Florida homeowners aren't imagining the pressure. Florida led the nation in home insurance non-renewal rates, with a 280% increase between 2018 and 2023, and the state's non-renewal rate reached 2.99% in 2023, far above Louisiana's 1.8% [Florida non-renewal data]. If your premium jumped, your carrier tightened underwriting, or you got a notice that made your stomach drop, your experience fits the market.

This is the current state of homeowners insurance in Florida right now. It's expensive, stricter than it used to be, and full of traps for people who assume a policy will work the way it did a few years ago.

The good news is that there are still workable ways to protect your home, compare policies intelligently, and avoid paying for coverage that won't help when a storm hits. The key is understanding how Florida policies are built, where the common gaps hide, and which actions move the needle.

Table of Contents

- The Florida Home Insurance Crisis Is Here

- Decoding Your Florida Homeowners Policy

- Hurricane Deductibles vs Flood Insurance Explained

- Why Florida Home Insurance Costs So Much

- How to Lower Your Premiums with Discounts and Mitigation

- The Smart Way to Get and Compare Quotes in Florida

- Navigating the Claims Process After a Disaster

- Florida Homeowners Insurance FAQs

- Is Citizens the same as regular private homeowners insurance?

- What should I do if I get a non-renewal notice?

- Is sinkhole coverage automatically included?

- Why is the 4-point inspection such a big deal?

- Should I self-insure if premiums are too high?

- What's the biggest mistake Florida homeowners make?

The Florida Home Insurance Crisis Is Here

Florida homeowners now pay far more to insure a house than owners in most other states, and the pressure is not limited to premium increases. The strain shows up in tighter underwriting, tougher inspections, reduced carrier appetite, and more households being pushed into hard choices about coverage. The Florida Office of Insurance Regulation has also tracked major movement in the market, including continued reliance on Citizens as private-market availability shifts [Florida property insurance market updates].

For homeowners, this crisis usually starts with a letter, an inspection report, or a renewal number that no longer fits the budget. A house that cleared underwriting a few years ago can now trigger questions about roof age, plumbing materials, prior claims, or updates that were never documented. That is why many Florida families feel trapped. They are not shopping for better perks. They are trying to keep a necessary policy in place without overpaying or buying a contract that fails them after a storm.

What this crisis looks like in real life

A stressed homeowner usually runs into one of these problems first:

- Renewal shock: the policy stays active, but the premium jumps enough to force a budget reset.

- Inspection friction: an older roof, aging plumbing, dated electrical systems, or HVAC wear creates placement problems.

- Non-renewal: the carrier decides the home no longer fits its underwriting rules.

- Claims anxiety: the homeowner is not confident the insurer will respond smoothly after a major loss.

That last point matters more than many guides admit. In Florida, a low premium can hide a painful setup. A policy may carry a deductible that is much larger than expected, stricter conditions on roof losses, or endorsements that narrow coverage in ways a homeowner does not notice until claim time.

What works

Panic shopping usually ends badly. So does waiting until the final week before renewal.

A better approach is plain and disciplined. Pull the current declarations page. Find out how the home would fare in an inspection today, not how it looked when the policy was first written. Identify the loss that would hurt your finances most. Then compare replacement cost, deductibles, endorsements, and inspection requirements on the same basis.

That is how homeowners insurance Florida buyers protect themselves in a bad market. You do not need insider jargon. You need a clear view of where the financial risk sits, what could trigger a non-renewal, and which compromises are acceptable before you sign.

Decoding Your Florida Homeowners Policy

A Florida homeowners policy can look fine at renewal and still leave a family exposed where it hurts most. I see that problem all the time. The declarations page shows a premium and a coverage limit, but the complete story lies in the deductibles, endorsements, exclusions, and settlement terms.

Start with the declarations page

The declarations page is the summary sheet, and it deserves more attention than the full booklet for most homeowners. It lists the named insured, property address, coverage limits, deductibles, and endorsements that change the standard policy form. If you only review one document before renewal, review that page.

Check these items first:

- Coverage A: the limit for rebuilding the house itself.

- Other coverage buckets: detached structures, personal property, loss of use, and liability.

- Deductibles: including whether hurricane losses use a separate percentage deductible.

- Endorsements: add-ons and restrictions that can expand or narrow what gets paid.

A cheap policy with the wrong endorsements is not a bargain.

What a standard policy usually includes

Most Florida homeowners policies are built around the same core coverage parts, but the limits and conditions vary more than many owners realize.

| Coverage part | Plain-English meaning |

|---|---|

| Dwelling | Repairs to the house after a covered loss |

| Other structures | Protection for detached features such as a shed, fence, or detached garage |

| Personal property | Coverage for belongings inside the home |

| Loss of use | Extra living expenses if a covered loss makes the home temporarily unlivable |

| Liability | Protection if someone claims injury or property damage tied to you |

That list matters, but so do the settlement rules. Some policies pay losses on a replacement cost basis for the dwelling, while some personal property may be settled at actual cash value unless the form or an endorsement says otherwise. That difference can mean a much smaller check than the homeowner expected.

The gaps that cause trouble in Florida

The biggest mistakes usually come from assumptions.

A standard homeowners policy does not cover flood damage from rising water. It also does not pay for wear, deferred maintenance, or every upgrade required to meet current building code unless the policy includes the right protection. If you want a clearer breakdown of the water side of the risk, review understanding flood insurance for Florida homes and compare it with this guide to private flood insurance vs NFIP in Florida.

Older homes face another issue before a claim ever happens. Insurers often want proof that the roof, electrical, plumbing, and HVAC systems still meet underwriting standards. The Florida Office of Insurance Regulation explains that carriers commonly use inspections, including 4-point inspections, as part of underwriting and renewal decisions for older properties [Florida Office of Insurance Regulation consumer resources]. A house can be clean, occupied, and well cared for, then still run into placement trouble because one system shows age, prior repairs, or materials the carrier does not like.

That is why reading only the coverage names is not enough. Homeowners need to know what the policy covers, what it excludes, how losses are settled, and what condition requirements the insurer can enforce before and after a claim. In this market, that is the difference between having a policy on paper and having protection that holds up under pressure.

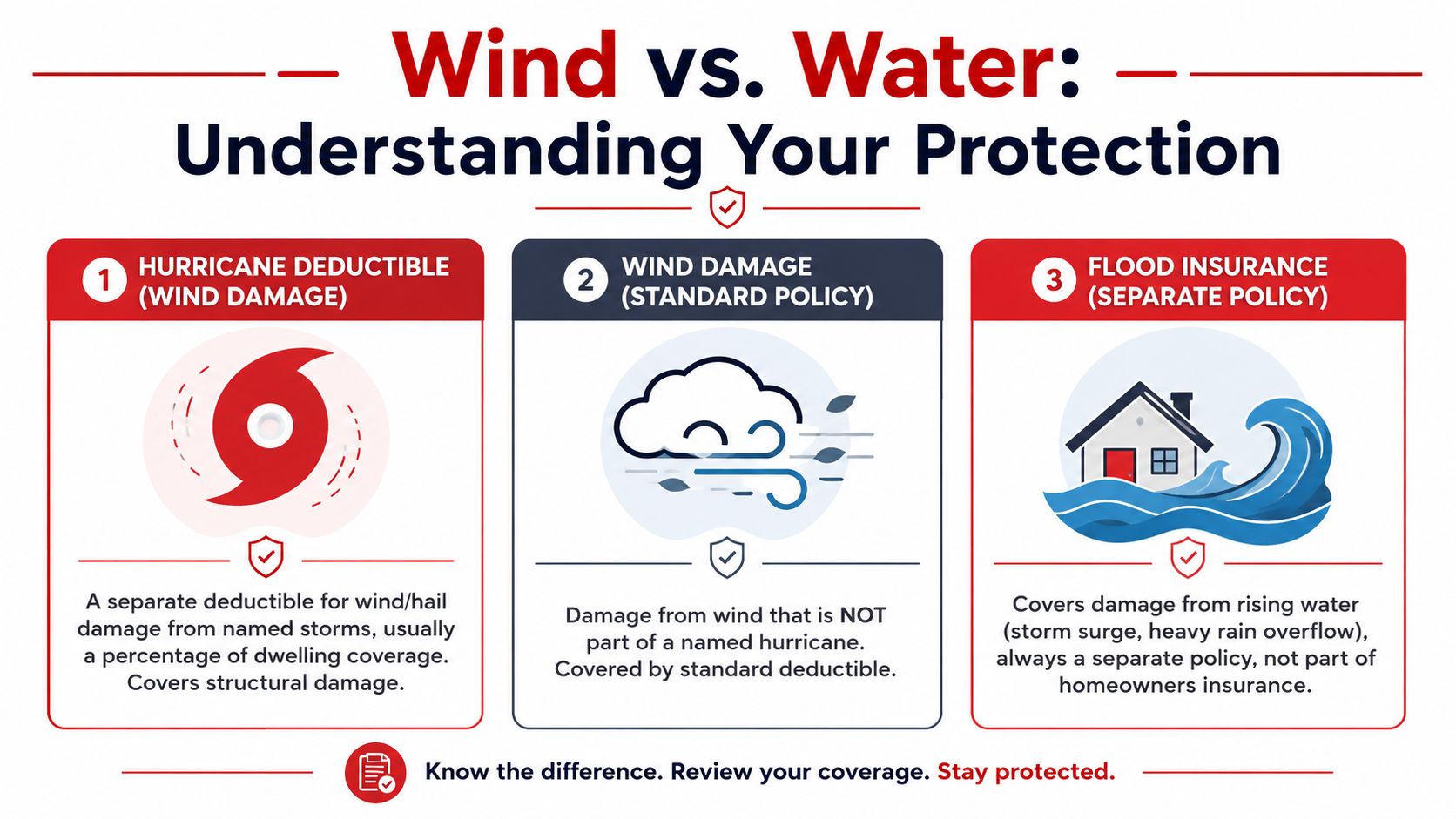

Hurricane Deductibles vs Flood Insurance Explained

This is the most misunderstood part of homeowners insurance Florida coverage. Many owners believe that if a hurricane causes the damage, one policy should handle all of it. That isn't how it works.

The first distinction is simple. Wind damage and flood damage are not the same thing in insurance, even when the same storm causes both.

Wind damage and flood damage are not the same claim

If wind tears shingles off your roof, breaks windows, or damages the structure, that usually falls under homeowners coverage, subject to the policy terms and deductible. If rising water enters the home from storm surge, overflow, or similar outside water events, that's a flood issue. Standard homeowners insurance does not absorb that loss.

That's why many homeowners need a separate flood solution. If you want a broader primer before shopping, this guide on understanding flood insurance for Florida homes gives a useful consumer-level overview. It helps people understand why “I'm not in a flood zone” isn't enough by itself to end the conversation.

If you're comparing forms of flood coverage, it also helps to review the differences between private flood insurance and NFIP options in Florida. That comparison matters because the right fit depends on the property, the lender requirements, and how much flexibility you need.

How a storm can trigger different coverage rules

Take a common scenario. A named storm hits your area. Wind peels back part of the roof, rain enters through that opening, and storm surge pushes water into the first floor.

Those damages may be split like this:

- Roof damage from wind: generally handled under the homeowners policy, often subject to the hurricane deductible if the storm qualifies under the policy.

- Interior rain damage tied to a wind-created opening: often addressed with the wind portion of the homeowners claim.

- Water entering from rising external floodwater: handled, if at all, under a separate flood policy.

That split is why homeowners get blindsided after storms. They weren't wrong that the storm caused the damage. They were wrong about how the policy classifies the source of the damage.

If you don't know whether the water came from above, through an opening, or from rising ground water, don't guess. Document what you see and let the claim be evaluated on facts, not assumptions.

The second distinction is the deductible. A hurricane deductible is separate from the standard deductible. It applies under specific storm conditions defined in the policy. Homeowners often focus on the premium and ignore this until claim time. That's a mistake. The lower premium can come with an out-of-pocket amount that feels manageable in theory and painful in reality.

Before you renew, ask one blunt question: “What exact storm damage would be covered under this policy, and which water losses would require separate flood coverage?” If the answer sounds vague, keep asking.

Why Florida Home Insurance Costs So Much

Florida homeowners have absorbed some of the steepest insurance increases in the country, and the reason is more complicated than “hurricanes.”

Carriers price Florida homes for repeated catastrophe risk, expensive claims, and a market where writing new business can go bad fast. A house does not have to sit on the beach to trigger that concern. Roof age, prior claims, local litigation patterns, repair inflation, and reinsurance costs all feed into the number on your renewal.

Catastrophe risk is only the first layer

Wind exposure still drives the conversation. State regulators at the Florida Office of Insurance Regulation track major shifts in availability and pricing because storm losses affect the entire market, not just the counties that take a direct hit.

The pressure shows up after landfall in repair bills and in the cost insurers pay to protect themselves. Global reinsurer analysts at Swiss Re Institute regularly note that rising catastrophe losses are increasing the price of reinsurance. In plain English, insurers are paying more for their own backup coverage, and that cost gets pushed down to policyholders.

Then there is the concentration problem. Florida has a huge number of homes exposed to the same weather system at the same time. The Insurance Information Institute's Florida market analysis explains why carriers become selective when too much exposure stacks up in one region. That is why two similar houses can get very different treatment based on ZIP code alone.

Claims costs in Florida are unusually hard to control

After a major storm, every part of the claim gets more expensive. Roofers get booked out. Materials tighten up. Temporary dry-in work costs more. Contractors and public adjusters flood the same neighborhoods. Even homeowners with modest damage can end up in a pricing surge created by losses all around them.

Florida also has a history of claim severity that makes underwriters cautious. The issue is not only how often storms happen. It is how expensive each claim becomes once emergency repairs, code upgrades, and longer rebuild timelines are involved.

That is why a premium can jump even if you never filed a claim.

Underwriting has gotten stricter because insurers are trying to avoid bad risks before they start

This is the part many guides soften, but homeowners feel it every renewal season. Insurers are not only charging more. They are screening harder.

Older roofs, outdated electrical panels, polybutylene plumbing, prior water losses, and vacant-property concerns can push a home from standard market to limited options very quickly. In some cases, the issue is not whether coverage exists. The issue is whether any carrier wants the risk at a price a homeowner can live with.

For owners in harder-to-place areas, this overview of Orlando homeowners insurance for high-risk zones explains the property details underwriters commonly examine.

A few practical realities matter here:

- Location changes availability as much as price. Some carriers stop writing in certain areas or tighten their inspection standards.

- Condition matters more than owners expect. An aging roof or outdated system can trigger a non-renewal, a higher premium, or a requirement to repair before binding.

- Cheap coverage can be expensive later. A lower quote may come with tighter exclusions, higher deductibles, or settlement terms that leave you exposed after a loss.

Homeowners can reduce some of this pressure by making the property easier to insure before renewal shopping starts. Simple hardening and maintenance steps will not fix the statewide market, but they can improve how your home is viewed. Pinnacle's advice on home weatherproofing is a useful starting point for that work.

In Florida, your premium reflects more than storm odds. It reflects how your home is built, how costly it would be to repair, how much regional exposure the carrier already has, and how much uncertainty the insurer is willing to accept.

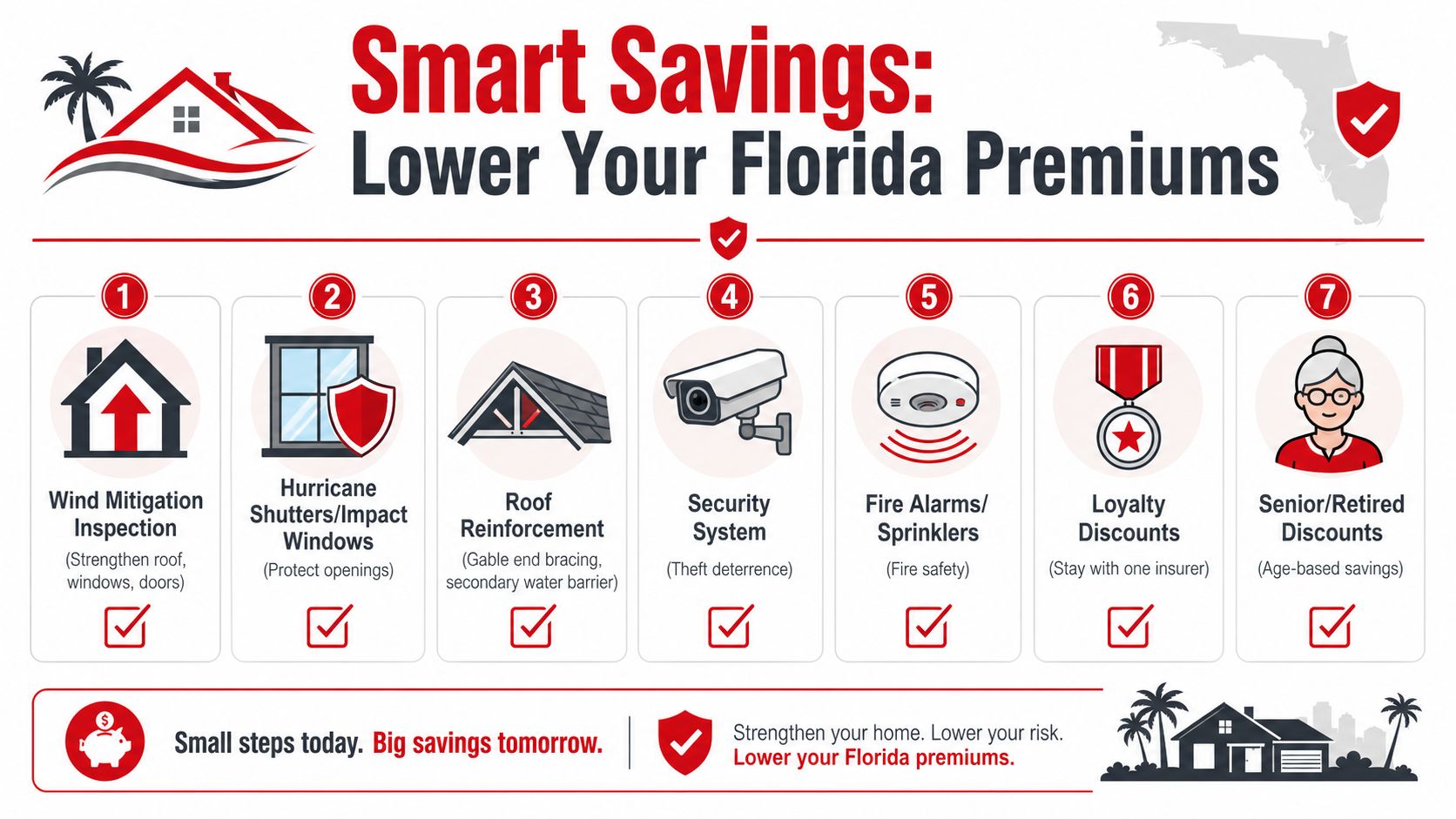

How to Lower Your Premiums with Discounts and Mitigation

Florida homeowners have seen premium increases large enough to wipe out the savings from shopping around. In this market, the biggest wins often come from making the home easier to insure, not from cutting coverage and hoping for the best.

Cosmetic upgrades rarely change an underwriter's view of risk. Protective features do. A remodeled kitchen may raise the home's value, but it does not do much for wind resistance, water intrusion, or claim severity after a storm.

The improvements that usually matter most are the ones tied to documented loss prevention:

- Roof hardening: roof condition, attachment method, secondary water resistance, and other details that reduce wind and water damage.

- Opening protection: impact-rated windows, shutters, and stronger exterior doors.

- Garage door reinforcement: garage failures can create major pressure changes during a wind event.

- Water loss prevention: maintenance and updates that reduce the chance of leaks, backups, and preventable interior damage.

If you want a practical homeowner-oriented checklist on prevention, Pinnacle's advice on home weatherproofing is a good companion resource. It's useful because it approaches the home like a system, not just a policy premium.

A wind mitigation report can save real money, but only if the credits are there

Many homeowners hear "get a mitigation inspection" and assume savings are automatic. They are not. The report has value when it documents features the carrier credits, such as roof-to-wall connections, roof deck attachment, opening protection, and roof shape.

That distinction matters. I have seen owners pay for an inspection expecting a major discount, only to learn their home lacks the features that drive meaningful credits. The report still helps clarify where the house stands, but the best use of it is often tactical: confirm what you already have, identify the upgrades that matter most, and bring that documentation into renewal shopping.

A good independent agent can help you match those reports to carriers that still give fair credit for them. If you are not sure how that model works, this explanation of what an independent insurance agency does for homeowners is worth a quick read.

The 4-point inspection often decides whether you get options at all

For older homes, underwriting usually starts with the 4-point inspection. Carriers use it to review the four systems that create the most concern: roof, electrical, plumbing, and HVAC. The exact age trigger and inspection requirement vary by company, but older homes commonly need this report before a policy is issued or renewed.

The strategic mistake is waiting for the inspector to find obvious problems.

Use the process this way:

- Check likely trouble spots before ordering the report. Older water heaters, recalled electrical panels, active leaks, and worn HVAC components are common friction points.

- Handle repair items that affect eligibility first. A modest update can be cheaper than losing access to better carriers or getting pushed into a more expensive option.

- Keep proof of work. Invoices, permits, photos, and inspection sign-offs help resolve underwriting questions faster.

- Pair it with mitigation documentation when appropriate. Eligibility and discount opportunities are different issues, and each needs its own support.

Roof age deserves special attention because it creates confusion and bad advice. Florida law changed to limit non-renewals based only on roof age in certain situations, but that does not mean every older roof is acceptable. Carriers still look at condition, useful life, and inspection results. A roof that is aging but in sound condition may remain insurable with the right documentation. A roof with brittle shingles, visible deterioration, or signs of prior patchwork may still create placement problems.

That is the practical trade-off most guides skip. Spending money on mitigation does not guarantee a lower premium, and raising deductibles does not fix an underwriting problem. The goal is to improve both insurability and price, in that order. In Florida's current market, a home that underwriters view as better protected usually gets more realistic options than a home that asks for less coverage.

The Smart Way to Get and Compare Quotes in Florida

Rate swings in Florida can be dramatic. Two quotes for the same house can come back far apart in price, yet the cheaper one may leave out protections you assumed were included.

That is why quote shopping has to be disciplined. The goal is to compare equal coverage, equal deductibles, and equal assumptions about the home. If those inputs change from one quote to the next, the price difference tells you very little.

Get your house data straight before you shop

Start with the information underwriters use to decide both eligibility and price. That usually includes roof age and condition, electrical, plumbing, and HVAC updates, prior claims, square footage, occupancy, and any recent inspection reports.

Then set your own boundaries before anyone starts quoting. Decide what deductible you could pay without creating a second financial problem after a storm. Decide which coverages you want included from the start. Decide which exclusions, limitations, or settlement terms you will not accept.

That prep work saves time, but it also keeps you from being steered into a policy that only looks affordable.

Compare policies line by line

A real comparison usually looks like a worksheet, not a pile of quote emails. Put each offer side by side and review the terms one line at a time.

| What to compare | Why it matters |

|---|---|

| Dwelling coverage | A lower limit can make a quote look cheaper fast |

| Deductibles | Hurricane and standard deductibles can change what you pay out of pocket after a loss |

| Water-related limitations | Misunderstandings here get expensive fast |

| Endorsements and exclusions | They often explain the real difference between two similar premiums |

| Inspection requirements | A quote has limited value if follow-up underwriting will reject the home |

A cheap quote is not a win if the water damage language is tighter, the hurricane deductible is higher than you expected, or the carrier is relying on inaccurate home data. Those are the details that create trouble later, especially when a claim is disputed.

Ask a harder question than “Which quote costs less?” Ask, “Which policy still holds up when the claim is complicated?”

Know who is shopping the market for you

That question matters a lot in Florida because market appetite changes fast. Some agents can offer only one carrier's policy. Others can check multiple carriers and look for a better fit based on the home's age, location, loss history, or inspection profile. If you want a plain-English explanation, this article on what an independent insurance agency does is a helpful reference.

Broader market access does not guarantee a low premium. It does improve the odds of finding a policy that matches the property instead of forcing the property into one carrier's box. Select Insurance Group, Inc. is one example of an independent agency model that shops multiple carriers for Florida homeowners, which can be useful when a home has underwriting complications.

One more practical point. Ask each agent whether they quoted the same coverage form, the same deductible structure, and the same updates to the home. If they did not, ask for a revised comparison before you bind coverage.

And if a major claim later turns into a coverage dispute or bad-faith concern, knowing your legal options matters. This Florida guide to insurance lawsuits is a useful starting point.

If a quote comes in much lower than the rest, assume there is a reason and find it before you sign. In this market, the expensive mistake is rarely the premium. It is discovering after a storm that the bargain quote was never the same policy at all.

Navigating the Claims Process After a Disaster

The claim process is where policy language becomes real. It's also where stress makes people rush, guess, or throw away evidence they later need.

One of the biggest frustrations in Florida is uncertainty about what happens after the storm. Homeowners consistently ask, “What will my insurer do after a hurricane?”, but few content sources provide concrete, data-backed answers about actual insurer response times, recovery capabilities, or fiscal readiness post-disaster [post-hurricane insurer response concern]. That uncertainty is justified.

What to do in the first day

After a disaster, the sequence matters.

First, protect people. Then protect evidence. Then protect the property from further damage if it's safe to do so.

A strong first-day routine looks like this:

- Confirm safety and follow emergency instructions.

- Photograph and video everything before cleanup starts. Wide shots first, close-ups second.

- Make temporary protective repairs if safe. Think tarping, drying, boarding, and moving salvageable property.

- Notify the insurer promptly.

- Start a claim file. Keep every email, estimate, receipt, and note in one place.

Keep a written log with dates, times, names, and what each person said. Memory gets unreliable fast after a major storm.

How to keep your claim from going sideways

The homeowner who does best in a difficult claim usually does three things well. They document thoroughly, they communicate in writing when possible, and they don't exaggerate.

If an adjuster visits, walk the damage with them carefully. Show all affected areas, including secondary damage that might be easy to miss. If emergency mitigation was necessary, save the receipts and the photos showing why you acted.

Be careful with cleanup crews and repair promises made in the immediate aftermath. Fast help matters, but so does paper trail discipline. If there's a serious dispute and you need to understand the legal side at a consumer level, this Florida guide to insurance lawsuits is a helpful starting point for understanding when a disagreement becomes more than an ordinary claims issue.

A claim is not just a story about damage. It's a file built from proof. The better that file is, the stronger your position.

Florida Homeowners Insurance FAQs

Is Citizens the same as regular private homeowners insurance?

No. Citizens is generally understood as the state-run option people turn to when private-market placement is limited or unavailable. It can be necessary coverage for some homes, but many homeowners should still review whether private-market options are available at renewal.

What should I do if I get a non-renewal notice?

Don't wait. Pull the notice, your current declarations page, and any recent inspection or claim documents. Then start remarketing immediately so you have time to address roof questions, inspection issues, or coverage gaps before the current policy ends.

Is sinkhole coverage automatically included?

Don't assume that it is. Florida homeowners need to read the policy and endorsements closely and ask for plain-English clarification on what earth movement or sinkhole-related losses are and are not covered.

Why is the 4-point inspection such a big deal?

Because it isn't just a form. For many older Florida homes, it's the underwriting checkpoint that determines whether the roof, electrical, plumbing, and HVAC systems are acceptable for a new policy or renewal.

Should I self-insure if premiums are too high?

That's a financial risk decision, not just an insurance decision. Going without coverage may reduce your immediate bill, but it can expose you to a catastrophic property loss you'd have to absorb personally. For financed homes, lender requirements can also limit that choice.

What's the biggest mistake Florida homeowners make?

They buy on premium alone. In this market, the dangerous mistakes usually involve deductible shock, water exclusions, inspection surprises, or assuming hurricane damage and flood damage are handled the same way.

If you want help sorting through homeowners insurance Florida options without guessing, Select Insurance Group, Inc. can review your current policy, explain the trade-offs in plain language, and help you compare available coverage choices for your home.