You opened a letter from your mortgage company, saw a note about flood coverage, and suddenly a simple question turned into a stressful one. Your neighbor says flood insurance is only required near the coast. Someone else says everybody in Florida will need it. Then your homeowners renewal mentions Citizens, and now you're wondering whether this is a lender issue, a state rule, or just a recommendation.

That confusion is normal. In Florida, flood insurance rules come from more than one place, and the answer depends on which layer applies to your home. The practical problem is that homeowners often hear one partial truth and assume it applies to everyone.

The stakes are real. Florida is the largest flood-insurance market in the U.S., accounting for roughly 35% of all National Flood Insurance Program policies, and there are more than 2.1 million flood-insurance policies in force in the state, according to a Wharton public policy brief on Florida flood insurance. This isn't a niche issue. It affects buyers, long-time owners, condo residents, landlords, and families trying to keep a policy compliant at renewal.

Table of Contents

- The Question Every Florida Homeowner Is Asking

- When Flood Insurance Becomes Mandatory in Florida

- Florida's New 2026 Citizens Insurance Flood Mandate Explained

- NFIP vs Private Flood Insurance What Is the Best Choice for You

- How Much Does Flood Insurance Cost in Florida

- Your Action Plan How to Check Requirements and Get Covered

- Why an Independent Agent Is Your Best Ally for Florida Flood Insurance

- Frequently Asked Questions About Florida Flood Insurance

The Question Every Florida Homeowner Is Asking

A lot of Florida homeowners are having the same conversation right now. It usually starts with a policy renewal, a loan closing, or a quick comment from a real estate agent that sends people searching for a clear yes-or-no answer. Instead, they run into a mess of half-answers.

One homeowner may hear, “It's only required if you're in a flood zone.” Another hears, “Citizens is making everyone get it.” A third finds out the lender wants it even though the house isn't where they expected a requirement. All three situations can be true, depending on the details.

Why the answer feels inconsistent

The phrase is flood insurance required in Florida sounds like it should have one statewide rule behind it. It doesn't. Florida does not have a single law that requires every homeowner to buy flood insurance. What people are really asking is which authority gets to require it in their situation.

That authority might be:

- A federal lending rule tied to the mortgage

- A state-specific Citizens requirement tied to the homeowners policy

- A lender's own underwriting rule tied to protecting the loan

Most homeowner confusion comes from mixing those three layers together.

Why so many people are asking now

This issue has gotten louder because more homeowners are seeing flood insurance move from “good idea” to “show proof of coverage.” For some, that happens during a purchase or refinance. For others, it happens at policy renewal. The trigger matters because the deadline and consequences are different.

What works is checking the exact source of the requirement before you shop. What does not work is assuming your neighbor's situation matches yours. Two homes on the same street can face different flood insurance obligations because their loans, insurers, and policy structures are different.

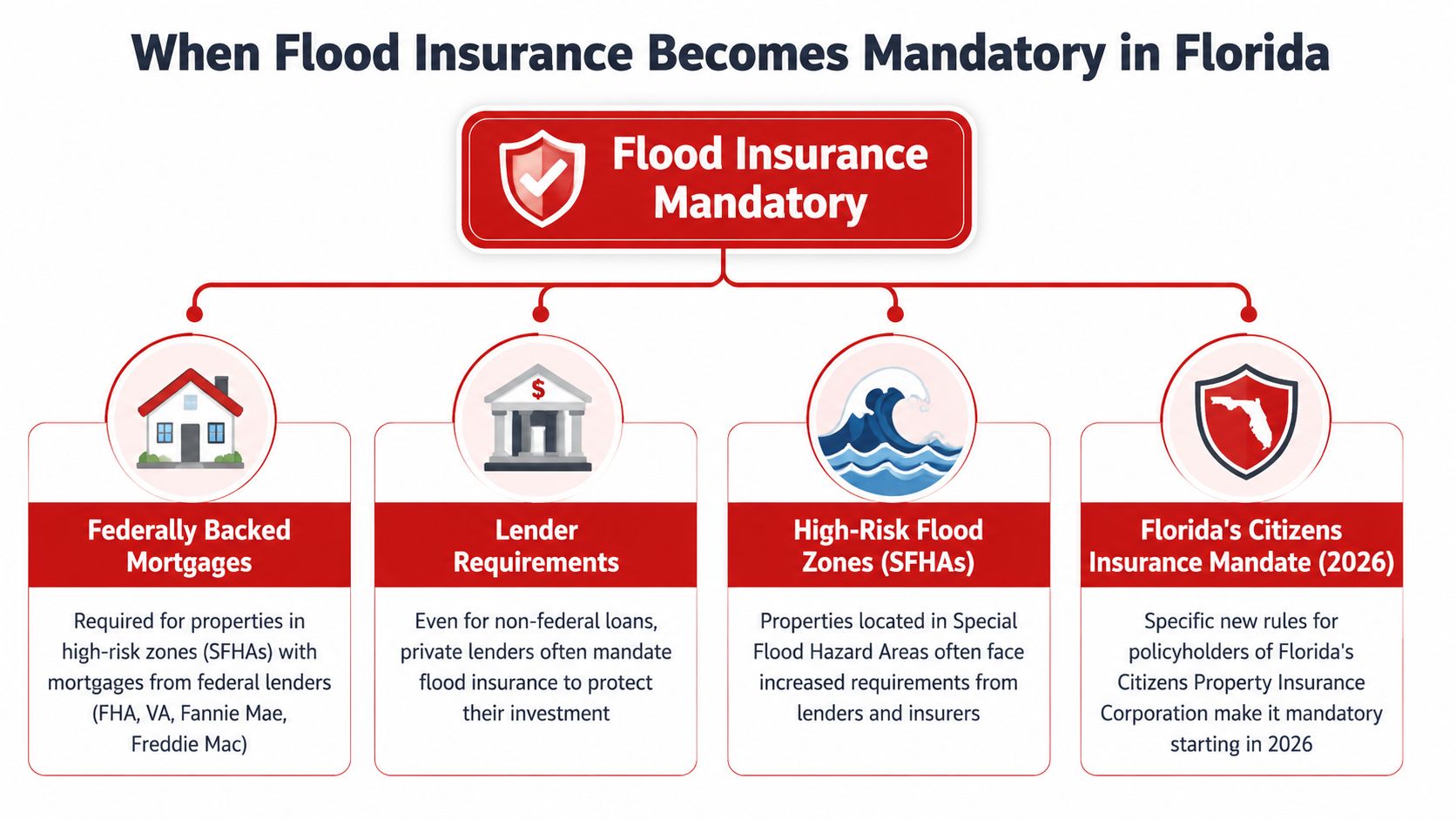

When Flood Insurance Becomes Mandatory in Florida

Flood insurance becomes mandatory in Florida through three practical channels. If you want a clean answer, identify which one applies first.

Federal rules come first

The clearest mandatory trigger is federal. The Florida Office of Insurance Regulation flood insurance guidance states that federal law requires flood insurance on properties in a Special Flood Hazard Area with a federally regulated or insured loan. It also explains that these high-risk areas have at least a 1% annual chance of flooding.

That means if your home is in an SFHA and your mortgage falls under that federal framework, flood insurance is not optional. The required amount must equal the outstanding loan balance or the NFIP maximum of $250,000, whichever is less.

Buyers often find themselves surprised. They focus on whether flood insurance is “required in Florida,” when the actual issue is whether their loan and flood map designation trigger the federal rule.

State rules can add another requirement

Even if a property owner is not dealing with the federal mortgage rule, state-specific insurance requirements can still matter. In Florida, that's most important for homeowners insured through Citizens. Those rules have their own schedule and compliance process, which is separate from the federal mortgage framework.

A common mistake is assuming, “I'm not in a federally required zone, so I'm done.” That's not always true if your homeowners coverage is with Citizens and your renewal falls under the phase-in requirements.

Practical rule: Treat your mortgage requirements and your homeowners policy requirements as two separate checklists.

Lenders can go beyond the baseline

Private lenders often add their own requirement as a condition of the loan. That can happen because they want stronger protection for the property securing the mortgage. From a homeowner's perspective, it doesn't matter much whether the requirement came from federal law or the lender's own standards. If the loan documents require flood coverage, you need to keep it in force.

Here's the easiest way to understand it:

- Check the flood zone. If the property is in an SFHA, federal rules may control.

- Check the loan type. Federally regulated or insured loans have specific flood requirements.

- Check the lender's closing package and servicing notices. The lender may impose its own flood condition.

- Check the homeowners carrier. Citizens may create a separate insurance-side requirement.

What homeowners get wrong

The biggest mistake is treating flood insurance as a one-time closing issue. In practice, this is an ongoing compliance issue. Lenders can force-place coverage if required protection lapses, and policyholders can run into renewal problems if they wait until the last minute to confirm what's needed.

A second mistake is buying a policy before confirming the required limit and acceptable proof. The coverage may exist, but if it doesn't meet the lender or carrier standard, you can still have a problem.

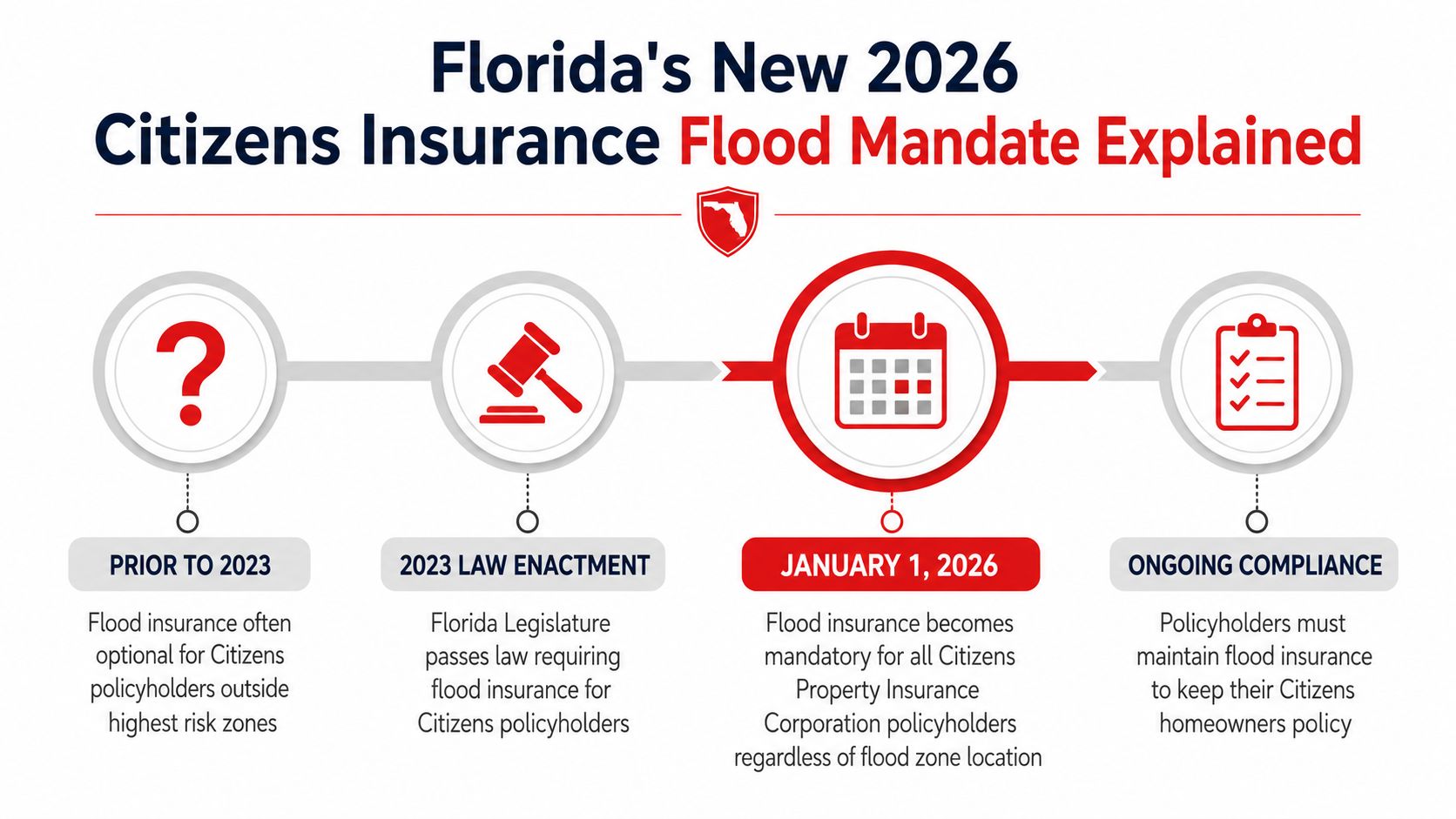

Florida's New 2026 Citizens Insurance Flood Mandate Explained

A lot of Florida homeowners get blindsided here. They assume flood insurance only becomes an issue if the home sits in a high-risk flood zone, then a Citizens renewal comes up and flood coverage suddenly becomes part of keeping the policy.

Who needs to pay attention now

If your home is insured with Citizens and your policy includes wind coverage, check this rule before renewal, not after. According to Citizens flood insurance requirements, Florida's phase-in requires many new and renewing personal residential policyholders to carry flood coverage based on Coverage A limits, and homes in a Special Flood Hazard Area generally must carry it regardless of insured value.

The phase-in started with higher-value homes first and is scheduled to widen over time. Based on Citizens' published schedule, the requirement applied to homes with $600,000 or more in Coverage A in 2024, is set to apply to $500,000 or more in 2025, and would apply to $400,000 or more in 2026. Citizens states that affected policyholders will be required to show proof of flood coverage by January 1, 2027.

That matters because this is a carrier requirement, not just a lender issue.

Why this catches homeowners off guard

I see the same confusion often. A homeowner checks the flood map, sees the property is outside the highest-risk zone, and assumes the flood question is settled. For Citizens policyholders, it often is not.

Citizens adds a second layer of requirements on top of any mortgage rule. That is the key trade-off Florida homeowners need to understand. Federal law can require flood insurance because of the loan. Citizens can require it because of the homeowners policy. You have to satisfy both when both apply.

Timing is where people get squeezed. Citizens wants proof of acceptable flood coverage at renewal. If you wait for the renewal packet, you may have very little time to confirm limits, compare policy forms, and fix documentation problems before the policy renewal is on the line.

If you have Citizens, ask one question now: Will my next renewal require proof of flood insurance?

What this rule is trying to do

The state did not set this up as a narrow map-zone rule. It was designed to push more Citizens-insured homes to carry flood coverage over time, which reduces the chance that uninsured flood losses create bigger problems for homeowners and for the broader property insurance system.

For a homeowner, the practical takeaway is straightforward. Stop treating flood insurance as a single yes-or-no question. In Florida, there are three separate layers to check: your lender, Citizens, and your own risk tolerance. Citizens is the layer many people miss until renewal is close.

The right move is to verify your Coverage A amount, confirm whether the home is in an SFHA, and ask your agent what proof Citizens will accept before your renewal date gets tight.

NFIP vs Private Flood Insurance What Is the Best Choice for You

Once you know you need flood insurance, the next question is where to get it. In most cases, the decision comes down to an NFIP policy or a private flood policy. Neither is automatically better for every property.

Where the NFIP fits

The NFIP is the standard path many homeowners know first. It's familiar to lenders, easy to document, and often works well when you need a straightforward solution that satisfies a mortgage or renewal requirement.

It can also be a practical starting point if your main goal is compliance and your coverage need lines up with the available federal structure.

Where private flood insurance can fit better

Private flood policies can be worth a serious look if you want more flexibility. Depending on the home, a private option may offer broader customization, different deductible choices, or a better fit for higher-value properties. The trade-off is that policy language, underwriting, and coverage details can vary more from one carrier to another.

That variation is why flood insurance shopping should never stop at the first quote.

NFIP vs. Private Flood Insurance at a Glance

| Feature | NFIP (Federal Program) | Private Insurance |

|---|---|---|

| Primary role | Standardized flood coverage framework | Carrier-specific flood coverage |

| Coverage structure | More uniform policy approach | More flexible policy design |

| Limit considerations | Federal cap structure applies | May fit homes needing more flexibility |

| Lender familiarity | Commonly recognized for compliance | Usually acceptable when it meets requirements |

| Customization | More limited | Often more tailored |

| Shopping process | Straightforward baseline option | Requires closer comparison of forms and terms |

| Best use case | Homeowners who want a known, standard route | Homeowners who want to compare features beyond the baseline |

Don't choose based only on premium. Choose based on whether the policy satisfies the requirement and protects the property the way you expect.

How to make the decision

Ask these questions before picking one path:

- What triggered the requirement? A lender or Citizens may have specific proof and limit expectations.

- What property are you protecting? A modest home and a high-value home may not fit the same policy well.

- Do you need building coverage only, or contents too? That choice changes the value of the policy.

- How much policy variation are you comfortable reviewing? Standardized can be easier. Customized can be stronger.

What works is comparing the actual policy design, not just the headline price. What does not work is assuming all flood policies respond the same way after a loss.

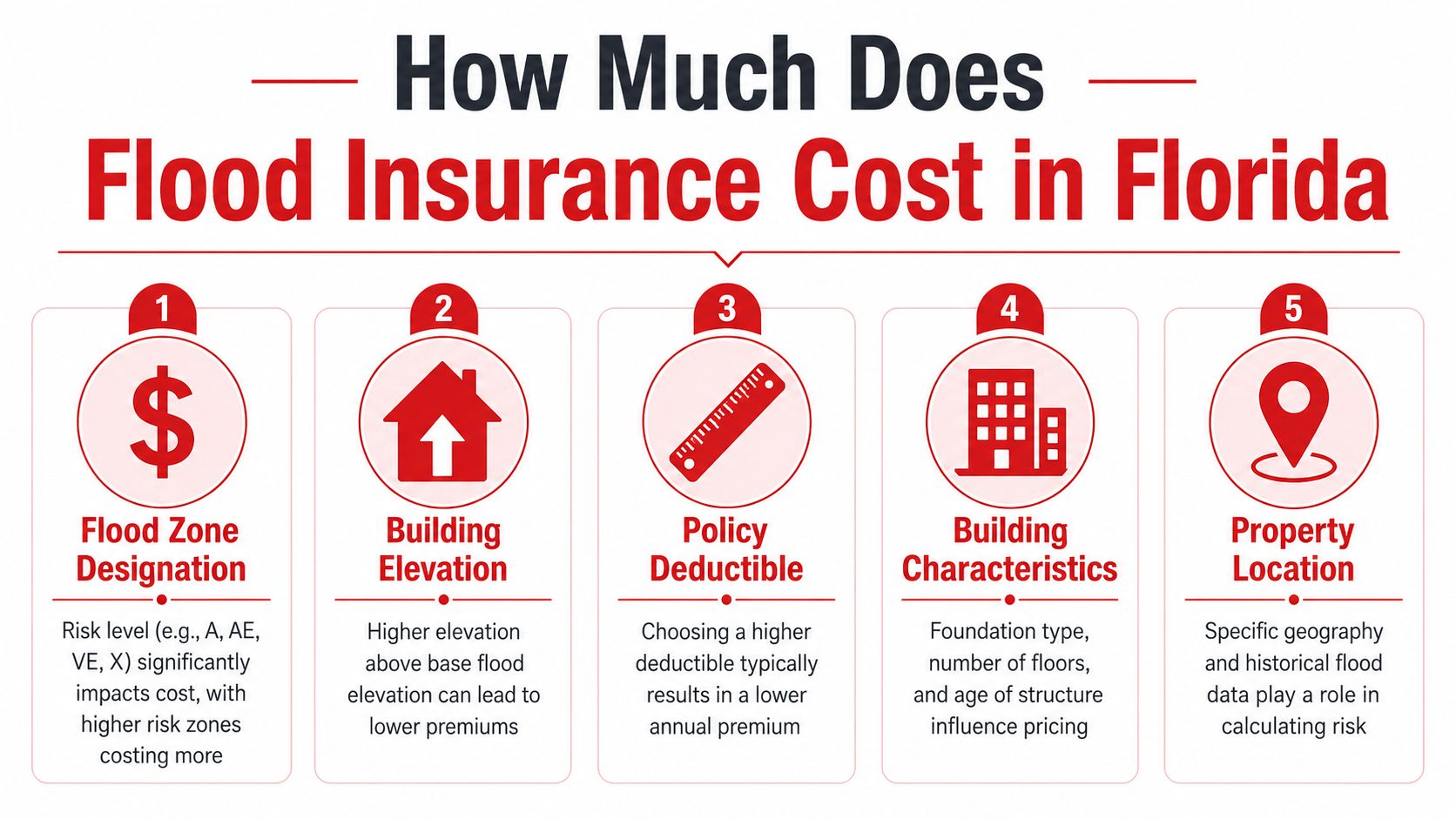

How Much Does Flood Insurance Cost in Florida

There isn't one statewide price for flood insurance. The premium depends on the property, the risk profile, and the coverage choices you make. That's why two homeowners in the same county can get very different quotes.

What actually drives the premium

A flood quote usually starts with the property itself. Carriers and programs look closely at the flood zone, elevation details, construction characteristics, and where the living area sits relative to expected flood exposure. They also look at the policy design you choose, especially your deductible and whether you're buying building coverage, contents coverage, or both.

The Florida Chief Financial Officer's consumer guidance notes that flood insurance may help pay to repair or rebuild the home and replace personal property, which is why pricing should be tied to what you're trying to protect, not just whether the lender requires a minimum form of coverage.

Here are the practical drivers most homeowners should review with an agent:

- Flood zone and map classification: This shapes the starting risk profile.

- Elevation and foundation details: These can materially affect how the risk is viewed.

- Coverage amount selected: More protection generally means more premium.

- Deductible choice: A higher deductible can lower annual cost, but increases out-of-pocket responsibility in a claim.

- Building characteristics: Age, layout, and structural details all matter.

Why the cheapest policy is not always the smartest one

A low premium can look attractive until you realize the policy was built around minimum compliance rather than meaningful recovery. That's especially important for homeowners who assume flood insurance only protects the structure. In reality, many policyholders also need to think about furniture, electronics, clothing, and other belongings.

If you own a condo, the same mindset applies. Unit owners often focus on the building policy and overlook gaps that can still affect them directly. That's one reason it helps to understand related protections such as condo loss assessment coverage in Florida, because flood planning and broader property-loss planning often intersect.

Your Action Plan How to Check Requirements and Get Covered

A common Florida scenario goes like this: a homeowner hears flood insurance is "only required in a flood zone," then gets a renewal notice, a lender letter, or a Citizens eligibility question that says otherwise. The mistake is treating flood insurance as one rule, when it can come from three different places. Federal loan requirements, Citizens rules, and your own exposure are separate issues, and each one needs to be checked for your specific address.

Start with documents tied to your home

Start with your address and your paperwork, not neighborhood advice.

Pull three items first: your mortgage documents, your current homeowners declarations page, and any recent renewal, escrow, or servicing letters. Then confirm how the property is mapped through FEMA's flood map tools and read your notices for direct language such as flood insurance required, proof of coverage needed, or renewal condition.

That short review usually tells you which layer of the problem you are dealing with.

Confirm who is actually requiring coverage

Ask each decision-maker a direct question and get the answer in writing if possible.

- Lender: Is flood insurance required for this loan today? If yes, what coverage amount, effective date, and proof of insurance do you require?

- Homeowners carrier: Is flood coverage a condition of renewal or continued eligibility?

- Citizens, if applicable: Does the 2026 phase-in apply based on my dwelling limit and renewal date?

- Agent or carrier representative: Will this specific flood policy form satisfy the lender or homeowners requirement?

Clear answers matter because a policy can look acceptable on paper and still fail a lender review or a renewal check if the form, limit, or documentation is wrong.

Quote coverage in the right order

I usually tell homeowners to make the decision in this order: compliance, protection, then price.

First, make sure the policy satisfies the actual requirement. Second, check whether it protects what you would need after a real flood, including structure, contents, and deductibles you could realistically absorb. Third, compare premium. That approach helps avoid the expensive mistake of buying the cheapest policy first and discovering later that it solved only part of the problem.

This is also the point where many people mix up flood loss with other water claims. Rising water is handled differently from pipe leaks, roof leaks, and similar events. If you want a clearer line between those issues, this guide to homeowners insurance water damage coverage is a useful companion.

Use one checklist if you own a condo

Condo owners need to be even more careful because the building policy, unit coverage, lender requirements, and personal property exposure do not always line up cleanly. If that is your situation, it helps to review flood planning alongside related gaps such as condo loss assessment coverage in Florida, since special assessments and flood-related building issues can affect unit owners in ways they do not expect.

Get help before the deadline hits

Flood insurance problems usually come from delay, not refusal. Waiting until a closing date, renewal deadline, or lender warning letter leaves very little room to fix documentation issues or compare policy options carefully.

Select Insurance Group, Inc. can help Florida property owners review the requirement, compare available flood coverage paths, and line up the policy with the rule that applies to the home.

Why an Independent Agent Is Your Best Ally for Florida Flood Insurance

Flood insurance gets complicated because one home can be affected by more than one rule at the same time. A lender may care about minimum compliance. A homeowners carrier may care about renewal eligibility. The owner may care about protecting the structure and belongings well enough to recover after a real loss.

One house can have multiple decision-makers

That's why an independent agent is useful. Instead of looking at one policy in isolation, the agent can help line up the flood quote with the mortgage requirement, the homeowners policy requirement, and the owner's actual risk tolerance.

This is especially important when a homeowner is trying to answer is flood insurance required in Florida and gets pulled into a vague online debate. The better question is narrower and more useful: “What is required for my address, my loan, and my policy?”

What practical help looks like

A good independent agent helps with the unglamorous parts that matter:

- Reviewing compliance triggers: Federal, lender, and Citizens issues are not the same thing.

- Comparing available policy paths: The quote should meet the requirement and make sense for the property.

- Checking proof of coverage needs: Renewal problems often come from missing or incomplete documentation.

- Explaining trade-offs in plain language: Deductibles, contents protection, and policy fit should be clear before purchase.

If you've never worked with one, this short explanation of what an independent insurance agency is helps clarify why the model fits a layered issue like flood coverage so well.

Frequently Asked Questions About Florida Flood Insurance

Does homeowners insurance cover any flood-related water damage

A claim often turns on where the water came from.

If water enters from outside and rises onto the property, that is usually treated as flood and handled under a separate flood policy, not a standard homeowners policy. Other water losses may fall under different parts of the homeowners policy, depending on the cause and the policy language. For renters sorting through nearby storm coverage questions, this guide on whether renters insurance covers hurricane damage addresses a related issue.

Can renters and condo owners buy flood coverage too

Yes. Flood insurance is available to renters, condo unit owners, and business owners, not just single-family homeowners.

That matters in Florida because flood losses often affect more than the building itself. A renter may need protection for personal property. A condo owner may need coverage for belongings and certain interior items inside the unit. The right fit depends on what the association insures, what the unit owner is responsible for, and what would be expensive to replace after a loss.

What if I am outside a high-risk zone

A lower-risk zone does not end the conversation. It only changes which question comes first.

Start with the three layers that matter. Check whether your mortgage lender requires flood insurance. Check whether your homeowners carrier, including Citizens if that applies to your policy, requires it for eligibility or renewal. Then look at the property's actual exposure and your ability to absorb a flood loss out of pocket. Those are separate decisions, and Florida homeowners get into trouble when they treat them as one.

If you want help sorting out which rule applies to your home and what kind of flood policy fits, contact Select Insurance Group, Inc. An agent can review your address, loan situation, and current homeowners policy, then help you compare flood coverage options that satisfy the requirement and make sense for the property.