If Tampa insurance quotes feel expensive, that's because they are. In 2026, the average six-month car insurance policy in Tampa is $1,827, or about $304 per month, which is 34% higher than the Florida average and 107% higher than the national average, according to The Zebra's Tampa auto insurance data.

That number changes how you should shop. In a market like Tampa, small mistakes in the quoting process, weak coverage choices, and slow comparison shopping can cost you real money. The good news is that the city average is not the price every driver or homeowner has to accept.

The practical way to shop Tampa insurance quotes is local, organized, and fast. If you want a side-by-side comparison built for this market, a local agency that works across multiple carriers can save time and help you avoid the usual quoting traps. That's the role of a Tampa independent insurance agency that understands how Tampa pricing behaves across auto, home, renters, and business policies.

Table of Contents

- Why Getting Tampa Insurance Quotes Requires a Local Strategy

- Prepare Your Information for Accurate Quotes

- Understanding Your Tampa Insurance Options

- How to Get Instant Quotes from Multiple Carriers

- Pro Tips for Lowering Your Tampa Insurance Costs

- Making Your Final Choice with Confidence

Why Getting Tampa Insurance Quotes Requires a Local Strategy

Tampa isn't a market where generic insurance advice works well. Local drivers deal with heavy traffic, theft exposure, weather risk, and claim patterns that make rates more volatile than what people expect when they move here. Homeowners deal with a different version of the same problem. A quote that looks reasonable in another part of the Southeast can land much higher in Tampa once the property details, ZIP code, and coverage structure are entered correctly.

That's why Tampa insurance quotes need local context. A basic online quote form may give you a starting point, but it usually won't explain why one ZIP code prices differently than another, why a carrier likes one home's construction details but not another, or why two policies with similar premiums can have very different deductibles and exclusions.

Practical rule: In Tampa, don't shop by price alone. Shop by price, coverage structure, and whether the quote can actually be bound without surprises.

Local strategy also matters because insurance here isn't one product. It's a set of decisions. A driver may need auto coverage with better protection against uninsured motorists. A homeowner may need to sort out wind exposure, deductibles, and whether flood coverage belongs in the plan. A small business owner may need to combine property, liability, and vehicle coverage in a way that doesn't leave gaps.

The people who usually get better results do three things well:

- They compare broadly. One carrier may price a clean driving record very well, while another may be stronger for bundled home and auto.

- They give clean information upfront. Accurate data avoids re-quotes, underwriting issues, and last-minute premium jumps.

- They work with someone who can translate the details. Coverage forms aren't identical, even when the monthly payment looks close.

That local approach is what keeps this process from turning into a stack of confusing quotes that all look cheap until you read the fine print.

Prepare Your Information for Accurate Quotes

The fastest way to get bad Tampa insurance quotes is to start with incomplete information. The second-fastest way is to rush through the details and assume the carrier will fix it later. That usually creates delays, revised premiums, or a quote that can't be bound as written.

Before you shop, organize your documents. You don't need a perfect file cabinet. You do need the right details in front of you.

What to gather before you start

For most personal and business quotes, this is the working checklist I'd use.

- For auto insurance: Have the VIN for each vehicle, the driver's license information for every driver in the household, and the details of any recent accidents, tickets, or violations.

- For home insurance: Gather the full property address, year of construction, prior claims information, and details about protective devices like alarms or monitored security systems.

- For commercial insurance: Keep your legal business name, FEIN, business address, vehicle list if applicable, payroll or staffing details when needed, and a clear description of what the business does.

If you're replacing an existing policy, have your current declarations page ready. That makes it much easier to compare liability limits, deductibles, and optional endorsements side by side instead of guessing.

A simple prep routine saves time:

- Pull your current policy documents first. They show what you have now.

- Confirm names and addresses carefully. Incorrect names and addresses frequently lead to avoidable errors.

- List all household drivers and vehicles. Leaving someone off creates problems later.

- Note recent losses accurately. Underwriting will review them.

Why quote accuracy matters

One of the worst habits in insurance shopping is trying to “test” a lower price with altered information. AM Best describes quote manipulation as a damaging practice where consumers or agents mismatch data such as ZIP codes to chase lower rates, and notes that it occurs in about 9% of agent-driven channels compared with 2% in direct channels, according to AM Best's quoting analysis.

That matters because a quote is only useful if it survives underwriting. If the address, garaging location, driver history, or household makeup changes after review, the premium can change too. In some cases, the policy may not be issued as quoted.

Clean data at the start beats a cheap-looking quote that falls apart when the carrier verifies the file.

Accuracy also protects you from a more expensive mistake. If you buy coverage based on incomplete information, then discover the policy doesn't match the actual risk, fixing it later can be messy. It's better to spend a few extra minutes upfront than to redo the entire process after an underwriter kicks it back.

Understanding Your Tampa Insurance Options

A Tampa quote is only useful if you know what is being priced. I see shoppers focus on the monthly number first, then find out later that two policies with similar prices cover very different risks.

That matters more in Tampa than in a lot of other markets. Local rates are already high, storm exposure affects property coverage, and even small differences in deductibles, exclusions, and driver history can change what you pay. An independent agency holds an advantage. Running the same risk through 40 plus carriers often reveals price gaps that a single-company quote never shows.

Auto coverage in a high-cost city

Auto insurance is where many Tampa drivers leave money on the table. One quote might look cheap because it strips physical damage coverage, raises deductibles beyond what you could comfortably pay after a crash, or leaves out add-ons you need.

A better way to compare auto quotes is to line up the parts that drive the result:

- Liability limits. Florida minimum limits keep the price down, but they do not go far after a serious accident.

- Collision and other-than-collision coverage. These protect your vehicle, but the value depends on the car's age, loan status, and replacement cost.

- Deductibles. Higher deductibles lower the premium. They also mean more out of pocket right after a loss.

- Uninsured or underinsured motorist coverage. This deserves attention in Florida because too many drivers carry little coverage or none at all.

- Roadside, rental, and custom equipment add-ons. These are small line items, but they can make two “full coverage” quotes very different.

For drivers trying to lower costs without gutting protection, this guide to cheap car insurance options in Florida helps explain which changes usually save money and which ones create problems later.

Young drivers need extra care here. Vehicle choice, mileage, grades, training, and household setup all affect the premium. Families comparing first policies should review this primer on car insurance for new drivers.

Home, renters, and flood coverage in Tampa

Home insurance in Tampa has its own pressure points. Roof age, wind mitigation features, prior claims, distance from the coast, and the home's rebuild characteristics all matter. Two houses on the same street can price very differently if one has an older roof or weaker opening protection.

The cheapest home quote is often not the best value. Check these items closely:

- Hurricane deductible. This is separate from the standard deductible on many Florida policies.

- Dwelling coverage. It should match rebuild cost, not market value or mortgage balance.

- Water exclusions and limitations. Many owners assume “water damage” is one category. It is not.

- Ordinance or law coverage. Older homes may need this if repairs trigger code upgrades.

- Personal property and loss of use. These become real issues after a major storm claim.

Renters usually have a simpler application, but the same mistake shows up all the time. Tenants assume the landlord's policy covers their furniture, clothes, electronics, and liability. It does not.

Flood coverage also needs a separate answer. In Tampa, never assume a homeowners policy includes flood just because the property is not right on the water. Ask whether flood is excluded, available separately, or already included through a different policy form.

A strong Tampa property quote makes the deductibles, exclusions, and separate flood question clear before you buy.

Commercial insurance for local businesses

Business owners often shop for the certificate first and the actual coverage second. That can backfire fast after a claim. A contractor in Brandon, a restaurant in South Tampa, and a delivery operation near the airport do not have the same exposure, even if they all ask for “basic business insurance.”

Start with what the business does every day, where it operates, who drives, what property moves, and whether employees work in the field or at a fixed location.

| Coverage Type | What It Protects |

|---|---|

| General liability | Third-party bodily injury, property damage, and common liability claims |

| Commercial property | Buildings, equipment, inventory, and physical business assets |

| Workers' compensation | Employee job-related injuries and related obligations |

| Commercial auto | Business-owned vehicles and liability arising from their use |

| Inland marine | Tools, equipment, and property that moves between jobs or locations |

Accuracy matters here too. If the application describes the business too broadly or leaves out part of the work, the quote can come back wrong, or worse, the policy can create claim problems later. The goal is not just to get a certificate. The goal is to make sure the policy matches the work the business performs.

How to Get Instant Quotes from Multiple Carriers

The old way to shop insurance is still common. Call one company, answer the same questions again, wait for an email, repeat the process, then try to compare different quote formats that don't line up cleanly. That approach burns time and usually creates confusion.

The better approach is to gather your information once and run it across multiple carriers through one quoting process.

The slow way versus the efficient way

Speed matters more than many shoppers realize. Industry data shows that 78% of customers bind with the first carrier that reaches them effectively, and that agencies need a speed to lead of under five minutes to avoid heavy abandonment, according to Drips' insurance quote conversion analysis.

That doesn't mean you should buy the first quote that hits your inbox. It means the process works better when someone responds quickly, confirms the details, and gets accurate options in front of you before the shopping momentum dies.

The slow method fails for a few reasons:

- You repeat yourself constantly. Every form asks for the same information.

- Quotes come back uneven. One includes stronger liability limits, another strips coverage to look cheaper.

- Follow-up is inconsistent. By the time someone circles back, you've already moved on.

A multi-carrier quoting setup fixes that by centralizing the intake, speeding up turnaround, and making comparison easier. One option available in this market is cheap car insurance in Florida through Select Insurance Group, where drivers can compare multiple carrier options through one agency process.

What a faster quote process should look like

A good quote workflow feels organized, not frantic. You provide complete information once. The agent or quoting team confirms the details that commonly create rating errors. Then you review a short list of viable options instead of a pile of random prices.

What works in practice:

- Immediate confirmation: You should know the quote request was received and what happens next.

- Coverage review: Someone should explain whether the options are comparable.

- Fast correction of errors: If a VIN, address, or driver detail is off, it should be fixed before the quote is presented as final.

What doesn't work is chasing “instant” numbers that were built on partial information. Fast is useful only when it's also accurate.

Pro Tips for Lowering Your Tampa Insurance Costs

Lowering insurance costs in Tampa usually comes down to cleaner underwriting, smarter policy design, and better shopping discipline. The focus is often only on premium. The stronger move is to reduce premium without creating a gap you'll regret later.

Smart ways to lower premium without stripping coverage

Start with the levers that move price.

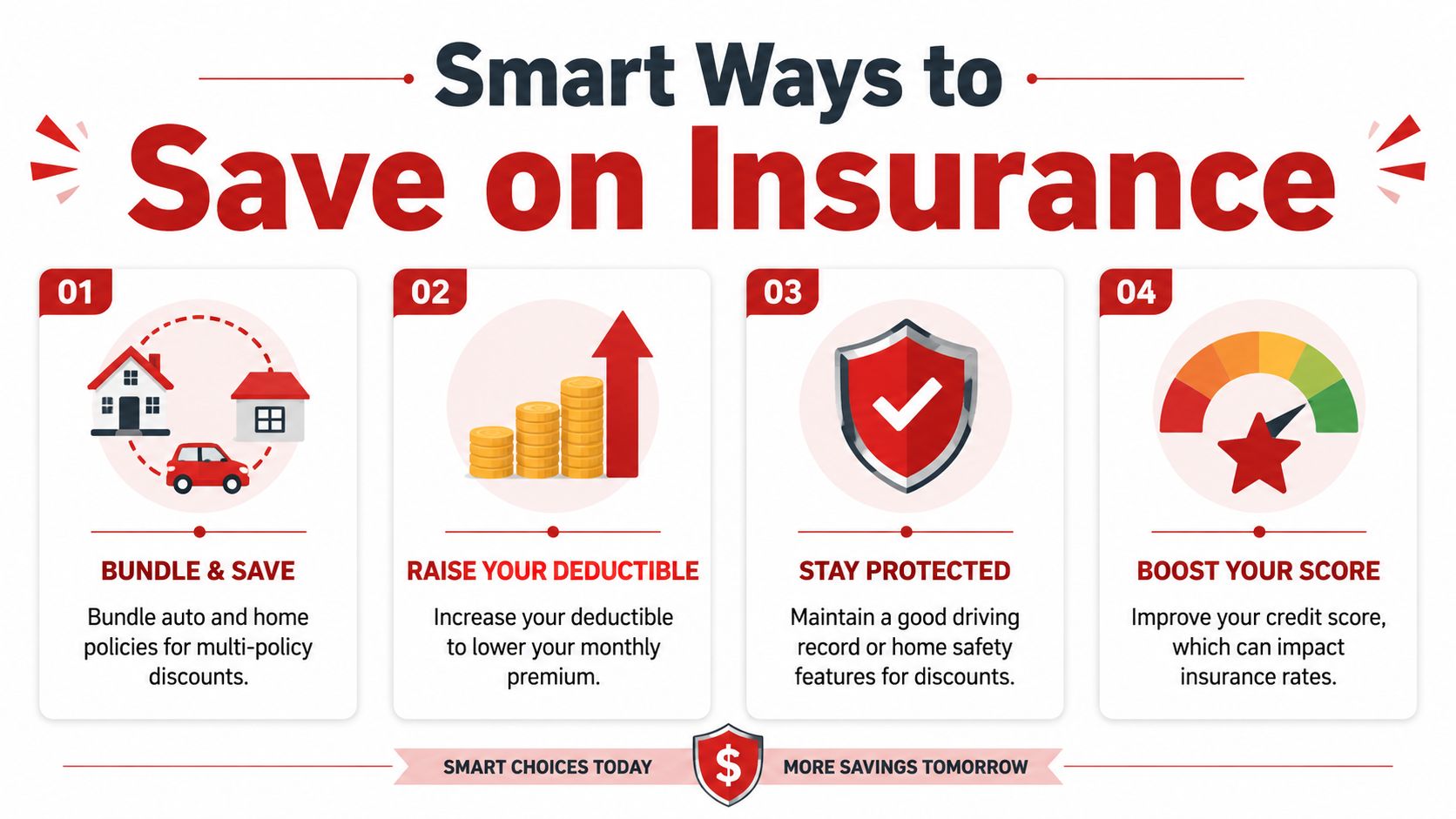

- Bundle where it makes sense. Combining auto and home or renters coverage can simplify billing and may open up multi-policy discounts.

- Adjust deductibles carefully. A higher deductible often lowers premium, but make sure the out-of-pocket amount is realistic for your household.

- Ask about protective features. Home alarms, monitored systems, and vehicle safety features can matter.

- Review the policy every renewal. A policy that was competitive last year may not be the strongest fit now.

Credit-related questions come up often, especially in Florida. The practical takeaway for shoppers is simple. Ask how your quote is being evaluated, ask what information affects the rate, and don't guess. If your profile has improved, make sure the quote reflects current information.

Tampa-specific choices that protect your budget

A local issue many drivers overlook is uninsured motorist exposure. Emerging 2025 to 2026 trends show an 18% spike in Tampa claims from uninsured drivers due to post-pandemic policy lapses, according to Policygenius' Tampa insurance discussion.

That matters for cost in two ways. First, it adds pressure to the market overall. Second, it makes the right coverage selection more important for your own protection. Cutting uninsured motorist coverage to save a few dollars can backfire badly if the other driver can't pay.

A practical Tampa checklist:

- For drivers: Ask whether uninsured or underinsured motorist protection fits your situation.

- For homeowners: Review wind-related deductibles and ask whether every major weather exposure has been addressed.

- For renters: Don't skip liability coverage just because you don't own the building.

- For everyone: Shop again when life changes. New car, new address, paid-off loan, teen driver, home update, and business growth all justify a fresh review.

For a local breakdown of budget-minded approaches, this guide on finding budget-friendly insurance in Tampa is a useful starting point.

Saving money on insurance isn't about buying less policy. It's about removing waste, correcting mismatches, and keeping the protection that would hurt most to replace out of pocket.

Making Your Final Choice with Confidence

Once the quotes are in front of you, the job changes. You're no longer shopping for a number. You're choosing which policy you'd trust on a bad day.

How to read the final quotes correctly

For homeowners, the cheapest quote can quickly become problematic. In Tampa, the average annual homeowners insurance cost is $2,602 for a $300,000 dwelling policy, which is 29% higher than the national average, and some lower-priced providers can come in far below the city average, according to Insurify's Tampa homeowners insurance data.

That should push you to compare details, not just totals. When you review final quotes, check:

- Coverage limits: Are the liability and property amounts enough?

- Deductibles: Can you comfortably absorb them after a loss?

- Exclusions and endorsements: What is not covered, and what has been added back in?

- Service fit: If there's a claim, will the communication process work for you and your family?

What to decide before you bind

The right quote is usually the one that balances affordability with clarity. You should know what you're buying, why it costs what it costs, and what trade-offs you accepted. If anything still feels vague, stop and ask before binding.

For many Tampa households and business owners, having a bilingual agent involved helps remove the last layer of confusion. That's especially useful when multiple policies are being compared and the language in the forms starts to blur together.

A good final decision should feel simple. The policy fits the risk. The deductible is manageable. The premium is acceptable. And the quote reflects your real information, not a rushed estimate.

If you want a free, no-obligation comparison for auto, home, renters, or business coverage, contact Select Insurance Group, Inc. by phone, text, or online form. A quick review of your current policy and basic details can help you compare multiple carrier options without doing the same quote process over and over.