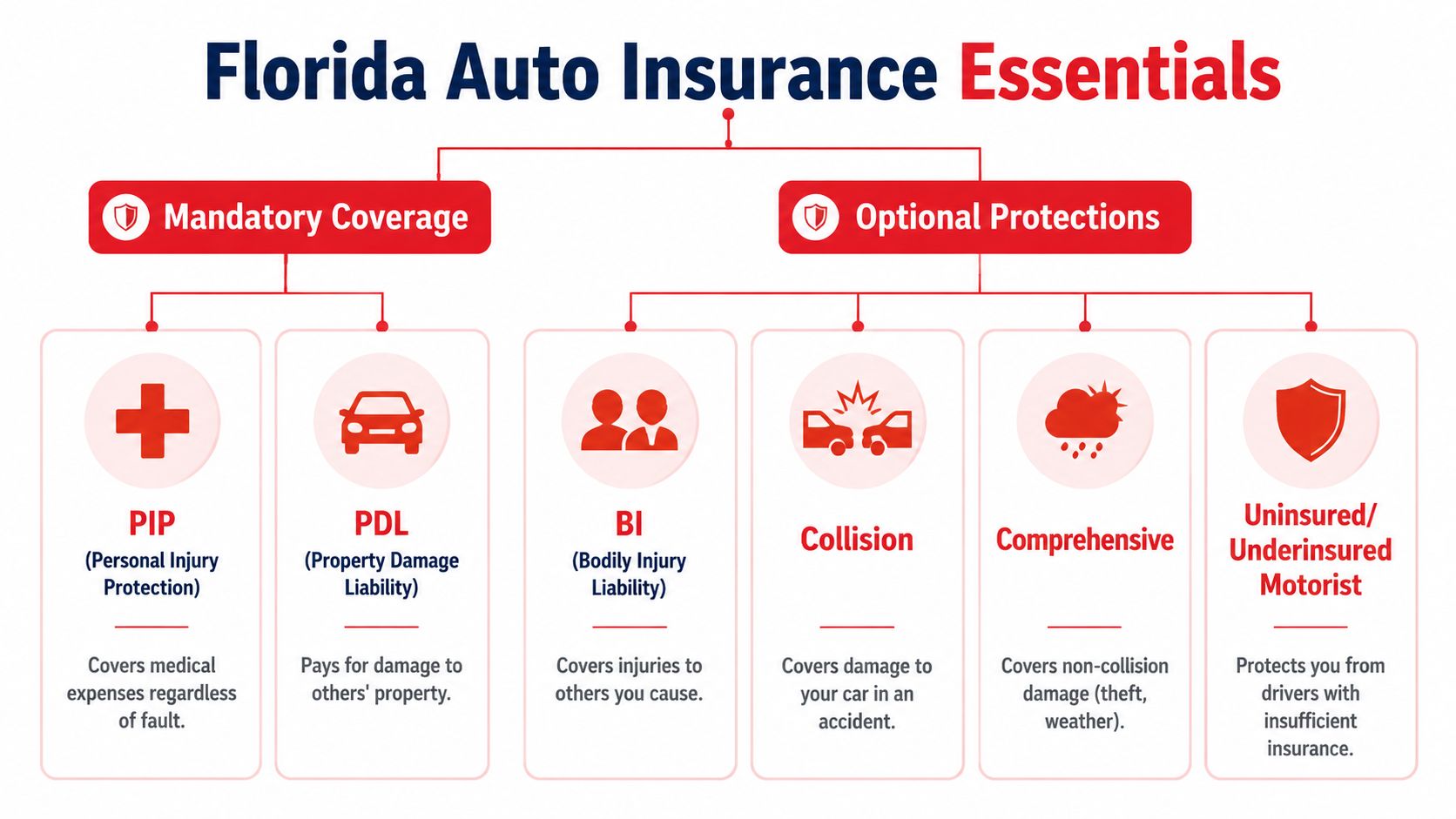

Decoding Florida's Unique Auto Insurance Requirements

Florida's rules shape your premium before discounts even enter the picture. If you don't understand the state's setup, it's easy to buy a policy that looks cheap but leaves major holes.

What Florida requires before you can legally drive

Florida uses a no-fault structure, which is why Personal Injury Protection, or PIP, plays such a central role in every policy discussion. The state historically requires $10,000 in PIP. Florida drivers also need property damage liability coverage to legally operate a vehicle.

Florida's minimum coverage environment is unusually expensive. Verified market analysis states that Florida has a 121% premium gap over the national average for minimum coverage, driven by aggressive litigation conditions and a high uninsured motorist burden. That means even bare-bones legal coverage often costs more here than many drivers expect.

For a clearer breakdown of the state's legal minimums and how they apply in practice, this Florida minimum auto insurance guide is a useful reference.

Why the legal minimum can still leave you exposed

Legal minimum doesn't mean financially safe. It only means you met the state's floor.

The bigger issue in Florida is what happens after a crash. Medical billing disputes, treatment questions, and injury-related claim complexity can all feed higher system costs. If you've ever wondered why treatment-related claims can become such a large part of the insurance equation, this plain-language article on chiropractic insurance coverage gives helpful context on how post-accident care and coverage questions can intersect.

Here's the practical way to think about Florida coverage choices:

- PIP handles your own injury expenses up to the policy structure: It's required, but it doesn't solve every loss scenario.

- Property damage liability protects against damage you cause to someone else's property: That's mandatory too, but it doesn't repair your own car.

- Bodily injury liability can matter even when it isn't the first thing shoppers ask about: If you seriously injure someone, low limits can create personal financial risk.

- Uninsured and underinsured motorist coverage deserves serious attention: In a state known for uninsured driver problems, this can be one of the most valuable protections on the policy.

A Florida policy should be judged by what it protects after a bad day, not just by what it costs on quote day.

Many people searching for cheap car insurance in Florida focus so hard on getting legal that they forget to get usable protection. That's where expensive surprises begin.

The Smart Way to Compare Car Insurance Quotes in Florida

Most Florida drivers don't need more quotes. They need better quote comparisons.

Calling carriers one by one is slow, and it rarely produces a clean apples-to-apples result. Coverage changes from quote to quote, deductibles drift, optional protections appear or disappear, and the shopper ends up comparing prices that don't match.

Start with the coverage type, not the company name

Before you compare rates, decide what kind of policy you're shopping for. Liability-only and full coverage serve different jobs.

If your vehicle is older, paid off, and low in market value, liability-only may be worth considering. If the car still has meaningful value or you'd struggle to replace it out of pocket, full coverage often makes more sense. The key is matching protection to the car's real-world replacement risk.

Current verified pricing shows how wide the difference can be. In 2026, Florida's average full-coverage cost is $235 per month, while one available full-coverage rate cited by Insurify is $129 per month, which means the gap between average and lower-priced options can exceed $1,200 annually, according to Insurify's Florida cheap car insurance data.

That spread is exactly why comparison matters.

Why independent quote comparison works better

An independent agent can line up multiple carriers using the same driver profile and coverage target. That removes a lot of the confusion that causes people to choose the wrong policy for the wrong reason.

Here's the practical difference:

| Approach | What usually happens |

|---|---|

| Direct shopping | You get one company's appetite, one company's underwriting, and one company's price logic |

| Independent comparison | You see multiple carrier options built around the same coverage request |

That second approach matters in Florida because pricing swings are often tied to carrier-specific exposure, not just your individual record.

If you're changing policies, this guide on how to switch auto insurance companies covers the timing issues that matter, especially avoiding cancellation gaps.

One practical option is Select Insurance Group, Inc., an independent agency that compares quotes across multiple carriers rather than offering only one in-house policy. That's often the more efficient route when you're trying to find cheap car insurance in Florida without spending hours repeating the same information.

Don't ask only, "Who is cheapest?" Ask, "Who is cheapest for my exact coverage setup, in my ZIP code, with my driving history?"

That's how experienced buyers shop in a difficult market.

Unlocking Every Available Discount and Telematics Savings

After you find a solid base quote, the next job is squeezing every legitimate discount out of it. Many drivers often leave money on the table.

Insurers don't always apply every available discount automatically. Some require proof. Some depend on the way the policy is written. Some are only available with certain combinations of coverage or billing choices.

Discounts drivers miss because they never ask

The basics still matter, but they need to be checked deliberately.

Use this checklist when reviewing any quote:

- Multi-policy savings: If you also insure a home, condo, or renters policy, ask whether bundling changes the auto rate.

- Safe-driver programs: A clean record can help, but some carriers require specific program enrollment or policy formatting to reflect it.

- Good student eligibility: Households with younger drivers often forget to ask.

- Low-mileage consideration: This can matter if your commute changed or you work from home more often.

- Vehicle equipment credits: Anti-theft devices and safety features may qualify.

- Paid-in-full option: Sometimes the total premium improves when installment fees are removed.

- Defensive driving course credit: Especially useful for some mature drivers and households trying to offset a recent rate increase.

The important point isn't the list. It's that each carrier treats the list differently.

Why telematics matters more in Florida

Usage-based insurance, often called telematics, has become one of the few tools that can directly reward actual driving behavior instead of relying only on broad risk categories. In a high-cost state, that matters.

Verified market guidance indicates that usage-based programs are one of the few mechanisms shown to significantly reduce the loss-adjustment expense component by lowering claim frequency. That's industry language, but the practical takeaway is simple. If you drive smoothly, avoid hard braking, keep reasonable hours, and don't rack up risky mileage patterns, telematics can improve your odds of getting a better overall rate.

A few rules help decide if it's worth trying:

- Good fit: Predictable driving habits, lower annual mileage, calm braking and acceleration.

- Bad fit: Late-night driving, frequent stop-and-go rush traffic, or lots of short trips in dense areas.

- Worth reviewing: Families with teen drivers who want a behavior-based path to rate relief.

Discounts tied to paperwork are nice. Discounts tied to your actual driving can be more powerful if your habits are strong.

For many Florida households, telematics isn't just another discount. It's one of the more credible ways to separate yourself from the state's broader risk pool.

How to Adjust Coverage and Deductibles for Optimal Savings

Once the quote is in the right ballpark, the final tuning happens inside the policy itself. Here, shoppers can lower cost without gutting protection, if they make measured choices.

When a higher deductible makes sense

A deductible is your share of the loss before the insurer pays on certain claims. As a rule, a higher deductible lowers the premium because you're agreeing to keep more risk in your own pocket.

That trade-off only works if you could afford the deductible tomorrow. Not in theory. In cash.

A practical test is simple:

- Good candidate for a higher deductible: You have emergency savings and wouldn't need to borrow to cover a claim.

- Poor candidate: A single repair bill would force you onto a credit card or leave the car parked.

The mistake I see most often is drivers choosing a deductible based only on the monthly savings, then regretting it at claim time.

When dropping physical damage coverage is reasonable

Collision and non-collision coverage protect your own vehicle. They can be worth keeping on many cars, but not every car.

If the vehicle is older, paid off, and worth relatively little, there comes a point where paying for physical damage coverage may not make financial sense. On the other hand, if replacing the car would be difficult, dropping those coverages just to trim the premium can create a much larger problem later.

Use this decision lens:

| Vehicle situation | Coverage thought process |

|---|---|

| Newer car with meaningful value | Keeping collision and comprehensive is usually easier to justify |

| Older car with low value | Review whether the premium still makes sense relative to what the car is worth |

| Car you depend on daily and can't replace easily | Cheap coverage can become expensive if one loss leaves you without transportation |

This is also where Florida drivers should be careful not to overreact to high premiums by stripping away too much. Cheap car insurance in Florida should still leave you with a policy you can live with after an accident, theft, storm loss, or hit-and-run.

The right deductible and coverage mix is rarely the absolute cheapest version of the policy. It's the version that lowers cost while keeping the risk at a level your budget can survive.

The Most Common and Costly Insurance Mistakes to Avoid

The biggest mistake Florida drivers make is assuming the lowest upfront premium is the lowest long-term cost. In this state, that's often wrong.

The cheapest price on day one can cost more later

Minimum coverage gets marketed as the fast answer to high premiums. Sometimes it's appropriate. Many times, it isn't.

One reason is Florida's uninsured driver problem. Verified data tied to Florida cheap-policy shopping notes that the state's uninsured driver rate is 27%, and drivers with cheap minimum policies can see premiums spike 40% to 60% after an incident. That's a brutal surprise for people who thought they were saving money by buying as little coverage as possible.

The issue isn't just the first accident. It's what happens after. Thin coverage leaves less room for the policy to absorb a serious event, and the rate consequences can be ugly.

Cheap on the declarations page doesn't always mean cheap over the life of the policy.

Other mistakes that quietly raise your premium

Some problems don't start with a crash. They start with avoidable policy errors.

- Letting coverage lapse: Even a short gap can hurt your options and pricing.

- Failing to update your policy: A move, a commute change, a new driver in the house, or a different garaging address all matter.

- Ignoring ticket impact: If you've had violations, review how long they may affect pricing with this guide on how long traffic tickets affect insurance.

- Assuming every violation affects insurance the same way: Major offenses can create very different consequences. If that's relevant to your situation, this article on understanding DUI insurance effects gives helpful legal and insurance context.

- Shopping alone and comparing mismatched quotes: This is one of the fastest ways to buy a weak policy that only looked cheap because coverages changed.

A smarter approach is to protect continuity, review your policy after life changes, and treat minimum coverage with caution rather than as a default answer.

If you're trying to find cheap car insurance in Florida without cutting the policy down to the bone, Select Insurance Group, Inc. can help you compare multiple carrier options, review coverage trade-offs, and look for savings that fit your actual driving and budget.