You're probably in one of three spots right now. Your renewal just jumped, you're shopping for a better rate, or you've realized your current policy might only be “legal” on paper and not nearly enough if a serious wreck happens.

That last problem is the one that catches Georgia drivers off guard. A lot of people buy the cheapest policy that satisfies the state, then assume they're covered. In an at-fault state, that can turn into a very expensive misunderstanding. If you cause a crash, the bills don't stop at the minimum limits just because your policy does.

Georgia auto insurance isn't hard to understand once someone cuts out the jargon. The primary job is balancing three things at once: staying legal, protecting your own finances, and not overpaying for coverage that doesn't fit your car, household, or driving habits.

Table of Contents

- Your Guide to Navigating Georgia's Insurance Market

- Georgia's Legal Auto Insurance Requirements

- Decoding Your Georgia Auto Insurance Rate

- Beyond the Minimum Building a Financially Secure Policy

- Proven Strategies to Lower Your Georgia Insurance Premiums

- Navigating Special Insurance Situations in Georgia

- How to Buy Your Georgia Auto Insurance with Confidence

Your Guide to Navigating Georgia's Insurance Market

Georgia is a big insurance state, and that matters to drivers. As of 2024, Georgia ranked 5th nationally in automobile premium volume, with insurers collecting over $17.5 billion in premiums, and the state's premium volume increased by more than 100% over 10 years according to the Georgia market trends report from the NAIC.

That tells you two things right away. First, there are a lot of policies being written in this state. Second, carriers are competing hard for Georgia business, which means pricing can vary more than most drivers expect.

Why shopping feels harder than it should

It's not that the rules are impossible. The challenge lies in how every quote looks a little different, every company packages coverage differently, and the cheapest offer often strips out protection you'd want after a real accident.

A Georgia driver usually has to sort through questions like these:

- How much liability is enough: State minimums keep you legal, but they may not protect your savings.

- Should you carry full coverage: That depends on your vehicle, loan status, and how much repair risk you can absorb yourself.

- Why does one quote come in much higher: Sometimes it's your ZIP code, driving history, vehicle type, or deductible choice. Sometimes the policy covers more.

Practical rule: Don't compare prices until you've confirmed the coverage lines up. A lower premium on a thinner policy isn't a bargain.

What works in a competitive market

The best approach is simple. Decide what financial risk you can't afford to carry on your own, then build coverage around that.

That usually means starting with legal compliance, then checking the bigger gaps. Liability limits. Protection from uninsured or underinsured drivers. Coverage for your own car. Medical-related protection. Deductibles you could pay without stress.

Georgia gives drivers plenty of options. That's good news, but only if you read past the monthly price.

Georgia's Legal Auto Insurance Requirements

A driver in Georgia can carry the legal minimum, cause one serious crash, and still owe far more than the policy pays. That is the gap drivers need to understand first.

Georgia requires liability insurance before you drive on public roads. The state minimum is 25/50/25, which means $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage per accident. If you want a plain-language breakdown of those limits and the policy options built around them, review this guide to Georgia auto insurance requirements and coverage choices.

Those numbers only pay for injuries or property damage you cause to other people. They do not pay to repair your car. They also do not guarantee enough protection if medical bills, lost wages, or vehicle values run past those limits.

What 25 50 25 means in plain English

Here is how Georgia's required liability coverage works.

| Coverage type | What it applies to | Georgia minimum |

|---|---|---|

| Bodily injury liability per person | One injured person in an accident you caused | $25,000 |

| Bodily injury liability per accident | All injured people combined in an accident you caused | $50,000 |

| Property damage liability per accident | Damage to someone else's car or other property | $25,000 |

A quick example shows why the minimum can fall short. If you hit a newer SUV and send two people to the hospital, the property damage portion can run out fast, and the bodily injury cap applies to the total claim, not each bill that comes in afterward. In an at-fault state like Georgia, the driver who caused the crash is financially responsible for the damage.

Driving uninsured can trigger penalties fast

Georgia also takes uninsured driving seriously. State enforcement can include fines, suspension of your registration or license, and in some cases criminal penalties, as outlined by the Georgia Department of Revenue's insurance lapse and penalty rules.

The legal penalty is only part of the problem.

If you cause a wreck without coverage, there is no liability policy stepping in to pay covered claims on your behalf. That can put your paycheck, savings, and future tax refunds under pressure if the other party pursues the balance.

State minimum coverage keeps you legal. It does not automatically protect your finances.

Where drivers get tripped up

Drivers often hear "minimum coverage" and assume it is a reasonable baseline. It is only the lowest amount Georgia will accept to register and operate a vehicle legally.

That difference matters more now because repair costs, medical treatment, and vehicle prices have all climbed. A policy can meet Georgia law and still leave a family exposed after one bad loss. That is why an independent agent adds value here. The job is not just to pull a cheap quote. It is to compare carriers, explain where the legal minimum stops, and help you buy limits you can afford before an accident makes the choice for you.

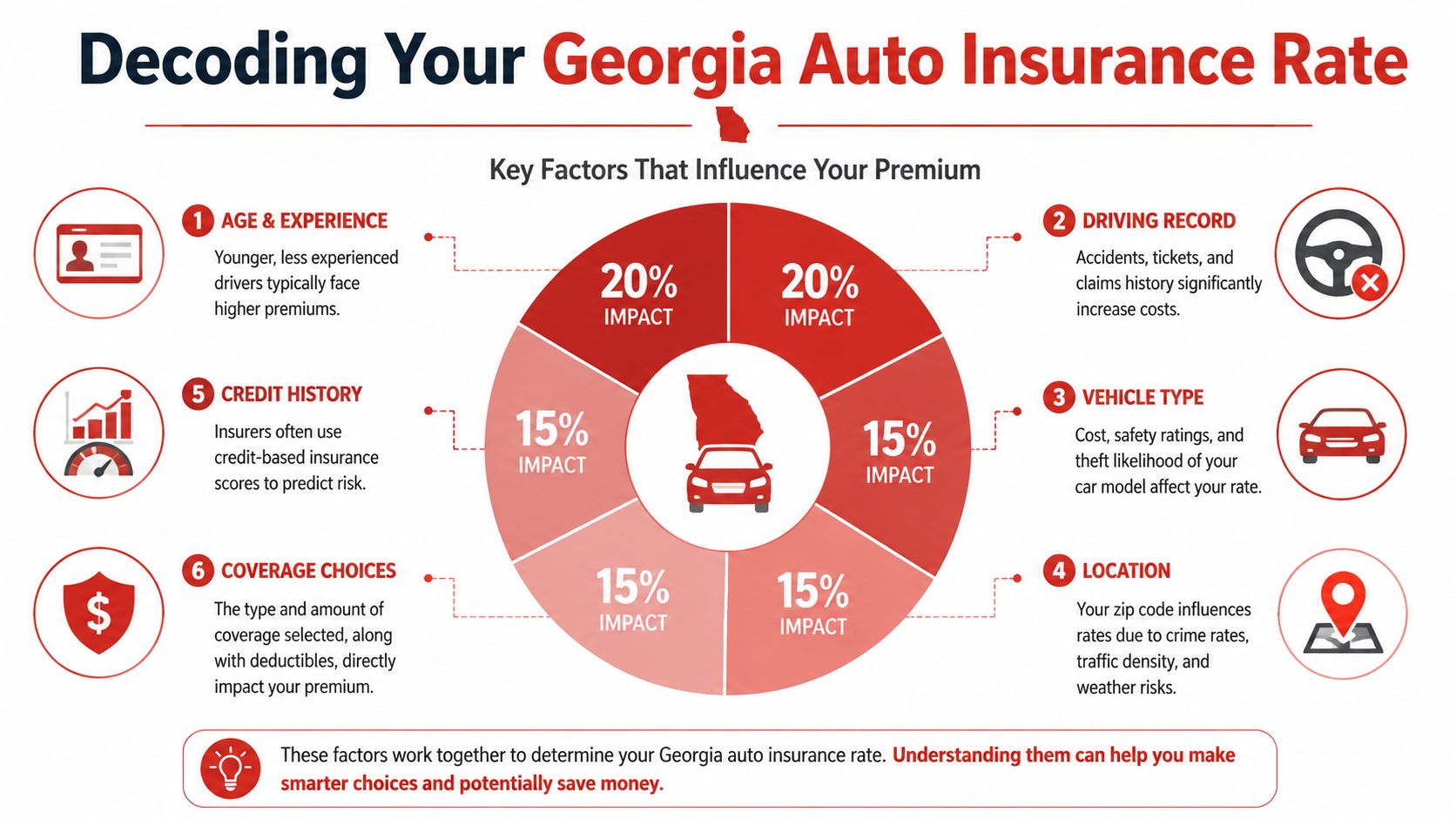

Decoding Your Georgia Auto Insurance Rate

A driver in Marietta and a driver in Macon can own the same car, carry the same limits, and still see very different prices. I see that every week. The quote is built from a mix of claim risk, repair costs, traffic patterns, driving history, and how much of the risk you keep versus pass to the insurer.

That matters in Georgia because price and protection are tied together. A low premium often means lower limits, a higher deductible, or fewer coverages for your own car. In an at-fault state, that trade-off deserves a close look before you buy.

The biggest rating factors

Insurers do not use one flat Georgia rate. They price each policy based on several details, and a few of them move the premium more than drivers expect.

- Driving record: Tickets, at-fault accidents, and recent claims usually push rates up fast. One violation can follow you for years at renewal time.

- Location: Your ZIP code affects the quote because carriers look at local claim frequency, theft, traffic density, lawsuit trends, and repair costs.

- Coverage level: Liability-only costs less because it covers damage you cause to others. Full coverage costs more because it also includes coverage for your own vehicle after a covered crash, theft, hail loss, or similar claim. If you want a plain-English breakdown, compare full coverage vs. liability insurance in Georgia.

- Vehicle choice: Some cars are cheaper to insure because parts are easier to get and repair bills are lower. Others carry higher rates due to theft risk, expensive sensors, or higher claim severity.

- Driver details: Age, years licensed, prior insurance history, annual mileage, and household drivers can all affect the premium.

Why ZIP code changes the price

Drivers often ask why a move of only a few miles changed the bill. The answer is simple. Car insurance is priced partly by local loss patterns, not just by your personal habits.

A new address can place you in an area with more uninsured drivers, more severe crashes, more theft claims, or higher body shop labor rates. Even if your car, commute, and record stay the same, the insurer may expect a different claim cost in that neighborhood.

Your rate reflects both you and the place where the car is garaged.

What you can control and what you can't

Some pricing factors are slow to change. Others are worth reviewing right now.

| Harder to change | Usually easier to adjust |

|---|---|

| ZIP code | Deductible amount |

| Age and driving experience | Liability limits |

| Past claims and violations | Vehicle choice next time you buy |

| Local repair and claim trends | Removing drivers or cars that no longer belong on the policy |

| Credit-based insurance factors, where allowed | Asking about available discounts |

I tell Georgia drivers to focus on the levers that produce savings without creating a bigger gap after a wreck. Keep the record clean. Review deductibles once a year. Make sure the policy still matches who drives the car and where it is kept. If a teenager left for school without a vehicle, or an old car was sold months ago, clean that up.

Cheap quotes can cost more later

The lowest quote on the screen is often the one that leaves the most risk with you. That can show up as low bodily injury limits, no collision coverage on a financed car, no rental reimbursement, or a deductible that looks fine until you have to pay it after a loss.

That is why independent agents earn their keep here. We can line up the coverages first, then compare prices across carriers, so you are not accidentally choosing a policy that is cheap only because it exposes your savings. In Georgia, where the legal minimum is already thin for current repair and medical costs, that difference matters.

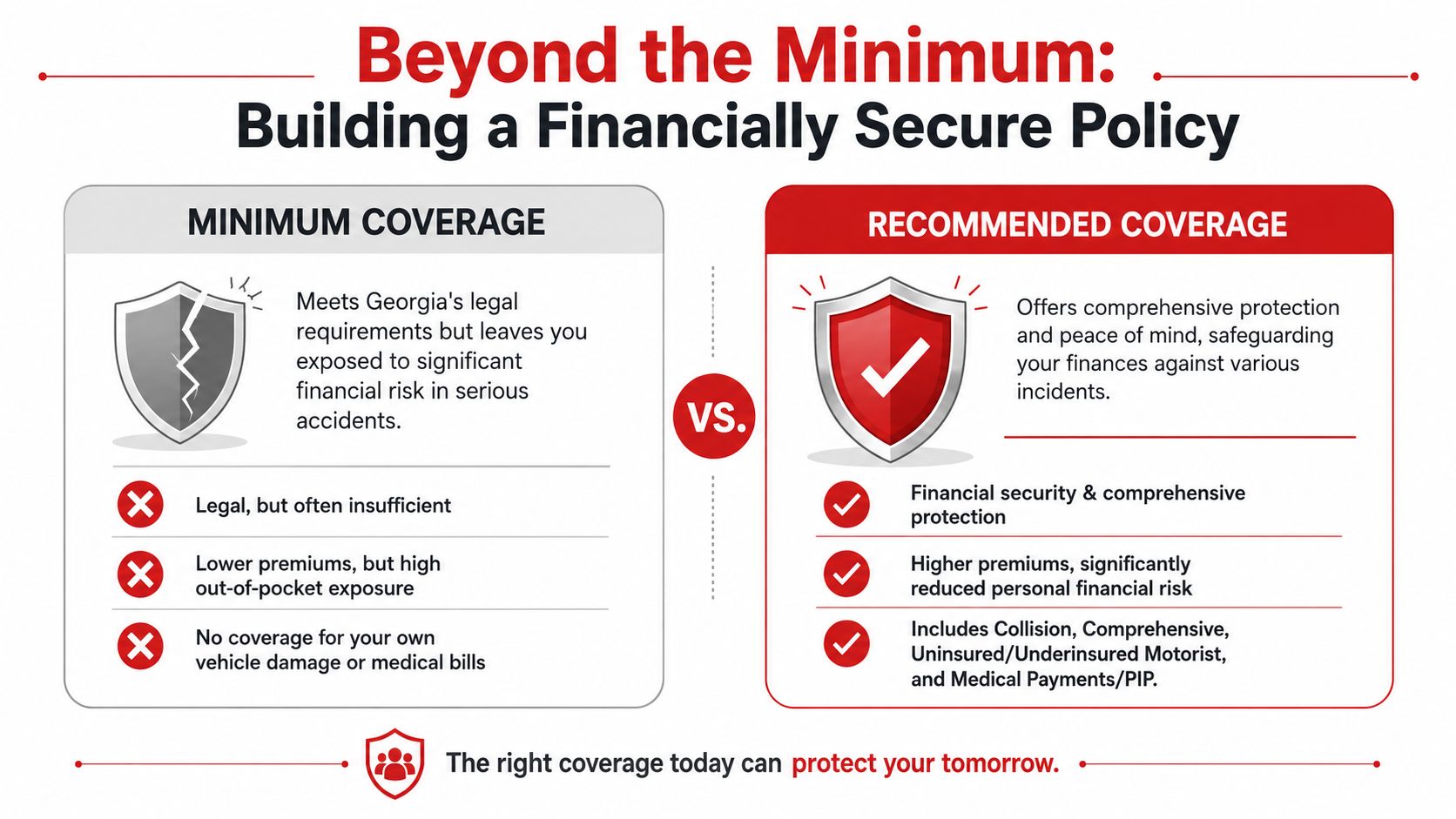

Beyond the Minimum Building a Financially Secure Policy

Minimum coverage keeps you legal. It doesn't reliably keep you financially safe.

Georgia is an at-fault state. If you cause an accident, your liability coverage is expected to respond to the damage and injuries you caused, up to your policy limits. The problem is that many drivers stop at the legal minimum and assume that's enough. In real claims, it often isn't.

One source on Georgia minimum requirements notes that drivers in the state pay an average of $157 per month for liability insurance, compared with a $98 national average, while still carrying minimum limits that may be too low for current medical and repair costs in an at-fault system, as explained in this Georgia minimum coverage overview.

Where minimum coverage falls short

A serious accident can create multiple layers of expense at once. Injury claims, property damage, towing, rental needs, and lost-use disputes don't arrive one by one. They stack.

With a minimum-only policy, the biggest gaps usually look like this:

- Your limits may be exhausted quickly: Once liability limits are used up, you may be left dealing with amounts above those caps yourself.

- Your own car isn't protected: Liability insurance doesn't repair your vehicle after a crash you caused.

- Your own immediate medical costs may not be addressed by liability alone: That can create pressure while fault and claim details are still being sorted out.

The optional coverage too many drivers reject

Georgia law requires insurers to offer uninsured and underinsured motorist coverage, but drivers can decline it in writing, as explained in this summary of Georgia UM/UIM rules under O.C.G.A. §33-7-11.

That distinction is critical. Many people hear UM/UIM mentioned so often that they assume it's automatic. It isn't.

If a hit-and-run driver disappears, or the at-fault driver carries too little insurance, UM/UIM can be one of the most valuable parts of the policy. Declining it may save premium in the short term, but it can leave you exposed in exactly the kind of accident you can't control.

Coverage check: Ask whether UM/UIM is on the policy, not just whether it was offered. Those are not the same thing.

The coverages that usually deserve a hard look

Instead of thinking in terms of “full coverage” as a vague bundle, think about what each part does.

Liability above the minimum

Higher liability limits can help protect income, savings, and other assets when damages are more severe than the state minimum can handle. This is often the first place I'd strengthen a Georgia policy.

Collision

Collision helps with damage to your own vehicle after an accident, regardless of fault structure in the claim process. If you rely on your car daily and couldn't comfortably absorb a major repair or total loss, this matters.

Comprehensive

Coverage for non-collision incidents applies to many losses such as theft, vandalism, weather-related damage, and animal strikes. It's especially important when replacing the car out of pocket would be a real burden.

Medical Payments

Medical Payments can help with immediate medical expenses after an accident. Drivers often overlook it until they need quick help with out-of-pocket treatment costs.

For a more detailed breakdown of how policy structure affects protection, this guide on full coverage versus liability insurance gives a helpful side-by-side view.

A better way to think about coverage

Don't ask, “What's the least I can buy?” Ask, “What financial hit can I realistically absorb on my own?”

That question usually leads to a stronger policy. Not a reckless one. Not an overpriced one. Just one built for the way life operates after a claim.

Proven Strategies to Lower Your Georgia Insurance Premiums

Saving money on Georgia auto insurance is rarely about one magic discount. It's usually the result of several smart adjustments that lower your premium without stripping out the protection you'll regret losing later.

The key is to cut waste, not coverage.

Start with policy design, not bargain hunting

A lot of drivers shop by monthly payment alone. That's backwards. First make sure the policy reflects how you use the car, who really drives it, and what risk you can afford to retain.

Try this review checklist:

- Check listed drivers: Remove anyone who no longer lives in the household or no longer uses the vehicle regularly, if your insurer allows it.

- Match coverage to the vehicle: An older paid-off car may call for a different structure than a newer vehicle with a loan.

- Review deductibles carefully: Raising a deductible can lower your premium, but only do it if you could pay that amount without scrambling after a loss.

The best savings move is often a cleanup move. Policies collect outdated vehicles, old addresses, and unnecessary add-ons over time.

Discounts worth asking about

Not every carrier offers the same discounts, and not every discount applies to every driver. Still, these are the areas that commonly help:

- Bundling: Combining auto with home or renters coverage often produces stronger pricing than keeping policies separate.

- Safe driving status: A clean record matters. So does avoiding small preventable claims when you can comfortably handle minor losses yourself.

- Good student eligibility: Families with younger drivers should ask about student-related discounts.

- Defensive driving course completion: Some insurers reward approved course completion, especially for drivers trying to offset a ticket or age-related pricing pressure.

- Paperless and payment preferences: Automatic payment and electronic documents can sometimes trim a little off the bill.

Credit and consistency matter

In many cases, insurers use credit-based insurance information when pricing risk. You don't need to become a finance expert to benefit from that. Paying bills on time, correcting obvious reporting errors, and avoiding policy lapses can help keep your insurance profile stronger.

Consistency matters too. Drivers who let coverage lapse often pay more when they come back into the market, even if they didn't have an accident during the gap.

A practical savings order

If you want a sensible order of operations, use this:

- Keep the record clean. Tickets and accidents can cost more than any single discount can save.

- Bundle if it makes sense. This is often one of the most useful places to look.

- Adjust deductibles. Raise them only to a level you could pay comfortably.

- Review vehicle decisions. Before buying your next car, get insurance quotes on the models you're considering.

- Re-shop periodically. Not every year has to be a shopping year, but don't assume loyalty always equals savings.

What doesn't work

Cutting UM/UIM just to save a little premium is usually a weak trade-off. Dropping collision on a car you still couldn't afford to replace can also backfire.

The right savings strategy preserves the coverages that protect against financial disruption and trims the parts of the policy that no longer fit your situation.

Navigating Special Insurance Situations in Georgia

Some Georgia drivers need more than a standard quote. The policy may be straightforward, but the surrounding situation isn't. That's where details matter.

If you need SR 22 support after a suspension

A suspended-license driver usually isn't looking for theory. They need to know what gets them back on the road legally and how to avoid another setback.

If the state requires an SR-22 filing, don't treat it like a normal shopping exercise. Confirm exactly what filing is needed, make sure the policy is active before any deadline passes, and don't let the coverage lapse afterward. A lapse during a filing period can create a second round of problems.

This guide to auto insurance for drivers with suspended licenses is a useful starting point if you're sorting through reinstatement issues.

If you're adding a teen driver

Parents usually see the premium jump and assume there's no way around it. There often is, at least in part.

Start with the car assignment. A teen on the most expensive vehicle in the household can make the policy harder to price. Ask about student-related discounts, driving training options, and whether the teen should be listed on one vehicle or the whole household setup based on the insurer's rules. The goal isn't just lowering the rate. It's making sure the new driver is insured correctly.

For families, the cheapest way to insure a teen isn't always the safest paperwork choice. Accuracy matters more than trying to outsmart the application.

If you're military or headed out of state for school

Military households often have moving pieces. Garaging address, deployment, vehicle storage, and who still drives the car all affect how the policy should be written. Before a deployment or long-term duty change, review every vehicle on the policy and confirm whether use, storage, or driver status needs updating.

College students create a similar issue. If a student attends school in Georgia but remains connected to a parent household elsewhere, the right setup depends on where the vehicle is kept, who owns it, and how often it's used. A rushed online application can miss that nuance.

If your situation changed recently

A move, marriage, divorce, new job commute, new vehicle, or adult child leaving the household can all change how your policy should be structured. Most insurance mistakes don't happen because people intended to cut corners. They happen because the policy never got updated after life changed.

When the situation is unusual, slow down and verify every detail before you bind coverage.

How to Buy Your Georgia Auto Insurance with Confidence

Buying Georgia auto insurance gets easier when you stop treating it like a race to the cheapest monthly number. A good buying process starts with your real exposure, not the ad price.

Step one, gather the right information

Before you shop, pull together the basics:

- Driver details: License information, accident history, and ticket history

- Vehicle details: VIN, lienholder information if financed, and current mileage estimate

- Usage facts: Commute, business use, household drivers, and garaging address

- Current policy details: Existing limits, deductibles, and optional coverages

This step saves time, but above all, it prevents bad comparisons. Quotes built on mismatched data aren't useful.

Step two, decide what you're protecting

A solid policy decision usually comes down to three questions:

| Question | Why it matters |

|---|---|

| Could you replace or repair your car without strain? | Helps determine whether collision and comprehensive make sense |

| Could you absorb a larger deductible comfortably? | Affects premium and claim-time cash flow |

| Would minimum liability protect your income and savings in a serious claim? | Guides liability limit decisions |

If those answers make you uneasy, that's usually a sign to build beyond the bare minimum.

Step three, compare value instead of just price

Many drivers encounter difficulties when evaluating auto insurance quotes. One quote may cost less because it excludes UM/UIM, carries higher deductibles than you intended, or reduces key protections you assumed were included.

When comparing options, line up these items side by side:

- Liability limits

- UM/UIM election status

- Collision and non-collision deductibles

- Medical-related coverage

- Any exclusions that affect household drivers or vehicle use

A quote is only “better” if it improves price without weakening the essential parts of the policy you need.

Here's a look at the kind of family-focused insurance experience many shoppers want from a modern agency website.

Step four, use an independent agent when the trade-offs aren't obvious

This is the point where an independent agency can save a lot of frustration. Instead of filling out form after form on separate sites, you can have one professional compare options across multiple carriers and flag the differences that matter.

That's especially useful in Georgia, where rates can shift based on location, driving history, household structure, and coverage elections. An independent agent can often spot issues that a quick online quote flow won't explain clearly, such as whether you declined a valuable optional coverage or chose a deductible that looks fine until claim day.

A good buying decision isn't “lowest premium wins.” It's “best protection for the price I can sustain.”

Step five, review before you bind

Before you say yes, check the declarations page or proposal carefully. Verify names, vehicles, garaging address, lienholder, limits, deductibles, and optional coverage elections.

If something is wrong at the start, fixing it after a claim is far harder than fixing it before payment.

If you want help comparing policies without doing all the legwork yourself, Select Insurance Group, Inc. can help you shop Georgia auto insurance with an independent agency approach. Their team compares instant quotes from multiple carriers, explains the trade-offs in plain language, and helps drivers find coverage that fits both their budget and their real risk.