You've planned the route, checked the tires, and probably already pictured that first warm Florida morning with coffee outside the rig instead of scraping ice off the windshield. For most snowbirds, the RV itself is ready long before the insurance questions are settled.

That's where confusion usually starts.

A weekend camper can often get by with a simpler setup. A snowbird usually can't. If your RV is crossing state lines, sitting in one place for months, carrying personal belongings, and doubling as a seasonal home, full coverage RV insurance Florida snowbirds need is a different conversation from ordinary recreational use. The big blind spot I see most often isn't the drive down. It's what happens after the RV is parked.

Your Florida Snowbird Dream and the Insurance Puzzle

A lot of snowbirds start in the same place. They know where they want to stay, which park they like, and how long they expect to be in Florida. What they don't know is whether their current RV policy still fits once the trip turns into a season.

The usual question is, “I already have full coverage. Isn't that enough?” Sometimes yes. Often, not in the way people think. The answer depends on how you use the RV once you arrive. Driving into Florida for a short visit is one risk profile. Parking in a resort for months, storing gear inside, hosting guests, and maybe leaving the unit in Florida during the off-season is another.

Why snowbirds get tripped up

Insurance companies care about use. So do regulators. And Florida adds its own layer because weather exposure, theft concerns, and long-term seasonal use all matter more here than they do in many other states.

That's why a snowbird policy review should answer questions like these:

- How long is the RV in Florida: A short vacation and a seasonal stay aren't treated the same way.

- Is the RV being lived in or just traveled in: Residential use changes liability and property needs.

- Will the RV stay parked for extended stretches: Parked risk is not “no risk.”

- Are belongings stored inside: Personal property inside the rig may not be fully protected elsewhere.

If you're still deciding whether your RV setup is closer to part-time travel or something more residential, this guide to living in an RV full-time is useful because it highlights just how quickly a vehicle starts acting more like a home than a car.

Practical rule: If your RV becomes your winter address in every way except the mailing label, your insurance needs usually start moving in that direction too.

The real puzzle

Snowbirds don't just need “more coverage.” They need the right mix of driving protection, parked liability, weather protection, and storage planning. That mix is what keeps a nice winter from turning into a claim dispute.

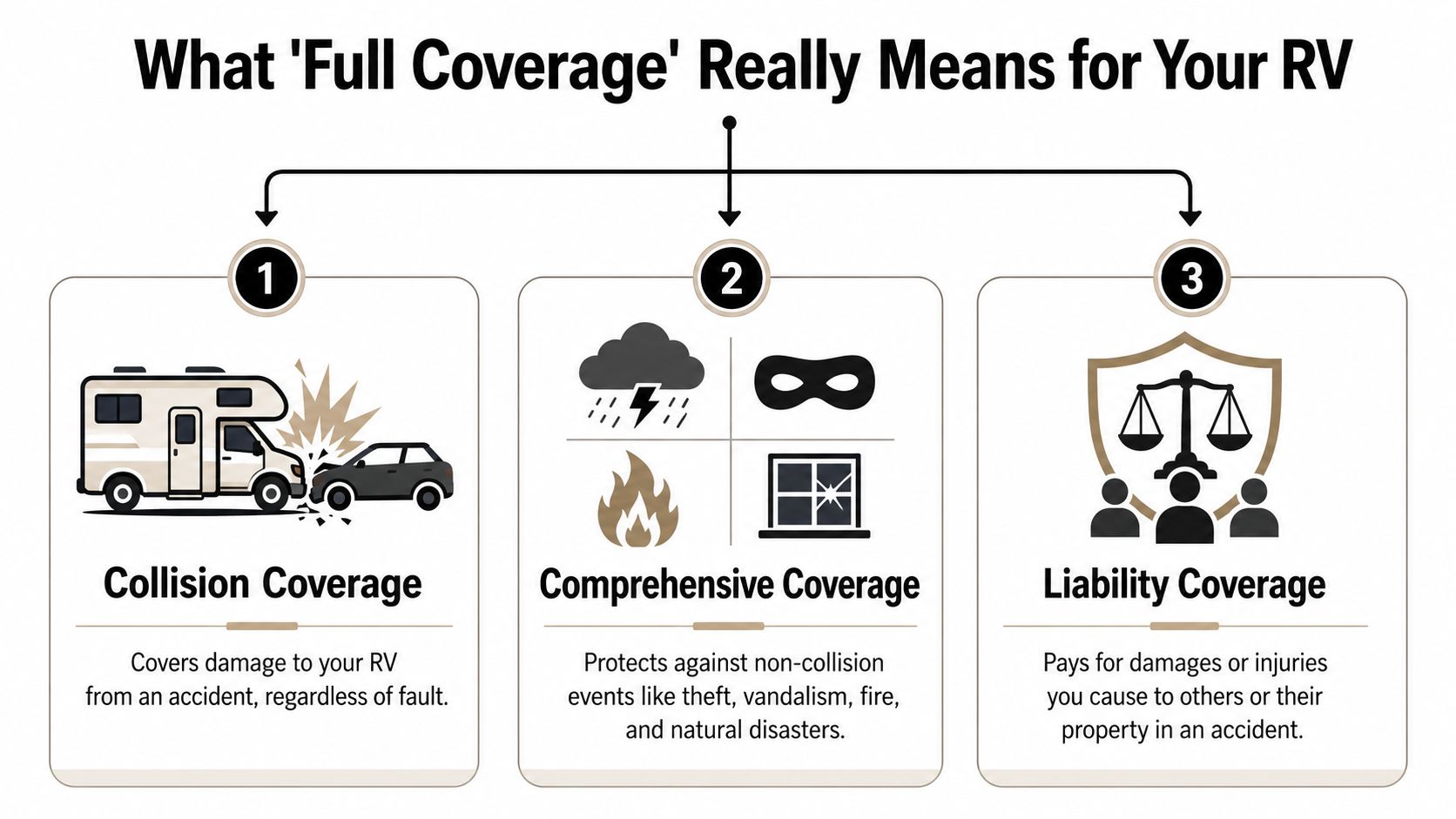

What "Full Coverage" Really Means for Your RV

“Full coverage” sounds like one product. It isn't. It's a bundle.

I explain it like this. Basic insurance is a sandwich. Full coverage is the meal with sides and a drink. You're not buying one thing called full coverage. You're combining parts that solve different problems.

Liability pays for damage you cause others

Liability is the part that protects your finances if you injure someone or damage their property with the RV. Think of it as the shield that steps in when a claim points outward, not inward.

For a snowbird, that matters while driving, backing into a site, or moving through a crowded campground. It may also matter when the RV is parked and being used more like a temporary residence, depending on the policy structure and endorsements.

Collision pays for damage to your RV after an accident

Collision is your repair fund for impact damage to the RV itself. You hit another vehicle. You clip a pole. You misjudge a turn. Collision is designed for those moments.

Many owners find out too late that “I'm a careful driver” isn't a coverage plan. Large rigs are expensive to repair, and claims don't only happen on the interstate. They happen in fuel stations, campground loops, and storage lots.

Comprehensive covers the non-collision headaches

This type of coverage is the broad “life happened” category. It usually responds to things like theft, vandalism, weather, and other non-collision damage. For Florida snowbirds, this is the pillar people most often underestimate.

RV insurance guidance notes that Florida's hurricane season runs from June through November, and standard RV policies do not automatically include hurricane coverage. Named-storm protection may need to be added through non-collision physical damage coverage or a full-timer-style policy, according to Florida RV insurance guidance on hurricane-related coverage gaps.

When an RV sits in Florida, weather becomes a property risk even when the keys aren't in the ignition.

That's the key point. A parked RV is still exposed.

What full coverage often includes beyond the core three

In practice, RV “full coverage” commonly expands beyond liability, collision, and non-collision damage. It can also include protection for personal property, vacation liability, and other RV-specific features. If you want a clean side-by-side explanation of what broad protection includes compared with minimum legal coverage, this overview of full coverage vs liability is a helpful reference.

One more issue gets overlooked until a serious claim happens: how the insurer values the RV after a total loss. If you've never had to argue over actual cash value, depreciation, or settlement language, it's worth reading this breakdown on understanding total loss valuations.

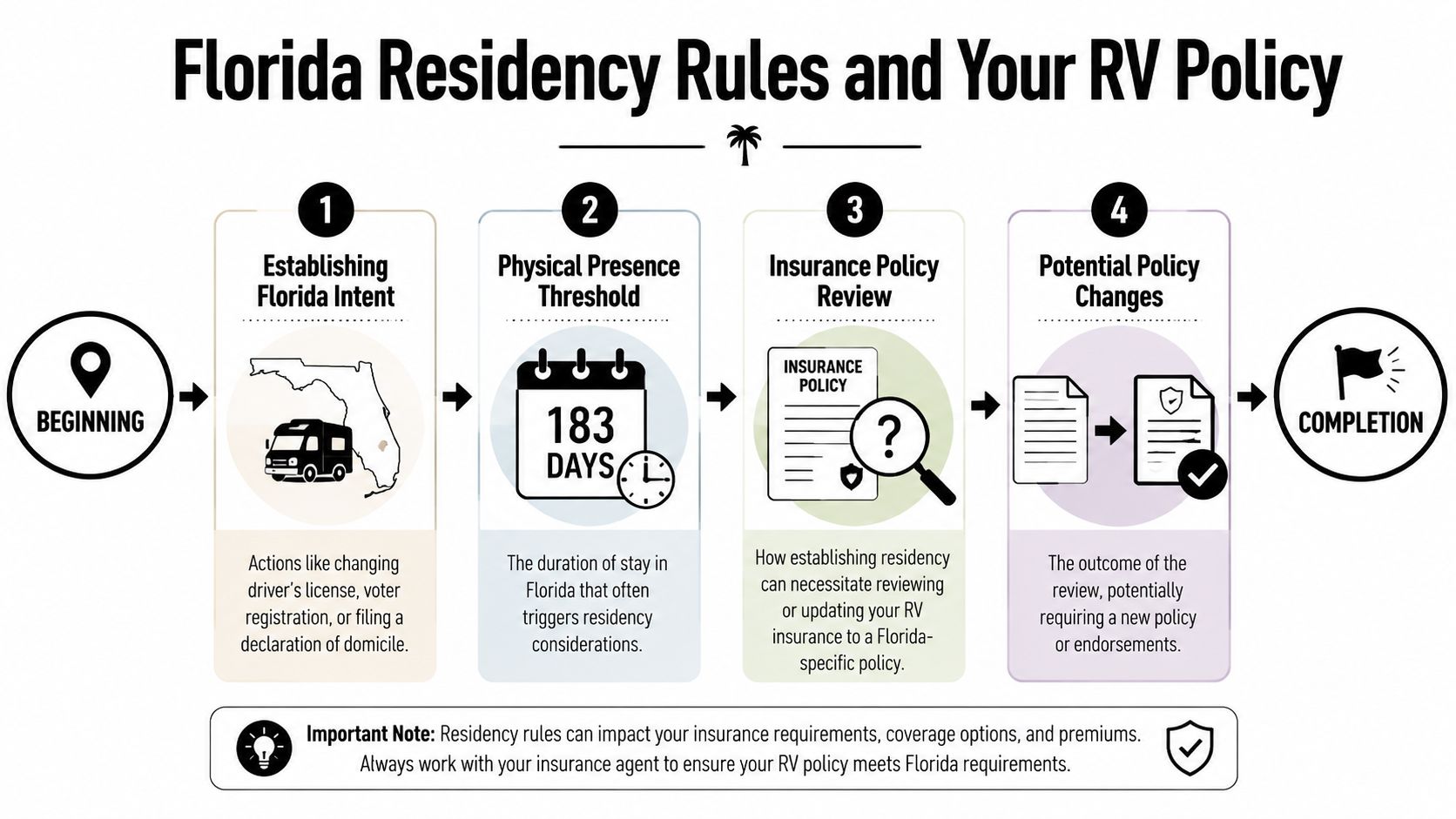

Florida Residency Rules and Your RV Policy

A lot of snowbirds focus on where they're sleeping. The legal question is where the RV is being treated as a vehicle for registration and insurance purposes.

That distinction matters because you can keep an out-of-state driver mindset while the state starts looking at the RV differently.

The trigger that catches snowbirds off guard

For Florida snowbirds, the key issue is whether the vehicle becomes subject to Florida registration and insurance rules. Nonresident vehicles physically present in Florida for more than 90 days in the preceding 365 days can fall under the state's continuous-security concept, which can create a compliance problem for owners relying on an out-of-state policy, as explained in this summary of Florida RV insurance requirements.

That doesn't mean every long stay automatically creates the same result in every situation. It does mean you shouldn't assume your home-state policy remains untouched just because you personally still consider yourself a visitor.

What this means in real life

The risk isn't just getting a technical rule wrong. The bigger problem is mismatch.

A snowbird can end up with a policy built for one state and one style of use, while the RV is being used another way in Florida. That mismatch can show up in a claim review, in registration questions, or when a carrier asks where the vehicle is kept.

Here's where people need to slow down and think through actual use:

- Driving exposure: How often is the RV on the road in Florida?

- Residential exposure: Is the unit functioning like a temporary home at a site?

- Stored exposure: Is it left in Florida storage for extended periods?

Ask this before renewal: “If my RV is in Florida for a season, stored there, or rotated in and out during the year, does my current policy still match that use?”

Minimum compliance is not the same as proper protection

The legal threshold and the practical protection question are two different things. A policy can satisfy a minimum requirement and still leave obvious holes for a snowbird lifestyle.

That's why the residency and presence issue should trigger a policy review, not just a registration question. Once the RV spends enough time in Florida, the smart move is to look at where it's garaged, how it's used, and whether the policy treats it as a traveler, a parked seasonal unit, or something closer to a residence.

Essential Insurance Add-Ons for Every Snowbird

A lot of snowbirds buy an RV policy that looks solid on paper, then leave the rig parked in Florida for three or four months and assume the job is done. That is usually the gap. Seasonal parking creates a different set of exposures than a road trip does.

Once your RV becomes your winter address, even part time, the useful add-ons change. A parked unit can still cause an injury claim. It can still take storm damage. It can still be broken into while you are back north. Those are snowbird problems, not generic RV problems.

The add-ons that solve snowbird problems

Some endorsements matter because you are driving cross-country. Others matter because the RV sits at one site for weeks at a time. For Florida snowbirds, the second group gets missed more often.

| Endorsement | What It Covers | Why a Snowbird Needs It |

|---|---|---|

| Vacation liability | Liability tied to the RV while parked and used at a campsite | Helps if a guest trips at your site or your setup causes property damage |

| Personal effects coverage | Belongings kept inside the RV | Helps cover clothing, electronics, cookware, tools, and other items that stay in the rig for the season |

| Storage-oriented protection | Risks while the RV is parked, such as storm, fire, theft, or vandalism | Matters when the RV spends long stretches sitting in Florida, occupied or not |

| Emergency expense coverage | Temporary living costs after a covered loss makes the RV unusable | Helps if a fire, wind loss, or other covered claim interrupts your winter stay |

| Roadside assistance or towing | Specialized help for breakdowns and towing needs | Standard auto roadside plans often fall short for larger RVs and trailers |

The add-on snowbirds skip too often

Long-term parking coverage gets overlooked all the time.

Clients often assume the risk drops once the keys are off the ignition. Driving exposure drops. Premises exposure, weather exposure, and unattended-unit exposure can stay high, especially in Florida. If your awning comes loose and damages a neighbor's unit, or someone slips near your hookup area, that claim does not care that the RV was parked.

Storage and property questions also get messy fast. If you leave furniture, clothing, tablets, golf gear, and kitchen equipment in the coach all season, do not assume another policy fills every gap. The rules can get especially murky after a storm, which is why it helps to review how hurricane damage is treated under renters insurance and then compare that with your RV property limits and exclusions.

Match the endorsement to the way you actually use the RV

The right setup depends less on the phrase "full coverage" and more on what the RV is doing most of the year.

If you move every week, roadside assistance, collision, and higher on-road liability limits deserve attention first. If you stay in one park for the season, vacation liability, personal effects, and protection during long parked periods usually matter more. If you leave the RV in Florida after you head north, ask a direct question: what coverage remains in force while the unit is stored, unattended, or visited only occasionally?

That last point matters more than people expect. Some policies handle seasonal occupancy well but get narrower during storage periods, especially if the carrier views the unit as laid up rather than in active use.

A good snowbird policy should answer two questions clearly: what is covered while the RV is being driven, and what is covered while it is parked in Florida for weeks or months.

Where policy comparisons help

Carrier language varies a lot on seasonal use, storage, personal property, and parked liability. One company may package those protections together. Another may make you add them one by one. An independent agency can compare those differences across carriers and help you avoid paying for road-use extras while missing the coverage that matters once the RV becomes your winter base.

Budgeting for Your Policy How Much Will It Cost?

Most snowbirds want a number first and an explanation second. That's fair. Price matters. But with RV insurance, cost only makes sense once you line it up with how the rig is used.

Recent Florida RV insurance guidance reports average annual premiums of about $1,386.04 for motorhomes and about $841.16 for travel trailers. The same guidance lists broader ranges of $1,000 to $5,000+ annually for Class A motorhomes and $500 to $1,000 for towed trailers with extra coverage in Florida, according to this Florida full-time RV insurance pricing overview.

Why one snowbird pays more than another

Those numbers can vary a lot because insurers price the RV you own and the way you use it.

A carrier usually looks closely at:

- RV type and value: A large motorhome is priced differently than a smaller trailer.

- Usage pattern: Seasonal occupancy and fuller residential use can cost more than occasional trips.

- Coverage choices: Lower deductibles and broader endorsements raise premium.

- Storage and location details: Where the RV sits matters, especially in Florida.

- Driver and claims history: Clean records still help.

What works if you want to control cost

The cheapest premium on paper often becomes the most expensive mistake after a loss. The better approach is to trim waste, not protection.

Good ways to shop smart include:

- Raise your deductible carefully if you can handle more out-of-pocket after a claim.

- Remove endorsements you won't use, but only after confirming they're optional for your situation.

- Be precise about usage so the policy reflects seasonal living, not generic recreation.

- Ask how storage changes pricing if the RV sits for part of the year.

- Compare multiple carriers because snowbird use isn't priced the same way across the market.

Cheap RV insurance is often cheap because it assumes less use, less property inside, or less liability around the site. Those assumptions need to be checked, not guessed.

A realistic budget starts with honest answers. How many months is the RV in Florida? Is it occupied? Is it left behind? Is it carrying the things you'd normally protect in a home? Once those answers are clear, the price starts to make sense.

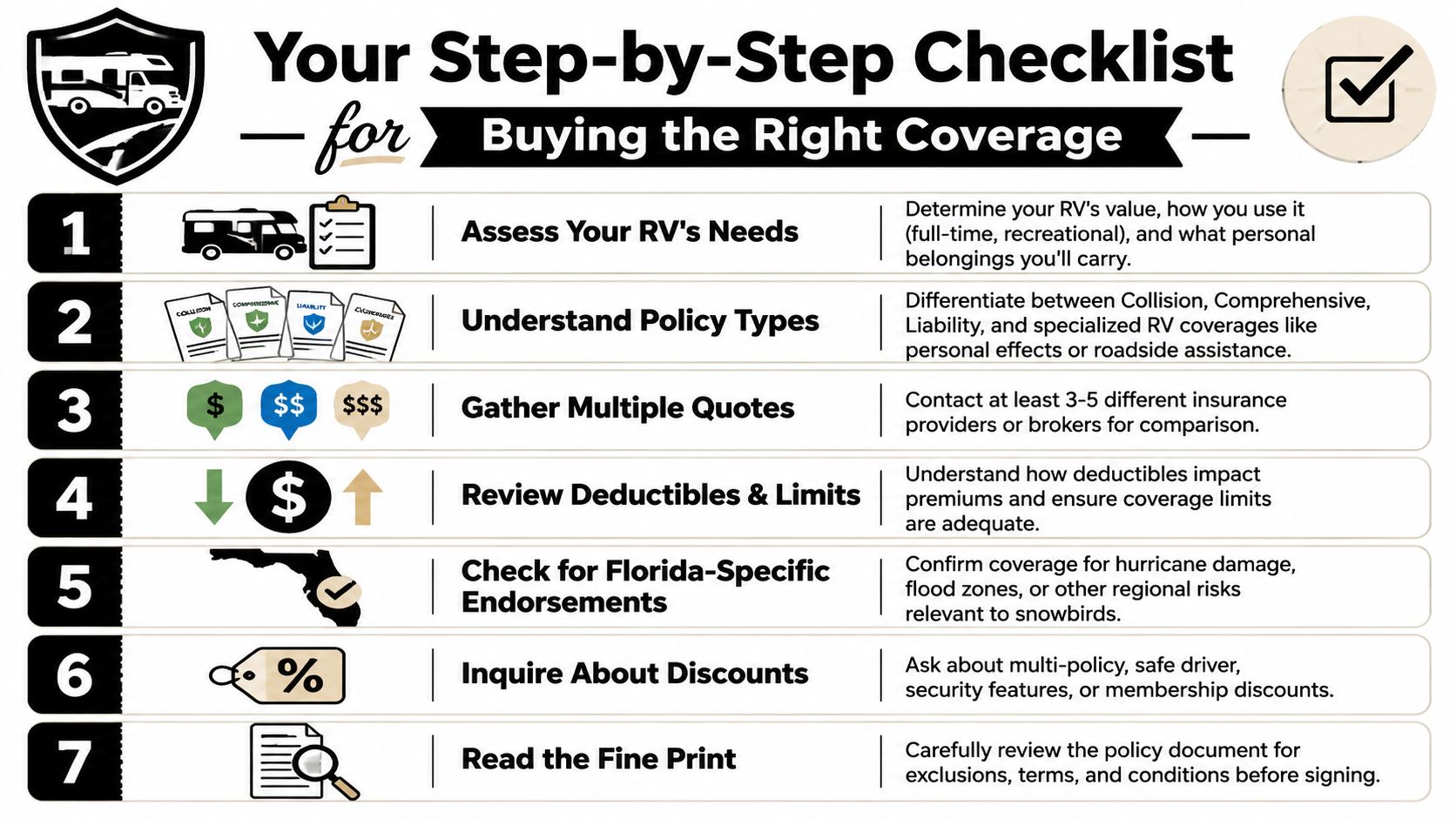

Your Step-by-Step Checklist for Buying the Right Coverage

Shopping for RV insurance gets easier when you stop thinking about it as one decision and treat it like a short sequence of smaller ones.

Start with your documents

Before you ask for quotes, gather the practical basics:

- RV details: VIN, make, model, class, and any custom equipment

- Driver information: License details and current garaging information

- Current insurance documents: Your declarations page matters more than a billing summary

- Loan information if financed: Lenders may require physical damage coverage

Then work through the questions that actually shape the policy

Use this checklist in order.

Define how the RV is used

Be specific. Seasonal travel, long-term site parking, and off-season storage are not interchangeable.List what stays inside the RV

If the unit carries valuable personal property, say so upfront.Ask about parked liability

If someone trips at your campsite, your policy should not leave you guessing.Ask how storage is handled

If the RV remains in Florida when you leave, confirm what protection stays in force.Review deductibles and limits

Don't focus only on premium. A lower price with weak limits can backfire.Compare more than one carrier

Language around seasonal use can vary more than people expect. A broad market comparison helps, and this review of RV insurance company options is a solid starting point for the kinds of differences to look for.Read the exclusions before you buy

A good quote isn't finished until you understand what it does not cover.

The questions I'd ask on every snowbird quote call

- Will this policy still fit if the RV is parked in Florida for months?

- Does the carrier treat this as seasonal use, storage use, or residential-type use?

- Are personal belongings inside the RV covered clearly?

- What happens if I leave the unit in Florida after the season ends?

That short list catches most of the mistakes before they become expensive.

FAQ Common Questions for Florida Snowbird RV Owners

Do I need a different policy if I leave my RV in Florida all summer?

Possibly, yes. This is one of the biggest gaps in ordinary RV planning. A key underserved issue for snowbirds is how coverage changes when the RV is parked in Florida for months. Major carriers now market storage-oriented protections for storm, fire, and theft while parked, which points to a real need for hybrid coverage that fits seasonal use rather than a one-size-fits-all annual package, as noted in Florida RV insurance information for long-term parked units.

If the RV sits unattended, ask specifically about broad protection while parked, any storage-related conditions, and whether campsite or premises-type liability still matters in that setup.

Does my auto policy liability cover my towed RV?

Sometimes for liability to others while towing, but that does not mean the trailer itself is protected. Snowbirds get into trouble when they hear “the tow vehicle extends coverage” and assume that applies to every kind of loss. It usually doesn't solve damage to the RV, theft, vandalism, weather loss, or property kept inside.

The safer approach is to ask two separate questions. “What liability follows the trailer while towing?” and “What policy pays if the trailer itself is damaged?”

Can I suspend parts of my coverage during the off-season to save money?

Sometimes carriers allow adjustments for periods when the RV isn't being driven, but this has to be handled carefully. Saving money by dropping the wrong protection is how people end up uncovered during storage.

The goal isn't to strip the policy down to almost nothing. The goal is to keep the parts that still matter while the RV is parked, especially in a state where weather and theft remain live risks.

If the RV is still valuable while parked, it still needs insurance designed for being parked.

What's the biggest mistake Florida snowbirds make?

They buy for the trip down and forget to buy for the months after arrival. Driving is only one chapter of the exposure. Seasonal living, long-term parking, stored belongings, and Florida-specific weather are the chapters that deserve just as much attention.

Get the Right Snowbird Policy with Select Insurance Group

The right snowbird policy usually isn't the broadest policy on the shelf. It's the one built for how your RV is used in Florida, especially if it spends long stretches parked, occupied seasonally, or stored between visits.

If you want help reviewing your current RV coverage or comparing options for a Florida snowbird setup, contact Select Insurance Group, Inc.. As an independent agency, it compares quotes from 20 to 40 carriers, offers bilingual support, and provides free, no-obligation guidance for RV owners who want coverage that matches real seasonal use.