A lot of business owners in the Southeast start shopping for insurance after something changes. A new truck goes into service. A landlord asks for higher liability limits. A storm watch pops up. Payroll grows faster than expected. Then you pull out the current policy and realize it was built for the business you had a year ago, not the one you're running now.

That gap is where expensive mistakes happen. A contractor in Georgia may need equipment coverage that moves with the crew. A restaurant in coastal South Carolina may need to think harder about water exposure than the same business inland. A trucking company running rural routes in Alabama faces a different pricing conversation than a fleet staying near metro corridors.

If you're looking for commercial insurance in the Southeast, the goal isn't just getting a certificate fast. It's getting coverage that matches how your business operates, where it operates, and what would hurt you most if a claim hit tomorrow.

Table of Contents

- Why Your Southeast Business Needs Region-Specific Insurance

- The Core Four Commercial Coverages for Southeast Businesses

- State by State Insurance Rules and Cost Factors

- Risk Guidance for Top Southeast Industries

- How to Compare Quotes and Purchase Your Policy

- The Value of a Local Agency and Bilingual Service

- Common Insurance Pitfalls and Top Questions Answered

Why Your Southeast Business Needs Region-Specific Insurance

A generic commercial policy can look fine until a real-world problem tests it. That happens all the time in the Southeast. A business owner buys a basic package, checks the box for liability, then finds out later that growth, weather exposure, vehicle use, or subcontractor work changed the risk far more than expected.

That matters because this isn't a slow, flat market. The Southeast has emerged as the fastest-growing market for commercial insurance, projected to grow at a CAGR of 11.55% from 2026 to 2035, driven by the region's expanding small business base, according to regional commercial insurance market projections. More businesses, more construction, more transportation, and more property exposure means a one-size-fits-all policy usually falls short.

Practical rule: If your business location, payroll, vehicles, or property changed, your insurance needs changed too.

A few examples make this plain:

- A Florida service company may carry tools, inventory, and electronics between sites. Standard property coverage written too narrowly may leave off-premises items exposed.

- A Georgia contractor may pick the cheapest liability policy, then lose a job because the certificate doesn't meet contract requirements.

- A South Carolina retailer may insure the building contents but miss a key water-related coverage issue.

- A North Carolina trucking operation may add drivers quickly and not update underwriting details until renewal.

Recovery planning matters just as much as buying coverage. If you haven't built one yet, this small business disaster recovery guide is worth reviewing because insurance works best when it's paired with a real continuity plan.

Regional insurance works when it reflects local weather, local contracts, local state rules, and the way Southeast businesses grow. That's the difference between a policy that looks adequate and one that holds up under pressure.

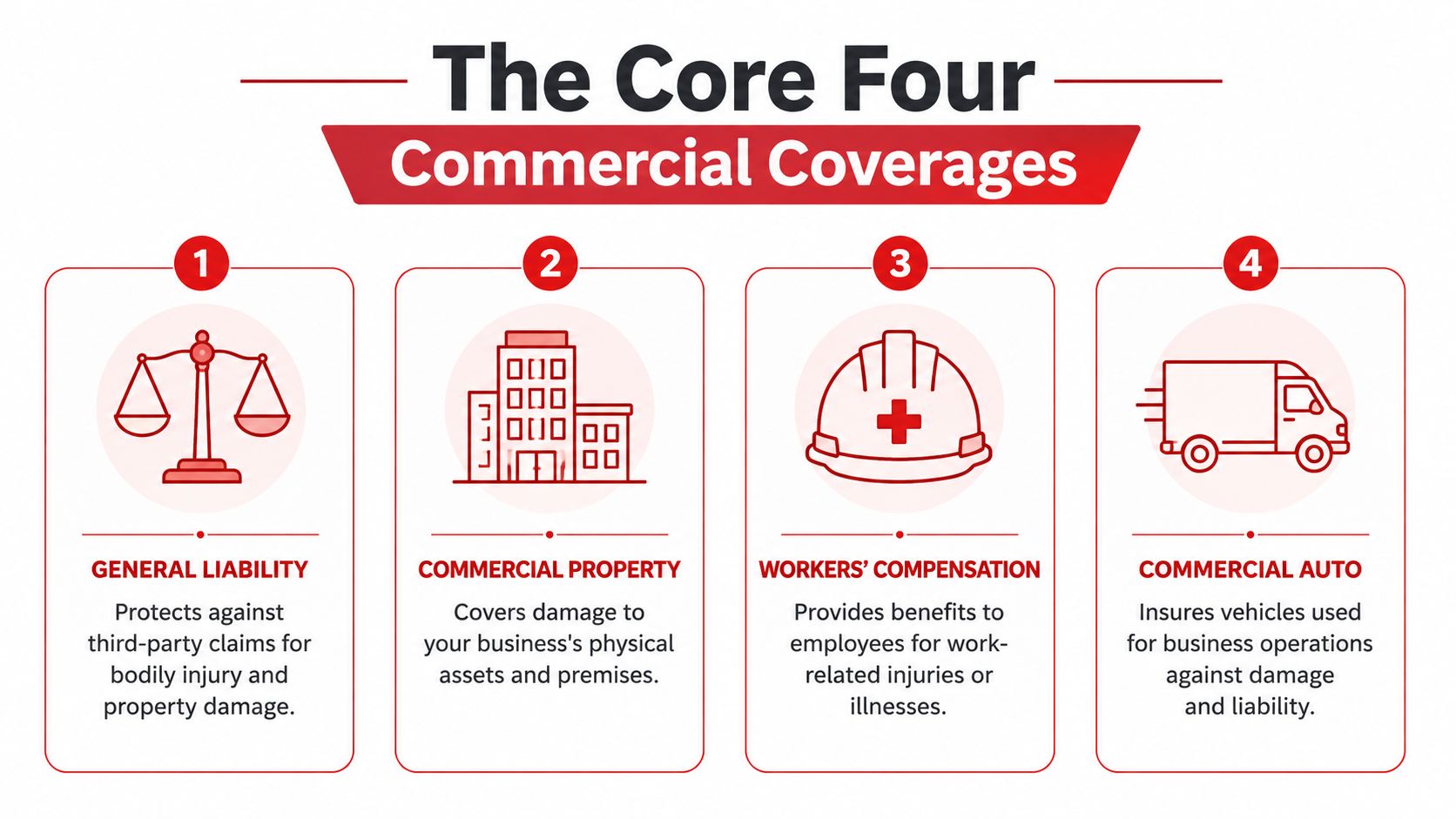

The Core Four Commercial Coverages for Southeast Businesses

Most Southeast businesses need four coverages at the center of the program. Everything else gets built around them.

General liability

Think of general liability as the shield between your business and third-party claims. If a customer slips, you damage someone else's property, or your work leads to a claim for bodily injury or property damage, this policy is usually the first line of defense.

For Southeast businesses, this coverage matters because many owners work in person, on-site, and under contract. Outdoor service providers, electricians, janitorial firms, and retailers all create day-to-day liability exposure by serving the public.

What works:

- Matching limits to your contracts: A policy that satisfies lease or job requirements avoids last-minute scrambling.

- Checking additional insured needs: Many jobs and landlords require it.

- Reviewing exclusions carefully: Cheap coverage can become expensive if the work you perform isn't clearly contemplated.

What doesn't work:

- Buying on price alone

- Assuming all liability forms are the same

- Ignoring certificates until the day a client asks for one

Commercial property

Commercial property insurance protects the physical side of the business. That can include the building, furniture, equipment, inventory, signage, and other business property.

In the Southeast, property coverage needs extra attention because location changes the exposure. A coastal business, an inland warehouse, and a mixed-use retail space don't present the same risk profile. In markets like Florida and the Carolinas, insurers using dynamic flood exposure data can reduce underwriting uncertainty by 15% to 20% and have lowered claim loss ratios by 12% over five years, according to the NAIC property and casualty market share report reference. For business owners, that means better risk classification and more accurate pricing when the property data is current.

A property policy should follow the real property exposure, not just the mailing address.

A few practical checks help:

- Building limit: Does it reflect current rebuild realities if you own the structure?

- Business personal property: Does it cover tools, stock, computers, and tenant improvements?

- Water and flood questions: Don't assume “water damage” means every kind of water loss is covered.

- Business interruption: If operations stop after a covered loss, how long could you survive?

Workers compensation

Workers compensation pays benefits for work-related injuries or illnesses. If you have employees, this is one of the most important policies on the board.

It protects your team, and it protects the business from the financial shock of workplace injury claims. For construction, hospitality, manufacturing, transportation, and service businesses across the Southeast, workers comp is often one of the first policies that becomes mandatory as the company grows.

Good workers comp planning includes:

- Accurate payroll estimates

- Correct class codes

- Timely reporting when roles change

- Reviewing subcontractor relationships carefully

Misclassified payroll is a common problem. Owners try to keep premiums low at the start, then get surprised at audit time.

Commercial auto and trucking

If a vehicle is used for business, personal auto coverage usually isn't enough. Commercial auto covers vehicles used in operations, and trucking programs go further with the endorsements and liability structures fleets often need.

This is especially important in the Southeast because so many businesses rely on pickups, vans, delivery units, and heavier commercial vehicles. A contractor with two trucks, a food distributor, and an owner-operator all have different exposures even if the vehicles look similar on paper.

Focus on:

- Who drives the vehicles

- What they carry

- How far they travel

- Whether they cross state lines

- Whether employees ever use personal vehicles for business

Commercial insurance in the Southeast works best when these four coverages are built together instead of bought one at a time with gaps between them.

State by State Insurance Rules and Cost Factors

The Southeast isn't one insurance market in practice. It's a group of states with different rules, filing systems, business mixes, and pricing pressure points. That's one reason commercial insurance here keeps growing. The Southeast commercial insurance market is projected to reach USD 416.83 billion by 2035, and the region's favorable regulatory frameworks have attracted over 35% of total U.S. commercial insurance market share in recent years, based on Southeast commercial insurance market outlook data.

What changes from one state to the next

A business owner usually feels state differences in four places first:

- Workers compensation requirements

- Commercial auto minimums and filing needs

- Construction-related rules

- Property underwriting appetite

Florida often creates harder conversations around property exposure and contractor operations. Georgia business owners frequently run into contract insurance requirements faster than they expect. North Carolina and South Carolina owners often discover that location, building details, and work classification affect pricing more than the business name or industry label alone. Tennessee and Alabama businesses, especially those with vehicles and crews, need to watch payroll, driver information, and territory closely.

If your company operates in Florida, it helps to review a more detailed breakdown of Florida commercial insurance considerations before you shop.

State rules don't just affect compliance. They affect how carriers underwrite, what they ask for, and how quickly a quote moves.

A simple workers compensation snapshot

Employee thresholds vary by state, and the exact rule can depend on business type. Construction can be treated differently from office operations, and owner exemptions may exist in some places. That's why a quick screening call matters before you bind coverage.

| State | Employee Threshold for Mandatory Coverage |

|---|---|

| Florida | Varies by business type |

| Georgia | Varies by business type |

| North Carolina | Varies by business type |

| South Carolina | Varies by business type |

| Tennessee | Varies by business type |

| Alabama | Varies by business type |

What usually drives cost in these states?

Florida

Property exposure, storm sensitivity, and construction details often move the conversation quickly. Vehicle-heavy businesses also need clean driver lists and accurate garaging information.

Georgia

Fast-growing contractors and service businesses often need stronger certificate support, higher limits, and careful job classification.

North Carolina

Rate structure and underwriting review can feel more formal than owners expect. Good documentation helps.

South Carolina

Hospitality, retail, and contractor risks often depend heavily on premises details and payroll accuracy.

Tennessee

Fleet use, driver quality, and territory matter for many small businesses with field operations.

Alabama

Rural and regional driving patterns can affect vehicle underwriting more than owners expect.

The practical takeaway is simple. Don't shop commercial insurance in the Southeast as if every state uses the same playbook. They don't.

Risk Guidance for Top Southeast Industries

The easiest way to understand coverage is to look at the jobs that create the claims. In the Southeast, three groups ask the most practical questions. Contractors. Truckers and fleets. Main Street businesses.

Contractors

A small contractor can look well insured on the certificate and still have weak spots. That happens when the owner buys liability and skips the coverages that follow tools, equipment, or completed work exposure.

A common Southeast example is the lawn care or small trade contractor who keeps equipment in trailers, on trucks, or at changing job sites. If you work in that kind of business, this overview on lawn care liability insurance issues highlights the kinds of exposures owners often overlook.

What usually matters most:

- General liability: For third-party injury and property damage claims

- Workers compensation: For crew injuries

- Commercial auto: For trucks and trailers used in the business

- Equipment-related property coverage: For tools and mobile gear that don't stay in one place

What doesn't work is assuming shop coverage protects property everywhere. If the equipment moves, the insurance needs to reflect that.

Truckers and fleets

Truckers usually know their vehicles are expensive to insure. What frustrates them is not understanding why one route, one driver change, or one garaging detail swings the quote.

In Georgia, Alabama, and Tennessee, insurers using standardized telematics data schemas have reduced claim processing times by 25% and improved loss ratio accuracy by 14%, according to commercial auto data analytics benchmarks. In plain English, cleaner vehicle and driver data can lead to faster claim handling and more precise pricing.

That doesn't mean every trucker gets a lower premium. It means better information leads to fairer underwriting.

A fleet quote is only as good as the schedule behind it. Wrong VINs, missing driver details, and vague route descriptions lead to bad pricing.

Truckers should pay close attention to:

- Radius of operation

- Urban versus rural routes

- Driver experience

- Cargo type

- Trailer use

- Downtime after a loss

Main Street businesses

Retailers, restaurants, offices, salons, and small wholesalers usually need a different mindset. Their biggest risk often isn't one dramatic claim. It's a combination of smaller hits. A slip-and-fall claim, a kitchen equipment loss, a water issue, or a short shutdown can all hurt cash flow fast.

For these businesses, the strongest setup is often built around:

- Liability for customer-facing risk

- Property coverage for contents and improvements

- Workers compensation if they have employees

- Business interruption protection when operations depend on daily revenue

A small family business in a rural town and one in a busy urban corridor may sell the same product, but they won't always face the same insurance pressure. Delivery exposure, foot traffic, landlord requirements, and staffing all change the picture.

Commercial insurance in the Southeast works best when the policy follows the trade. Contractors need mobility built in. Truckers need route clarity and driver discipline. Main Street businesses need income protection as much as building and contents protection.

How to Compare Quotes and Purchase Your Policy

Shopping for business insurance goes smoother when you do two things first. Gather clean information and compare forms line by line. Most quote problems come from missing details, not from a lack of options.

Get your information ready first

Before you request quotes, pull together the basics:

- Business details: Legal name, address, entity type, years in business

- Operations summary: What you do, where you do it, and whether work is residential, commercial, or both

- Payroll and staffing: Estimated payroll, employee roles, subcontractor use

- Property information: Building details, occupancy, security features, inventory or equipment values

- Vehicle information: VINs, driver list, garaging, radius, and use

- Loss history: Prior claims matter, and leaving them out creates delays later

If you're buying remotely, many agencies now bind coverage through secure uploads and e-signatures. If you haven't used them before, this guide to electronically signing documents gives a straightforward overview of how the process works.

Compare the quote details, not just the price

A good comparison checks more than premium. You want to know whether each quote is solving the same problem.

Review these items side by side:

- Coverage form: Are the policies comparable?

- Limits: One quote may look cheaper because the limits are lower.

- Deductibles: Higher deductibles can hide real out-of-pocket risk.

- Exclusions: Cheap policies often disappoint here.

- Endorsements: Added language can expand or restrict coverage in important ways.

- Certificates and compliance needs: If your landlord or client requires something specific, make sure the quote includes it.

Ask one question on every quote: “What claim would this policy not cover that I might assume it covers?”

A practical buying process looks like this:

- Start with your biggest risk: Property, payroll, vehicles, or contracts

- Request comparable limits: Don't compare apples to oranges

- Clarify operational details early: Especially for trucks, crews, and multi-location businesses

- Read the proposal summary carefully: Don't skip the exclusions page

- Bind only after documents match reality: Names, addresses, vehicles, payroll, and locations must be correct

The right quote is the one that fits the business you run today, not the one that only looks cheapest on the first page.

The Value of a Local Agency and Bilingual Service

A local agency earns its value when something is unusual. A claim happens on a weekend. A certificate needs to be revised before a job starts. A policy audit shows payroll was estimated wrong. That's when local knowledge matters more than a generic call center script.

Why local service matters

In the Southeast, local service helps because business conditions vary block by block and county by county. A local agent usually understands the difference between inland and coastal property questions, urban and rural vehicle use, and the contract habits of local landlords and general contractors.

That matters in practical ways:

- Faster correction of bad classifications

- Better preparation for audits

- Cleaner certificate handling

- Clearer conversations around local exposure

If you've ever wondered why an independent agency approach helps with that, this explanation of what an independent insurance agency does is a useful starting point.

Why bilingual support changes the outcome

Language issues in insurance aren't minor. They create missed expectations. A business owner may think a policy includes one thing, while the actual form says something narrower.

Data indicates that 38% of Hispanic small business owners in the Southeast report significant difficulties understanding policy terms due to language barriers, according to research on language barriers for Hispanic business owners. That's a serious problem because many small businesses need quick decisions on certificates, payroll reporting, and coverage changes.

A bilingual-friendly process helps owners:

- Ask better questions before binding

- Understand exclusions before a claim

- Compare multiple quotes more confidently

- Avoid paying for the wrong coverage

The best insurance conversation is the one the owner fully understands. That isn't a luxury. It's part of reducing risk.

Common Insurance Pitfalls and Top Questions Answered

Business owners rarely make insurance mistakes because they don't care. Usually they're moving fast, juggling payroll, jobs, vehicles, and leases, and the policy gets treated like paperwork. That's where trouble starts.

Common mistakes

- Choosing the lowest premium without reading exclusions: A cheap policy can leave out the exact loss you're most likely to face.

- Forgetting to update the policy after growth: New employees, vehicles, locations, or services should trigger a review.

- Using personal auto coverage for business driving: If the vehicle is used in the business, ask the question directly and get a clear answer.

- Understating payroll or operations: That can create audit problems and claim friction later.

Some agencies and back-office teams improve service speed by tightening document handling and support workflows. For owners curious about the operations side, this overview of insurance process outsourcing benefits gives useful context on why response times and policy administration can vary.

Quick answers to real questions

Why are rural trucking routes sometimes priced higher than expected?

Because carriers often see route type, road conditions, claim patterns, and service territory as separate risk factors. In 2025, 45% of small trucking firms in the Southeast discontinued rural operations due to unexplained rate hikes, according to reporting on rural route insurance pressure. That tells you the transparency problem is real, and it's one reason truckers should ask for a plain-language explanation of route assumptions before binding.

Can one policy cover every part of my business?

Usually no. Some businesses can package major coverages efficiently, but vehicles, workers comp, property, and specialized liability often need separate attention.

When should I review my policy?

At renewal, of course. But also when you add vehicles, hire staff, sign a new lease, expand territory, buy equipment, or change operations.

What's the best way to save money without cutting corners?

Keep business information accurate, report changes early, improve risk controls, and compare quotes on equal terms. Saving money usually comes from better matching, not just lower limits.

If you want help sorting through commercial coverage options in Alabama, Florida, Georgia, North Carolina, South Carolina, Tennessee, or Virginia, Select Insurance Group, Inc. can help you compare options across multiple carriers and find coverage that fits how your business really operates.