You're probably closer to needing umbrella coverage than you think.

In Florida, risk doesn't stay neatly inside your driveway or your lane. It follows you onto I-4 during rush hour, into the backyard when friends come over, onto the water on a weekend, and into ordinary online interactions that can turn hostile fast. Many individuals commonly carry auto and home insurance and assume that means their assets are protected. Sometimes they are. Sometimes they're only protected up to the point where a serious claim breaks through those limits.

That's where a Personal umbrella policy for asset protection FL becomes practical, not theoretical. It isn't for “wealthy people only.” It's for anyone who owns a home, has savings, earns a good income, has a teen driver, hosts guests, owns a pool or boat, or wants a legal claim to stay an insurance problem instead of becoming a personal financial problem.

Why Your Florida Lifestyle Needs More Than Standard Insurance

A common Florida scenario starts out ordinary. You're driving home on a packed highway. Traffic compresses fast, one driver brakes late, and multiple vehicles are involved. Or you host a weekend barbecue, kids are in and out of the pool, and a guest gets badly hurt. The underlying event may be an accident. The financial aftermath is often a liability claim, then a demand letter, then a lawsuit.

Florida adds its own pressure to that equation. Roads are crowded with residents, visitors, delivery traffic, and distracted drivers. Homes often come with pools, docks, golf carts, and other features that raise liability exposure. After storms, properties see more foot traffic from contractors, roofers, cleanup crews, and vendors. More people on your property means more chances for someone to allege that a condition, hazard, or decision caused an injury.

A serious liability claim doesn't have to come from reckless behavior. It often comes from an ordinary day that went sideways.

Standard auto and homeowners liability coverage matters, but it has limits. If a claim exceeds those limits, the unpaid portion can put pressure on savings, non-exempt assets, and future earnings. That's the gap many Florida households don't discover until they're already under stress.

Renters face the same issue from a different angle. If you lease your place and assume your risk is lower, that may be true for the building itself, but not necessarily for personal liability. If you're reviewing how storm-related protection fits into the bigger picture, this guide on whether renters insurance covers hurricane damage helps separate property coverage from liability exposure.

Where the Florida risk feels different

A few patterns show up again and again:

- Driving risk: Dense traffic and multi-vehicle crashes can push an auto liability claim well past basic limits.

- Home risk: Pools, dogs, trampolines, and frequent guests create more chances for a premises liability claim.

- Boat and water risk: Weekend recreation can create large injury claims, especially when several people are involved.

- Rental and hosting risk: A landlord or short-term host can face claims tied to steps, railings, walkways, lighting, or supervision.

That's why umbrella insurance works so well in Florida. It's a financial raincoat for a legal downpour.

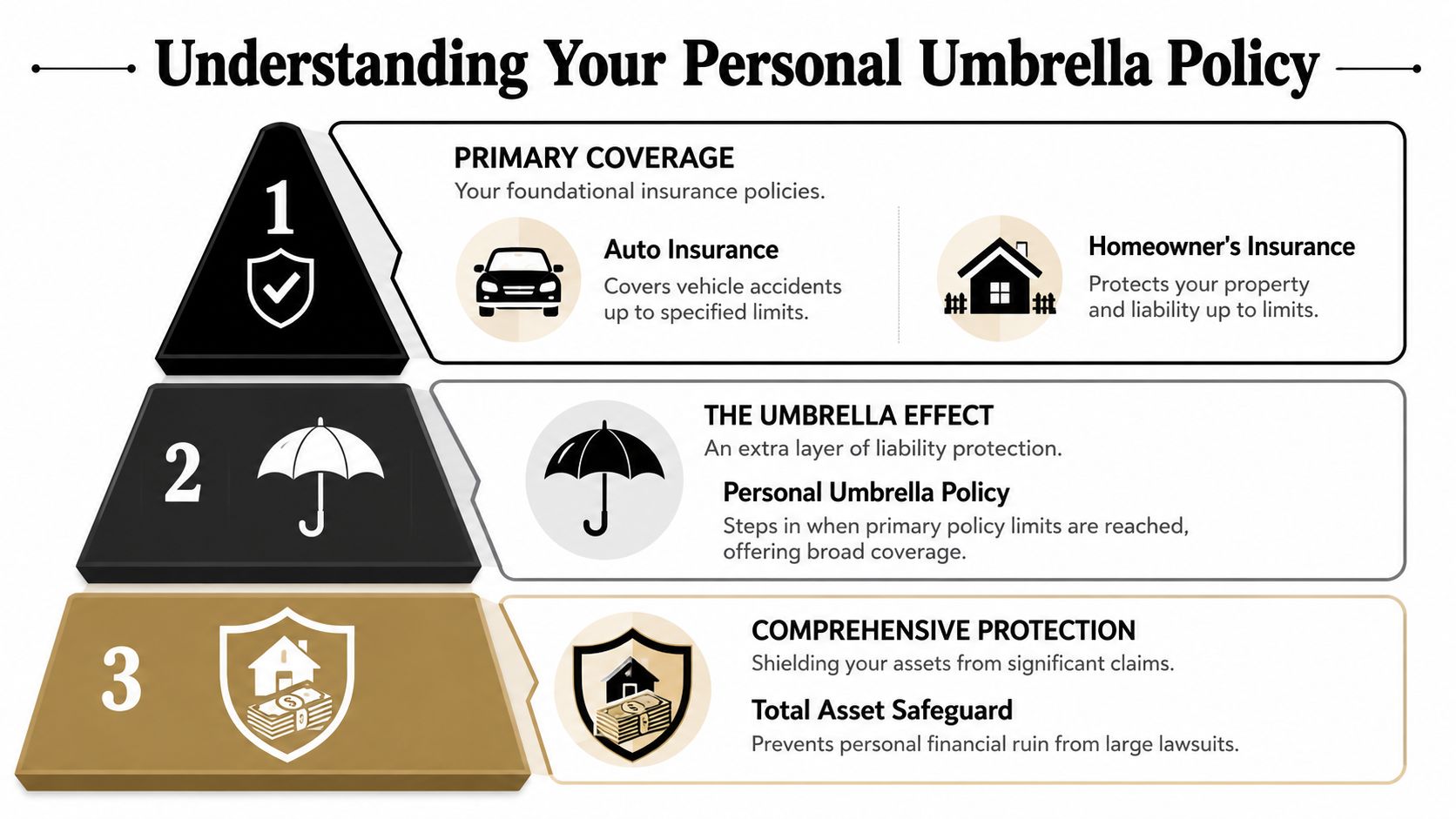

What Exactly Is a Personal Umbrella Policy

A personal umbrella policy is an extra layer of liability insurance that sits above certain policies you already have, such as auto, homeowners, renters, and sometimes watercraft or landlord coverage. Think of your primary policies as the first roof over your head. The umbrella opens only when that first roof has already taken all it can.

What it does

In plain English, the umbrella is designed to help pay when you're legally responsible for major damages and the liability limit on the underlying policy has already been used up. That can involve bodily injury, property damage, and in some cases personal injury claims such as libel or slander, depending on the policy language.

If you want a plain-language legal overview before getting into umbrella details, this explanation of understanding liability insurance is a useful starting point because it helps clarify what liability coverage is designed to do when someone claims you caused harm.

What it is not

Avoid a common misunderstanding: An umbrella policy is not:

- Property insurance for your home: It won't rebuild your roof or replace your furniture after a covered property loss.

- Health insurance for you or your family: It doesn't pay your own medical bills because you were injured.

- A substitute for primary insurance: It works above your base policies, not instead of them.

- Business coverage: If the claim grows out of a business or side hustle, a personal umbrella may not respond.

Practical rule: Buy an umbrella to protect assets from large liability claims, not to fix gaps in property or business insurance.

Why people buy it

The practical value is asset protection. A major claim doesn't stop at what's in your checking account today. It can threaten investment accounts, exposed property, and future income. The umbrella gives you a bigger liability backstop so a severe claim is more likely to stay inside the insurance tower instead of spilling over into your personal finances.

In Florida, that matters because many households have a mix of risks. Two cars, one teen driver, a pool, a rental condo, or a boat can all change the severity of a claim quickly. Umbrella coverage is built for severity, not routine fender-benders or small incidents.

How an Umbrella Policy Works with Your Existing Coverage

People often buy umbrella insurance because the concept makes sense, then still ask the right question: how does it pay in a real claim?

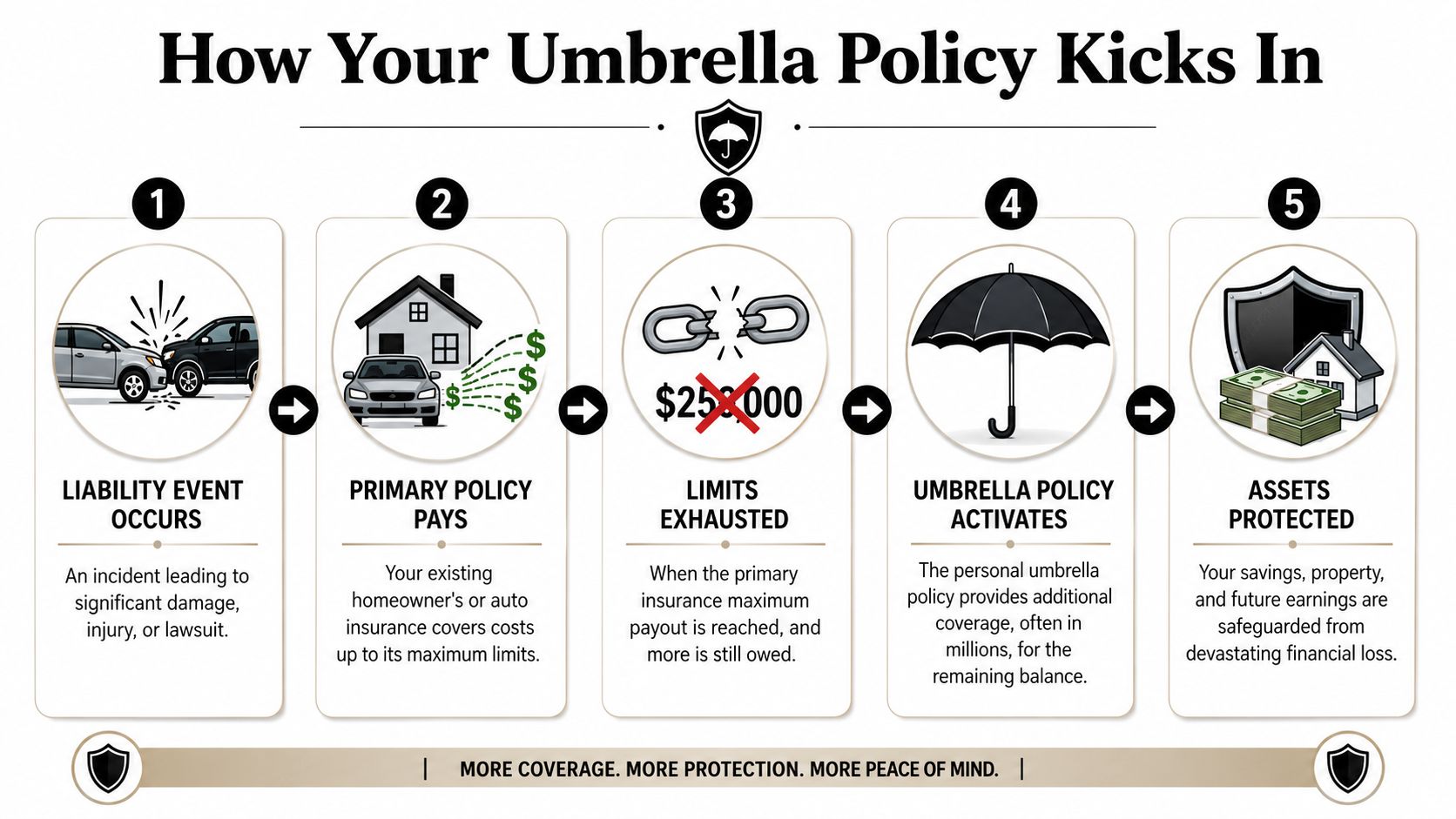

The key is this. A personal umbrella policy is an excess-liability layer. It attaches only after the liability limits on the underlying auto, homeowners, renters, or landlord policy are exhausted. Some carriers also require minimum underlying liability limits before they'll issue the umbrella at all, and some expect auto and homeowners liability to be at least $250,000 to $300,000 before the umbrella will drop down as excess coverage, as explained by Amerus Financial's umbrella coverage overview.

A simple claim flow

Here's the practical sequence:

An accident or incident happens.

A serious auto crash, a pool injury, or a guest's fall leads to a claim or lawsuit.Your primary policy responds first.

Your auto or home liability coverage handles the defense and pays covered damages up to its stated limit.That primary limit gets used up.

If the covered damages and legal costs continue beyond that amount, your base policy has reached its ceiling.The umbrella takes over above that point.

If the claim is covered and the underlying requirements were met, the umbrella provides the next layer of liability protection up to its own cap.Your assets are less exposed.

The point of the umbrella is to absorb that excess portion before creditors or plaintiffs look beyond insurance proceeds.

Why the underlying limits matter so much

This is the part people tend to underestimate. Buying a large umbrella doesn't help if your underlying policies are too low for the carrier's requirements or aren't aligned properly. Carriers want to see strong base limits because the umbrella is supposed to sit on top of solid primary coverage, not rescue a thin policy structure.

If you need a better grounding in auto liability before reviewing an umbrella, this guide on car insurance liability explained is worth reading alongside a review of full coverage vs liability, since many buyers confuse physical damage protection on their own vehicle with liability protection for injuries and damage they cause to others.

The umbrella is only as useful as the policies underneath it. Weak primary limits can create the wrong kind of surprise at claim time.

What works and what doesn't

What works is coordinated planning. Your auto, home, rental, and watercraft liabilities should match the umbrella carrier's requirements and be reviewed together.

What doesn't work is treating umbrella insurance like a stand-alone product. It isn't. It's more like the top floor of a building. If the lower floors aren't built correctly, the top floor can't do its job.

Florida Umbrella Policy Costs and Coverage Requirements

For many Florida households, umbrella insurance is one of the more cost-efficient ways to buy meaningful liability protection. The surprise usually isn't the price. It's that more people don't buy it sooner.

Florida-specific guidance commonly cites these underlying requirements for umbrella eligibility: $250,000 per person and $500,000 per accident in bodily injury liability on auto, plus $300,000 in homeowners liability coverage. The same Florida guidance also notes that a $1 million personal umbrella is often quoted around $150 to $400 per year, and that many households buy between $1 million and $5 million in limits depending on their risk profile, according to GreatFlorida's umbrella policy discussion.

Sample annual premiums for personal umbrella insurance in Florida

| Coverage Amount | Typical Annual Premium Range |

|---|---|

| $1 million | $150 to $400 |

That table is intentionally short because that's the verified premium range available. Once you move above the entry limit, pricing becomes more individualized based on the carrier and the household exposures involved.

Who should look closely at an umbrella

The strongest candidates usually include:

- Homeowners with savings or equity: A lawsuit doesn't care whether you consider yourself affluent. If you've built assets, you have something worth protecting.

- Parents of teen drivers: Teen drivers can create severe exposure in one accident, even when they're generally responsible kids.

- Pool or boat owners: Florida households often carry recreational risks that increase injury severity.

- Landlords and owners of additional property: More premises usually means more opportunities for a liability claim.

- Higher earners: Even if much of your balance sheet is protected by law, future income can still be a target in some situations.

The trade-off most people miss

An umbrella may be affordable, but it can require raising your underlying liability limits first. That means the real decision isn't just whether you want an umbrella. It's whether you're willing to carry the stronger auto and home liability foundation that makes the umbrella valid and effective.

That's usually the right move. A large umbrella sitting above weak primary coverage is a planning mistake. A properly structured liability stack is what protects assets well.

Real-Life Scenarios Where an Umbrella Policy Is Crucial

The easiest way to understand umbrella coverage is to stop thinking about insurance products and think about households.

Teen driver and a chain-reaction crash

Your teenager is driving home from school in heavy traffic. One bad decision, one delayed stop, and several vehicles are involved. Multiple people claim injuries. One person misses work. Another hires an attorney quickly. Your auto policy responds first, but the claim doesn't stay small just because the crash looked minor at the scene.

That's when an umbrella can keep a family from negotiating the difference between “insured” and “personally exposed.” Parents often focus on whether the teen is listed properly on the auto policy. That matters. But the bigger issue is whether the household's liability structure can handle a severe loss.

Guest injury at a pool party

A friend comes over for a birthday party. People are outside, kids are running around, and someone suffers a serious injury near the pool area. It may involve a slip, a dive, horseplay, or an allegation that supervision or maintenance was inadequate. Once medical treatment, lost income, and legal allegations stack up, homeowners liability can come under pressure fast.

Florida homes with pools create exactly the kind of severity risk umbrella insurance is designed for. The accident may happen in seconds. The lawsuit can hang around for much longer.

Most liability disasters don't look dramatic when they begin. The money risk shows up later, after attorneys and medical records enter the picture.

An online comment becomes a legal problem

This one catches people off guard. A homeowner posts a harsh review, writes a heated neighborhood social media comment, or repeats an accusation online. The other person claims defamation and sues. Not every umbrella policy handles personal injury allegations the same way, but some are broader than people expect.

The lesson isn't that every online dispute is covered. It's that liability exposure now includes digital behavior, not just car accidents and slip-and-falls. A smart coverage review looks at how you live, drive, host, post, and own property.

What these scenarios have in common

Each example starts with a different trigger. A vehicle, a property condition, a social interaction. But the financial pattern is the same:

- A claim turns serious

- Primary liability coverage responds first

- Damages may exceed standard limits

- The umbrella can protect the gap

That's why asset protection planning in Florida can't stop with the words “I already have insurance.”

How to Get the Right Umbrella Policy with Select Insurance Group

Buying umbrella coverage gets easier when you approach it like a liability audit instead of a quick add-on.

Start with your exposure list

Before you ask for quotes, list the things that create liability in your household. Include drivers, vehicles, homes, rental property, pools, boats, dogs, and any regular hosting activity. If an insurer is evaluating whether to offer umbrella coverage, these details matter more than broad assumptions about your income or lifestyle.

Review your current liability limits

Pull the declarations pages for your auto, homeowners, renters, landlord, and watercraft policies if you have them. The first question isn't “How much umbrella should I buy?” It's “Do my current policies meet the required underlying limits?”

If they don't, raise those first. Otherwise, you're shopping for a top layer before the lower layers are built correctly.

Work with an independent agency

An independent agent provides significant value. Different carriers look at drivers, homes, and recreational exposures differently, and umbrella rules aren't identical across the market. If you want a quick primer on how that shopping process works, this overview of what an independent insurance agency is explains why many buyers prefer someone who can compare more than one insurer.

Select Insurance Group, Inc. is one example of an independent agency that can compare multiple carriers for personal umbrella coverage and check whether your underlying auto and home policies line up with carrier requirements.

A practical buying checklist

- Estimate what you're protecting: Think in terms of assets, earnings, and anything a plaintiff's attorney would see as collectible.

- Fix weak base limits first: Umbrella coverage depends on the policies underneath it.

- Disclose exposures clearly: Pools, teen drivers, boats, and rental property shouldn't be surprises later.

- Ask about exclusions: Don't assume a side hustle, board role, or online claim is covered.

- Match coverage to reality: The right umbrella limit should reflect how you live, not just what feels comfortable.

A good umbrella policy isn't the biggest one on paper. It's the one that fits your full risk picture and coordinates properly with the rest of your insurance.

Frequently Asked Questions About Florida Umbrella Insurance

Does a personal umbrella cover my small business or side hustle

Usually, you should assume no unless the policy specifically says otherwise or an endorsement changes that result. Personal umbrella policies are designed for personal liability exposures. If you run a business from home, sell products, manage clients, or use personal property for business purposes, those facts can trigger exclusions.

A separate business policy is often the cleaner solution.

What are the common exclusions people overlook

The biggest mistakes usually involve assuming the umbrella covers everything serious. It doesn't. Common problem areas can include business activities, intentional acts, certain professional services, and liabilities tied to vehicles or watercraft that aren't properly scheduled or insured underneath.

The safe approach is simple:

- Read the exclusions section

- Check the definitions

- Ask how your real activities fit the form

Will it protect me if I serve on a nonprofit board

Maybe, but don't assume your personal umbrella is the first or best protection for that role. Board service can involve a separate liability structure, and many nonprofits carry their own directors and officers coverage. Your umbrella may not be designed for claims arising from organizational decisions or governance disputes.

This is one of those areas where policy language matters more than assumptions.

If a role, asset, or activity sits even halfway between personal and business use, ask the question before a claim happens.

Does it cover incidents while I'm traveling internationally

Some personal umbrella policies can extend to covered personal liability claims that arise outside the United States, but the answer depends on the carrier form and the facts of the incident. Travel itself isn't the deciding factor. The issue is whether the event fits the policy's covered liability grant and doesn't fall into an exclusion.

If you travel often, ask for that point to be reviewed specifically.

Does an umbrella policy cover hurricane damage

No. Umbrella insurance is liability coverage, not property coverage. It's there for claims that you caused injury or damage to others and those losses exceed your underlying liability limits.

If a hurricane damages your home, roof, or personal belongings, that question belongs under homeowners, wind, flood, or renters coverage depending on the loss.

How much umbrella coverage should I buy

There isn't a universal answer. Florida guidance commonly notes that many households purchase between $1 million and $5 million in umbrella limits depending on assets and exposures such as teen drivers, pools, boats, or rental properties, as noted earlier in the article. The right amount should reflect what you own, what you earn, and how much liability risk your household creates.

If you own little, rent an apartment, and have a simple risk profile, the answer may be modest. If you own property, host guests, or have younger drivers in the household, the conversation changes quickly.

Is a personal umbrella policy for asset protection FL worth it if I already have strong base coverage

Often, yes. Strong base coverage is necessary, but it may still not be enough for a severe claim. The umbrella exists for the uncommon event that creates outsized financial exposure.

That's the point. You're not buying it for the claims that stay small.

If you want help reviewing whether a Personal umbrella policy for asset protection FL makes sense for your household, Select Insurance Group, Inc. can help compare underlying liability requirements and available umbrella options across multiple carriers so you can see how the pieces fit before you make a decision.