Florida holds about 35% of all National Flood Insurance Program policies in the country, yet only 13% of Florida households carry flood insurance, leaving 8 out of 10 households unprotected from flood damage, according to the Wharton issue brief on Florida's flood market. That gap tells you something important. A lot of homeowners in this state know flood is a real risk, but many still assume their own house is the exception.

That assumption gets expensive fast in Florida. Rain backs up. Streets overflow. Lakes rise. Canals spill over. Storm surge isn't the only threat, and standard homeowners insurance doesn't cover flood damage from rising water.

If you're shopping for flood insurance in Florida, the challenge isn't just finding a policy. It's figuring out what risk you carry, when coverage is required, how long it takes to start, and whether the federal option or a private policy fits your home better.

Table of Contents

- Florida's Flood Reality Why Standard Home Insurance Is Not Enough

- NFIP vs Private Flood Insurance A Head-to-Head Comparison

- Are You in a Flood Zone? Understanding Florida's Maps and Requirements

- How Much Is Flood Insurance in Florida? Costs and Savings Explained

- What Does Flood Insurance Cover? A Practical Checklist

- Getting Covered How to Get Your Florida Flood Insurance Policy

- Florida Flood Insurance Frequently Asked Questions

Florida's Flood Reality Why Standard Home Insurance Is Not Enough

Flooding is one of the costliest disaster threats Florida homeowners face, yet many families still assume their home policy covers it until a claim proves otherwise.

That mistake gets expensive fast. A standard homeowners policy usually covers certain sudden water losses that start inside the home, such as a burst pipe, depending on the cause. It generally does not cover floodwater that rises from outside and enters the house after heavy rain, storm surge, overflowing canals, saturated ground, or street flooding.

That distinction sounds technical. It is not. It is the difference between a covered water loss and paying for repairs out of pocket.

I see another misunderstanding all the time in Florida. Owners hear they are in Zone X and take that to mean no flood risk. In practice, Zone X usually means flood insurance is not required by the lender, not that flooding cannot happen. Inland rain events, drainage backups, and neighborhood runoff do not care what label appears on a map.

A separate flood policy fills that gap. It matters on the coast, but it also matters well away from the beach.

Practical rule: If water comes from outside and rises into the home from the ground level, do not assume your homeowners policy will pay.

Timing matters too, especially during hurricane season. Flood coverage does not always start the day you buy it. Many homeowners wait until a storm is on the radar or the streets have already started to pond. By then, the waiting period can leave them uninsured for the event they were trying to protect against.

The money question homeowners should ask earlier is simple. If one or two feet of water got into the house, could you absorb the cost of demolition, drying, flooring, cabinets, and replacement of damaged belongings without a flood policy?

Flood insurance should be part of the same review as wind coverage, roof condition, deductibles, and reserves. If you are sorting out how it fits with your broader property protection, it helps to compare it alongside Florida home insurance options, because each policy is built for a different kind of loss.

Insurance is only part of the job. Physical upgrades can also reduce storm damage and repair costs, and Ofir Engineering for hurricane protection is a useful resource if you are looking at the construction side of protecting a Florida home.

NFIP vs Private Flood Insurance A Head-to-Head Comparison

Florida homeowners usually have two paths for flood coverage. The federal NFIP policy or a private flood policy. The better choice depends on the house, the loan, the budget, and how much coverage the owner needs after a real water loss.

A simple way to frame it is this. NFIP works like a standard off-the-shelf policy. Private flood can offer more room to tailor limits and terms, but the details matter.

How the two options differ

| Feature | NFIP | Private flood insurance |

|---|---|---|

| Dwelling limit | Standard federal cap of $250,000 | Often offers higher limits |

| Contents limit | Standard federal cap of $100,000 | Often offers more flexibility |

| Waiting period | Standard 30-day waiting period in many cases | Some carriers offer shorter waits |

| Availability in Florida | Broadly available through the federal program | Availability depends on the property and carrier appetite |

| Policy design | Standardized forms and limits | More variation by carrier |

NFIP's biggest advantage is consistency. Agents, lenders, and closing teams know what it is, and homeowners with modest coverage needs often find it easier to fit into the federal structure.

Private flood insurance is often worth a hard look for higher-value homes, homes with rebuilding costs above the NFIP cap, or owners who want to compare whether the market prices their address more favorably. This is especially true in Florida, where two houses on the same street can present very different flood characteristics. If you want a closer breakdown, this comparison of private flood insurance vs NFIP in Florida explains where each option tends to fit.

Waiting periods also deserve more attention than they usually get. A policy is not always active the day you pay for it. NFIP commonly has a 30-day wait, and private carriers may have different rules. During hurricane season, that timing can decide whether you have protection for the next storm or are still on the sidelines when water gets in.

Which type of policy usually fits which homeowner

For a lower-value home with a straightforward lender requirement, NFIP can be a practical answer. The limits are clear. The form is familiar. If the house would be adequately covered within those caps, simplicity has value.

A higher-value home needs a closer review. I see this issue regularly in Florida. Homeowners focus on the premium first, but the bigger question is whether the policy limit would rebuild the damaged part of the home and replace covered contents after a flood. If the numbers do not work, a lower premium is not much comfort.

Private coverage can also help when the owner wants broader options in how the policy is structured. That does not mean private is always cheaper or always broader. It means the comparison should be done line by line, with attention to limits, waiting periods, lender acceptance, and how the claim would play out after a loss.

A flood policy should match the property and the financial risk. The cheapest quote and the safest choice are not always the same thing.

Use this practical filter:

- NFIP may fit well when the home falls comfortably within federal limits and the goal is a familiar policy structure.

- Private flood may fit better when rebuilding costs are higher, the owner wants different coverage options, or the quote compares favorably for that address.

- Both should be quoted when possible because Florida flood risk is not uniform, and pricing can vary for the same homeowner.

One last point. If there is a mortgage, lender acceptance is part of the decision. A policy can look good on paper and still create problems if it does not meet the lender's requirements for form, limits, or documentation.

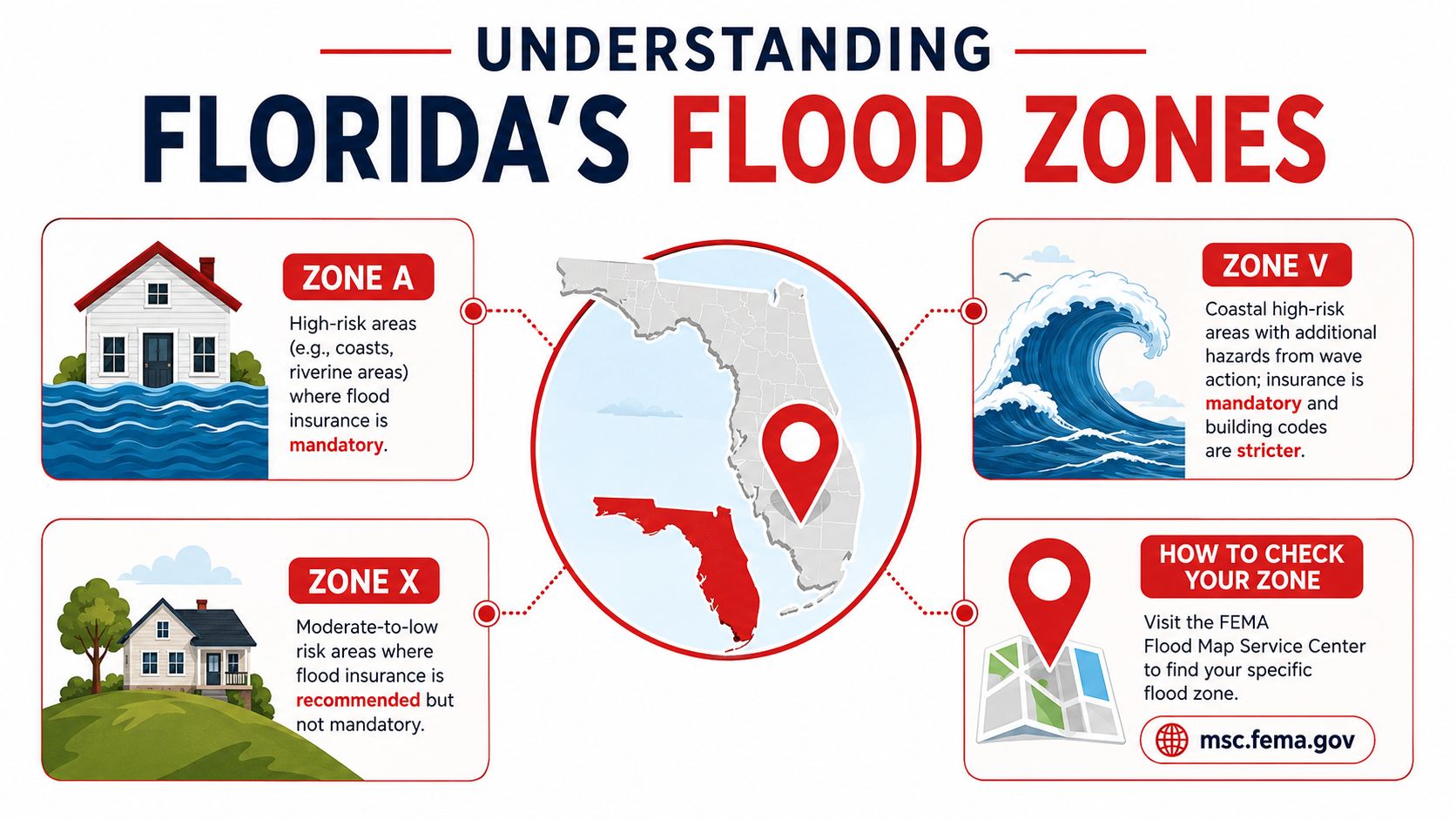

Are You in a Flood Zone? Understanding Florida's Maps and Requirements

Many homeowners hear one flood zone label and stop there. That's where trouble starts. Your zone tells part of the story. It doesn't tell the whole story, and it definitely doesn't tell you whether you're “safe.”

What the main flood zones mean

In plain terms, Zone A and Zone V are the labels homeowners hear most often when talking about higher-risk flood areas. These zones matter because they often trigger lender requirements when there's a mortgage involved.

Zone X is where confusion takes over. Homeowners often hear “not required” and translate that into “no risk.” That isn't the same thing. “Not required” only answers one question: whether a lender is forcing the purchase.

If you want a plain-language breakdown of lender rules and zone-related requirements, this overview of when flood insurance is required in Florida is helpful.

When flood insurance is required

There are two major situations Florida homeowners need to watch closely.

- Federally backed or regulated mortgage in a high-risk zone: Flood insurance is required for mortgaged properties in high-risk zones such as A and V, according to the Florida Citizens flood requirement summary.

- Certain Citizens policyholders: That same source states that, under Florida Statute 627.715, Citizens policyholders with homes valued at $400,000 or more must obtain flood insurance by Jan. 1, 2026, regardless of flood zone.

- Lender-specific compliance: Some homeowners also need to meet a specific minimum amount of coverage tied to the loan and property, even after they've confirmed flood insurance is required.

That last point catches people off guard. Buying any flood policy isn't enough if the limit doesn't satisfy the mortgage requirement.

Important distinction: A flood zone is a mapping tool. An insurance requirement is a legal or lending rule. Those aren't the same thing.

Zone X deserves special attention even when no one is forcing the purchase. In practice, moderate-to-lower risk doesn't mean impossible loss. Florida's weather patterns, drainage issues, and development patterns can create flood damage far from the shoreline.

If your address is in Zone X, the smart question isn't “Can I skip flood insurance?” It's “What risk am I comfortable keeping on myself?”

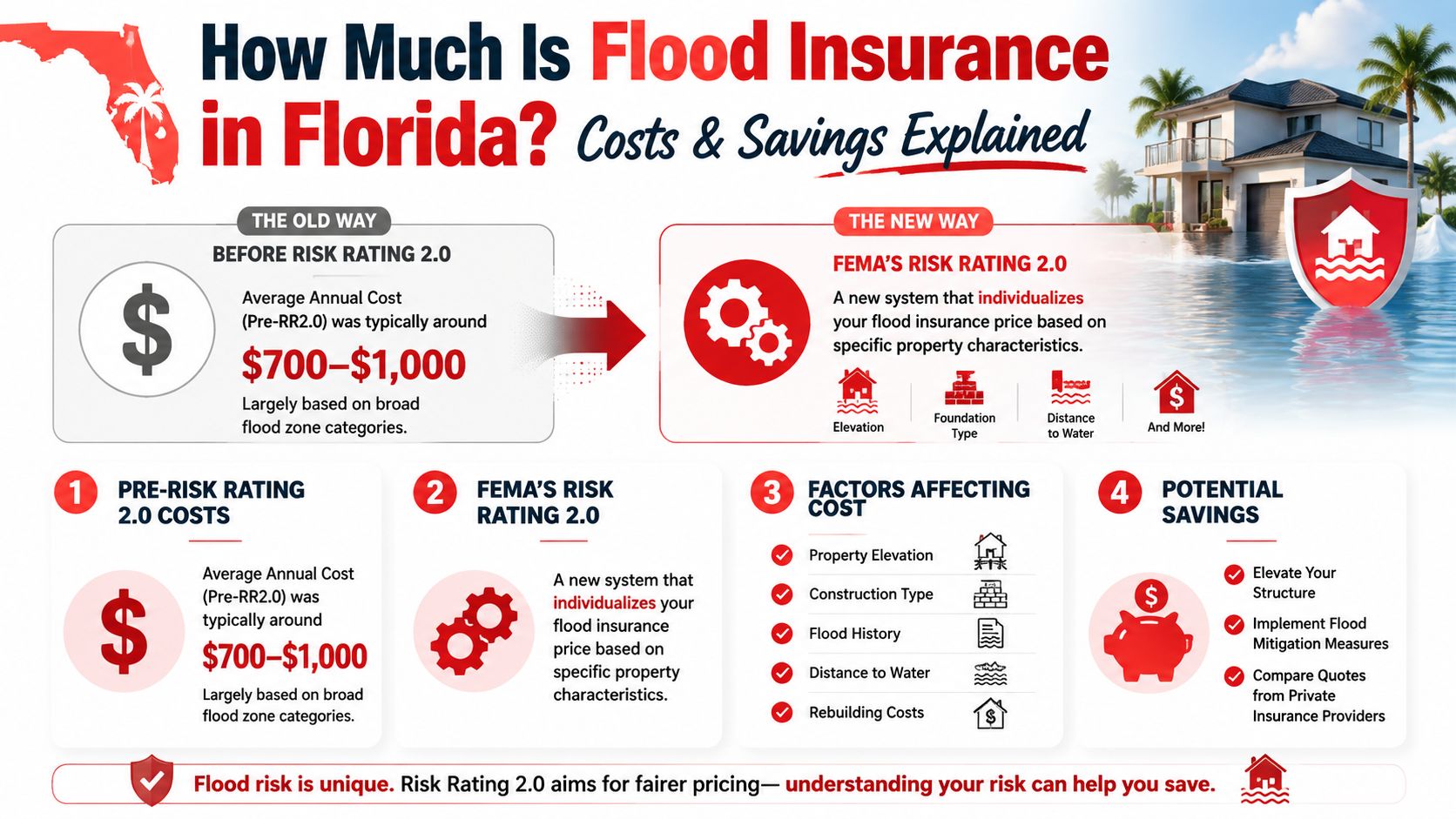

How Much Is Flood Insurance in Florida? Costs and Savings Explained

The price of flood insurance in Florida feels less predictable than it used to, and homeowners aren't imagining that. FEMA's newer pricing approach changed how many properties are evaluated.

Why rates are changing

A simple way to understand Risk Rating 2.0 is to think about the difference between pricing a whole neighborhood by a broad label and pricing one specific home by its own characteristics.

Under FEMA's newer model, Florida premiums can rise by up to 18% annually, and some areas may see much steeper long-term changes. The WUSF reporting on Risk Rating 2.0 in Florida notes that ZIP code 33469 in Palm Beach County could see an average premium increase of 342% over time as the new pricing is fully implemented.

That's why neighbors can compare notes and get completely different answers. The system now looks more closely at property-specific factors instead of leaning as heavily on broad map categories.

What usually helps lower the price

You can't negotiate flood risk away, but you can make the risk picture clearer and sometimes more favorable.

- Document the property well: An elevation certificate can help in some cases because it gives underwriters better information about the structure.

- Focus on mitigation: Features that reduce flood exposure or damage severity can matter. The details depend on the home and the insurer.

- Review rebuild assumptions: Replacement cost plays into pricing. If a policy is built on inaccurate home details, the quote may not reflect the property correctly.

- Compare policy structures: One carrier may value the risk differently than another, especially in the private market.

A homeowner usually gets the best result when they treat flood insurance like underwriting, not like a commodity. The details of the house matter.

The most common pricing mistake is shopping too late and too narrowly. Homeowners wait until a storm is on the map, pull one quote, and assume that's the market. By then, timing may work against them, and they may have no room to make improvements that could affect the premium.

Flood insurance in Florida rewards preparation. It doesn't reward panic buying.

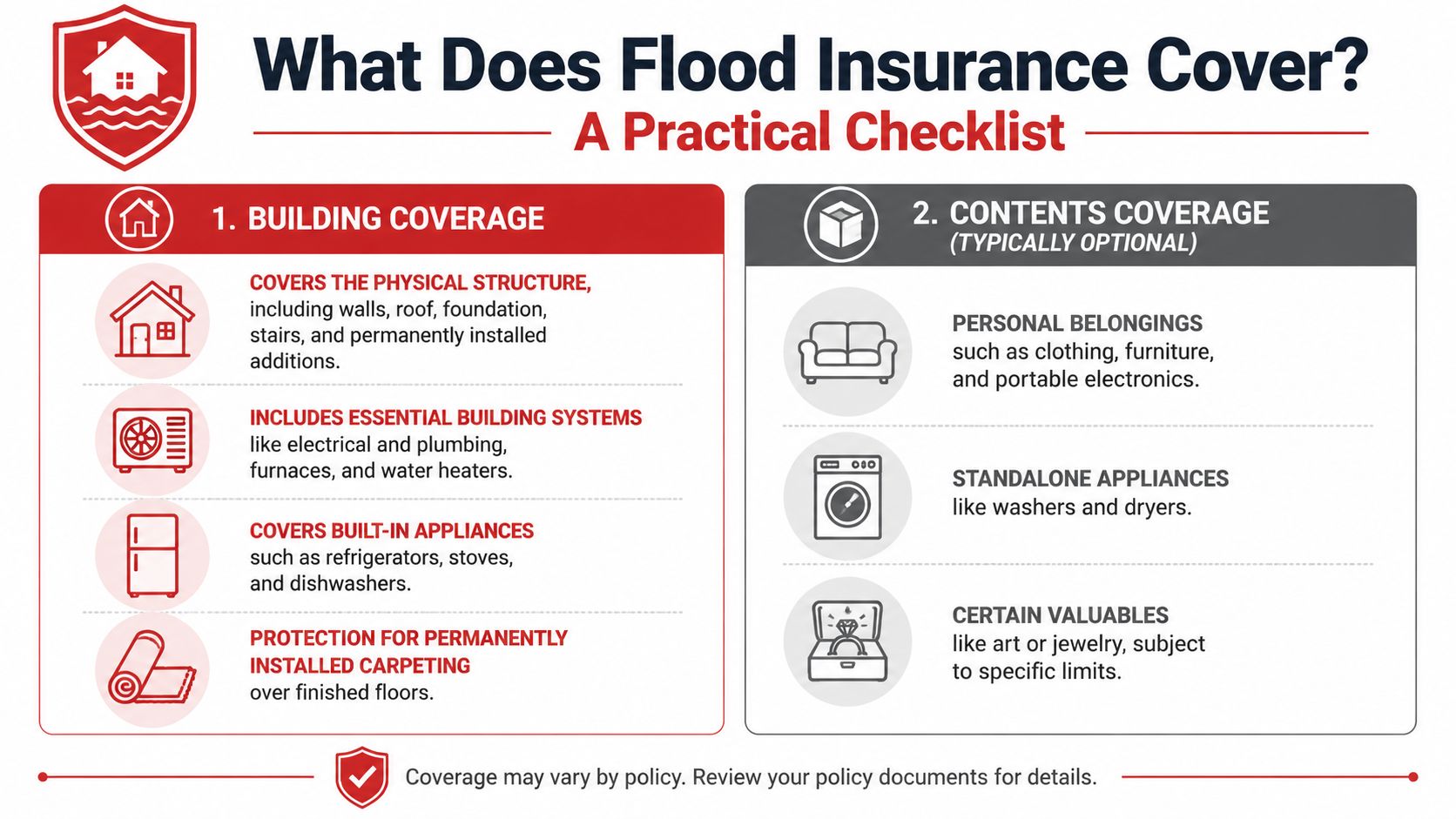

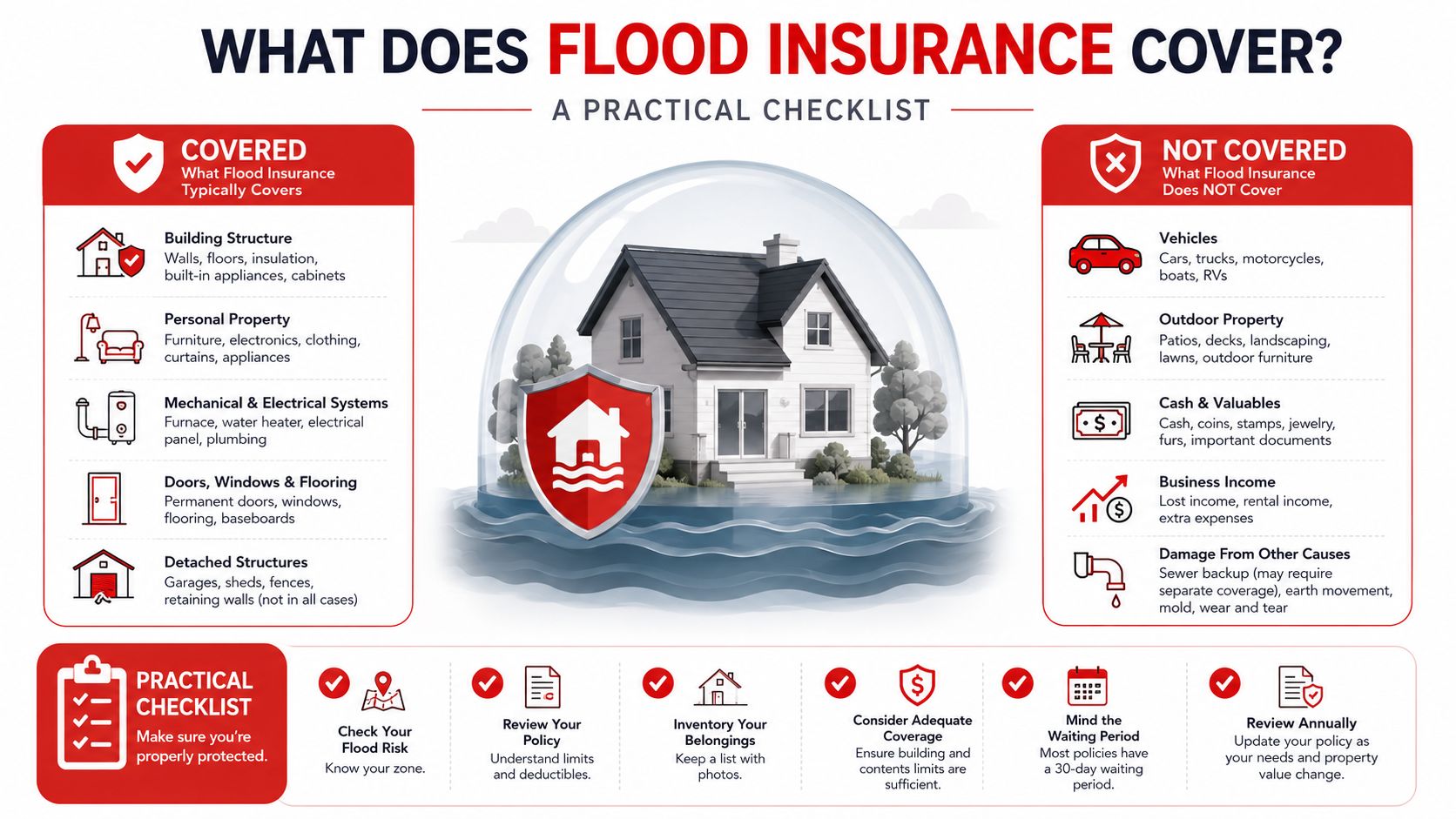

What Does Flood Insurance Cover? A Practical Checklist

Expectations need to be clear. Flood insurance is valuable because it covers a very specific type of loss. It's not a catch-all water policy, and it doesn't cover every flood-related expense a homeowner might face after a storm.

Building coverage

A flood policy commonly centers first on the structure itself. In practical terms, homeowners usually expect protection for the parts of the home that make the building function again after a covered flood loss.

Typical building-related protection often includes:

- The structure itself: Walls, foundation elements, stairs, and attached parts of the home.

- Core systems: Electrical, plumbing, furnaces, and water heaters.

- Built-in appliances: Items that stay with the home rather than move out with the owner.

- Permanently installed finishes: Certain installed flooring materials may fall into this category.

That's the part many people get right. They know they need the house protected. Where confusion starts is with everything around the house and everything inside it.

Contents coverage and common gaps

Contents coverage is usually a separate decision, not something to assume is built in automatically. If you want protection for belongings, ask specifically how the policy handles them.

A practical checklist for personal property usually includes:

- Furniture and clothing: These often fall under contents rather than building.

- Portable electronics: Coverage depends on the policy terms and category.

- Standalone appliances: Washers and dryers often belong in contents discussions.

- Valuables: Special limits may apply, so don't assume broad protection.

Common gaps matter just as much as covered items.

| Often misunderstood item | Typical issue |

|---|---|

| Additional living expenses | Often excluded under NFIP policies |

| Vehicles | Usually handled under auto coverage, not flood coverage on the home |

| Landscaping and outdoor property | Often limited or excluded |

| Basement improvements or nonessential lower-level items | Frequently more restricted than homeowners expect |

Read flood coverage with one question in mind: “If water fills this room, which items are insured as part of the building, which are contents, and which aren't covered at all?”

That question prevents a lot of claim frustration later.

Getting Covered How to Get Your Florida Flood Insurance Policy

Buying flood insurance in Florida is usually easier when you approach it in the right order. Most homeowners make this harder than it needs to be because they start with price instead of fit.

A practical way to shop for coverage

- Confirm your property details. Get the address, mortgage information, and any prior flood policy documents together first. If you have an elevation certificate, keep it handy.

- Decide what you're protecting. Some homeowners only need to satisfy a lender. Others want broader protection for the structure and belongings.

- Compare both pathways. Look at federal and private options when available. The policy form, limits, and waiting period all matter.

- Check lender acceptability before binding. A policy that doesn't meet loan requirements can create delays and forced revisions.

- Buy before storm headlines start driving decisions. Timing becomes critical.

Why timing matters more than most people think

The Florida Office of Insurance Regulation warns that policy activation timing can leave buyers exposed if they wait too long. According to the Florida flood insurance consumer guidance, most NFIP policies have a 30-day waiting period, while some private policies may have shorter waiting periods of 10 to 15 days.

That means a homeowner who shops when a storm is approaching may pay for a policy that doesn't protect the house in time.

Buy flood insurance when the forecast is quiet. Once a storm becomes the reason you're shopping, your options may not start soon enough to help.

The practical move is simple. Put flood coverage in place before you feel urgency. That's when you still have choices.

Florida Flood Insurance Frequently Asked Questions

Is Zone X the same as no flood risk

No. Zone X means flood insurance usually is not required by a lender. It does not mean water cannot reach the property.

I explain Zone X to homeowners this way. It often means lower mapped risk, not zero risk. In Florida, flood losses also come from street drainage failures, heavy rain, canal overflow, and stormwater backing up into areas that do not sit in the highest-risk zones. If a home would be hard to repair out of pocket, Zone X is still worth a serious look.

Why doesn't my homeowners policy cover flood damage

Homeowners insurance and flood insurance handle different kinds of water loss. A standard home policy generally covers sudden internal water damage from causes like a burst pipe. Flood insurance is designed for rising water that affects normally dry land and enters the home.

That distinction surprises people after a loss. From the homeowner's side, it is all water. From the policy side, the cause of that water decides whether there is coverage.

Should renters and condo owners think about flood coverage too

Yes. Renters can insure personal property, and condo unit owners may need protection for belongings and some interior items inside the unit.

I tell condo owners to read the association's master policy before assuming they are covered. In many cases, the association insures the building structure, while the unit owner still carries the risk for flooring, cabinets, contents, and upgrades. Renters face the same problem with furniture, clothing, and electronics.

Can I buy flood insurance right before a storm

Usually, no. Timing is one of the biggest mistakes Florida homeowners make.

Most flood policies do not start the same day you buy them. Many NFIP policies have a 30-day waiting period, and some private policies may start sooner, but they still may not take effect fast enough if a storm is already on the radar. Waiting until hurricane season feels active can leave you paying for a policy that does not protect you yet.

Is private flood insurance always better than NFIP

Not always. It depends on the property, the lender, the coverage limits you want, and how soon coverage needs to begin.

Private policies can offer higher limits or broader features for some homes. NFIP coverage can still be the better fit for other properties, especially if pricing, eligibility, or lender acceptance points in that direction. The right question is not which option sounds better. It is which policy form gives your household the best protection for the premium.

If you want help sorting through flood insurance in Florida without guessing, Select Insurance Group, Inc. can help you compare your options and understand what fits your home, lender requirements, and budget. A good flood policy is about more than price. It is about having coverage in force before the next round of heavy rain or storm surge.