A lot of Tampa Bay homeowners start thinking seriously about windstorm coverage the same way. You open a weather app, see a storm spinning in the Gulf, and suddenly your house feels less like an address and more like a financial responsibility. The roof, the windows, the screened enclosure, the mortgage, the question of what your policy covers. It all gets very real, very fast.

That moment is exactly why windstorm insurance for Tampa Bay properties deserves attention before a storm watch goes up. Along the Gulf Coast, people don't buy this coverage because it's abstract. They buy it because a near miss can still rip shingles off a roof, push rain through a weak opening, and leave a homeowner sorting through deductibles, exclusions, and claim paperwork when they're already under stress.

Table of Contents

- Protecting Your Tampa Bay Home From the Wind

- What Is Windstorm Insurance and Is It Required

- Decoding Your Coverage and Hurricane Deductibles

- How Insurers Price Windstorm Premiums in Tampa Bay

- Saving Money with Wind Mitigation Discounts

- Finding and Comparing Coverage with Select Insurance Group

- Tampa Bay Windstorm Insurance FAQ

Protecting Your Tampa Bay Home From the Wind

A Tampa Bay storm scenario usually begins with little fanfare. The forecast cone shifts west, local stores get busier, and homeowners begin walking the yard, checking loose items, and wondering whether their insurance is set up the right way. That anxiety is normal. On this coast, even people who've lived here for years still go back to the same questions every hurricane season.

The financial stakes are not small. NOAA reports that tropical cyclones have caused more than $1.5 trillion in damage in the United States since 1980, with an average cost of $23 billion per event and 7,211 deaths. For a Tampa Bay homeowner, that national figure translates into a local reality. Wind isn't a background risk here. It's one of the main forces shaping how people insure property along the Gulf.

Why Tampa Bay feels this differently

Tampa Bay properties face a mix of exposures that can look mild at first and become expensive quickly. A storm doesn't have to level a house to create a painful insurance problem. Uplift at the roof edge, broken seals around vents, failed soffits, damaged lanai screens, and wind-driven rain can all turn into repair decisions that test your policy language.

Neighborhood also changes the conversation. Homes closer to open water, barrier islands, and exposed coastal corridors often face tighter underwriting and more scrutiny around roof condition and opening protection. Inland homes aren't immune either. Strong gusts and driven rain can travel far from the shoreline.

Tampa Bay homeowners usually regret two things after a storm. Not reading the deductible ahead of time, and assuming flood and wind are the same claim.

People shopping coastal real estate elsewhere in Florida often run into the same lesson. If you're comparing Gulf properties more broadly, browsing Destin beachfront homes for sale can be a useful reminder that location, exposure, and insurance structure are closely tied across waterfront markets.

What actually helps

The homeowners who handle storm season best usually do three things well:

- They verify the policy structure: They know whether wind is included, endorsed, or written separately.

- They check the deductible before storm season: They don't wait until claim time to learn how much stays on them.

- They document mitigation features: They keep records of roof work, shutters, and upgrades that can affect both eligibility and price.

Windstorm insurance for Tampa Bay properties isn't about buying more paperwork. It's about reducing unpleasant surprises when the weather turns.

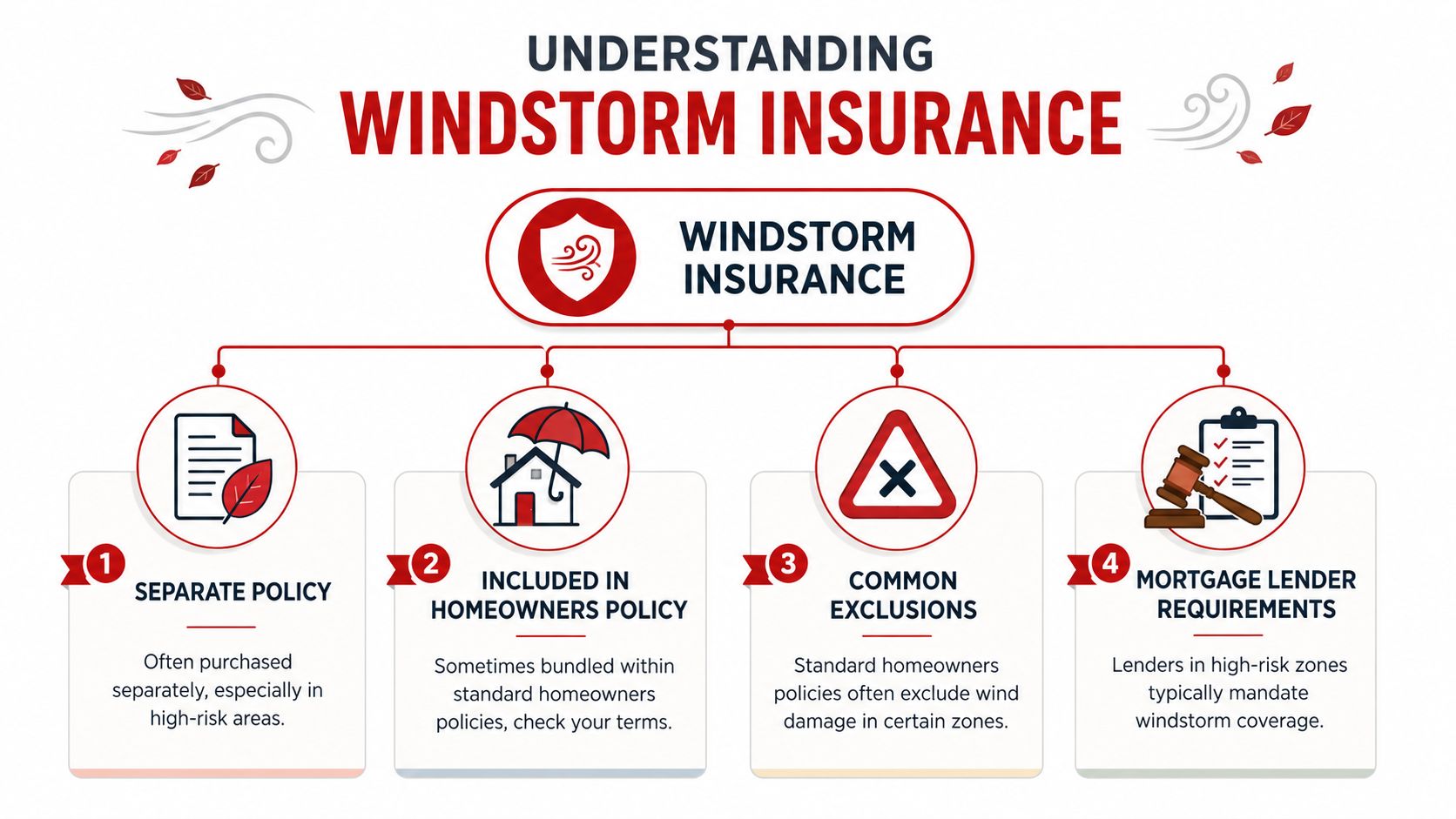

What Is Windstorm Insurance and Is It Required

Windstorm insurance is best understood as a coverage structure, not just a label. In Tampa Bay, wind protection may be included inside a homeowners policy, added by endorsement, or handled through a separate wind-only arrangement. The exact setup depends on the property, the insurer, and how exposed the home is to hurricane risk.

Think of your homeowners policy like a house with several doors. One door handles fire. Another handles liability. Wind may be one of the open doors, or it may be a door that needs a separate key. If you assume it's open without checking, that's where trouble starts.

How it shows up on Tampa Bay policies

In coastal and higher-risk areas, standard homeowners policies often need separate windstorm protection or a wind or hurricane endorsement. For Tampa properties, Policygenius notes that windstorm insurance can be purchased either as an add-on to homeowners coverage or as a separate wind-only policy. That matters because many new homeowners still expect wind to work the same way every time. In Florida, it often doesn't.

A practical review starts with your declarations page and endorsements. Look for how wind and hurricane losses are referenced, whether a separate deductible applies, and whether the mortgage company has any coverage conditions attached to closing or renewal.

Is it required by law

Usually, no, not in the sense many people mean.

Florida doesn't generally require every homeowner by law to carry windstorm insurance as a stand-alone purchase just because they own a house. The pressure more often comes from the loan side. If you have a mortgage, the lender may require coverage that protects the collateral. In coastal or high-risk areas around Tampa Bay, that often means you need clear wind protection in place before the lender is satisfied.

Practical rule: If you owe money on the house, treat lender requirements as non-negotiable even when people casually say coverage is "optional."

For cash buyers, the decision is technically more flexible. Financially, though, going without wind protection in this market can leave a homeowner carrying a very large repair burden alone.

What new homeowners should ask immediately

Before you assume you're protected, ask these questions:

- Is wind included in this policy: Don't settle for "it should be." Ask where it appears in writing.

- Is there a separate hurricane deductible: This affects claim math more than often realized.

- Is the lender asking for anything specific: Closing requirements and renewal requirements can differ.

- Would this home be written differently if the roof were newer or documented better: Carrier appetite can shift based on property details.

That short conversation clears up most of the confusion people have about windstorm insurance for Tampa Bay properties.

Decoding Your Coverage and Hurricane Deductibles

Most claim frustration in Tampa Bay doesn't come from the idea of coverage. It comes from the details. Homeowners often know they have wind protection, but they don't know how the payout works until the storm has already passed.

A standard deductible is usually a flat dollar amount. A hurricane deductible is often calculated as a percentage of the insured value of the home. That difference changes what you pay out of pocket before insurance contributes.

What wind coverage usually responds to

Wind coverage commonly applies to direct wind damage to the structure. That can include roof damage, siding damage, broken exterior openings, and certain interior damage if wind creates an opening that lets rain enter. The phrase that matters in many claims is whether the storm caused the opening.

What it usually does not handle is rising water or storm surge. That's where many homeowners get tripped up after a Gulf storm. Wind and flood can happen in the same event, but they are not the same insurance problem. If you want a plain-language breakdown of that distinction, this guide on does Florida home insurance cover water damage is a helpful companion read.

For homeowners trying to sort out whether flood coverage is part of the bigger picture, it's also worth reviewing Florida flood insurance requirement questions.

Why the deductible surprises so many homeowners

If your declarations page shows a hurricane deductible as a percentage, that's not a small surcharge. It's a share of the dwelling coverage amount. On a higher-value home, that can leave a large out-of-pocket responsibility before the carrier pays for covered wind loss.

Here is the cleanest comparison:

| Attribute | Standard Deductible | Hurricane Deductible |

|---|---|---|

| How it's stated | Flat dollar amount | Percentage of insured dwelling value |

| How homeowners read it | Usually straightforward | Often misunderstood at first glance |

| Out-of-pocket impact | More predictable | Can be much larger on higher-value homes |

| When it matters most | Everyday property claims | Storm and hurricane-related wind claims |

The practical problem isn't just size. It's timing. Storm losses often create immediate expenses. Temporary repairs, debris removal, interior drying, and roofing work can start before claim funds arrive.

Review the deductible as if the storm already happened. If the amount would strain your emergency funds, the policy deserves another look before hurricane season.

What works and what doesn't

A few habits consistently help:

- Read the declarations page first: That's where deductible structure usually becomes visible fastest.

- Match the deductible to your cash reserves: A lower premium can become the wrong choice if the deductible is painful to absorb.

- Separate wind from flood planning: One policy can't automatically stand in for the other.

What doesn't work is relying on assumptions. Many homeowners hear "covered for hurricanes" and assume that means every form of water and every storm-related loss will flow through one clean claim. In real life, claim handling is more specific than that. If you understand the deductible and the coverage trigger before a storm, you'll make better decisions under pressure.

How Insurers Price Windstorm Premiums in Tampa Bay

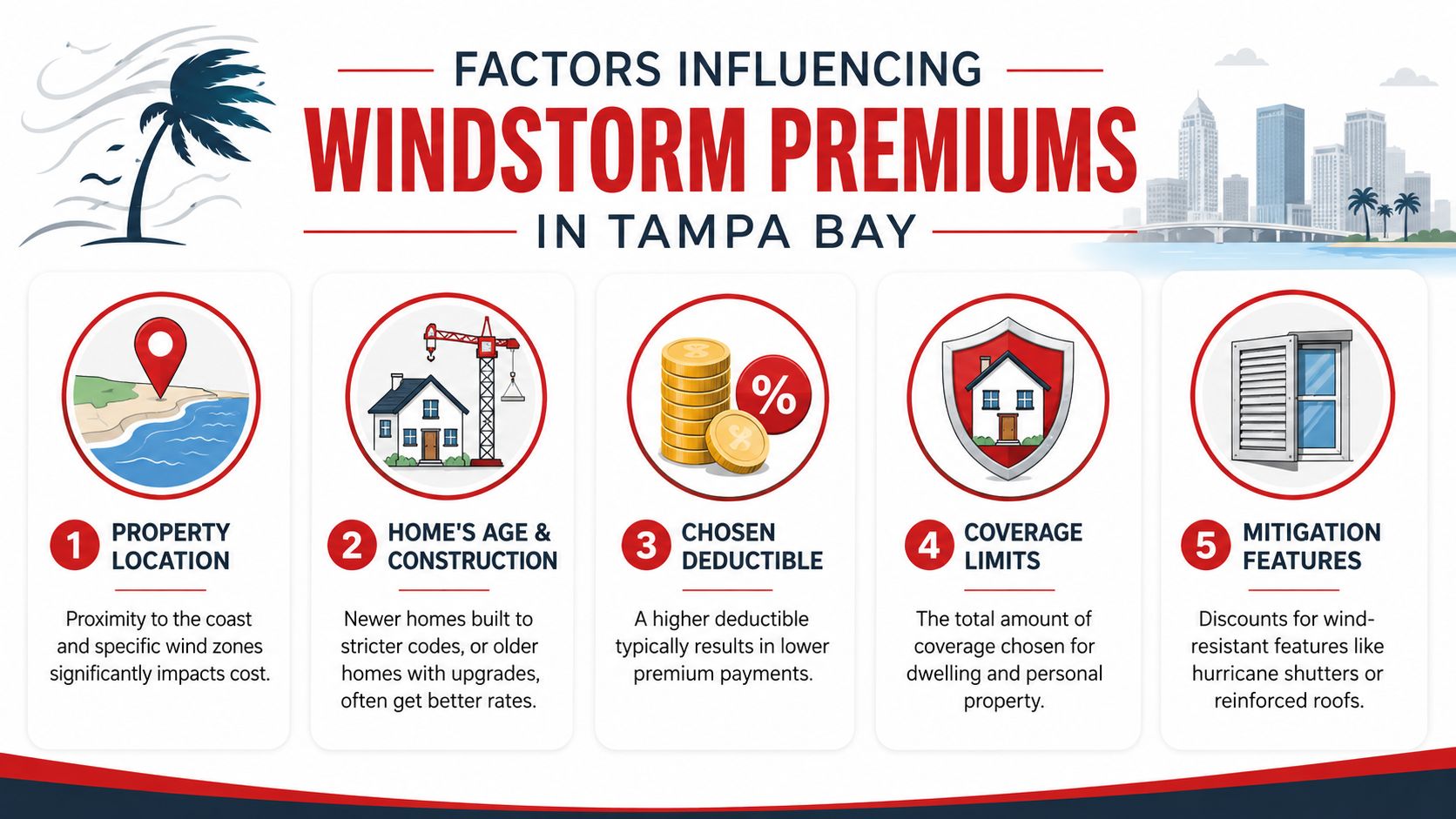

Two houses in the same ZIP code can get very different premiums. That's normal in Tampa Bay. Insurers don't price wind exposure by city name alone. They look at where the house sits, how it's built, how it's maintained, and how much risk they think they're taking on if a storm tracks toward the Gulf Coast.

For a basic market reference, the average annual homeowners premium in Tampa is about $2,266 for $300,000 in dwelling coverage and $3,768 for $500,000 in dwelling coverage. That doesn't mean every house should fall near those numbers. It does show how strongly dwelling value and local storm exposure shape pricing.

Location changes everything

A home near open water, on a barrier island, or in a more exposed coastal area usually gets reviewed differently from a similar home farther inland. Underwriters care about wind vulnerability, surrounding terrain, and how likely the property is to take the brunt of gusts and driven rain.

In Tampa Bay, geography affects more than just a mailing address. A house in South Tampa, a waterfront property in Pinellas, and a home farther inland in eastern Hillsborough can all produce different underwriting responses even if the homes look similar in photos.

For local pricing context beyond raw wind exposure, homeowners often also compare options for cheap homeowners insurance in Tampa.

The house itself matters just as much

Insurers typically look hard at construction details. Roof age, roof shape, attachment method, window protection, prior updates, and overall condition can all influence whether the home gets favorable terms, limited terms, or a harder underwriting conversation.

A practical breakdown looks like this:

- Roof condition: Older roofs usually receive more scrutiny, especially if documentation is weak.

- Construction type: Some homes resist wind better because of design and materials.

- Coverage limit selected: Insuring a larger dwelling amount raises the carrier's potential payout.

- Deductible choice: Higher deductibles often reduce premium, but they shift more cost back to you after a storm.

- Mitigation features: Shutters, reinforced openings, and stronger roof systems can help.

A neighbor's premium isn't a benchmark unless your homes match on roof, updates, distance from water, deductible, and coverage structure. Most don't.

Why rates can feel unpredictable

Carrier behavior in Florida changes. Some insurers tighten guidelines, limit certain property types, or become more selective in coastal areas. Others may still write business but are very careful about inspection results and roof documentation. That's why one quote can look manageable while another comes back with restrictions or a decline.

Homeowners get better results when they treat pricing as a full underwriting review, not a quick online guess. In Tampa Bay, the premium is rarely just about square footage. It's about how the carrier sees your storm profile.

Saving Money with Wind Mitigation Discounts

If you want the most practical way to reduce the cost side of windstorm insurance for Tampa Bay properties, start with wind mitigation. In Florida, carriers care about whether the home can better resist wind loss. If you can document that resistance clearly, you give the insurer a reason to price the risk more favorably.

This isn't just about making the house safer, though that's the first benefit. It's also about proving the features that already exist. Plenty of homeowners have qualifying improvements and never get full credit because the carrier never receives the right inspection or supporting paperwork.

What carriers usually want documented

A wind mitigation inspection focuses on features tied to storm resilience. The report often becomes the bridge between "I upgraded the house" and "the underwriter gave credit for the upgrade."

Common items reviewed include:

- Roof-to-wall connection: How the roof is attached matters in high-wind conditions.

- Roof deck attachment: Stronger attachment can improve how the structure performs.

- Roof shape: Some shapes are viewed more favorably for wind resistance.

- Opening protection: Impact-rated or otherwise protective features on windows and doors can matter.

- Secondary water resistance: Certain roof system details may help limit intrusion if shingles fail.

If you're unsure whether the roof condition will support a strong mitigation submission, a recent certified roof inspection can help clarify what you're working with before you start shopping.

Improvements that tend to matter most

Not every home project helps equally. Cosmetic work rarely moves the insurance needle. Structural and protective upgrades do.

Here are the changes that usually produce the most meaningful insurance value:

Roof replacement done to current standards

A newer roof with proper documentation often changes both eligibility and pricing conversations.Opening protection

Shutters or impact-rated openings can help when a carrier evaluates how vulnerable the house is to breach and driven rain.Documenting prior upgrades

Homeowners often lose credits because permits, invoices, or inspection forms are scattered or missing.Addressing weak points before underwriting sees them

Small repair issues can become larger insurance issues if they suggest deferred maintenance.

Spending money on the right upgrade is different from spending money on a visible upgrade. Carriers reward documented wind resistance, not curb appeal.

The best approach is to think in two buckets. First, what improves the home's real storm performance. Second, what can be clearly documented in a way the insurer will accept. When both line up, savings become much more realistic.

Finding and Comparing Coverage with Select Insurance Group

Shopping for wind coverage in Tampa Bay goes better when you approach it like a file review, not a casual quote request. The cleaner your information, the easier it is to compare policy structure, deductibles, and underwriting fit across available options.

What to gather before you shop

Before asking anyone for quotes, assemble the documents and facts that carriers usually care about most.

Bring together:

- Your current declarations page: This shows present limits, deductibles, endorsements, and gaps.

- Roof details: Year of replacement, permit information if available, and any recent inspection paperwork.

- Mitigation report: If you have one, it should be part of every quote conversation.

- Basic property updates: Electrical, plumbing, windows, and protective features can all matter.

- Loss history and claim details: Be ready to discuss prior claims accurately and plainly.

A homeowner who submits complete information usually gets a more useful answer than someone who asks for "a rough number." In this market, rough numbers often age badly once underwriting starts.

How an independent agent helps in Tampa Bay

An independent agent can make this process easier because the job isn't just finding a premium. It's matching the property to a carrier that will write the risk on acceptable terms. That matters in Tampa Bay, where roof age, distance from the coast, and documentation can all affect appetite.

One practical option is to work with the Tampa office of Select Insurance Group, which can help homeowners submit information for review and compare available carrier options. The value in that setup is straightforward. You don't have to guess which details matter most, and you don't have to rely on a single quote to define the market.

A smart comparison process usually looks like this:

- Check the coverage structure first: Is wind included, endorsed, or separate?

- Compare deductibles next: Premium alone doesn't tell you enough.

- Review exclusions and conditions: Especially anything tied to roof age or water entry.

- Ask what documentation could improve terms: Sometimes the path to a better option is paperwork, not a different house.

Getting one quote and stopping there is usually the mistake. In Florida property insurance, the first answer isn't always the most workable one.

Tampa Bay Windstorm Insurance FAQ

Is windstorm damage automatically included in every homeowners policy

No. Some policies include wind coverage, some add it through endorsement, and some properties need a separate arrangement. The safest move is to verify the structure in writing on your declarations page and endorsements rather than relying on verbal assumptions from a prior conversation.

If you're buying a home, ask this before closing. If you already own the home, ask it before storm season.

If rain gets in after a storm is that wind or flood

It depends on how the water entered. If wind damages the roof or another part of the exterior and rain enters through that storm-created opening, the claim may fall under wind coverage. Rising water, storm surge, and flooding are handled differently and usually require separate flood protection.

That distinction matters in Tampa Bay because one storm can produce both kinds of damage at the same property. The photos, timing, and damage pattern often become important.

When a storm hits, document where the water came from, what failed first, and how the damage spread. Those details can matter as much as the visible damage itself.

What if my current carrier won't renew me

Don't panic, but don't wait either. A non-renewal or tighter underwriting response usually means you need to shop early and gather documentation fast. Start with roof information, mitigation paperwork, and your full current policy.

Then focus on what can still be improved. Sometimes the solution is a different carrier fit. Sometimes it's better documentation. Sometimes it's completing a repair the next underwriter will want to see before offering terms.

If you're proactive, a non-renewal doesn't automatically mean you won't find coverage. It means the file has to be presented well, with the property details organized and the trade-offs understood.

If you want help reviewing windstorm insurance for your Tampa Bay property, Select Insurance Group, Inc. can help you compare coverage options, review deductibles, and sort through the policy details that matter most before the next storm is on the map.