You finally get the car where you want it. The paint lays right. The idle sounds right. The stance is right. Then you drive it home from a Charlotte meet and realize the insurance card in the glove box may still be built for an ordinary used car.

That's the gap a lot of owners discover late. A classic car can look perfect, run strong, and carry years of restoration work, but a standard auto policy may still value it through a depreciation lens. If there's a serious loss, the question isn't what the car means to you. It's what the policy says it's worth.

For Charlotte owners, that matters more than most guides admit. It's not just about understanding agreed value. It's knowing how usage limits, storage expectations, documentation, and value updates affect whether that protection works when you need it.

Your Classic Car Deserves More Than Standard Insurance

A lot of classic car owners start in the same place. The vehicle is insured. The tag is current. The owner assumes that means the car is protected.

Then the details come out. The car has a rebuilt engine, custom paint, suspension work, rare trim pieces, and a folder full of receipts. The policy, meanwhile, treats it like aging transportation.

What owners feel in the real world

At a cars-and-coffee event, nobody looks at a clean first-generation Camaro, restored C10, vintage Jaguar, or square-body pickup and thinks, “That's just an old car.” Owners know what sits in the garage. They know how hard certain parts were to source. They know what the bodywork cost, how long the drivetrain build took, and how much effort went into getting details correct.

Insurance has to match that reality.

Agreed value classic car insurance Charlotte NC searches usually come from owners who already sense the problem. They don't want broad promises. They want to know whether the policy recognizes the car's collector value instead of defaulting to used-car logic.

Practical rule: If losing the car would expose years of restoration cost, rare parts, or documented upgrades, a standard policy is usually the wrong starting point.

Why this matters in Charlotte

Charlotte has a strong mix of weekend cruisers, show cars, modified classics, and carefully preserved originals. Some owners drive across town for events. Others keep the car garaged and only bring it out on clear weekends. Those patterns fit collector coverage better than regular auto coverage, but only if the policy is set up correctly from the beginning.

That means more than buying “full coverage.” It means making sure the insured value, use of the vehicle, and supporting records all line up.

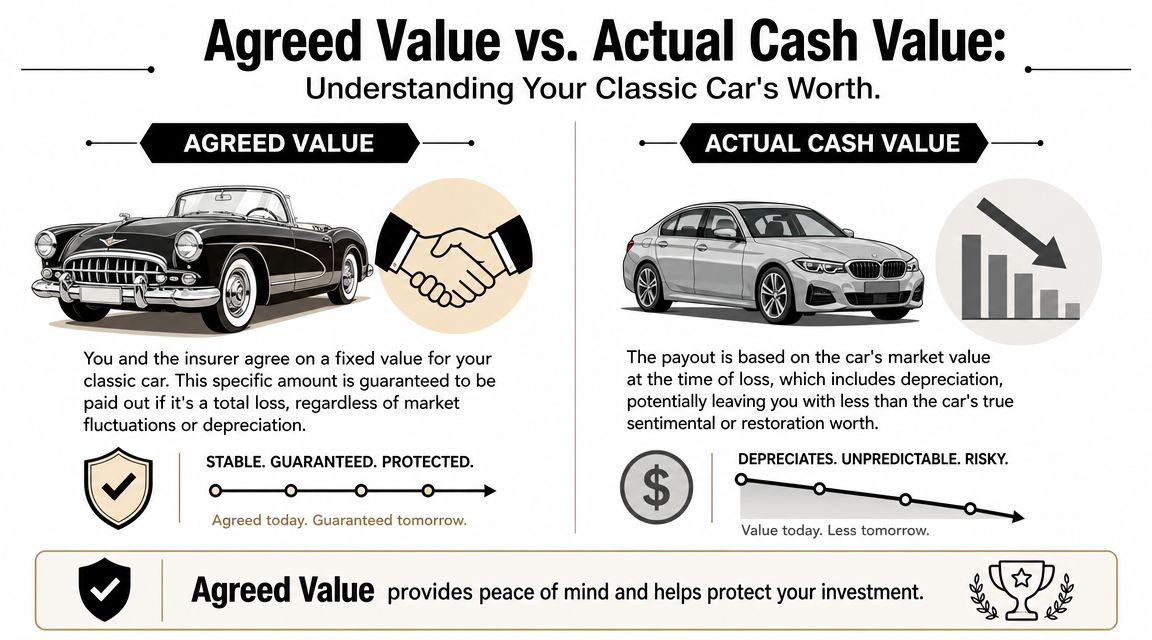

Agreed Value vs Actual Cash Value Explained

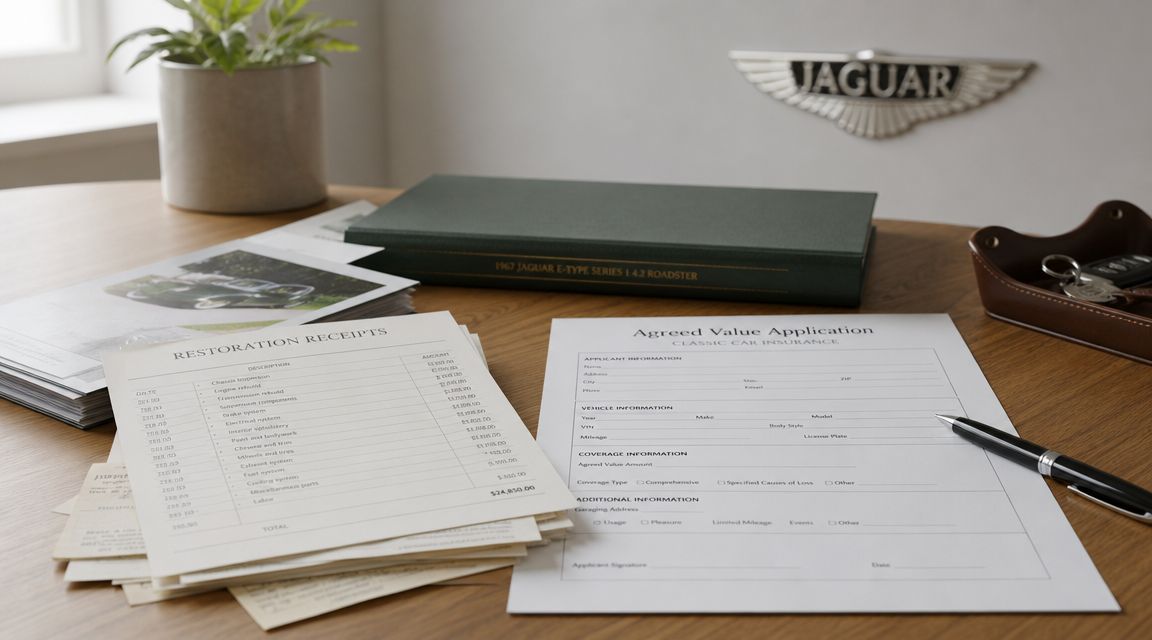

A Charlotte owner buys back a restored Chevelle after years of work, then gets rear-ended on Independence Boulevard and the car is totaled. The policy either settles on the number agreed to before the loss, or it starts arguing over what an old car was worth that day. That is the difference that matters.

Agreed value means you and the insurer set the vehicle's insured value in advance, based on records such as photos, appraisals, restoration receipts, and market support. If the car is a covered total loss, the policy pays that agreed amount, minus any deductible. The value discussion happens before the claim, while everyone is calm and the car is still sitting in the garage.

Actual cash value works the opposite way. The insurer determines what the vehicle was worth at the time of loss, usually with depreciation built into the calculation. That method makes sense for ordinary cars that lose value with age and mileage. It creates problems for classics, restomods, and collector vehicles that may hold value, gain value, or carry far more money in them than a standard pricing tool will capture.

The core difference

With agreed value, the hard work is done up front.

With actual cash value, the hard conversation often starts after the loss, when values, condition, and comparable sales are being debated under pressure. For a collector in Charlotte, that matters because local ownership is rarely static. Owners improve paint, sort drivability, replace trim, rebuild drivetrains, and buy scarce parts over time. If the insured value is never revisited, even an agreed value policy can lag behind the car's real market position.

For another practical view of how insurance valuation affects drivers, this breakdown from Total Loss Northwest is useful because it explains valuation through actual claim outcomes instead of generic policy language.

Agreed Value vs Actual Cash Value (ACV)

| Feature | Agreed Value | Actual Cash Value (ACV) |

|---|---|---|

| How value is set | Set in advance between owner and insurer | Determined at time of loss |

| Depreciation | Not based on post-loss depreciation | Includes depreciation |

| Total loss payout | Pre-set amount, minus deductible | Current depreciated value at loss time |

| Best fit | Classic, antique, collectible, or appreciating vehicles | Standard daily-use vehicles |

| Documentation needed | Usually stronger proof of value | Usually less collector-specific proof |

| Owner concern | Keeping the agreed figure current as the car and market change | Avoiding undervaluation after a loss |

Where owners get tripped up

Owners often hear "agreed value" and assume every part of the claim will be simple. The valuation method helps, but it does not override the rest of the contract. Usage limits, storage requirements, driver eligibility, deductible choices, and parts coverage still matter.

That point gets missed in a lot of online guides. In Charlotte, many classics are driven more than owners first expect. They go to Matthews, Concord, Lake Norman events, service appointments, club cruises, and weekend dinners when the weather is good. If the policy was priced for limited hobby use but the actual pattern looks closer to regular transportation, the value clause alone will not fix that mismatch.

There is also an inflation issue that owners should watch closely. A value agreed on three years ago may no longer reflect what it would cost to replace the car or duplicate the work already done. Good collector coverage needs periodic review, especially after a fresh appraisal, a major mechanical build, new paint, or a noticeable shift in the collector market.

If you are also sorting out the broader difference between physical damage protection and state minimum coverage, this guide to full coverage vs liability insurance gives useful context before you compare collector policy forms.

Why Standard Policies Fail Charlotte's Collectors

A Charlotte owner finishes a five-year restoration, drives the car to a Saturday meet, and gets hit on the way home. The problem with a standard auto policy shows up right then. The carrier often handles the car like older transportation, even if the owner has treated it like a collectible asset with documented money in the drivetrain, paint, interior, and parts sourcing.

That gap is larger here than many owners expect. Classic cars around Charlotte do not just sit under covers. They go to local shows, tuning shops, alignment appointments, club events in Concord and Mooresville, and occasional dinner runs when the weather is right. A standard policy is built around ordinary depreciation and everyday use assumptions. Those assumptions do a poor job with a collector car whose value depends on condition, rarity, provenance, and the quality of the work done.

What a standard policy usually gets wrong

Actual cash value claims are often centered on age, mileage, and broad market comps. For a late-model daily driver, that approach is normal. For a classic, it can miss the parts of the car that took the most time and money to get right.

Here is where owners feel the shortfall:

- Restoration labor often gets discounted: Hours spent on body alignment, trim fit, wiring correction, and drivability sorting do not always show up well in standard valuation tools.

- Parts availability changes the math: Rare original pieces, date-correct components, and quality reproduction parts can cost far more than a typical adjuster expects.

- Modifications are not valued evenly: A well-executed engine build, suspension upgrade, or paint job may help market value, but a standard policy may treat it as money spent, not value added.

- Condition matters more than age: Two cars with the same year and model can be worlds apart in value if one is garage-kept, documented, and freshly sorted.

I see this mistake most often after owners assume liability limits and collision coverage are the hard part. They are not. The hard part is making sure the carrier insures the car you own, not a generic version of it.

There is also a Charlotte-specific trade-off that many online guides skip. Owners want to drive their classics. Insurers want usage patterns that stay inside collector guidelines. If the car starts being used for errands, commuting, or regular transportation, a standard policy still may not value it correctly, and a collector policy may have usage concerns of its own. Good advice matters here. Working with an independent insurance agency that can compare collector carriers helps owners match the policy form to how the car is stored, driven, and maintained.

Why collectors get burned by ordinary depreciation

Ordinary auto insurance assumes a car loses value as it gets older. Collector cars do not follow that pattern consistently. Some appreciate. Some hold steady because the restoration quality is strong. Some rise sharply after a fresh appraisal or after the market starts rewarding a specific model, body style, or drivetrain combination.

That is why a standard policy can fail even when the premium looks reasonable. It may satisfy the basic insurance requirement, but it often leaves the owner arguing about value after a major loss. For a collector in Charlotte, that is the wrong time to find out the policy was built for transportation value instead of investment protection.

Qualifying for Agreed Value Coverage in North Carolina

A Charlotte owner buys back the same Chevelle he sold years ago, puts real money into paint and drivetrain work, and wants the policy to reflect what the car is worth now. That part is possible. The harder part is meeting the collector carrier's rules on value support, storage, and use before the policy is issued.

Agreed value approval in North Carolina usually comes down to three questions. Can the owner support the number requested. Is the car stored like a collector vehicle. Will it be used in a way the carrier accepts. If one of those pieces is weak, the quote can still look attractive, but the fit is wrong.

What to gather before you apply

Underwriters do not want a guess. They want a file.

For a clean application, gather current photos, title and VIN details, restoration invoices, parts receipts, and any prior appraisal or valuation support that explains why your number is reasonable. Clear documentation matters even more on cars with engine swaps, paint changes, custom interiors, or upgraded suspensions, because those changes can raise value for one buyer and reduce it for another.

I also tell owners to organize the records by date and by major system. Engine, paint, interior, chassis, trim. That saves time and helps show whether the car was restored carefully or pieced together over several years.

If your car has a following tied to a specific trim or production run, model-specific documentation helps. A buyer insuring a limited-production Fox-body, for example, should understand what collectors look for in authenticity and market appeal. A Saleen Mustang collector's guide is a good example of the kind of background that can help an owner document why one version of a car commands more than another.

Usage rules matter more than many owners expect

It's often the case that many Charlotte owners misjudge the fit.

Collector carriers usually expect limited pleasure use, club events, shows, and occasional drives. They get uncomfortable when the classic becomes a backup commuter, errand car, school pickup vehicle, or regular transportation. State Farm's antique and classic car guidance outlines the kind of use restrictions owners need to review before binding coverage.

Be honest about how you drive. If the car goes to Cars and Coffee twice a month and sees fair-weather weekend miles, that is one risk profile. If you plan to take it to the office every Friday, run to SouthPark in it, and rely on it when your daily driver is in the shop, that is a different conversation.

The practical issue is not just eligibility today. It is claim friction later.

Storage and owner profile

Garage storage carries a lot of weight because it lowers theft exposure, storm damage, and avoidable deterioration. In Charlotte, that matters more than many online guides admit. Summer humidity, sudden hail, and long periods of heat can affect paint, trim, weatherstripping, and interiors. Carriers know that, and they price and qualify accordingly.

They also want to see that you have another vehicle for everyday use and a driving record that supports specialty coverage. A strong file tells the carrier the car is part of a collection or hobby, not your transportation fallback.

There is another trade-off owners miss. If your agreed value is based on today's restoration cost or market demand, revisit it regularly. Parts, labor, and collector demand change. A value that made sense two years ago may be light now, especially after a major refresh or a changing market for certain body styles and drivetrains. Working with an independent insurance agency that compares collector-car carriers helps you sort out which companies are flexible on modifications, mileage, and storage, and which ones are not.

Understanding the Costs and Value Drivers in Charlotte

A Charlotte owner buys back a freshly restored classic after paint work, updates the policy once, and assumes the number will hold. Two renewals later, labor rates are higher, parts are harder to find, and the car is worth more than the policy reflects. That gap does not show up until there is a serious claim.

Collector coverage can still cost less than a standard auto policy because the car is usually driven less and stored more carefully. Leavitt Group notes in its classic car insurance overview that annual premiums for classic policies are often lower than everyday auto coverage for that reason. Lower premium does not mean lower stakes. The whole point of agreed value coverage is to protect a specific asset with a supportable number.

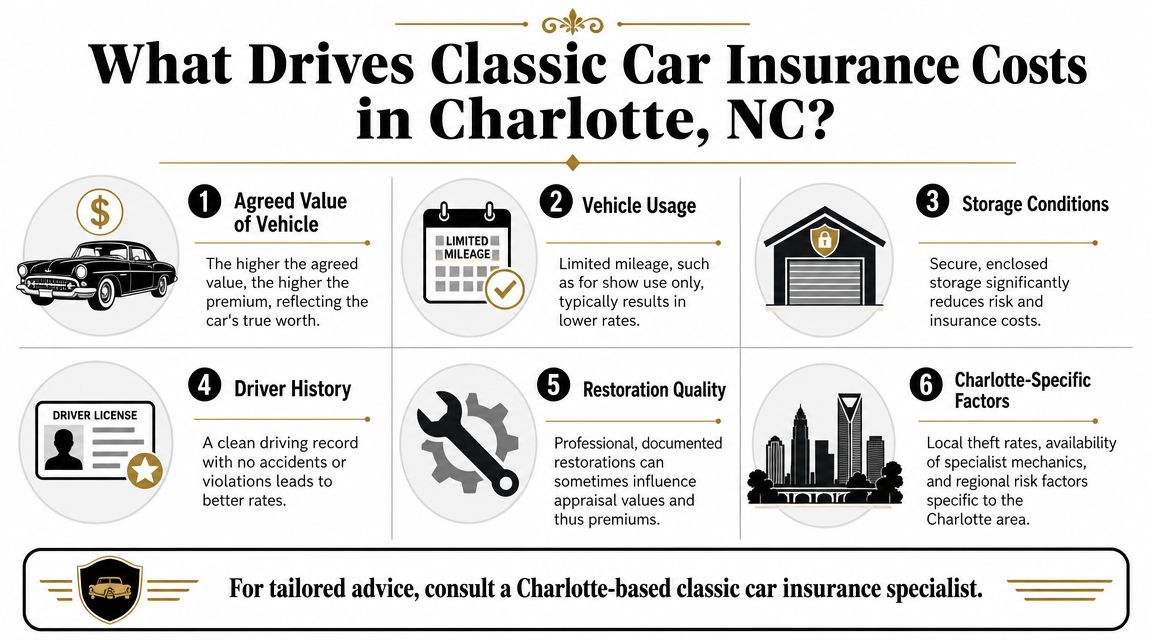

What actually drives the premium

In Charlotte, price usually follows exposure and documentation more than the age of the vehicle alone. A clean, well-kept car with a clear file often underwrites better than a more valuable car with weak records and vague usage.

The main cost drivers usually include:

- Agreed value amount: Higher limits mean the carrier is accepting a larger potential payout.

- Condition and documentation: Strong photos, appraisals, and receipts make valuation easier and reduce disputes.

- How the car is used: Occasional pleasure drives and events are different from routine trips across town.

- Where and how it is stored: A locked garage generally presents less risk than a car left under a cover or in an open carport.

- Driver history: Specialty carriers still care who is behind the wheel.

- Repair complexity: Cars that require specialty shops, rare trim, or hard-to-source mechanical parts usually bring more claim cost uncertainty.

Charlotte adds a few local realities. Hail, summer heat, humidity, and heavy traffic all affect risk in practical ways. Even if the car is not driven daily, local storage conditions and where the vehicle goes on weekends can still influence how a carrier prices it.

Inflation protection matters more than many owners expect

Agreed value is not a set-it-and-forget-it number. It should be reviewed whenever the market moves, the car gets upgraded, or restoration costs change.

Some collector policies include inflation guard features that automatically increase the insured value over time where approved. That can help, but it is not a substitute for a real review. If the car had major mechanical work, fresh paint, or a documented upgrade to originality, the file should be updated and the value should be reconsidered. Owners replacing a current policy should review how to switch auto insurance companies without creating gaps in coverage before making that change.

This issue shows up often with niche collector cars. A limited-production Mustang, for example, may look similar to a standard car to a generalist, while the collector market sees a meaningful difference in provenance, equipment, and buyer demand. A focused resource like this Saleen Mustang collector's guide helps owners document why one car deserves a different value than another.

Where owners get into trouble

Problems usually start with drift. The value drifts from the market. The usage drifts from what was disclosed. The storage arrangement changes, but nobody updates the policy.

The better approach is simple. Review the agreed value regularly, keep receipts and current photos together, and tell the carrier when the car changes in a way that affects value or use. That is how agreed value coverage stays aligned with the investment sitting in your garage.

Your Step-by-Step Guide to Securing a Policy

A Charlotte owner buys a restored Chevelle, gets a quote in ten minutes, and assumes the hard part is over. Then underwriting asks for better photos, a stated value they can defend, proof of garage storage, and a clearer answer on how often the car will be driven. That is the actual process.

Collector coverage usually goes smoothly when the owner treats the application like a file for a valuable asset. The goal is not just to get a policy issued. It is to get the right value on paper, with usage terms you can live with in Charlotte.

Step 1 through Step 3

Set a value you can support

Start with an appraisal, recent comparable sales, or other documentation that matches the car's condition, provenance, and restoration quality. The number should hold up if an underwriter asks how you got there. If you guessed high because the market feels strong, expect pushback. If you guessed low to save premium, you are the one taking that risk.Organize the file before you apply

Gather current photos, prior appraisals, restoration invoices, parts receipts, and any records that explain originality or period-correct changes. Include interior, exterior, engine bay, VIN, and anything unusual that affects value. Good documentation helps at the quoting stage and matters later if there is a dispute over what the car was before a loss.Be precise about use

Underwriters care how the car will be driven, not how you hope to describe it. Weekend pleasure use, club events, and local shows fit many collector programs. Regular commuting, school runs, and backup daily-driver use often do not. In Charlotte, I tell owners to think through the whole year, including Cars and Coffee trips, cruise-ins, parade use, and whether the car ever fills in when another vehicle is down.

Step 4 and Step 5

Compare restrictions, not just premiums.

A lower quote can cost more if the policy does not match real life. Check mileage limits, storage requirements, who is allowed to drive, deductible options, spare parts coverage, and how the carrier treats modified cars. A lightly upgraded C10 and a numbers-matching Corvette may both qualify for agreed value, but they are not underwritten the same way.

Review the terms before you bind.

Confirm the agreed value, listed drivers, garaging address, and any usage language that seems vague. Ask how often the value should be reviewed, especially if you are still putting money into the car or if the market for that model has been changing. If you are replacing an existing policy, follow this guide on switching auto insurance companies without a coverage gap so the old policy does not cancel before the new one is active.

One mistake I see often is assuming approval means flexibility later. It does not. If storage changes, if a child starts driving the car, or if the vehicle begins seeing more road time than you disclosed, update the policy while those details are still small. That is much easier than explaining them during a claim.

The practical mindset

The best applications are clear, consistent, and boring in the right way. The value is documented. The storage is settled. The usage matches the policy.

That discipline protects more than the premium. It protects the payout, the claim process, and the value of a car that may have taken years to buy, restore, and maintain.

Frequently Asked Questions About Agreed Value Claims

What happens if the loss is partial, not total

Agreed value matters most in a total loss. Partial claims still depend on the policy terms, repair scope, deductible, and how the carrier handles parts and labor. For classics, the practical issue is often repair quality and parts sourcing, not just whether coverage exists.

If the vehicle has rare or specialized components, ask before binding how the carrier handles repair approval, shop selection, and documentation for replacement parts.

How do rare parts affect a claim

Owners need patience and paperwork. Rare parts can slow the repair process because availability, originality, and condition all matter. Keep invoices, photos, and a current parts inventory for anything especially hard to replace.

The more clearly you've documented the car before the loss, the easier it is to show what belonged on the vehicle and why a generic substitute may not be appropriate.

How often should I revisit the agreed value

Review it whenever the car changes in a meaningful way. That includes restoration work, major upgrades, market shifts you can support, or a renewal where the old number no longer feels defensible.

Don't wait until after a loss to realize the policy value was stale. Agreed value is strongest when the number on the declarations page still reflects the vehicle you own today.

If you want help comparing collector-car options without guessing which policy language matters most, Select Insurance Group, Inc. can help you review agreed value classic car insurance choices, compare carriers, and make sure the policy fits how your Charlotte classic is stored, driven, and documented.