You open the mail, or your association posts a notice in the portal, and the number is the part that stops you cold. The bill isn't for your kitchen, your flooring, or anything inside your unit. It's your share of damage, deductibles, or liability tied to the whole building.

That is the situation regarding Condo loss assessment coverage Florida owners need to understand right now. In today's market, the old assumption that the association's master policy will handle the big stuff is dangerous. Between storm deductibles, tighter building requirements, and expensive repairs in older communities, condo owners can get hit with costs they never expected and often can't absorb easily.

The Unexpected Bill Every Florida Condo Owner Dreads

A Florida condo owner can do almost everything right and still get blindsided.

You carry your HO-6 policy. You pay your association dues. You assume the building's master insurance is there for the roof, the lobby, the elevators, and the exterior. Then a major storm hits, the association's costs come in higher than expected, and owners receive a special assessment notice. Suddenly, your share is due even though the damage wasn't inside your unit.

That's where many people first learn what a loss assessment is. The association had a covered loss to common property, but the master policy didn't make everyone whole. Maybe the deductible was large. Maybe the limit wasn't enough. Maybe reserves helped but didn't close the gap. The remaining amount gets spread among unit owners.

Why this catches owners off guard

The misunderstanding is simple. Owners think of insurance in two separate boxes:

- The association's policy covers the building

- Their HO-6 policy covers their unit

In practice, there's overlap, and there are gaps. One of the biggest gaps is your personal share of an association assessment after a covered loss to common elements.

A condo owner usually doesn't feel the risk until the assessment letter arrives. By then, the question isn't what the policy should have covered. The question is whether your current limit is enough.

A common real-world problem is storm damage to shared property. The building suffers roof damage, exterior damage, or damage to other common areas. The association makes a claim. The master policy responds, but not fully. Owners then absorb part of the remaining bill.

The protection most owners overlook

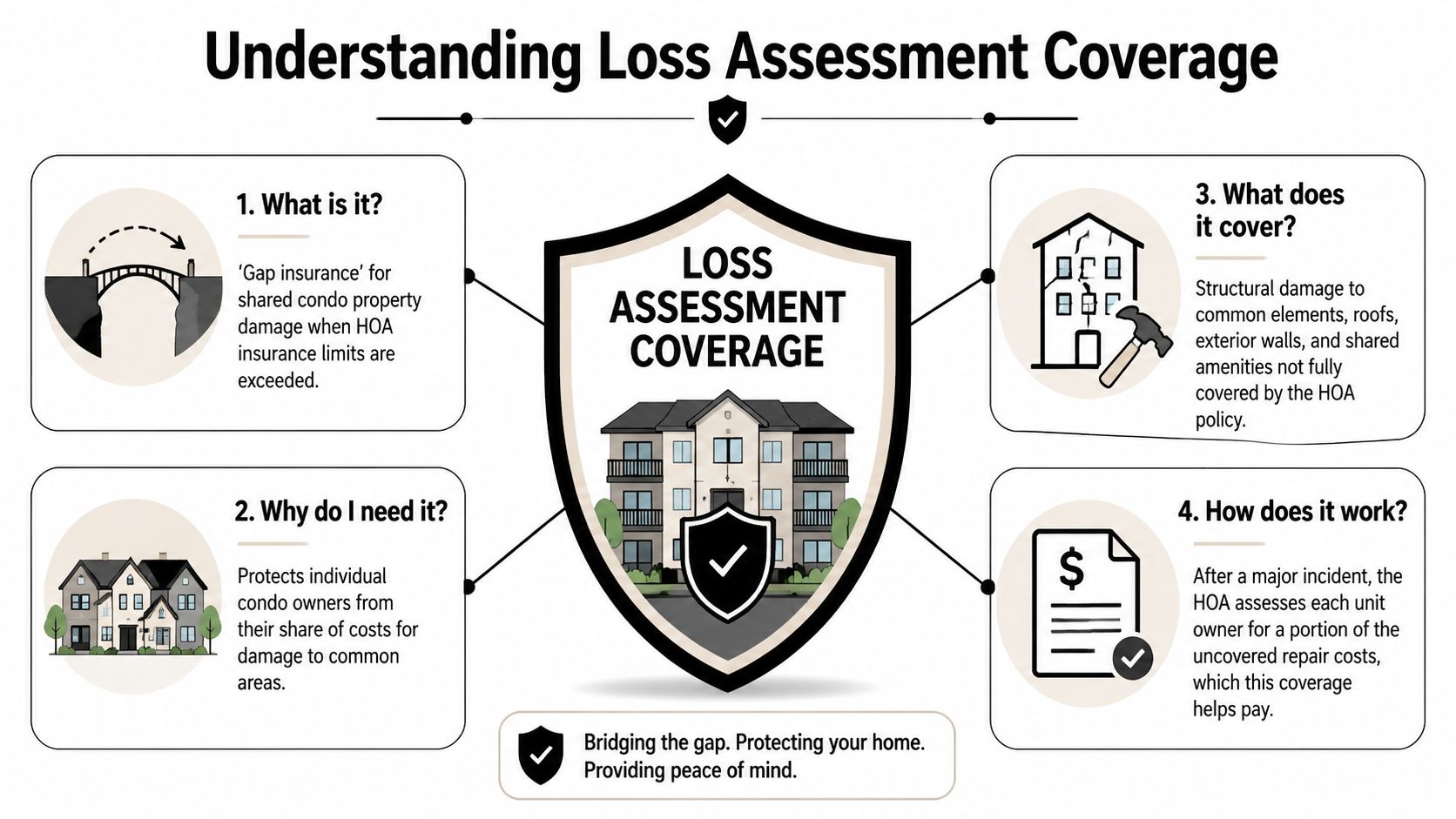

Loss assessment coverage is the part of an HO-6 condo policy designed for this situation. It helps pay your share of certain assessments the association levies after a covered event.

That sounds technical, but the purpose is straightforward. It protects you from having to write a large check because the building's insurance didn't cover all of a covered loss.

For Florida condo owners, that protection matters far more now than it did a few years ago. The state's condo market changed after Surfside, and storm exposure hasn't gotten any easier. If you own in a mid-rise, high-rise, coastal building, or older community, this isn't a niche coverage. It's part of basic financial self-defense.

What Is Loss Assessment Coverage

Think of loss assessment coverage as gap insurance for condo ownership. It doesn't insure the whole building by itself. It helps with your share of certain costs when the association assesses unit owners after a covered loss.

The legal framework in Florida matters here. Under Florida Statute § 627.714, every residential condo unit owner's policy must include at least $2,000 in property loss assessment coverage for assessments arising from the same direct loss to common elements, the coverage is excess over the association's master policy and other applicable insurance, and the deductible can be no more than $250 per direct loss. That same statute-based example shows the problem clearly: with a $1M master policy shortfall in a 100-unit building, a $10,000 per-unit assessment would leave the statutory minimum covering only $2,000.

How it fits with the master policy

The association's master policy is the first layer. Your HO-6 loss assessment coverage is not meant to replace it. It steps in after the master policy and any other available funds are exhausted.

That “excess” feature is critical. Owners sometimes assume their own policy will cover whatever bill the association sends. It won't work that way. The assessment must arise from a qualifying loss, and the association's coverage position matters.

Here's the practical version:

- A covered event damages common property.

- The association files under the master policy.

- There's a remaining amount allocated to owners.

- Your HO-6 loss assessment coverage may pay your share, up to your policy limit and subject to policy terms.

What the coverage is really designed to do

This coverage is built for shared ownership risk. Condo living means you don't just own your unit. You also share responsibility for common elements and, in some situations, shared liability.

Practical rule: If a bill comes from the association because of a covered loss affecting the community, your HO-6 loss assessment coverage is the first place to check.

That doesn't mean every special assessment is covered. It means this is the policy section that responds when the assessment stems from a covered peril and falls within the policy language. If your current declarations page shows only a small default amount, you may technically have the coverage while still being badly underinsured.

Why Loss Assessment Is a Critical Florida Concern

Florida condo owners are dealing with two pressure points at once. One comes from storms. The other comes from building conditions, inspections, and deferred maintenance surfacing all at once.

Post-Surfside, associations have been forced into a different operating reality. According to this Florida condo assessment overview discussing Surfside, SB 4-D, and hurricane deductible pressure, individual unit owner shares have frequently reached $50,000 to $100,000+. That same source notes the 2022 Condo Safety Act (SB 4-D) requires milestone inspections by Dec. 31, 2024 for buildings over 30 years old, and that hurricane deductibles of 2% to 5% of insured value can add $10,000 to $25,000 per unit in a storm loss.

The post-Surfside shift

Before Surfside, some owners saw loss assessment coverage as a minor add-on. Now it sits in a much more serious conversation about ownership risk.

Associations are reviewing structural conditions more aggressively. Repair schedules are tighter. Funding decisions are harder. Owners are seeing just how quickly a large community expense turns into a personal bill.

That doesn't mean loss assessment coverage solves every condo financial problem. It doesn't. But it does address one very specific and very painful exposure: being assessed after a covered loss that affects common property or shared liability.

Why Florida is different

Florida's condo environment is unforgiving because several risks stack on top of each other:

- Storm exposure: Wind events and hurricanes create large losses to shared building components.

- High master deductibles: A deductible tied to building value can create a major owner assessment after a single event.

- Older buildings: Deferred maintenance and structural findings increase financial pressure on associations.

- Compressed timelines: Legal and operational demands can force communities to act faster than owners expected.

Owners often focus on whether a building has insurance. The harder question is whether the building has enough insurance, enough reserves, and a deductible structure that won't push major costs back onto owners.

The practical takeaway is this: in Florida, “I have condo insurance” doesn't tell you much. The better question is whether your HO-6 includes enough loss assessment coverage for the kind of building you live in, the deductible structure your association carries, and the kinds of assessments your community could realistically issue.

How Much Loss Assessment Coverage Do You Really Need

Florida raised the minimum, but the minimum is not the target.

According to this Florida guidance on special assessment coverage and the CS/HB 625 increase, policies issued after July 1, 2024 must carry at least $5,000 in loss assessment coverage. The same source says that floor is often inadequate and notes recommendations of $25,000 at a minimum, $50,000 for typical owners, and $100,000 for coastal high-rises because a single event can produce assessments above $50,000 per unit.

Why the legal minimum falls short

The statutory floor exists to ensure condo owners have some built-in protection. It does not mean that amount reflects current Florida exposure.

The weakest buying decision I see is this: an owner notices they already have loss assessment coverage and assumes they're set. If the declarations page shows a low default amount, you may be compliant and still far from protected.

A better way to think about it is to match your limit to the building you live in.

A practical way to choose a limit

Look at your association's master policy and ask these questions:

- What is the hurricane deductible? If the deductible is tied to building value, your share can become large quickly.

- What kind of building is this? Coastal high-rises and larger communities usually justify more protection than a smaller inland property.

- How old is the property? Older buildings can face more financial stress around repairs, insurance structure, and shared costs.

- How comfortable are you writing a surprise check? Coverage decisions are really about balance-sheet tolerance.

If you want a clearer framework for understanding insurance policy limits, that resource helps explain why a legally required minimum and a useful limit are often two different things. The same principle applies to condo loss assessment coverage.

For owners comparing broader home insurance decisions, it also helps to understand how low-price shopping can leave important gaps. This discussion of cheap homeowners insurance trade-offs is useful because the least expensive policy is often the one with the smallest built-in cushions.

What tends to work better

In practice, these ranges make more sense than relying on the statutory floor alone:

- $25,000 if you want a stronger baseline than the minimum

- $50,000 for many typical condo owners

- $100,000 if you own in a coastal high-rise or a building with higher shared exposure

Buy enough loss assessment coverage so that an association notice feels stressful, not financially destructive.

What doesn't work is assuming your community's reserves or master policy will always absorb the hit. Those are important protections, but they don't eliminate owner exposure.

What Loss Assessment Covers and Excludes

Many claims go sideways at this stage. Owners hear “special assessment” and assume any charge from the association is insured. That's not how it works.

According to this Merlin Law Group explanation of condo loss assessment coverage, loss assessment coverage generally applies when the assessment comes from a peril that matches your policy's Coverage A, such as fire or windstorm, and it can also apply to liability shortfalls. The same source gives a clear liability example: if a $500,000 association liability judgment exceeds policy limits by $100,000 in a 50-unit building, each owner's $2,000 share would be covered up to the policy limit. It also warns that structural assessments tied to post-Surfside reforms are often denied as non-covered perils without specific endorsements.

The core rule

Loss assessment coverage usually responds when all of these are true:

- The association levies an assessment to owners

- The underlying cause is a covered peril under your HO-6 policy

- The charge falls within your policy language and limits

It usually does not respond just because the association needs money.

Covered vs excluded special assessments

| Assessment Scenario | Typically Covered by Loss Assessment? | Reasoning |

|---|---|---|

| Your share of a hurricane-related master policy deductible after wind damage to common elements | Typically yes | Windstorm is generally a covered peril if it matches your HO-6 coverage |

| Your share of a fire loss to shared hallways, roof areas, or lobby damage not fully paid by the master policy | Typically yes | Fire is commonly a covered peril under the unit policy |

| Your share of an association liability overage after a covered judgment exceeds master liability limits | Often yes | Loss assessment can extend to liability shortfalls |

| Assessment to replace an old roof because of age and deterioration | Typically no | Wear and tear is usually not a covered peril |

| Assessment for deferred maintenance discovered during milestone or structural review | Typically no | Gradual deterioration and maintenance issues usually aren't covered causes of loss |

| Assessment to build up reserves or fund future projects | Typically no | Reserve funding is not a covered direct loss |

| Assessment for upgrades, code-driven improvements, or elective amenity projects | Typically no | These costs usually aren't tied to a covered direct loss under the HO-6 |

Where owners get tripped up

The phrase special assessment is broader than loss assessment coverage. Some special assessments are tied to covered losses. Many are not.

That distinction matters more now because some of the biggest condo bills in Florida come from structural repair obligations, reserve pressures, and major maintenance needs. Those bills can be severe, but they often don't come from a sudden covered peril.

For a broader plain-English comparison of what insurance is meant to pay for versus what remains your responsibility, this explanation of full coverage vs liability is helpful. The same mindset applies here: labels can sound all-inclusive, but policy triggers still control.

If the association's charge is tied to age, deterioration, maintenance, reserve shortages, or upgrades, don't assume your loss assessment coverage will respond.

That's why a policy review should include more than just the limit. You need to understand the trigger. A large limit on a misunderstood coverage can still leave an owner frustrated when the assessment arrives.

Your Action Plan Buying Coverage and Filing a Claim

The best time to fix this coverage is before your association sends a notice. Once the loss happens, you can't go backward and buy protection for that event.

Buying the right coverage

Start with your HO-6 declarations page. Find the line for loss assessment and look at the limit. If it shows only the built-in minimum or another low amount, ask your agent whether higher limits are available by endorsement.

Then gather the building-side details that matter:

- Request the master policy summary from the association or property manager.

- Check the deductible structure, especially for hurricane and wind.

- Review recent association notices for repair funding pressure, insurance changes, or upcoming owner votes.

- Ask how your carrier handles increased loss assessment limits and whether any special endorsements are available.

If you've dealt with unit damage claims before, practical documentation habits matter here too. This guide with actionable water damage insurance advice is useful because the same claim discipline applies: keep notices, photos, timelines, and communications organized from day one.

Filing a claim when the assessment arrives

When your association sends a covered assessment notice, move quickly.

- Notify your insurer right away: Don't wait until the payment deadline is close.

- Send the assessment letter: Your carrier will want the formal notice showing what is being charged and why.

- Document the underlying cause: Storm, fire, or liability matters. The trigger has to line up with policy coverage.

- Ask for the master policy information: The carrier may need to see what the association insurance paid and what remained.

- Track deadlines carefully: The same GreatFlorida guidance cited earlier notes claims must be noticed within 3 years of damage occurrence, or the later of 1 year after loss or 90 days after the association vote to levy, depending on the situation.

A good independent agency can also help you understand how the policy language works across carriers. If you're not sure what that role looks like, this explanation of what an independent insurance agency does gives a useful overview.

What works and what doesn't

What works is simple: higher limits, early review, and fast reporting.

What doesn't work is waiting until renewal to think about it, assuming every special assessment is covered, or treating the master policy as if it eliminates your personal exposure.

Florida Condo Owner FAQs

Is a milestone inspection or structural repair assessment covered?

Usually not. If the assessment comes from deferred maintenance, age, deterioration, or structural issues uncovered through post-Surfside compliance work, that usually doesn't fit the sudden covered-peril trigger that loss assessment coverage depends on.

Is loss assessment the same thing as a special assessment?

Not exactly. A special assessment is the bill the association sends owners. Loss assessment coverage is the insurance protection that may help pay your share when that bill arises from a covered loss. Some special assessments qualify. Many don't.

If my association has reserves, do I still need this coverage?

Yes. Reserves help, but they don't remove the risk. A covered loss can still exceed what the association's reserves and master policy can handle, especially when deductibles are large or damage is widespread.

Does this only matter for hurricane claims?

No. It can matter for other covered causes of loss and for certain liability assessments too. The issue isn't whether the event was dramatic. The issue is whether the association assessed owners because of a covered loss that fits your policy.

Should I just buy the highest limit available?

Not blindly. Buy a limit that matches your building's real exposure, your association's deductible structure, and your own ability to absorb a surprise bill. Higher is generally better than the minimum in Florida, but the smart move is a policy review tied to your specific property.

If you own a Florida condo and aren't sure whether your current HO-6 policy can handle a serious assessment, Select Insurance Group, Inc. can review your coverage, explain your options clearly, and help you compare carriers for stronger protection before the next notice arrives.