You're probably here because insurance in North Carolina feels less straightforward than it should. Maybe you just bought a house and learned flood coverage is separate. Maybe you're insuring a work truck and someone mentioned a trucking endorsement. Maybe you only wanted a quick auto quote and ended up sorting through deductibles, exclusions, and state rules that don't sound simple at all.

That confusion is normal. North Carolina has a big, active insurance market, but it also has some state-specific wrinkles that catch people off guard. Coastal property issues, market-of-last-resort plans, commercial vehicle rules, and the need for clear bilingual guidance all matter more here than many people expect. A good local agency should make that easier, not more confusing.

Table of Contents

- Navigating the North Carolina Insurance Landscape

- What an Independent Insurance Agency Does for You

- Protecting Your Family and Assets with Personal Insurance

- Safeguarding Your Business with Commercial Coverage

- Understanding Unique North Carolina Insurance Rules

- How to Choose the Right NC Insurance Agency

- Your North Carolina Insurance Questions Answered

Navigating the North Carolina Insurance Landscape

A couple buys a home near Wilmington, closes on Friday, and calls Monday asking for the same homeowners setup they had in another state. Then key questions start. Is flood insurance separate? How is wind handled? Are there coastal limits, deductibles, or exclusions that change the numbers?

That is a common North Carolina insurance problem. The policy names may sound familiar, but the rules, exposures, and pricing pressure can shift fast from the coast to the Piedmont to a rural county with more driving miles and fewer carrier options.

The state also has a busy insurance market, which gives buyers plenty of agencies to choose from. Choice helps, but it also creates noise. A low quote can look fine until someone reviews how the property is built, how a truck is used for work, or whether the household needs a bilingual agent who can explain coverage clearly before a claim happens. If you want a simple explanation of how local agencies compare options across carriers, this guide on what an independent insurance agency does is a helpful starting point.

Where North Carolinians usually get stuck

The first mistake is usually buying for the price on the screen instead of the risk in real life.

- Homeowners focus on the base premium: Then they learn that flood is usually separate, coastal property questions can change eligibility, and the cheapest option may leave a serious gap after a storm.

- Drivers ask for state minimum limits only: Then an accident exposes how little protection those limits provide, especially if there are prior violations, youthful drivers, or a work-use vehicle in the household.

- Business owners insure a vehicle but miss the operation behind it: A pickup used for a trade, a box truck making deliveries, or a larger trucking account can trigger different underwriting questions and different coverage needs.

- Spanish-speaking families accept unclear explanations: That creates avoidable problems. If no one explains deductibles, exclusions, and claim steps in plain language, the policy may be in force but the customer is still left guessing.

The right policy starts with the right questions. If an agency does not ask how you use the home, car, or truck, the quote may not fit the risk.

Why local guidance matters

North Carolina has its own insurance rules, coastal property concerns, and business-use details that do not show up well on a generic quote form. That matters for families buying near the water, contractors with heavier vehicles, and trucking operations that need to match state and federal requirements.

There are real trade-offs. Paying less up front can mean a higher wind deductible, a missing flood policy, or liability limits that run out too fast after a serious claim. Paying more is not automatically better either. The goal is to choose coverage that matches how you live and work in North Carolina.

Good local advice also means catching the issues many national call centers miss. Coastal flood exposure, trucking classifications, and bilingual service are not side topics here. They are often the difference between a policy that merely exists and one that does its job when something goes wrong.

What an Independent Insurance Agency Does for You

A Jacksonville family closes on a home, adds a teenage driver, and keeps a work truck for weekend jobs. On paper, those look like separate policies. In real life, one change affects the others, and a cheap quote can turn into an expensive gap if nobody connects the dots.

An independent agency handles that job. Instead of offering one carrier's version of the answer, the agency checks multiple options, explains the trade-offs, and helps match coverage to the way you live or work in North Carolina.

What independence changes for the customer

The biggest benefit is judgment.

A good independent agent is not just collecting prices from different carriers. Their value is knowing why one option fits better than another. One company may be more workable for a coastal property. Another may handle a driver with violations more reasonably. Another may be a better fit for a contractor, a box truck, or a small trucking account that needs closer attention to classifications and filings.

That matters in North Carolina because the details are rarely generic. Coastal exposure, flood gaps, business-use vehicles, and the need for bilingual explanations can all change what a policy should look like. Large call centers often miss those issues because the quote process is built for speed, not local accuracy.

If you want a clearer explanation of how that model works, this guide on what an independent insurance agency is gives a useful overview.

What a good independent agent actually does

A strong agency reviews the risk before it shops the policy. That sounds simple, but it is where many insurance problems start or get prevented.

A solid review usually includes:

- How the property or vehicle is used. Personal use, rental activity, deliveries, contractor work, and long-haul driving all raise different underwriting questions.

- Where the risk sits. A home inland is different from a home with coastal wind concerns or flood exposure.

- Who needs to be protected. Household drivers, employees, family members, and business owners can all affect liability planning.

- What would hurt most in a claim. Low premiums look good until a wind deductible, excluded water loss, or thin liability limit creates a much bigger bill later.

- What happens after the sale. Endorsements, certificates, policy changes, renewals, and claim support are part of the job.

Good advice is specific. If an agent can explain the monthly premium but cannot explain the exclusions, deductible structure, or claim process in plain English, the customer still does not have a clear recommendation.

That is also where bilingual service matters. Spanish-speaking households and business owners should be able to ask detailed questions and get direct answers, not a rushed summary. Insurance only works well when the buyer understands what is covered, what is excluded, and what to do when something goes wrong.

Where independent agencies earn their keep

The strongest agencies save people from bad fits.

That may mean spotting that a personal auto policy does not match delivery use. It may mean warning a coastal homeowner that standard homeowners insurance does not solve every water risk. It may mean helping a business owner line up commercial auto, general liability, and property coverage so each policy supports the others instead of leaving holes between them.

One example in this space is Select Insurance Group, Inc., which operates as an independent agency and compares quotes across multiple carriers for personal and commercial insurance. That structure can be especially helpful for North Carolinians whose risks do not fit neatly into a standard profile.

The wrong approach is buying each policy in isolation and hoping everything works together later. An experienced North Carolina agency checks the full picture up front, explains the trade-offs clearly, and helps prevent surprises that only show up at claim time.

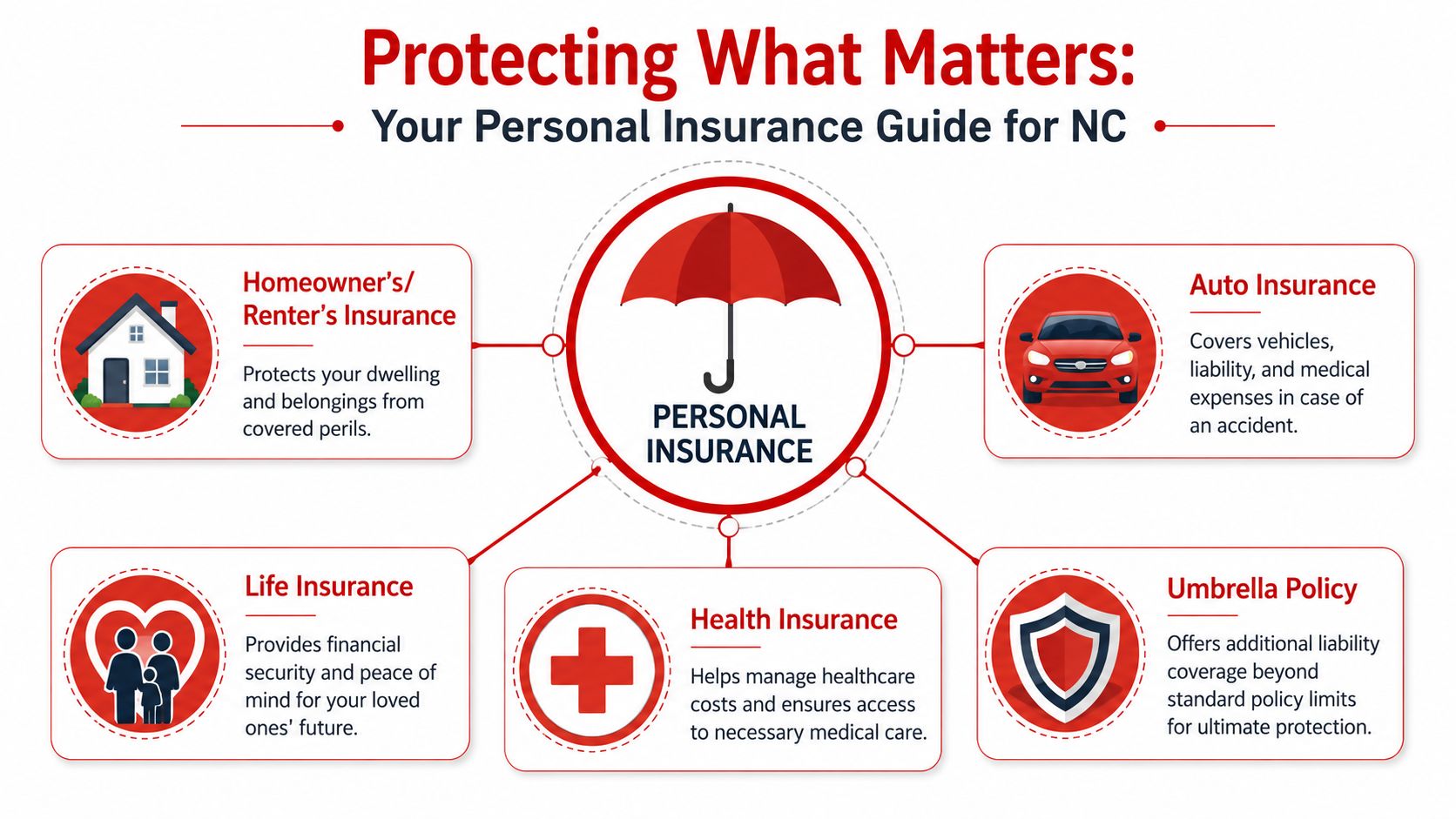

Protecting Your Family and Assets with Personal Insurance

Personal insurance should protect your life as it's lived in North Carolina. That means your car, your home, your belongings, your liability exposure, and the gaps many people don't see until an agent points them out.

The biggest mistake is treating each policy as separate paperwork. In real life, they overlap. A home purchase can change your auto needs. A teen driver can change liability planning. A property near the coast or in a flood-prone area can change the entire insurance strategy.

Auto coverage that matches how you drive

Auto insurance isn't just about carrying a card in the glove box. The important question is whether the policy fits the driver and the vehicle.

If you need an SR-22 filing, have a less-than-clean driving record, or use a vehicle differently than a standard commute, you need an agency that asks detailed questions. The wrong quote can look fine until a filing issue, excluded use, or liability limit problem surfaces later.

A practical auto review should include:

- Driver profile: Tickets, accidents, licensing status, and any filing needs.

- Vehicle use: Personal driving, business use, deliveries, or heavier-duty operation.

- Protection level: Whether your limits and deductibles make sense for your budget and assets.

Homeowners and renters coverage in a coastal state

North Carolina's property market has its own character. The state ranks 8th nationally in federal flood premium and 9th in homeowners multiple peril premium, according to the NAIC North Carolina market trends report. Those rankings tell you something simple: property risk here isn't theoretical.

The state also has specialized risk pools. The NCIUA, often called the Beach Plan, serves coastal property situations, and the NCJUA, often called the FAIR Plan, exists for other high-risk properties that may have trouble finding standard market placement.

What those property options mean in practice

Not every homeowner needs one of those plans. But many homeowners should at least understand why they exist.

| Situation | What to ask an agency |

|---|---|

| Coastal or near-coastal home | Do I need separate wind consideration or a specialty placement review? |

| Property declined by standard market | Is the FAIR Plan or another alternative relevant here? |

| Renters who assume the landlord covers everything | What protects my belongings and my liability if there's a loss? |

A standard homeowners conversation in North Carolina should include storm exposure, flood separation, and whether the property fits the standard market at all.

Umbrella, motorcycle, RV, and the overlooked layers

Some of the most valuable policies are the ones people buy only after a close call.

- Umbrella coverage: Useful when you want extra liability protection above underlying personal policies.

- Motorcycle and RV policies: Important because these vehicles often need coverage built around seasonal use, storage, and different liability concerns.

- Life and health planning conversations: Even when purchased separately, they belong in the same household risk review.

Good personal insurance doesn't just check a requirement. It protects the assets you've built and the income your family depends on.

Safeguarding Your Business with Commercial Coverage

Business insurance gets complicated when owners assume a general policy covers everything. It doesn't. General liability, commercial property, workers' compensation, commercial auto, and trucking-related coverage all solve different problems. If they're blended carelessly, gaps show up fast.

That's especially true in North Carolina for businesses with vehicles. Contractors, farm operations, and small fleets often start with “commercial auto” and stop there. In many cases, that's where trouble begins.

Commercial auto and trucking are not the same thing

A heavier vehicle or a business that hauls for work may need more than a standard commercial auto setup. This is one of the most overlooked issues I see in practice. Owners know the truck is insured, but they haven't confirmed that the operation is insured correctly.

Many agencies still don't explain that 2025 DOT regulations require separate trucking endorsements for vehicles over 10,000 lbs, and that change caused 34% of small operators to be underinsured. The same source also notes the importance of bilingual specialists for North Carolina's 1.8 million Spanish-speaking residents trying to understand these rules, as outlined by Select Insurance Group's North Carolina commercial auto guidance.

Where businesses make expensive mistakes

The pattern is usually the same. A business owner asks for “coverage on the truck,” gives the VIN, and assumes the rest is handled. But underwriting cares about use, weight, radius, cargo, drivers, ownership structure, and whether the vehicle falls into a trucking exposure.

Here's where specialized advice pays off:

- Construction fleets: A pickup towing equipment is different from a vehicle performing regulated hauling.

- Farm vehicles: Rural operators often move between personal, farm, and commercial use without realizing the policy distinction matters.

- Growing businesses: A company that started with one truck may now have employees driving, jobs crossing county lines, or heavier vehicles than it had last year.

If your business vehicle earns money in a way that's more complex than a simple service call, ask whether the policy should be reviewed as trucking, not just commercial auto.

Bilingual service is part of accuracy

Bilingual support isn't just a convenience. It helps prevent misunderstandings in applications, endorsements, and claims reporting. For Spanish-speaking owners, especially in rural areas, clear explanation matters when the business depends on getting classification details right.

A strong commercial review should cover these categories:

- General liability: Protection when your work causes injury or property damage to others.

- Commercial property: Coverage for buildings, equipment, inventory, and business personal property, depending on the policy.

- Workers' compensation: Important when you have employees and need the right structure for workplace injury exposure.

- Vehicle-specific protection: Commercial auto, hired and non-owned considerations, and trucking endorsements where required.

Cheap commercial insurance is often just incomplete commercial insurance. For many North Carolina businesses, especially those with trucks, the smarter move is slower, more detailed underwriting up front.

Understanding Unique North Carolina Insurance Rules

North Carolina insurance gets tricky where common assumptions meet state realities. The biggest example is flood coverage. Many homeowners still assume flood is part of a standard homeowners policy. It usually isn't.

That misunderstanding matters because flood risk in this state doesn't stay neatly inside the lines people expect.

Flood risk is broader than many owners think

North Carolina's insurance market features both coastal exposure and inland flood concerns. The state uses specialized property pools for hard-to-place risks, and flood insurance often requires a separate decision rather than an automatic assumption.

An underserved issue in the state is the gap between bundle marketing and real flood cost. North Carolina's flood-prone areas include 1.2 million properties, and many owners don't realize separate flood coverage may be needed. The same state-level reporting notes that 68% of flood claims in North Carolina were for properties outside federal high-risk zones, according to the NC DOI 2025 Flood Report as described in the verified data provided. That's why agencies should discuss flood even when a property owner says, “I'm not in a flood zone.”

Why independent shopping matters on flood options

Another overlooked point is that some policies and riders may offer alternatives beyond the default path many consumers first see. In practice, the job of the agent is to explain where standard coverage stops, where separate flood coverage starts, and whether excess flood options should be reviewed.

That's also where plain-language advice matters more than marketing. “Bundle and save” sounds helpful until a client learns the water loss they feared most was never included in the homeowners form.

Ask one direct question: “Show me what water losses are excluded, and show me what policy would cover them.”

Consumer protection and licensing standards

North Carolina also regulates agency conduct in a way that consumers should take seriously. Agency representatives must hold active licenses and comply with consumer-protection, ethics, and data-security requirements. The state's Unfair Trade Practices Act prohibits misrepresentation, fraud, and deceptive marketing, as summarized by IIANC technical guidance on North Carolina insurance compliance.

That matters for a simple reason. A licensed agency isn't just selling insurance. It's operating under rules that require transparent quotes, proper handling of client information, and ethical representations of coverage.

If you want a plain-English overview of vehicle-related legal basics, this guide to North Carolina car insurance laws is a useful starting point.

A better way to think about North Carolina rules

Don't think in terms of “required” versus “optional” only. Think in terms of “what loss would hurt me, and which policy responds?”

That mindset helps with flood, high-risk property placement, filing issues for drivers, and business vehicle classification. North Carolina's rules aren't impossible to work through. They just punish assumptions.

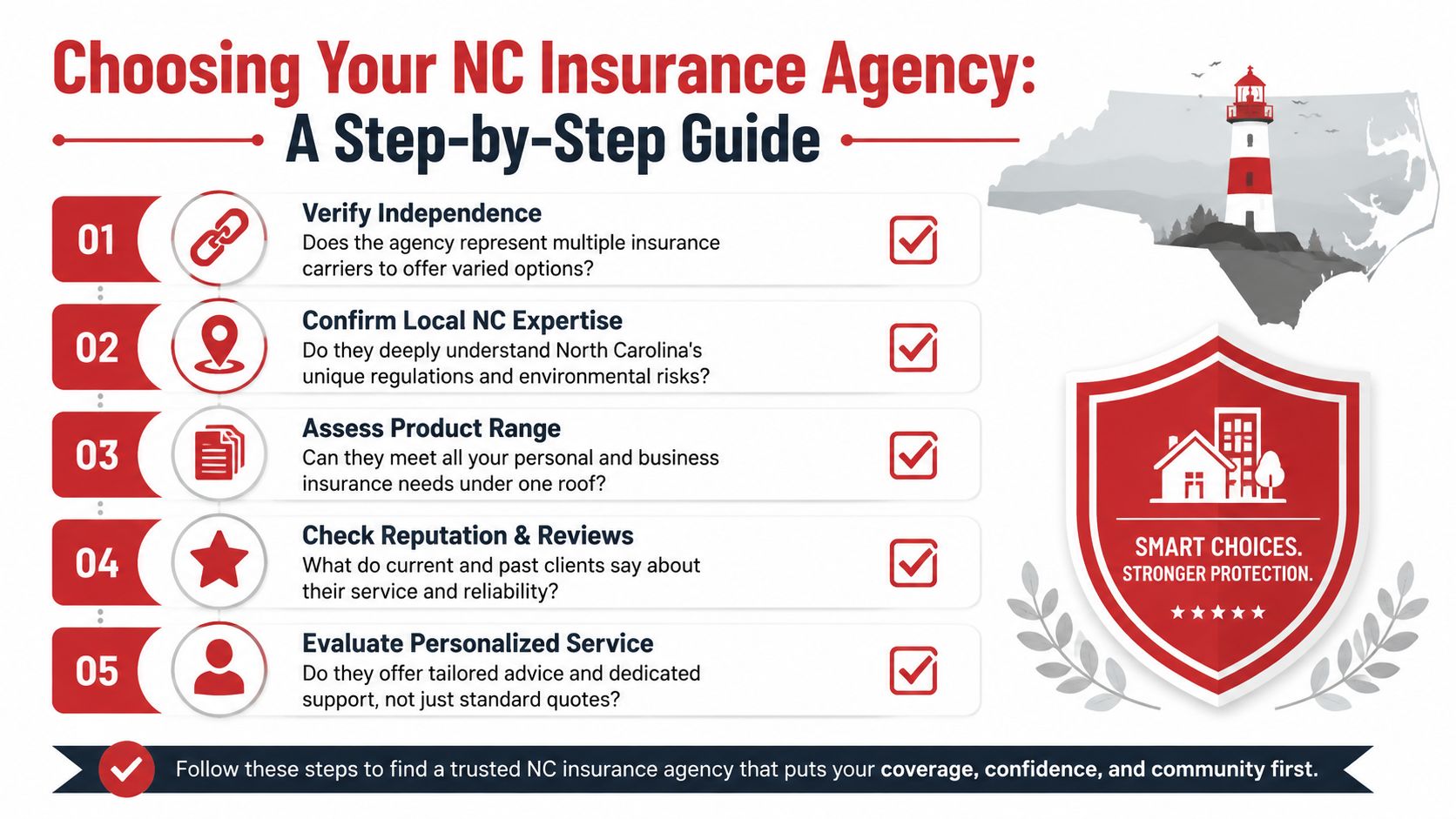

How to Choose the Right NC Insurance Agency

Choosing an insurance agency in North Carolina should feel more like hiring an advisor than grabbing the cheapest quote. Price matters, but if the agency misses a classification issue, an exclusion, or a state-specific gap, the savings can disappear fast.

The cleanest way to choose is to use a short checklist and stay disciplined.

A practical checklist

- Confirm independence: Ask whether the agency compares multiple carriers or only offers one company's products.

- Check North Carolina familiarity: Ask how they handle coastal property issues, flood questions, SR-22 situations, or commercial vehicle classification.

- Look for bilingual support: If anyone in your household or business is more comfortable in Spanish, make sure explanation won't get lost in translation.

- Test responsiveness early: Call, text, or email with one real question and see how clearly they answer.

- Compare coverage, not just premium: Put deductibles, exclusions, endorsements, and liability limits side by side.

What to bring before asking for quotes

A faster quote process starts with better information. For most personal lines, gather driver details, VINs, current declarations pages, property address, prior claims history, and any loan or lien information. For business insurance, add payroll context, vehicle schedules, employee driver details, and a clear description of operations.

A well-run agency should also have reliable call handling, because missed calls often mean missed service opportunities. If you're evaluating operations on the agency side, resources like SkipCalls AI receptionist for agencies are worth reviewing because they address a real problem in this business: clients usually call when they need help now, not later.

Checklist insight: A good agency answers the hard question directly. If you get vague answers before you buy, expect the same after a claim.

How to compare offers intelligently

Don't ask, “Which one is cheapest?” Ask:

- What does this policy leave out?

- Are the deductibles realistic for my budget?

- Does this quote assume anything that isn't true about my property, driving, or business?

- Who will help me make changes or report a claim?

That approach usually leads to a better decision than chasing the lowest number on page one.

Your North Carolina Insurance Questions Answered

Is minimum coverage enough?

Sometimes it satisfies a legal requirement. That doesn't mean it protects your savings, income, or property well. Minimum-focused shopping often works poorly for households with assets to protect or for drivers with any complexity in their record.

Can a high-risk driver still get coverage?

Usually, yes. The key is being upfront about the driving history and any filing needs so the quote reflects the actual situation from the start.

Why is homeowners insurance so confusing here?

Because North Carolina property insurance can involve coastal issues, separate flood decisions, and placement questions for higher-risk properties. Homeowners often think they're comparing one policy to another when they're really comparing very different coverage structures.

What if insurance problems connect to credit trouble?

That won't apply to everyone, but for some households, financial cleanup and insurance planning go hand in hand. If someone also needs outside help sorting credit issues in another state, a resource like help with collections Birmingham AL can be relevant in the broader financial recovery process.

What's the main benefit of working with an independent agent?

Clarity. A good independent agent helps you compare options, catch gaps, and match the policy to how you live or work in North Carolina. That's especially useful when the issue involves flood, high-risk property placement, business vehicles, or bilingual communication.

If you want help sorting through your options, Select Insurance Group, Inc. can help you compare coverage for your home, auto, renters, commercial auto, or business insurance needs in North Carolina. Reach out for a free, no-obligation quote and a plain-language review of what fits, what doesn't, and what may be missing. Insurance done right, right now.