You're probably doing what most Florida drivers do when renewal hits. Open a few tabs, punch in your ZIP code, click for a “free quote,” and then wonder why every number is different.

That confusion isn't your fault. In Florida, a cheap-looking quote can hide weak coverage, a missing driver, the wrong deductible, or a rate that changes the minute the carrier verifies your record. If you want free insurance quotes in Florida that are useful, you need two things: the right information going in, and a clean way to compare what comes back.

This guide is the practical version. No fluff. No pretending the lowest price is always the best deal. Just how to shop smart in one of the toughest insurance markets in the country, avoid the common traps, and land on a policy you can live with.

Table of Contents

- Why Getting Insurance in Florida Is So Different

- Before You Quote Gather Your Key Information

- Requesting the Right Coverage for Your Needs

- Smart Strategies to Lower Your Florida Insurance Premiums

- Comparing Quotes Apples to Apples Not Estimates to Promises

- How Select Insurance Group Makes It Simple

- Florida Insurance FAQs Your Questions Answered

Why Getting Insurance in Florida Is So Different

You get a free quote online, the price looks decent, and then underlying details start to surface. The car is financed. A household driver was left off. The coverage is bare-bones. In Florida, that kind of gap happens all the time because this market is expensive, weather-exposed, and full of policy details that change the price fast.

That is why Florida shoppers need to be careful with the word "free." The quote may not cost anything to request, but a cheap number that is built on thin coverage or incomplete information can cost plenty later.

Florida prices start from a higher baseline

Florida drivers deal with a tougher insurance market than drivers in many other states. Rates are pushed up by storm exposure, heavy traffic, higher repair costs, fraud concerns, and a large number of uninsured or underinsured drivers. The result is simple. Many quotes start high before you change a single coverage option.

That creates a common mistake. Shoppers compare a Florida quote to what a friend pays in Georgia, Ohio, or North Carolina and assume something is wrong. Usually, the better question is whether the quote makes sense for Florida and whether the coverages match.

For a broader explanation of how Florida rules and claim trends affect auto policies, this ultimate Florida auto insurance guide gives helpful background.

Practical rule: In Florida, an unusually low quote often means reduced protection, missing driver information, or both.

State minimum coverage is only the legal starting point

Florida requires drivers to carry at least $10,000 in Personal Injury Protection and $10,000 in Property Damage Liability under the state's no-fault system, according to the Florida Highway Safety and Motor Vehicles insurance requirements page. That gets you legal. It does not mean you are well protected.

I see this confusion a lot. Drivers hear "no-fault" and assume their injuries, their passengers, and their car are fully covered after a crash. That is not how these policies work in real life.

A few Florida trouble spots come up again and again:

- PIP has limits: It can help with injury-related costs, but it does not mean every medical bill gets paid in full.

- PDL only covers damage you cause to someone else's property: It does not pay to repair your own vehicle.

- Bodily injury liability is not included in the basic legal minimum for many drivers: That surprises people after a serious accident.

- Uninsured motorist coverage is often skipped to save money: In Florida, that can be a costly shortcut.

There is another myth worth clearing up. There is no special Florida government car insurance program that gives most drivers a cheaper standard policy just because money is tight. Real savings usually come from choosing the right deductibles, discounts, vehicle, and coverage structure, not from chasing a program that does not exist.

The goal is not to get the lowest quote on the screen. The goal is to get an accurate quote for coverage that will hold up in a Florida claim.

Before You Quote Gather Your Key Information

Most bad quotes start with missing details. The form looks simple, so people rush through it. Then the final price changes, a driver gets excluded, or the policy has to be corrected after purchase.

You'll get a much cleaner result if you spend a few minutes getting organized first.

What to have ready for auto insurance

For car insurance, accuracy depends on details that many people guess at. Guessing is what turns a “free quote” into a bad surprise later.

Bring these together before you start:

- Driver details: License numbers, dates of birth, and full names for everyone in the household who should be listed.

- Vehicle details: Year, make, model, trim if you know it, and the VIN for each vehicle.

- Use of the vehicle: Whether it's a commute car, business-use vehicle, or mostly personal use.

- Current insurance information: Your present carrier, coverage levels, and renewal date if you have an active policy.

- Driving history: Accidents, tickets, claims, lapses in coverage, and any license issues.

- Financing status: Whether the car is owned outright, financed, or leased.

A quote built on a guessed VIN or partial driving history isn't a real shopping result. It's just a placeholder.

One more thing people miss: mileage and garaging. If the car lives in one ZIP code but you quote it in another, the pricing can shift. Same if the annual mileage is way off.

What to gather for home renters and small business coverage

Property quotes also go sideways when people answer from memory instead of records.

For homeowners or renters, pull together:

| Policy type | Key details to gather |

|---|---|

| Homeowners | Property address, year built, roof age, construction type, updates to plumbing/electrical/HVAC, security features, prior claims |

| Renters | Address, estimated value of personal belongings, pet information if applicable, prior claims |

| Condo | Unit details, association insurance responsibilities, interior improvements, personal property estimate |

| Small business | Business name, location, operations, payroll estimate, vehicles used, current policy info, claims history |

For free insurance quotes in Florida, the goal is simple: make the quote match real life. If you do that, you'll spend less time fixing errors and more time deciding what coverage makes sense.

Requesting the Right Coverage for Your Needs

A quote can be accurate and still be wrong for you. That happens when the price is built on coverage you'd never choose if somebody explained it plainly.

The fix is to ask for specific coverage on purpose, not just “full coverage” or “minimum coverage” and hope for the best.

What to ask for on an auto quote

For Florida auto insurance, start with the structure of the policy, not the premium.

A practical request usually includes:

- Liability discussion: Don't stop at the state minimum. Ask what liability limits are being quoted and what higher options look like.

- Collision coverage: Request this if you want protection for damage to your own vehicle after a crash.

- Non-collision coverage: Ask for this if you want coverage for non-collision losses such as theft, vandalism, or weather-related damage.

- Uninsured or underinsured motorist discussion: In Florida, this is worth a serious conversation.

- Medical and injury review: Confirm how PIP fits with the rest of your protection.

- Rental reimbursement and roadside options: Small add-ons can matter if you rely on the car every day.

If you've got an older vehicle, it may be reasonable to review whether collision and other physical damage coverage still make sense. But don't remove them automatically just because someone says the car is “not worth much.” The better question is whether you could comfortably replace or repair it out of pocket.

“Cheap” auto insurance is only cheap until you have to pay the uncovered part yourself.

What to request for property and business policies

For homeowners, ask for a quote based on a standard homeowners form that clearly shows what the dwelling, personal property, liability, and loss-of-use sections look like. Then ask what is not covered. That second question matters more than commonly understood.

A few practical points:

- Flood isn't automatic: Many Florida property owners assume water damage is just water damage. It isn't. Flood needs its own discussion.

- Deductibles matter as much as premium: A low premium with a deductible you can't handle isn't a strong deal.

- Renters need liability too: Too many renters think the policy is only about furniture and clothes.

- Business owners should ask about package options: If you run a small operation, it often makes sense to quote property and liability together rather than piecing things together blindly.

For any policy type, ask the agent to show the quote in plain language. If you can't explain back what's covered, don't buy it yet.

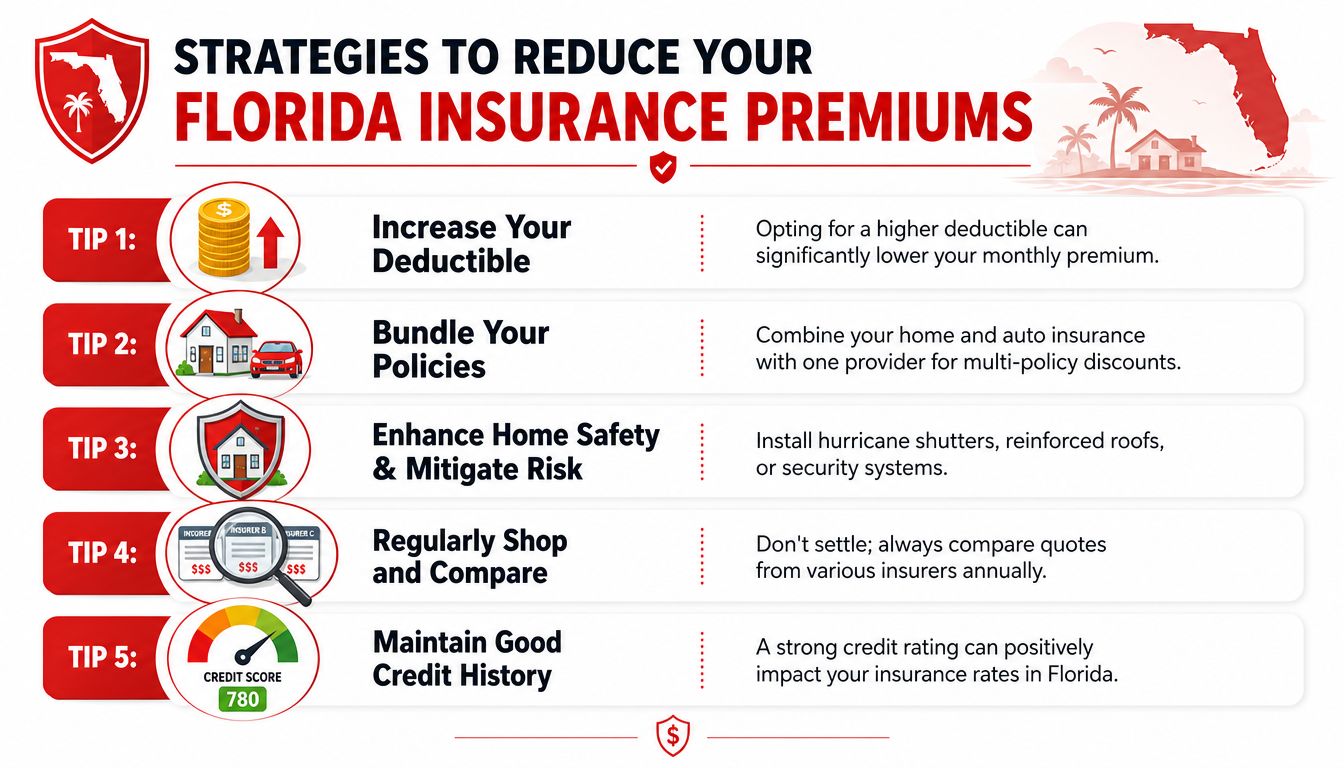

Smart Strategies to Lower Your Florida Insurance Premiums

A Florida driver gets a cheap online quote, feels good about the number, then sees the final premium jump after the application is verified. I see that happen all the time. The goal is not just a free quote. The goal is a quote you can afford to keep.

A lower premium usually comes from better choices, not from stripping the policy down until it fails you in a claim.

Florida premiums run high for a reason. Repair costs are up, claim severity is up, weather losses affect the whole market, and rates can vary a lot from one insurer to the next for the same driver profile. That spread is where smart shopping helps.

If you want more Florida-specific ways to cut costs without gutting coverage, this guide to cheap car insurance in Florida is a useful next read.

The moves that usually help

Some savings strategies work consistently.

- Shop the same coverage across multiple quotes: Real savings come from price differences for the same protection, not from lowering coverage by accident.

- Raise deductibles only to a level you can pay: A higher deductible often lowers premium, but it only makes sense if you could handle that amount tomorrow after a crash or storm loss.

- Ask for every discount you legitimately qualify for: Multi-policy, paid-in-full, paperless, prior insurance, good driving history, vehicle safety features, and homeownership can all affect price.

- Review unused coverage on older vehicles: Collision and other physical damage coverage may be worth revisiting if the car has low value, but only if you could replace it yourself without creating a bigger problem.

- Keep your record and insurance history as clean as possible: Lapses, late payments, tickets, and preventable claims can all make Florida quotes more expensive.

One practical point gets missed a lot. Small monthly savings can create a big out-of-pocket problem later. Saving $18 a month does not help much if it leaves you with a deductible or coverage gap you cannot absorb.

What usually backfires

A few habits make policies look cheaper without making them better.

First, chasing the lowest monthly payment often leads to deductibles that are too high or liability limits that are too low.

Second, buying only the state minimum can leave a Florida driver badly exposed after one serious accident. Legal minimum coverage and adequate coverage are two different things.

Third, changing several parts of the quote at once makes it hard to tell what saved money. Change one variable at a time. Then compare the result.

The simple approach is the one that works. Decide what protection you need, keep that structure steady, and then look for the best price on that exact setup. That is how you get a policy that is both affordable and real.

Comparing Quotes Apples to Apples Not Estimates to Promises

A Florida driver gets two "free quotes" for the same car on the same day. One is far cheaper. Later, after the carrier verifies the drivers, address, prior insurance, and vehicle details, the price jumps. That is a common problem in this market.

Cheap-looking quotes often win attention for the wrong reason. They were built on different assumptions, missing information, or lighter coverage. The only useful comparison is one where the details match line by line.

Estimated quote versus accurate quote

A quick online estimate has value. It gives you a ballpark. It does not guarantee the price you can buy.

An accurate quote usually needs the full driver list, correct garaging address, vehicle VIN, prior insurance history, and the exact coverages requested. In Florida, small mistakes on any of those items can change the premium fast. That is why "free quotes" can create confusion. Some are just rough pricing screens, while others are close to bindable.

Use this simple filter:

- Estimate: Fast pricing based on limited inputs

- Accurate quote: Pricing built from verified, complete details

- Bound price: Final premium after underwriting review

If a quote was built without full information, treat it as a starting number, not a promise.

What to match before you compare price

Put the quotes side by side and check the setup first. Price comes second.

Drivers on the policy

Make sure every quote includes the same household drivers.Vehicle information

Check the VIN, trim, usage, and garaging ZIP code.Liability limits

One quote with lower limits will almost always look cheaper.Deductibles

Verify 'other than collision' and collision deductibles match.Optional coverages

Compare uninsured motorist, medical payments, rental reimbursement, roadside assistance, and physical damage coverage the same way across every quote.Discount assumptions

Confirm whether each quote assumes paperless, autopay, prior insurance, or homeowner status.Policy restrictions

Look for exclusions, endorsements, named driver limitations, or coverage conditions that narrow what the policy does.

This is the part many shoppers skip. It costs them.

A quote is only "better" if the coverage structure is the same and the price still holds up after review. If you want a cleaner side-by-side process, a Florida car insurance quote review through Select Insurance Group can help you compare real options instead of chasing numbers that change later.

How Select Insurance Group Makes It Simple

You fill out one quote form, get a low number, and then the details start shifting. A driver was left off. The coverage is thinner than expected. The company writing the quote is fine with one ZIP code and tough on another. That is a common Florida problem.

An independent agency helps by doing the sorting work up front. Instead of sending you carrier by carrier to repeat the same information, the agency can check multiple markets while keeping your quote request consistent. In Florida, that matters because rates can change fast based on where you live, what you drive, your prior insurance, and how each carrier views risk in your area.

The primary benefit is accuracy, not just speed.

Select Insurance Group helps shoppers compare real options without turning "free quotes" into a guessing game. The agency reviews the details that often cause problems later, flags gaps, and shows where a cheaper policy is cheaper for a reason. That is how you avoid comparing a solid policy to a stripped-down one and calling it a deal.

If you want a simpler way to shop, start with a Florida insurance quote request through Select Insurance Group. You can see options from multiple carriers, ask direct questions, and get help matching coverage to your budget before you bind anything.

That saves time. It also helps you avoid one of the biggest mistakes I see in Florida. Buying the lowest number first, then finding out too late it was never the same policy.

Florida Insurance FAQs Your Questions Answered

Is there a Florida low-income government car insurance program

No. Florida does not offer a government-run low-income car insurance program.

That trips people up. Shoppers call expecting a state discount, a public option, or a special low-cost plan they can apply for. In Florida, those programs do not exist. The practical option is to compare private-market quotes carefully and decide what coverage you can afford without assuming outside help is coming.

If your budget is tight, ask for two versions of the quote. One at the lowest coverage you are willing to accept, and one with better protection so you can see the price gap clearly.

Is a free quote the final price

Usually, no.

A free quote is often a starting number based on the information entered. The price can change after the carrier checks driving history, prior coverage, household drivers, garaging address, and the VIN. In Florida, small details can move the premium more than people expect.

Ask this before you buy: “Is this price based on verified information, or is it still an estimate?” That one question saves a lot of frustration.

Should I buy only the state minimum to save money

Sometimes that is the only payment that fits the budget. If that is the case, make the choice on purpose.

Minimum coverage gets you legal, but it does not give much room for a serious claim. If you hit a newer car, cause injuries, or get into a mess with an uninsured or underinsured driver, low limits can leave you paying out of pocket. I tell Florida drivers to at least price the next step up before deciding. The increase is sometimes smaller than expected, and the difference in protection is real.

If you want a cleaner way to shop, Select Insurance Group, Inc. can help you compare free Florida insurance quotes with the coverage details lined up clearly, so you can see what you're buying before you commit.