You're probably here because Florida insurance already feels upside down.

Maybe you just bought a house and your lender asked for proof of coverage before closing. Maybe your renewal jumped, a carrier declined the home, or someone told you flood insurance is “separate” without explaining what that really means. New residents run into this every day. They expect insurance shopping to be a simple price comparison, then discover Florida doesn't behave like most states.

That confusion is reasonable. Florida isn't just another regional market. It is 4th in the United States for total premium in 2024, accounts for 10.67% of the U.S. homeowners premium market, and holds 22.8% of U.S. private flood premium, according to the NAIC Florida market facts. In plain English, a lot of the country's hardest property insurance problems show up here first.

A good insurance agency in Florida doesn't just sell a policy. It helps you understand why one home gets approved and another gets declined, why one quote looks cheap but isn't, and where your real exposure sits if a storm hits. That's the difference between buying insurance and building protection.

Table of Contents

- Finding Your Bearings in the Florida Insurance Market

- Core Insurance Coverages Every Floridian Needs

- Navigating Hurricane Risk and Flood Zones

- Independent Agency vs Captive Agent in Florida

- The Underrated Power of Bilingual Insurance Service

- Your Step-by-Step Guide to Getting and Comparing Quotes

- Why Select Insurance Group Is the Right Choice for Florida

Finding Your Bearings in the Florida Insurance Market

You buy a house in Florida, get a quote that looks fine, and assume the hard part is over. Then the lender asks for revisions, the roof age becomes an issue, flood exposure was never addressed, or the carrier changes its underwriting before closing. That is a common Florida insurance experience.

The first job is not finding the lowest number. The first job is finding coverage that still fits after the inspection report comes in, the mortgage company asks questions, and storm season puts pressure on the market. Florida is a hard market because several forces hit at once. Storm risk is obvious, but it is only part of the story. Carrier appetite changes quickly, underwriting is stricter than many new residents expect, and pricing can shift fast even when the house itself has not changed.

Florida also carries unusual weight in the national insurance picture. It ranks among the largest premium states and holds an outsized share of homeowners and private flood premium, according to the NAIC Florida market facts. That matters because big volume does not make this market simple. It makes the consequences of pricing pressure, claims costs, and underwriting changes show up faster.

A new resident usually sees only the quote. An experienced Florida agent looks at the moving parts behind it.

What makes Florida different

In many states, insurance shopping is mostly a price exercise. In Florida, it is a fit exercise first and a price exercise second. Roof age, construction type, prior claims, distance to the coast, flood exposure, occupancy, and even how quickly paperwork is returned can affect whether a quote holds up.

That is why cheap can turn expensive in a hurry.

A policy with the wrong deductible, a wind exclusion you did not expect, or a carrier that does not really want your type of risk is not a bargain. It is a problem waiting for a closing date, a renewal notice, or a claim to expose it. Florida buyers need to know not just what a policy costs, but why that price exists and what assumptions are built into it.

What a strong agency actually does

A good Florida agency does more than collect a few rates.

- Explains underwriting changes in plain language. If the quote changed because of the roof, prior losses, occupancy, or protection class, you should know that before you bind coverage.

- Checks for gaps across policies. Home, flood, auto, umbrella, and business coverage often connect. If one piece is missing, the problem usually shows up at the worst time.

- Keeps the file moving. Inspections, signatures, mortgagee details, proof of prior coverage, and policy updates have to be handled in the right order or the deal can stall.

- Shops for stability, not just a teaser rate. In Florida, the better question is whether the policy will still make sense at renewal and whether the carrier is a realistic fit for the property.

Independent agencies are useful here because Florida rarely rewards a one-size-fits-all approach. Their value is not just access to quotes. It is having someone sort through the trade-offs, catch the weak spots, and explain the difference between a policy that looks good on paper and one that is built to hold up in this market.

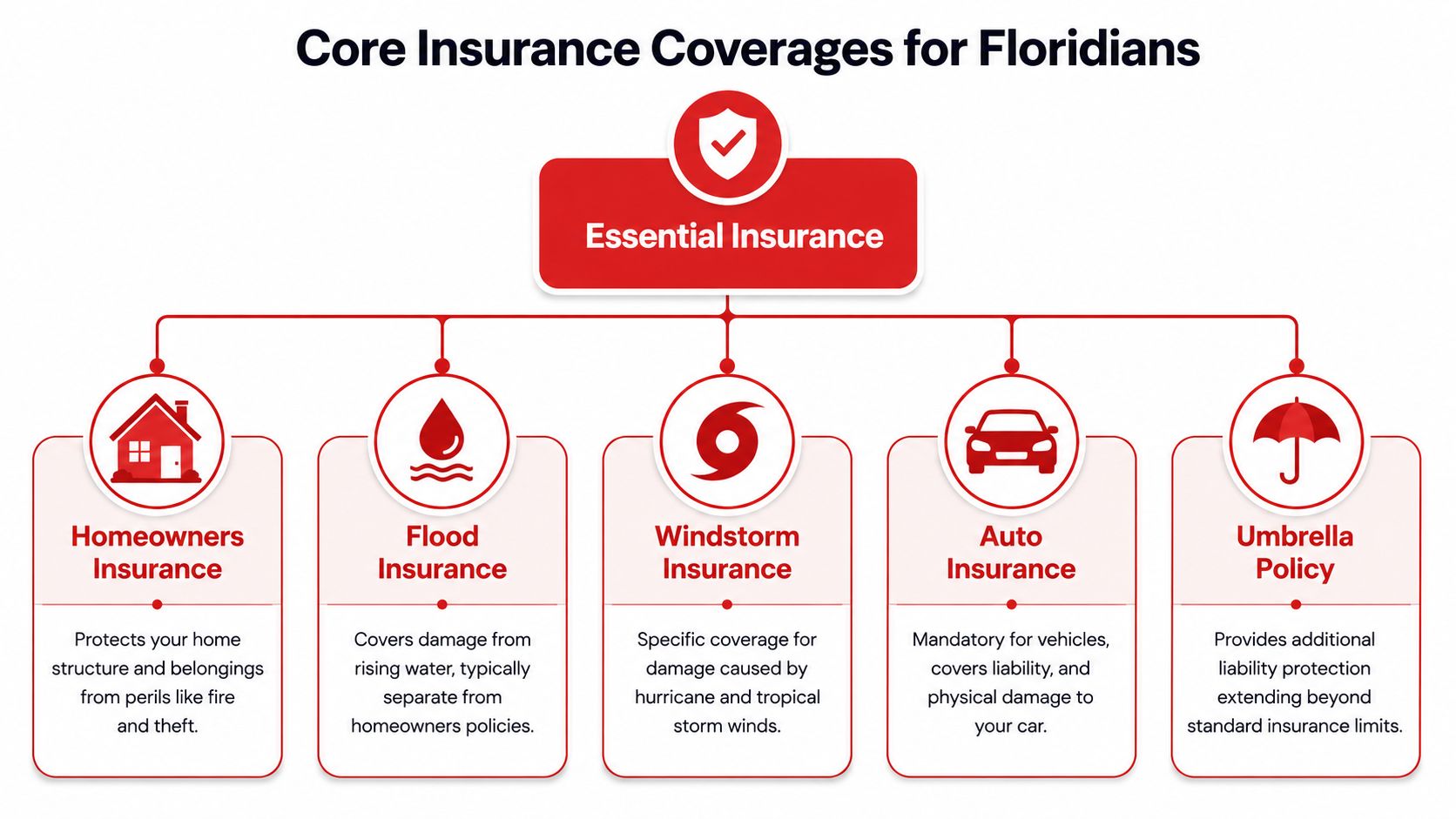

Core Insurance Coverages Every Floridian Needs

Florida coverage works best when you stop thinking in product names and start thinking in jobs. Each policy has a specific job. When one job is missing, the whole protection plan gets shaky.

Think in layers, not single policies

Homeowners insurance protects the house itself and usually your belongings, liability exposure, and loss of use. But many buyers assume it covers every kind of water damage. It doesn't. That misunderstanding causes more trouble in Florida than almost any marketing slogan.

Flood insurance handles rising water. If water enters because of flooding conditions, that's generally a different policy conversation than a standard homeowners claim. A lot of new residents learn this too late.

Wind-related protection matters because Florida storms don't damage homes in just one way. Wind can damage the roof or structure, while flood affects the ground-up water side of the loss. You have to know where one policy stops and another begins.

Auto insurance protects driving exposure, but it also often becomes the first policy families shop because it feels simple. It isn't simple if the household has teenage drivers, multiple vehicles, long commutes, or mixed personal and business use.

Umbrella coverage adds extra liability protection over underlying policies. Think of it as the overflow valve. If a serious claim runs past the base policy's liability limits, umbrella coverage can become the difference between inconvenience and a financial disaster.

A complete insurance plan in Florida should fit together like roof decking, underlayment, and shingles. If one layer is missing, the others can't do the whole job.

Where business owners get caught short

Small business owners often make one dangerous assumption. They think a personal auto policy will handle work driving. That gap shows up all the time.

A common problem in Florida is that owners use personal vehicles for deliveries, job site visits, tools, or employee errands and don't realize they may also need hired/non-owned auto, cargo, workers' comp, or general liability. That overlap is one reason many agencies end up bridging personal and commercial lines for clients, as noted by Angle Insurance Agency's discussion of personal and business coverage needs.

Here's the practical breakdown:

- General liability: Protects against many third-party injury or property damage claims tied to business operations.

- Commercial auto: Handles vehicles used in business when personal auto coverage won't match the exposure.

- Workers' comp: Matters when people are working for you, especially where physical job duties create injury exposure.

- Cargo or equipment-related protection: Important when tools, materials, or goods move with the vehicle.

The mistake isn't buying too little of one policy. It's assuming one policy can do another policy's job.

Navigating Hurricane Risk and Flood Zones

The phone call usually sounds the same. A new Florida homeowner gets a quote that looks manageable, then notices a separate hurricane deductible, a flood exclusion, and an inspection requirement tied to the roof. The confusion is understandable. In Florida, the premium is only one part of the decision. The harder question is whether the policy will hold up the way you expect when a storm hits.

Why property quotes feel unpredictable

Florida property pricing changes fast because carriers are judging the house as much as the buyer. Roof age matters. So does distance to the coast, prior claims, updates to electrical or plumbing systems, and whether the home fits the carrier's current underwriting appetite. Two houses on the same street can get very different results if one has an older roof or a history of water losses.

That is why generic definitions do not help much here. Buyers need to know why one company says no, why another offers coverage with tighter terms, and why a cheap quote can turn expensive after the first claim. A good independent agency spends time sorting that out before binding coverage, not after there is a problem.

A few examples make the pattern clear:

- Older roof: The carrier may ask for an inspection, limit terms, or decline the risk until repairs or replacement are complete.

- Coastal exposure: Wind risk can narrow carrier options and change both deductible structure and price.

- Prior claims: One past loss may be manageable. Several water or roof claims can sharply reduce available markets.

- Flood exposure: Standard homeowners insurance generally does not cover rising water, so flood protection often has to be placed separately.

If you want a plain-English explanation of where homeowners coverage usually stops and flood coverage begins, Onsite Pro on flood insurance is a helpful primer. If the lender requirement is your first concern, this guide on whether flood insurance is required in Florida explains when that issue comes up.

How hurricane deductibles really work

A hurricane deductible is a separate cost-sharing rule tied to storm losses that meet the policy's hurricane trigger. It does not work like the flat deductible many buyers are used to on other claims.

The simplest way to explain it is by example. A standard all-other-perils deductible might be a fixed dollar amount for a kitchen fire or a burst pipe. A hurricane deductible is often a percentage of the dwelling coverage. On a well-insured home, that can mean a much larger out-of-pocket expense after a named storm. Buyers who compare premium only often miss that point until it is too late.

Ask these questions on every Florida home quote: What deductible applies to hurricane losses? What losses are excluded? Is flood covered anywhere in this package, or do I need a separate policy?

Those questions matter because Florida insurance shopping is less about finding the lowest number and more about building a policy stack that matches the actual risk. That is where an independent agency earns its keep. The job is not just to produce quotes. The job is to explain the trade-offs, spot the gaps, and help place coverage that is still workable when carrier rules tighten.

Independent Agency vs Captive Agent in Florida

The easiest way to explain this is travel.

If you walk up to a single airline counter, the agent can only sell seats on that airline. If you work with a travel advisor who can check many carriers, you have a better shot at finding a route that fits the trip. Insurance works much the same way.

The simplest way to think about the difference

A captive agent represents one carrier. A policy recommendation has to fit that carrier's products and underwriting rules.

An independent agent works with multiple carriers. If one company won't take the home, vehicle, driver profile, or business class, the agency may still have other markets to review. In Florida, that flexibility is often the whole game.

The independent channel is large here. IBISWorld estimates 38,691 businesses in Florida's Insurance Brokers & Agencies industry in 2026, with a projected market size of $19.9 billion and 88,038 employees, according to IBISWorld's Florida industry data. That density tells you something important. Customers have choices, and agencies have to earn trust with service, carrier access, and actual know-how.

When choice matters most

Choice matters when the risk is clean enough for standard placement. It matters even more when it isn't.

| Feature | Independent Agency (like Select Insurance Group) | Captive Agent (like a single-brand agent) |

|---|---|---|

| Carrier access | Reviews options across multiple carriers | Limited to one carrier |

| Fit for unusual risks | Can pivot if one market declines | Must fit one company's rules |

| Shopping convenience | One agency can compare multiple paths | Customer may need to shop elsewhere |

| Advice style | Often focused on matching risk to available markets | Often focused on one company's product set |

| Account flexibility | Can help when home, auto, flood, or business needs don't line up neatly | May have fewer placement alternatives |

One useful explanation of this model is what an independent insurance agency does.

An independent agency earns its keep in Florida when the first answer is no.

That doesn't mean captive agents never help. It means Florida buyers benefit from optionality. When underwriting tightens, being able to move from one carrier appetite to another saves time and often saves the deal.

The Underrated Power of Bilingual Insurance Service

People treat bilingual service like a convenience feature. In insurance, it's often a risk-control feature.

A misunderstanding in a restaurant order is annoying. A misunderstanding about deductibles, exclusions, listed drivers, business use, or claim reporting can cost real money. Florida households and business owners frequently handle these issues while stressed, rushed, or dealing with a lender, landlord, contractor, or employer at the same time.

Clarity matters most when there is stress

The value of bilingual service shows up in ordinary moments.

A family is reviewing a homeowners package and doesn't fully understand what water losses are excluded. A contractor is trying to explain who drives which vehicle for what purpose. A driver is reporting an accident and can describe what happened much more accurately in Spanish than in English. In each case, language precision changes the quality of the outcome.

Good bilingual service helps with:

- Application accuracy: The details entered at the start shape pricing and eligibility.

- Coverage understanding: Clients need to know what the policy does and does not do.

- Claims communication: Stress makes technical language harder, not easier.

- Commercial questions: Business owners often juggle auto, liability, employees, and contracts in the same conversation.

Sometimes clients also need formal help understanding policy paperwork. For that, a resource on accurate insurance policy translations can be useful when exact terminology matters.

A policy isn't clearer because someone says it faster in English. It's clearer when the client understands what they're buying, what they're signing, and what they should expect if they file a claim.

Your Step-by-Step Guide to Getting and Comparing Quotes

A new Florida resident often learns the hard way that two quotes with the same price can protect very differently. One has a higher hurricane deductible. Another leaves out a coverage you assumed was included. A third looks fine until underwriting asks for roof documentation, prior policy proof, or updated photos and the deal stalls.

That is why quote shopping in Florida needs a method. The goal is not just to get a low number. The goal is to find coverage you can place, afford, and keep in a market that changes fast.

What to gather before you shop

Start with documents, not guesswork. A clean submission gets better results and cuts down on back-and-forth with underwriters.

Driver and household details

Have names, dates of birth, license information, and the full driver list ready. If a college student still comes home and drives the car, or a relative lives with you, say so up front.Vehicle or property specifics

For auto, gather VINs, garaging address, current insurer, and current limits. For property, have the address, year built, roof age, square footage, occupancy type, and any updates to plumbing, electrical, or HVAC if you know them.Current declarations pages

This is the fastest way to compare what you have to what you are being offered. An agent can see deductibles, liability limits, endorsements, and named insured details without making assumptions.Loss history and prior insurance

Prior claims, canceled policies, and coverage gaps matter in Florida. Hiding them only wastes time because underwriting usually finds them later.

How to compare quotes the right way

Price matters. Structure matters more.

Florida premiums are heavily shaped by details that do not show up in a quick online form. Roof age, distance from the coast, prior claims, occupancy, dog breed, business use of a vehicle, and even whether the home is seasonal or owner-occupied can change both price and eligibility. That is why an independent agency is useful here. One submission can be adjusted and remarketed without making you restart the process every time a carrier declines or changes terms. If you split time between states, a multi-state independent insurance agency serving Florida, South Carolina, and North Carolina can also help keep the application details consistent.

Use this checklist when you compare:

- Match deductibles first: A lower premium may mean you are taking on more out-of-pocket risk.

- Check liability limits: One quote should not look cheaper just because it protects less.

- Review separate or excluded coverages: Flood, wind, water damage limits, and business-use exposures need direct answers.

- Ask what is required to bind: Photos, inspections, proof of repairs, signatures, and mortgage details can delay approval.

- Confirm every named person and address: Missing drivers, wrong mailing addresses, or incorrect loan information create preventable problems.

A hurricane deductible works like a larger self-insured share tied to a specific storm loss. If one quote shows 2 percent and another shows a flat deductible, those are not equal offers even if the premium is close.

Good agencies also explain why a quote came back the way it did. That matters in Florida. Sometimes the cheapest option is cheap because the carrier is strict on inspections, less flexible on older roofs, or more likely to change appetite at renewal. Clear communication on those trade-offs helps clients make better decisions, and agencies that use systems to improve insurance client interactions usually handle the quote-and-bind process with fewer errors.

Comparable quotes take work. The payoff is fewer surprises after closing, after binding, and after a claim.

Why Select Insurance Group Is the Right Choice for Florida

A Florida insurance buyer usually needs three things at once. Access to multiple carriers. Clear guidance through tricky property and auto questions. Fast communication when paperwork has to move now.

That combination is where an independent model helps most. For someone dealing with a home purchase, a flood question, a hard-to-place vehicle, or a business account that mixes personal and commercial exposure, having one agency compare multiple options is usually more practical than restarting the process every time one path stalls.

What practical help looks like

Select Insurance Group, Inc. is an independent agency serving Florida and other Southeastern states, and it connects customers with quotes from multiple carriers across personal and commercial lines. For Florida shoppers who need one place to review home, auto, flood, renters, motorcycle, RV, general liability, commercial property, workers' compensation, commercial auto, or trucking options, that structure fits the complexity of the market. If you split time between states or have moving parts outside Florida, their multi-state insurance agency overview shows how that broader service model works.

Service quality also matters because insurance buying is part paperwork, part advice, and part follow-up. Agencies that handle communication well tend to reduce confusion during quoting, issuing, and account changes. For a broader look at systems that improve insurance client interactions, that resource gives useful context on why responsiveness and organized communication matter so much in this business.

The right insurance agency in Florida won't promise that the market is simple. It will make the market understandable. That's what most buyers need.

If you want help sorting through Florida home, auto, flood, or business coverage without the usual confusion, contact Select Insurance Group, Inc. for a free, no-obligation quote. A licensed agent can review your current coverage, explain the trade-offs, and help you compare options that fit your property, vehicles, and budget.