You bring the baby home, set the car seat by the door, and realize your financial life changed overnight. The same thing happens when you sign for a first home, take on daycare, or start relying on one income while the other parent cuts back at work. The question isn't abstract anymore. It's simple and uncomfortable: if one of you dies, how does the other keep everything standing?

Most young parents assume life insurance will be expensive, complicated, or something to handle later. In practice, Affordable term life insurance young families can buy is often much simpler than people expect. The right policy isn't about fancy features. It's about making sure your partner can cover the mortgage, keep food on the table, and buy time to recover without financial panic.

Protecting Your Future Without Breaking Your Budget

A lot of families I talk to are already stretched. Mortgage payment. Rent. Formula. Diapers. Daycare. Car payment. Student loans. There isn't much patience for another bill unless it solves a real problem.

That's why term life insurance works so well at this stage. It gives you a large death benefit for a set period, without the higher cost that comes with permanent coverage.

Published market examples make the affordability point clearly. Aflac lists average premiums for a 20-year, $500,000 term policy at $26.98 per month for a 25-year-old man and $20.92 per month for a 25-year-old woman, and Policygenius reports that a healthy 30-year-old can often find a $500,000 policy for around $23 to $30 per month, as summarized by MassMutual's guide for new parents.

What that monthly premium is really buying

You're not buying an investment product. You're buying breathing room for the people who depend on you.

That money can help your family handle things like:

- Housing costs: Keeping up with the mortgage or rent

- Daily bills: Groceries, utilities, insurance, transportation

- Child-related expenses: Daycare, school costs, routine family spending

- Outstanding debt: Car loans, student loans, credit balances

Practical rule: Young families usually need protection when their cash flow is tightest, not when life finally feels settled.

For some families, term coverage is also part of a broader estate planning conversation. If you want to understand how proceeds may be handled in a trust arrangement, this overview of a life insurance trust in Texas gives a useful legal perspective.

Why waiting usually costs more

The biggest mistake I see isn't buying the wrong policy first. It's waiting because life feels too busy. Young, healthy applicants usually have the easiest path to affordable rates. Once a diagnosis appears in the medical record, or stress starts showing up in blood pressure and lab work, the conversation can change quickly.

If you've got a young child, a partner who depends on your income, or a home loan with your name on it, this isn't a "someday" task. It's a current household responsibility.

Why Term Life Is the Smart Choice for Young Families

When parents first shop for life insurance, they usually run into two lanes. Term life and permanent life. For most young families, the practical choice is term.

The reason is straightforward. Your biggest financial obligations usually aren't lifelong. They're concentrated in a window. You're raising children, paying down a mortgage, and trying to protect income while your family still depends on it.

Buy coverage for the years that matter most

Policygenius puts it well. Term life is a fit for many young adults because it "only lasts during the period of your life when you have the biggest expenses," such as raising children. Their explanation also notes that term options commonly run 10, 20, or 30 years, which lets families match coverage to the period of highest financial dependency in their life insurance guide for young adults.

That structure is exactly why term works. You can line the policy up with real milestones instead of paying for features you may not need right now.

A simple comparison that helps

| Coverage type | What it does best | Main trade-off |

|---|---|---|

| Term life | Covers a specific period when children are young and debts are high | Coverage ends after the term |

| Permanent life | Provides lifelong coverage and may include cash value | Premiums are typically much higher |

Think of term insurance as renting protection during your highest-risk financial years. That isn't a weakness. For many households, it's the smartest use of limited dollars.

If your priority is maximum protection on a young family budget, term usually solves the right problem.

When permanent insurance might come up

Permanent coverage has a place. Some households want lifelong coverage. Others are planning around estate issues or long-term dependents. But that's a separate conversation from the question most young parents are asking, which is, "How do I protect my family right now without crushing the budget?"

For that question, term life usually wins on clarity, affordability, and fit.

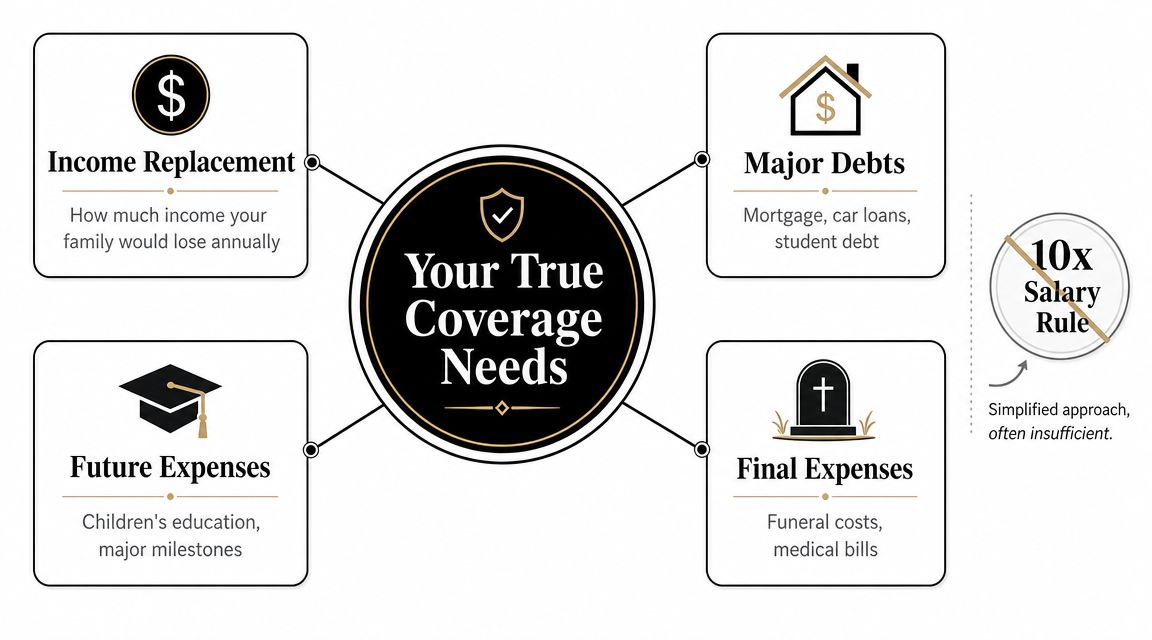

Calculating Your True Coverage Needs

The old 10x salary rule is easy to remember, but it can be a bad fit for real families. A couple with a big mortgage, daycare bills, and one primary earner has a different risk profile than a debt-free couple with no children. A rule of thumb can't see that.

A stronger method is a coverage stack. Instead of guessing from income alone, you total the actual obligations your family would face if your paycheck stopped.

Many family finance guides don't move past the salary multiple approach. A more accurate method is to build a coverage stack around liabilities like mortgage balances, childcare costs, and student loans, as discussed in this young families term life overview from Olde Raleigh Financial.

Use the DIME framework

I like to keep it simple with DIME.

Debts

Start with non-housing debts. Car loans, personal loans, student loans, and credit card balances all belong here. If your spouse would have to pay it after your death, count it.Income

This is the money your family would need replaced for a period of time. Don't overcomplicate it. Ask what your household would need to keep functioning while the surviving parent adjusts.Mortgage

Some families want the house fully paid off. Others just want enough coverage to keep payments manageable. Either approach can work, but be intentional.Education

If you want to set aside money for college, trade school, or future child expenses, include that in the stack. This is often where families realize the generic salary rule is missing a major goal.

A practical way to build your number

Use this checklist:

- List every debt your family would still owe if you died.

- Estimate income replacement based on how much of your earnings the household uses.

- Add the mortgage need based on whether you want payoff or support.

- Include future child costs that matter to you, especially education.

- Add final expenses so your family isn't paying urgent costs out of pocket.

A good life insurance number should match your household balance sheet, not a slogan.

What works and what doesn't

What works is building from actual obligations. What doesn't is buying the smallest policy that feels comfortable today, then hoping it's enough later.

A lot of underinsurance starts with one thought: "We'll just get something in place for now." The danger is that later coverage may cost more, or health changes may limit your options. Buying too little can feel affordable at first and expensive when your family needs the protection.

If you're between two coverage amounts, I usually tell families to decide based on the stack, not emotion. The more your household depends on one income, the less room there is for guesswork.

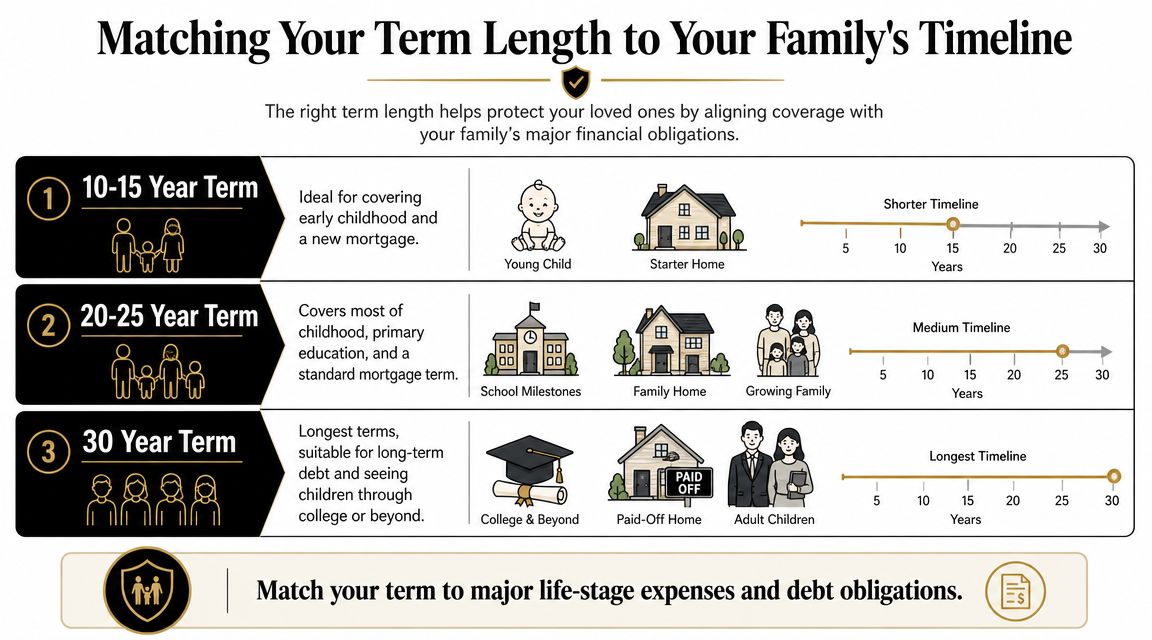

Matching Your Term Length to Your Family's Timeline

Getting the amount right is only half the job. You also need the policy to stay in force for the years your family is most exposed.

Many buyers cut corners. They choose the shortest term because the price looks better, then discover the policy may end while the mortgage is still large or while the kids still need support.

Match the term to the obligation

A useful way to think about term length is to line it up with your longest major responsibility.

| Term length | Often fits families who need to cover | Main concern |

|---|---|---|

| 10 years | Shorter debt windows or older children | May expire too early |

| 20 years | Much of child-rearing and a large portion of mortgage years | Can still fall short for newborn-stage families |

| 30 years | New mortgage, very young children, longer dependency window | Higher premium than a shorter term |

A family with a newborn and a brand-new home loan often needs a longer runway than they first assume. A family with teenagers and fewer years left on the mortgage may be fine with less.

Don't buy a term that ends before the risk does

A short term can look efficient on paper. But if your child is still in school or your spouse still depends heavily on your income when that policy ends, you haven't really solved the problem.

The right term isn't the cheapest option. It's the one that still protects your family when the financial consequences would be worst.

I generally tell parents to look at two dates. When will the youngest child likely be financially independent? When will the mortgage become manageable or be mostly paid down? Your term should stretch across the later of those two milestones, not the earlier one.

Choosing a slightly longer term is often the safer move when the budget allows it. The extra premium can be worth it if it keeps you from facing a costly reapplication later in life.

Simple Steps to Lower Your Life Insurance Premiums

There are only a few levers that reliably lower life insurance cost. The biggest one is timing. Age and health matter at application, and insurers price accordingly.

That means the cheapest time to buy is often before a family thinks it has time to buy. Waiting until after a major life event can narrow your options fast.

Apply before life gets more complicated

Consumer guidance on younger buyers makes this point clearly. Premiums are based on your age and health when you apply, and buying before a major life event, such as a new diagnosis or pregnancy, can help lock in lower rates, according to AAA's explanation of why buying term life early matters.

That advice matters for young parents because family life rarely gets less complicated. It usually gets busier.

A short checklist that actually helps

- Buy while you're healthy: If you're in decent shape today, don't wait for a calmer season. Calm seasons rarely arrive on schedule.

- Be honest on the application: Underwriters verify information. Incomplete or misleading answers create problems.

- Manage health issues early: If you've been told to address blood pressure, weight, or follow-up care, do it before applying if time allows.

- Avoid shopping based on price alone: A cheap quote that assumes a better health class than you'll receive isn't a useful quote.

- Keep your records organized: Medication lists, doctor information, and basic health history can speed up the process.

One point that surprises some applicants is how many insurance decisions depend on details from everyday life. Even outside life insurance, insurers price risk based on records and history. If you're curious how a separate line of coverage weighs driving violations, this guide on how long traffic tickets affect insurance is a helpful example of how timing and rating factors can affect premium.

What doesn't help

What usually doesn't work is waiting until after the baby arrives, after a move, after a job change, or after medical testing you've already been putting off. Parents often think they'll apply when life stabilizes. In reality, underwriting doesn't care whether your life feels organized. It cares what your file looks like on the day you apply.

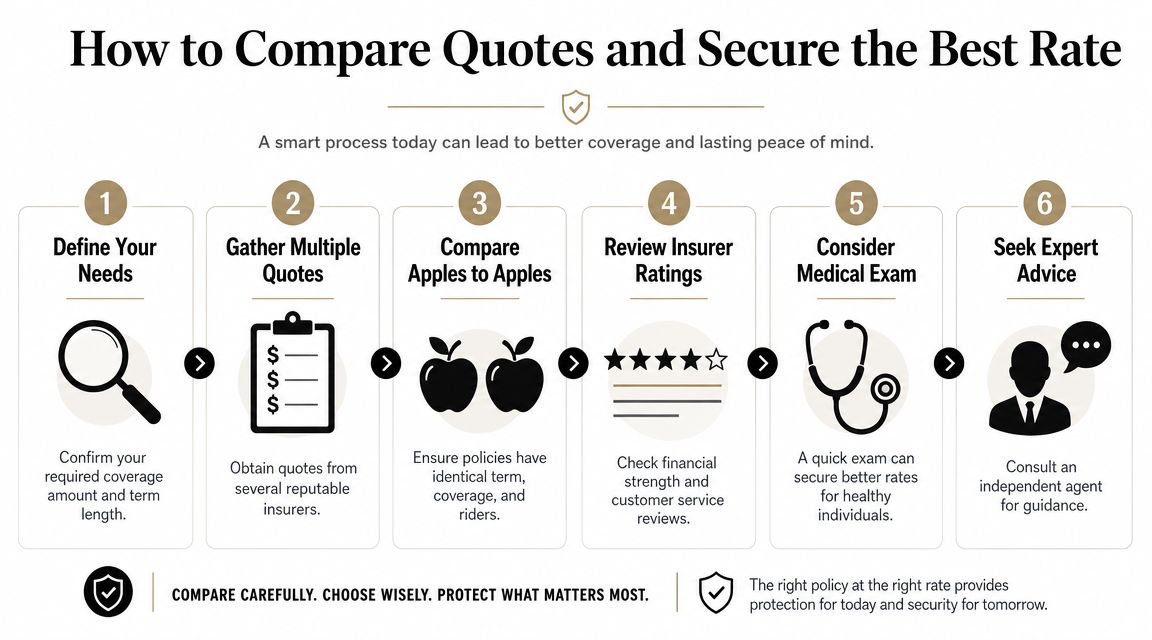

How to Compare Quotes and Secure the Best Rate

Once you've chosen a coverage amount and term length, quote shopping gets much easier. But people often make another common mistake. They compare prices that aren't built the same way.

One quote may be for a different health class. Another may have a shorter term. A third may come from a carrier with different underwriting assumptions. If you only compare the monthly premium, you're not really comparing policies.

Compare apples to apples

Western & Southern's guidance gets this exactly right. To find true value, you need to normalize quotes by coverage amount, term length, underwriting class, and insurer financial strength, as explained in its article on life insurance mistakes to avoid.

Here's the checklist I use with families:

- Match the death benefit across all quotes.

- Keep the term identical on each comparison.

- Confirm the underwriting class being assumed.

- Review insurer strength before treating a quote as final.

- Check riders carefully so you know what's included and what isn't.

- Ask how the quote changes if the medical results come back differently than expected.

Where an independent agent helps

This is one place where an independent agency can save time. Instead of filling out similar forms over and over, some agencies can pull quotes from multiple carriers and sort them by the structure that matters. Select Insurance Group, Inc. says it compares instant quotes from 20 to 40 carriers, which is the kind of setup that can help families review multiple options without restarting the process each time.

Cheap isn't the same as competitive. Competitive means the quote still looks good after you line up every major detail side by side.

The families who do this well usually make three decisions in order. First, they decide how much protection they need. Second, they choose a term that matches real obligations. Third, they shop carefully and compare structurally equivalent quotes. That's how you keep the premium affordable without cutting the protection your family needs.

If you're ready to price out term life coverage with real numbers instead of rough guesses, Select Insurance Group, Inc. can be a practical starting point. As an independent agency, it can help families review multiple carrier options, compare quotes on the same terms, and sort through the application process without adding more stress to an already busy season of life.