The search for auto insurance in Orlando often begins after a frustrating moment. A renewal lands in the inbox. A move across town changes the rate more than expected. A family adds a teen driver or replaces an older car, and the quote suddenly feels disconnected from the household budget.

That reaction is normal in Orlando. This market can punish drivers who shop fast and only compare the monthly payment. The better approach is to look at price, coverage, and local risk together. A policy that looks cheap on screen can become expensive the first time you deal with a parking lot collision, storm damage, or a driver who carries too little coverage.

If you're trying to find real value in auto insurance Orlando drivers can live with, the goal isn't just a lower quote. It's a policy that fits how and where you drive, what you can afford out of pocket, and what Florida's newer insurance rules now require.

Table of Contents

- Why Your Orlando Car Insurance Is Different

- Florida's New 2026 Insurance Rules Explained

- Orlando Auto Insurance Costs and Risk Factors

- Choosing Coverage Beyond the Legal Minimum

- Smart Ways to Lower Your Orlando Insurance Bill

- Your Checklist for Comparing Orlando Car Insurance Quotes

- Why Partner with a Local Orlando Insurance Expert

Why Your Orlando Car Insurance Is Different

A lot of Orlando drivers think they're being singled out when they see a high quote. They aren't. They're being rated in a city where the driving environment is unusually complicated.

A typical day here can include stop-and-go traffic, aggressive merging, visitors who don't know the roads, sudden downpours, crowded parking lots, and long commutes that mix local traffic with resort-area congestion. Even careful drivers get pulled into that risk pool.

The local driving pattern matters

Orlando isn't just a commuter city. It's also a tourism hub. That creates a different kind of exposure than a smaller market where most drivers follow the same routine on familiar roads.

You see it in common claim situations:

- Intersection confusion: A visitor hesitates, changes lanes late, or brakes unexpectedly near an exit or attraction area.

- Parking lot damage: Tight lots at apartments, shopping centers, and entertainment venues create constant low-speed claim opportunities.

- Weather surprises: A car parked outside all day is more exposed to wind-driven rain, hail, and storm debris.

- Dense daily use: More time in traffic usually means more chances for a claim, even if you're a careful driver.

Orlando drivers often feel like they're paying for problems they didn't create. In many cases, that's partly true. Insurance pricing reflects the environment around you, not just your personal habits.

Why this changes how you should shop

In a lower-risk area, it can make sense to sort quotes by price and pick the cheapest acceptable option. In Orlando, that shortcut often leads to the wrong policy.

The question isn't only, "What's the lowest premium?" The better question is, "If I have a real claim here, what part of the loss will I have to absorb myself?"

That shift matters for renters who park outside, apartment residents dealing with theft or weather exposure, and families who can't comfortably handle a large surprise bill after an accident. When drivers start with exposure instead of just premium, they usually make better decisions on deductibles, liability limits, and whether to carry protection for their own injuries and vehicle.

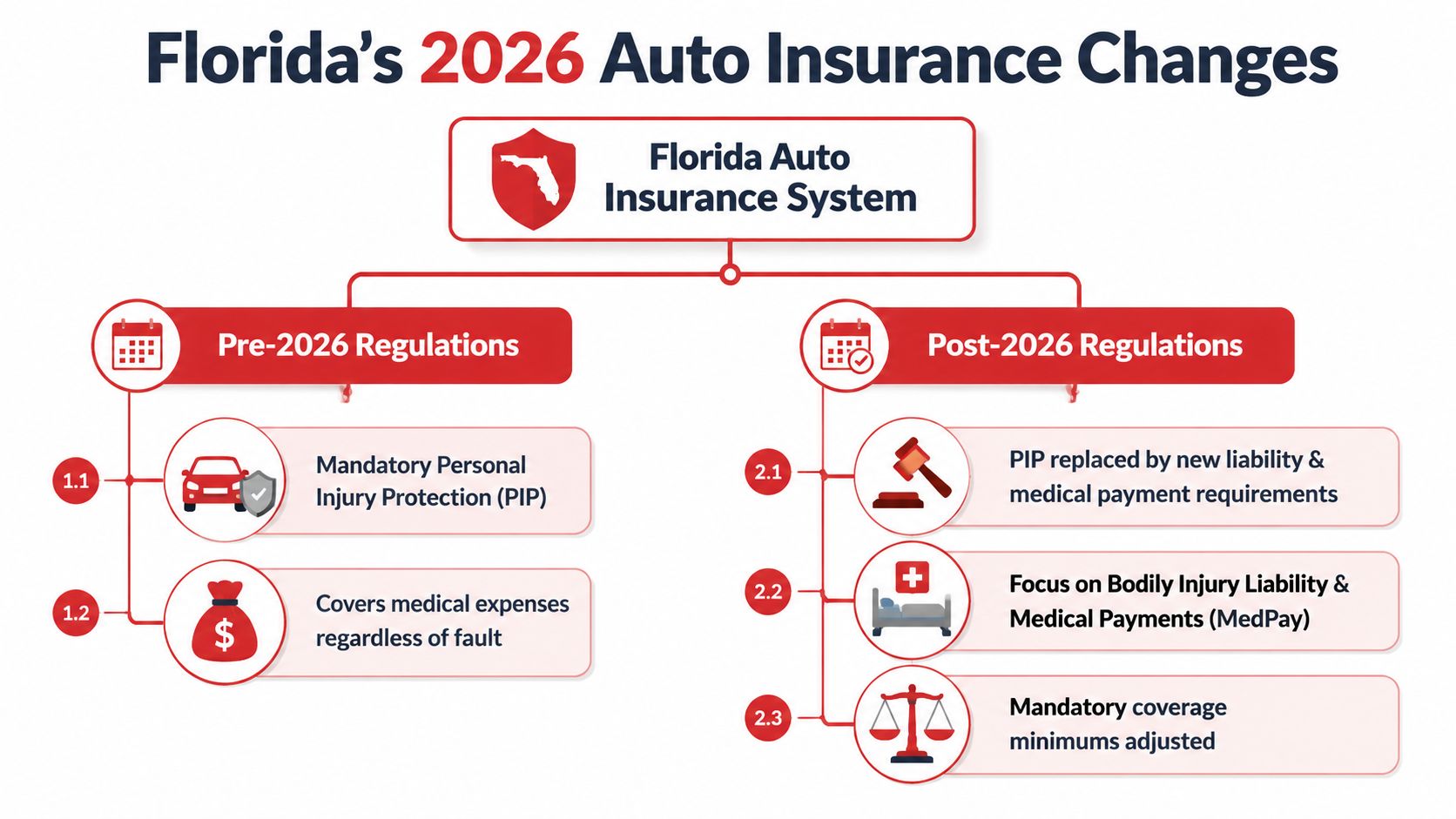

Florida's New 2026 Insurance Rules Explained

Florida drivers have had a lot of confusion around the law changes. The practical takeaway is simple. Policies issued or renewed on or after January 1, 2025 no longer require PIP. Instead, Florida requires bodily injury liability of $25,000 per person and $50,000 per accident, plus $10,000 in property damage liability, as outlined in Florida coverage guidance from ORCA Insurance.

What changed for Florida drivers

Under the old setup, many drivers focused on PIP because it was the familiar requirement. Under the newer rules, the legal foundation shifted toward liability coverage for injuries you cause to other people.

That means:

| Coverage piece | What it does |

|---|---|

| Bodily injury liability | Pays for the other person's injury-related costs if you cause a crash |

| Property damage liability | Pays for damage you cause to someone else's vehicle or property |

| No PIP requirement on new or renewed policies after the change | Removes the old mandatory first-party framework many drivers were used to |

Think of liability as a financial shield for the other driver, not a medical fund for you. If you cause the accident, liability coverage is there to pay their bills up to your policy limits. It doesn't rebuild your own car, and it doesn't automatically solve your own injury costs.

If you want a plain-language legal walkthrough of how PIP used to work and why the shift matters, expert Florida PIP advice from CAINE LAW-guide-2026) is a useful companion read.

Why the legal minimum still leaves gaps

A lot of people hear "required minimum" and assume that means "reasonable protection." Those are not the same thing.

The minimum is the floor that keeps you legal. It isn't designed around your savings, your car loan, your ability to miss work, or the cost of repairing your own vehicle after a bad day in Orlando traffic.

Here's the practical way to look at it:

- If you injure someone badly: Your bodily injury limit can run out.

- If your own car is damaged: Liability-only coverage doesn't fix it.

- If you get hurt by someone with weak coverage: Their policy may not be enough to protect you.

- If you rely on your car for work or family logistics: A thin policy can create a much larger financial problem than the premium savings were worth.

Practical rule: Buy the minimum only if you've already accepted the risk of paying more yourself after a claim.

For many drivers, the smarter move is to treat the new legal minimum as a starting point, then build around it based on the car, the neighborhood, and how much financial shock the household can absorb.

Orlando Auto Insurance Costs and Risk Factors

A driver on I-4 gets clipped during a stop-and-go backup, then learns the repair bill is higher than expected and the rental clock is already running. That is the Orlando insurance problem in one scene. Rates here are not just about finding the lowest quote. They reflect how often claims happen, how expensive they are to settle, and whether a policy gives you enough protection when a routine commute turns costly.

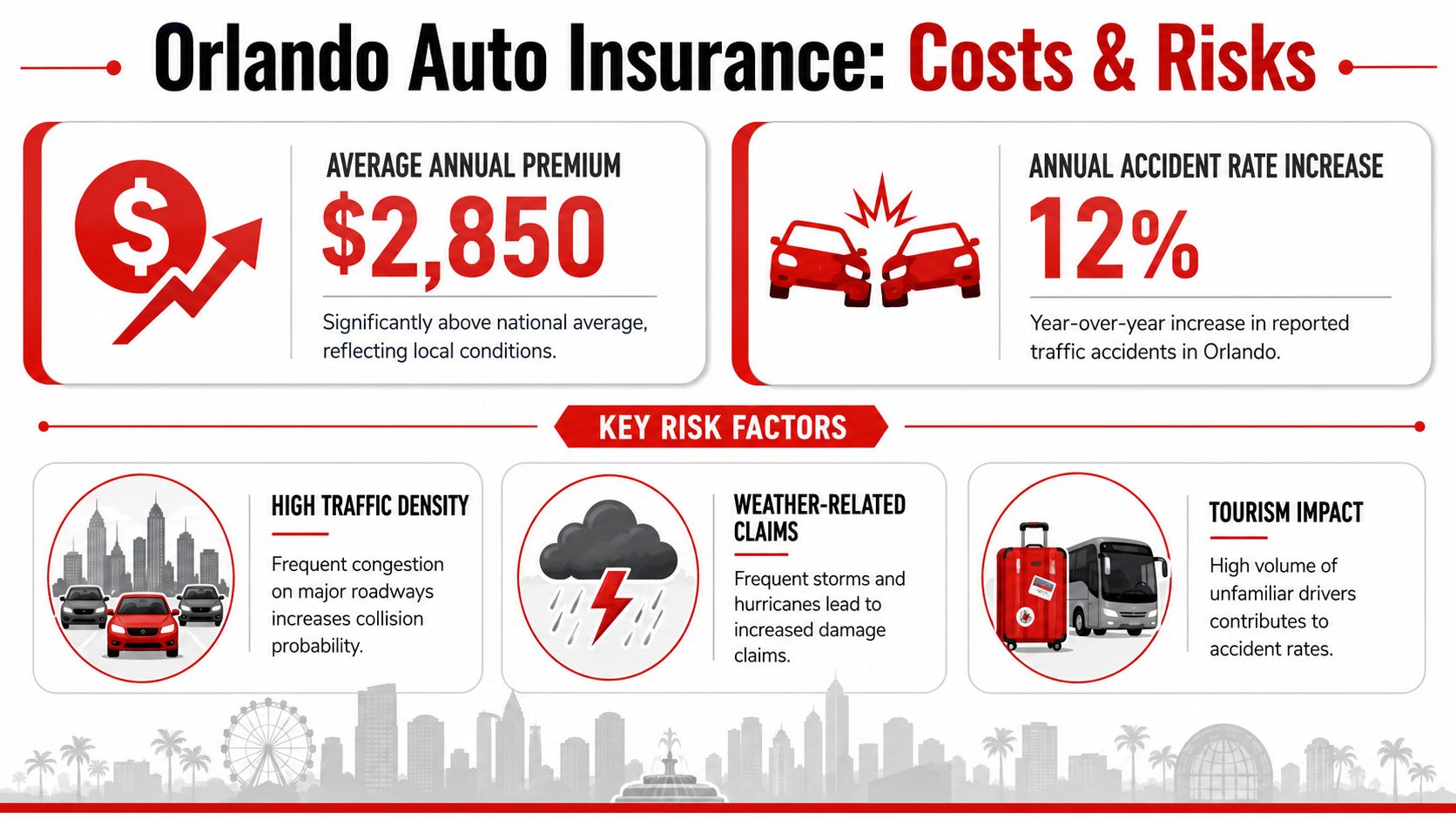

What Orlando drivers are paying

Orlando drivers usually pay more than many households expect, and the actual spread shows up from one carrier to the next. That is why quote shopping matters, but price alone is a poor filter. Two policies can look similar on the front page and leave you with very different out-of-pocket costs after a crash, weather loss, or tourist-area fender bender.

For a local benchmark before you compare options, this Orlando average car insurance cost guide gives useful context.

The more practical question is value. A lower premium can make sense if the deductibles fit your emergency fund and the liability limits match your financial exposure. It becomes a bad deal if the policy saves a little each month but shifts a large repair bill, injury claim, or rental expense back onto you.

For a broader consumer explanation of why quotes can vary so much, the BDISchool guide to insurance savings is a helpful reference.

Why Orlando gets priced higher

Carriers price Orlando based on claim frequency and claim severity. Both are a factor here.

Several local conditions push those numbers up:

- Heavy commuter traffic: Packed roads raise the odds of rear-end crashes, lane-change claims, and low-speed collisions that still produce expensive repairs.

- Tourism-related driving patterns: Visitors miss exits, stop suddenly, drift across lanes, and slow down in unfamiliar areas.

- Storm risk: Hail, wind, flooding, falling branches, and flying debris can damage parked vehicles with no warning.

- Repair costs: Newer cars cost more to fix because sensors, cameras, calibration, and parts pricing have changed the math on even moderate damage.

- Injury exposure: A multi-car crash on a busy corridor can create medical bills and liability claims that climb fast.

The Insurance Information Institute reports that average claim costs remain significant across the major coverage types, including property damage liability, bodily injury liability, collision, and other-than-collision losses, according to Insurance Information Institute auto insurance facts.

That matters more in Orlando than many drivers realize. A cheap policy may look fine until it meets local traffic, local weather, and local repair invoices.

The 2025 law changes also make this value question more important. As minimum requirements shift, some drivers will focus on staying legal at the lowest price possible. I would be careful with that approach. In this market, the better move is usually to balance premium, deductible, and liability limits so the policy still works when the claim is larger than you hoped.

Choosing Coverage Beyond the Legal Minimum

A lot of Orlando drivers learn this lesson in a parking lot, not at the kitchen table. A summer storm rolls through, a branch lands on the hood, or someone backs into the car at an apartment complex and leaves. The policy is legal, the premium was cheap, and then the out-of-pocket bill shows up.

That is why coverage selection should start with one question. If your car is damaged or you are hurt, how much of that cost can you absorb without wrecking your monthly budget?

What collision and other-than-collision coverage do

These coverages protect your own vehicle, but they pay for different problems.

Collision pays when your car is damaged in a crash. In Orlando, that can mean a low-speed hit in a crowded garage, a rear-end accident on a tourist-heavy corridor, or a bad lane change during rush hour.

Other-than-collision coverage applies to damage that happens outside a crash. That includes storm damage, falling branches, theft-related loss, vandalism, fire, and some animal strikes. For local drivers, this matters because weather and parking lot exposure create claims that have nothing to do with fault.

A simple way to separate them:

- Collision: Your vehicle is damaged in an impact with another car, object, or structure.

- Other-than-collision: The loss comes from weather, theft, debris, vandalism, or another non-crash event.

- Liability: You pay for damage or injuries you cause to other people.

If you want to review the state baseline before choosing optional protection, this Florida minimum auto insurance guide lays out the required coverage clearly.

Why uninsured motorist coverage deserves serious attention

In my experience, this is one of the most underbought parts of an Orlando auto policy.

Florida drivers often focus on staying legal first. I understand that. Premium matters. But legal minimums and real-world protection are not the same thing, especially after the recent rule changes. A serious injury claim can outgrow a minimum-limit policy fast, and Orlando traffic increases the odds of dealing with a driver who does not have enough coverage to make you whole.

Uninsured and underinsured motorist coverage can help with your injuries and related losses when the at-fault driver cannot. That matters more if any of these apply:

- Your emergency savings are limited

- You commute through heavy traffic most days

- You regularly drive with children or family members

- Missing work after a crash would strain your finances

The goal is not to load up every option and drive the premium through the roof. The goal is value. In Orlando, that usually means choosing limits and deductibles that protect your income, your vehicle, and your savings from the kinds of losses local drivers face most often.

Smart Ways to Lower Your Orlando Insurance Bill

A driver picks the lowest quote, saves a little each month, then finds out after a summer hail claim or an I-4 crash that the policy was cheap because it left out protection they needed. I see that mistake often in Orlando.

The better approach is to lower cost while keeping the parts of the policy that protect your savings, your car, and your income. That matters more here because local drivers deal with congested roads, storm exposure, rental-heavy neighborhoods, and a lot of out-of-town traffic. With Florida's newer insurance rules changing how many households think about coverage, value matters more than bare-minimum price.

Savings that help

Start with changes that improve the policy structure.

- Shop quotes using the same coverage setup: If one quote has lower liability limits or a much higher deductible, it is not a true apples-to-apples comparison. Match the structure first, then compare price.

- Ask for a full discount review: Good discounts are often available for bundling, safe driving habits, vehicle safety features, paid-in-full billing, good students, and multi-car households. Do not assume every discount was applied automatically.

- Raise deductibles only to a level you can comfortably afford: A higher deductible can reduce premium, but it only works if you could handle that out-of-pocket cost without putting repairs on a credit card.

- Fit physical damage coverage to the car's value: A newer financed vehicle usually needs stronger protection. An older paid-off car may justify a different setup, especially if a claim payout would be limited by the car's market value.

- Review mileage and vehicle use: A policy built for a long commuter should not stay the same if the car is now driven less, used mainly around town, or no longer used for work-related trips.

One of the biggest pricing mistakes I see is cutting coverage first instead of fixing inefficiencies first. Many Orlando households can save money by correcting mileage, removing unused add-ons, adjusting deductibles carefully, or reviewing discounts before they touch liability or uninsured motorist limits.

Cuts that often backfire

Cheap insurance gets expensive fast after the wrong claim.

A few common examples:

- Dropping coverage for non-collision losses on a car parked outside: In Orlando, weather, falling debris, theft, and vandalism are real risks.

- Choosing the highest deductible only to shrink the monthly bill: If the deductible would delay repairs or force you to borrow money, the premium savings are not worth much.

- Keeping only minimum liability because it satisfies the law: A legal policy can still leave a serious gap after a major accident.

- Skipping uninsured or underinsured motorist coverage to save premium: That can hurt when the other driver does not have enough insurance to cover your injuries and lost income.

The goal is not to buy the most coverage. The goal is to buy the right coverage at a price your household can carry. In Orlando, the best value usually comes from careful quote comparisons, smart deductible choices, and keeping protection against the losses that create the biggest financial strain.

Your Checklist for Comparing Orlando Car Insurance Quotes

A lot of bad insurance decisions happen because people compare quotes that aren't equivalent. One quote includes broader protection. Another uses a much higher deductible. A third leaves out something important and looks cheaper because of it.

Use a simple checklist and the process gets easier.

Before you request quotes

Get your information together first so each quote starts from the same facts.

- Gather your driver and vehicle details. Have license information, VIN, garaging address, and current insurance details ready.

- Know how the car is used. Daily commuting, business-related use, household drivers, and annual mileage all affect quoting.

- Decide your target coverage before shopping. Pick your liability limits, deductible comfort zone, and whether you want collision, coverage for non-collision events, and uninsured motorist protection.

How to compare them correctly

Once the quotes come in, compare them line by line.

- Check liability limits: Make sure each quote is built on the same bodily injury and property damage structure.

- Match deductibles: A lower premium with a much higher deductible is not an apples-to-apples comparison.

- Look for omitted coverage: Some quotes look attractive because they do not include physical damage or uninsured motorist options.

- Review payment terms: Monthly price matters, but so does the total cost of the policy term.

- Ask about discounts and claim process: Service after a claim matters just as much as the quote itself.

A short comparison table can help:

| Quote item | What to verify |

|---|---|

| Coverage limits | Same liability structure across all quotes |

| Deductibles | Same out-of-pocket level for each policy |

| Vehicle protections | Collision and comprehensive included or excluded the same way |

| Injury protection for you | UM/UIM included if that's part of your plan |

| Total cost | Compare full-term cost, not just the monthly number |

Bring every quote back to one question. If I file a claim, what exactly will this policy pay, and what will I owe myself?

That question keeps you from buying a low price that hides a high risk.

Why Partner with a Local Orlando Insurance Expert

Orlando drivers aren't dealing with a simple insurance market. The rules changed. Local pricing runs high. Weather matters. Traffic patterns matter. Small coverage decisions can have large consequences after a claim.

That's where local guidance earns its keep.

Where local guidance makes a difference

A local independent agent can catch problems that online quote forms often miss. That includes mismatched deductibles, weak liability limits, missing uninsured motorist options, and coverage choices that don't fit where the vehicle is parked or how it's used.

This matters even more in a changing market. Mesa Insurance Group reports that recent Florida reforms have helped drive premium declines, including insurer rate reductions of up to 11.5%, and notes an average premium decrease of 6.5% in its discussion of Orlando auto insurance. It also points to a broader post-reform downward shift in rates, which makes review shopping worth doing now, based on Mesa's Orlando auto insurance overview.

Select Insurance Group, Inc. is one local option for drivers who want help comparing coverage across multiple carriers rather than relying on a single quote. The agency states that it compares 20 to 40 carriers, has over 30 years of experience, and offers bilingual service for Florida customers.

If you want a broader look at how local agencies fit into the Orlando market, this guide to insurance agencies in Orlando gives additional context.

What to do next

If you're shopping for auto insurance Orlando coverage right now, don't stop at the first low number. Build your quote list carefully. Match the coverage. Review the deductibles. Think through your real out-of-pocket risk.

Then talk through the weak spots before you bind the policy.

That extra step usually costs nothing, and it can prevent the most common mistake Orlando drivers make. Buying a policy that was affordable on quote day, but inadequate on claim day.

If you want help reviewing coverage, comparing quotes, or finding a policy that balances cost with real protection, contact Select Insurance Group, Inc. for a free, no-obligation quote.