You're probably dealing with this right now. A landlord asks for a certificate of insurance before handing over the keys. A client sends over a contract that requires liability coverage. Or you've opened your doors and realized one bad accident could put your business bank account, equipment, and future revenue on the line.

That's where General Liability insurance comes in. For North Carolina businesses, it isn't just a box to check. It's the policy that steps in when your business gets blamed for bodily injury, property damage, or certain advertising-related claims. And in this state, the legal environment makes that protection more important than many owners realize at first.

If you're financing a startup, expansion, or equipment purchase, insurance usually sits alongside the larger budget conversation. A practical resource for that planning stage is GoSBA Loans' 7(a) guide, especially if you're trying to line up working capital and operating costs at the same time. For business owners who want local insurance guidance, working with a North Carolina insurance agency can also make the process less trial-and-error.

Table of Contents

- Your NC Business Needs a Financial Shield

- What General Liability Insurance Actually Covers

- Why North Carolina Is a Unique Risk Environment

- Navigating NC and Industry Insurance Requirements

- Estimating Your General Liability Insurance Cost in NC

- General Liability vs Other Essential Business Policies

- How to Get Your NC General Liability Policy Today

Your NC Business Needs a Financial Shield

A lot of owners first think about insurance when someone else demands proof of it. That's understandable, but it's not the best way to look at general liability insurance NC businesses rely on every day.

The better view is simpler. Your business interacts with people, property, and public space. If someone says your company caused harm, you need a financial backstop between that claim and your operating cash.

A contractor leaves materials where a visitor can trip. A coffee shop customer slips near the counter. A cleaning company damages a client's floors. These aren't dramatic, rare disasters. They're normal business exposures. When they happen, the cost isn't limited to the damage itself. Significant pressure often comes from legal defense, medical claims, repair demands, and the time you lose dealing with all of it.

Practical rule: If your business meets the public, enters client property, advertises, or signs contracts, you already have liability exposure.

New owners sometimes assume careful operations are enough. Care matters, but it doesn't prevent allegations. Plenty of claims start with a disagreement over what happened, who caused it, and who should pay. Insurance exists because even a defensible claim can still be expensive to answer.

That's why I describe general liability as a financial shield, not a technical product. It protects the business you've built from the kind of third-party claim that can derail a young company fast.

Here's what usually works for small businesses in North Carolina:

- Buy before you need the certificate: Waiting until a lease or contract deadline creates rushed decisions.

- Match the policy to your actual operations: A consultant, a retailer, and a contractor don't present the same risk.

- Review exclusions early: The biggest mistakes happen when owners assume “liability” means “everything.”

What doesn't work is buying the cheapest option without checking whether it fits how the business operates. That's how coverage gaps show up at the worst time.

What General Liability Insurance Actually Covers

General liability insurance is your business's front-line protection when a third party says your company injured them, damaged their property, or harmed them through certain advertising-related actions. The simplest way to think about it is this: it's built for claims from other people, not for damage to your own building, your own vehicles, or your own employees.

A lot of policy language sounds abstract until you tie it to real business activity. Once you do that, the coverage is easier to understand.

The three claims most owners run into

Bodily injury is often the first category that comes to mind. Someone gets hurt and blames your business. That could be a customer falling in your store, a vendor getting injured while visiting your job site, or a member of the public alleging your operations created a hazard.

Property damage applies when your business is accused of damaging someone else's property. A technician drops equipment at a client location. A contractor cracks tile while moving materials. A service crew causes water damage during a job. Those are the kinds of events that often lead to this part of the policy being tested.

Personal and advertising injury is less obvious, but it matters for businesses that market themselves. If someone claims your ad harmed their reputation or misused protected material, this part of the policy may come into play depending on the wording and facts.

General liability is broad, but it isn't universal. It handles many third-party claims, not every business problem.

Where owners get tripped up

The most common misunderstanding I hear is that general liability covers anyone injured around the business. It doesn't work that way. A key example involves subcontractors and volunteers.

A practical warning from North Carolina guidance is that general liability typically excludes employee injuries, and NC courts may classify uninsured subcontractors as “employees” under workers' comp laws, which creates a major coverage gap. That's one reason it's so important to make sure partners and subs carry their own insurance, as noted in this North Carolina small business insurance guide.

That issue shows up often in construction, installation, event work, and service businesses that use flexible labor. The owner thinks, “They're not on payroll, so my GL should handle it.” Then a claim comes in and the classification issue changes everything.

A quick way to pressure-test your own exposure is to ask:

- Who visits your location: Customers, vendors, delivery drivers, or the public?

- Where do you work: Only from an office, or also at client sites and job sites?

- What do you handle: Tools, products, rented space, fragile client property, or advertising content?

If you can answer those three questions clearly, you're already close to understanding what your general liability policy needs to account for.

Why North Carolina Is a Unique Risk Environment

North Carolina isn't just another state regarding liability risk. The legal backdrop is different, and business owners who ignore that usually don't understand the stakes until a claim appears.

How pure contributory negligence changes the stakes

North Carolina is one of only four states with a pure contributory negligence rule, and the North Carolina Department of Insurance notes that this doctrine makes robust general liability coverage “critically important” even when it isn't legally mandated by the state in every situation. The department also explains that plaintiffs' attorneys are highly motivated to prove the business was 100% at fault in these cases, which raises the pressure around liability claims in this state. That guidance appears in the North Carolina Department of Insurance business insurance overview.

At first glance, some owners think this rule sounds favorable to businesses. They hear the legal phrase and assume fewer valid claims will get traction. In practice, the fight over fault can become more intense, not less. That means a business may still need to respond forcefully to allegations, preserve records, work with counsel, and rely on insurance to defend the claim.

Why this rule makes defense matter

In plain terms, North Carolina's liability environment rewards preparation. A business with weak documentation, no contract controls, poor housekeeping, or no insurance is exposed from multiple directions at once.

That's especially true after events that leave a messy fact pattern behind. Storms are a good example. Water intrusion, debris, temporary repairs, blocked walkways, and emergency contractors can all create confusion around who did what and when. If you're dealing with a property event, a practical companion read is immediate storm damage steps, because the first decisions after damage often affect both safety and later claims.

A North Carolina claim doesn't have to be simple to become expensive. It just has to require a defense.

That's why I tell owners not to treat general liability insurance NC coverage as optional just because state law doesn't universally force every business to buy it. In this state, the rulebook itself is a reason to carry it.

Navigating NC and Industry Insurance Requirements

Many owners hear that North Carolina doesn't require every business to carry general liability and stop there. In real life, that's rarely the full answer. Contract terms, lease requirements, and client onboarding rules often make coverage mandatory long before a state regulator does.

When coverage becomes mandatory in practice

The clearest hard requirement applies to businesses that contract with the state. In North Carolina, businesses working under state contracts must carry Commercial General Liability coverage on an occurrence basis with a minimum combined single limit of $1,000,000 per occurrence, according to the North Carolina DHHS contract terms. For many contractors and service vendors, that number becomes the practical benchmark for doing serious commercial work.

That standard matters beyond direct state jobs. Once one customer requires a certain limit, other customers often expect similar proof of insurance. Landlords do the same thing in commercial leases. Property managers, municipalities, event organizers, and larger private clients often won't let a business start work without a certificate.

If you're building a hands-on service company, this comes up early. For example, anyone researching starting a moving company business will quickly run into contracts, cargo concerns, premises risks, and customer damage allegations. Liability insurance becomes part of the setup, not an afterthought.

What to review before you sign

Before you sign a lease or service agreement, check these items carefully:

- Required limits: The contract may set a minimum liability amount.

- Coverage form: Some agreements specifically require occurrence-based coverage.

- Certificate timing: You may need proof before move-in, setup, or project start.

- Additional insured language: A client or landlord may ask to be added where appropriate.

- Scope of work: Make sure your policy matches what you do.

For broader business protection across multiple states and industries, owners often look at commercial insurance options in the Southeast when comparing what lines they may need in addition to GL.

What works is reviewing insurance requirements before you negotiate the final contract. What doesn't work is discovering the requirement the day before the job starts. That usually leads to rushed certificates, avoidable delays, or a policy that satisfies paperwork but misses the actual exposure.

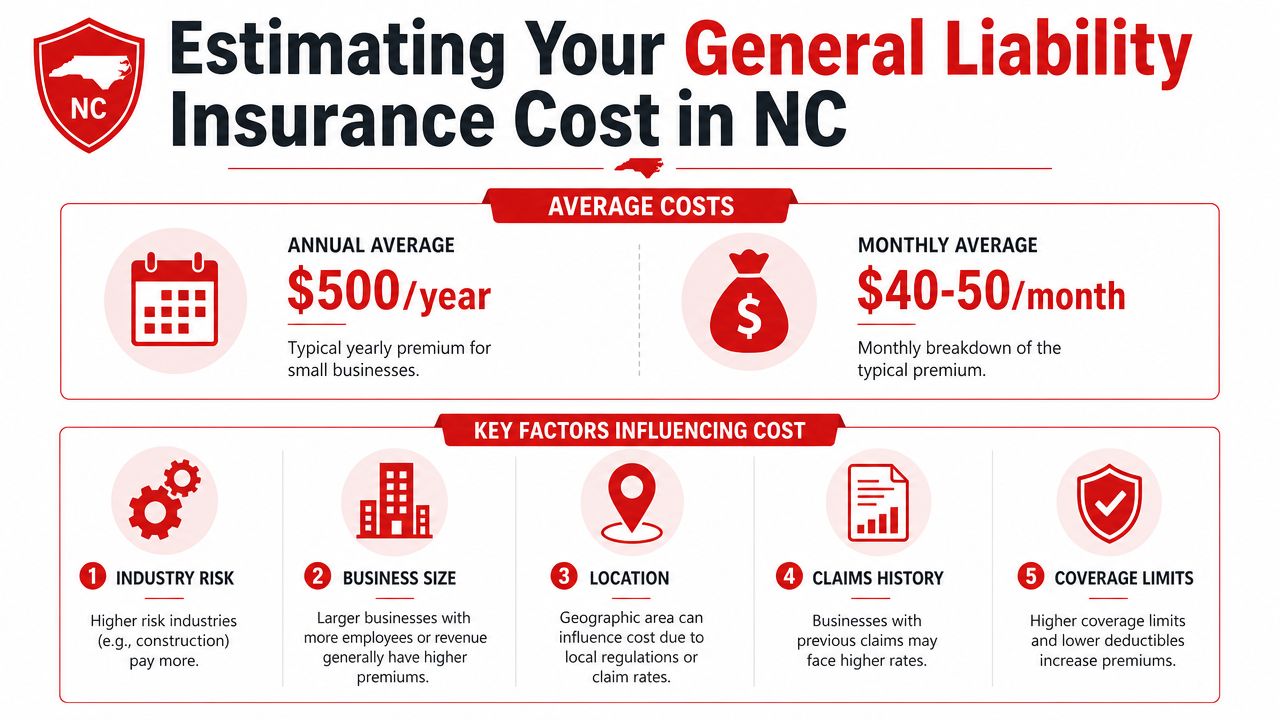

Estimating Your General Liability Insurance Cost in NC

Cost is usually the first practical question, and it should be. There's no point talking about risk management in vague terms if the owner needs a realistic number for the monthly budget.

A realistic starting point

For North Carolina businesses, the average annual premium for general liability insurance is $1,341, or about $112 per month, according to MoneyGeek's North Carolina general liability cost overview. That same source notes that actual premiums can range from $26 per month for lower-risk professions to more than $300 per month for higher-risk industries.

That range tells you something important. There isn't one “NC price.” There's a pricing band, and where your business lands depends on the kind of work you do and how much exposure you bring to the insurer.

Here's a simple way to think about the range:

| Business profile | Likely position in the range | Why |

|---|---|---|

| Low-contact office or consulting work | Lower end | Fewer physical injury and property damage exposures |

| Retail, café, or customer-facing storefront | Middle | Public foot traffic raises premises risk |

| Contractor, trades, or hands-on field work | Higher end | Job site hazards and third-party property exposure are greater |

Why one business pays more than another

Insurers price general liability by looking at the chance of a claim and the likely cost if one happens. In day-to-day terms, these factors usually move the price:

- Industry risk: A bookkeeper and a remodeling contractor don't present the same bodily injury exposure.

- Employee count: More people involved in operations can mean more opportunities for mistakes or incidents.

- Location: The business environment and operating setup affect how underwriters view exposure.

- Claims history: Prior issues can change how a carrier evaluates future risk.

- Coverage choices: Higher limits or broader needs can push premium upward.

Cost shortcut: The fastest way to waste money is to compare price without comparing class code, operations description, and exclusions.

What works is giving the underwriter a clean, accurate description of your business. What doesn't work is oversimplifying your operations to chase a lower quote. If the description doesn't match what you really do, the short-term savings can become a long-term problem when a claim is investigated.

General Liability vs Other Essential Business Policies

General liability is foundational, but it doesn't cover every loss a North Carolina business can face. A lot of expensive mistakes come from buying one policy and assuming it handles all accidents, all injuries, and all lawsuits.

It doesn't.

NC Business Insurance Coverage at a Glance

| Insurance Type | What It Covers | Example Scenario in NC |

|---|---|---|

| General Liability | Third-party bodily injury, property damage, and certain personal or advertising injury claims | A customer slips in your shop and alleges your business caused the injury |

| Workers' Compensation | Job-related injuries or illness involving employees | An employee hurts their back lifting materials on a job |

| Commercial Auto | Liability and physical damage involving business vehicles | Your company van hits another car while making deliveries |

| Professional Liability or E&O | Claims that your advice, service, or professional work caused financial harm | A consultant's mistake costs a client money even though nobody was physically injured |

That distinction between GL and workers' compensation is where many owners get caught. If someone is considered your employee for purposes of an injury claim, general liability usually isn't the policy designed to respond. For a practical breakdown of that separate coverage, this guide on what workers' compensation insurance covers is useful.

The gaps that surprise owners

Here are the misunderstandings I see most often:

- “My GL covers my staff if they get hurt.” Usually, employee injury issues point toward workers' comp, not general liability.

- “My GL covers my work truck.” Vehicle-related claims generally require commercial auto coverage.

- “If a client says my advice caused them to lose money, GL handles it.” That's usually a professional liability issue, not a premises or bodily injury claim.

- “One policy should cover everything my business does.” Most businesses need a small group of policies that work together.

A restaurant may need GL for customer injuries, workers' comp for staff, and commercial auto if it delivers. A contractor may need GL, workers' comp, commercial auto, and possibly other lines depending on tools, property, and contract obligations. A consultant may need less premises coverage than a storefront, but more attention to professional liability.

Buying the wrong policy isn't much better than having no policy at all when the claim falls outside the coverage grant.

The practical takeaway is simple. General liability is one pillar. It's not the whole building.

How to Get Your NC General Liability Policy Today

A lot of owners start shopping for general liability after a landlord asks for a certificate, a client sends over contract insurance requirements, or a job is ready to start and coverage is suddenly holding everything up. In North Carolina, waiting until the last minute is a costly mistake. One claim, or even one disputed claim, can create real expense fast, and our pure contributory negligence rule makes liability disputes less forgiving than many owners expect.

The fastest way to get it right

The quickest path is to give the agent or carrier a clear picture of your business the first time. Vague applications slow everything down, and they can lead to a policy that fits poorly once the underwriter understands what you do.

Start here:

Define your operations clearly

Be specific about the work. “Construction” says almost nothing. “Interior painting for residential remodels” or “janitorial service for small office buildings” gives the underwriter enough detail to classify the risk correctly.Gather your business details

Have your legal business name, business address, estimated revenue, employee count, and prior claims history ready. If a landlord, lender, or client requires certain limits or additional insured wording, get that requirement in hand before you request quotes.Compare fit before price

A lower premium can come with exclusions, the wrong class code, or limits that do not satisfy your contract. I tell owners to read the quote like a working document, not a receipt. If the description of operations is off, fix it before binding.Bind coverage before your deadline

Leave time for certificate corrections, policy review, and any underwriting follow-up. Coverage bought the same day a lease is signed or a project starts often creates unnecessary problems.

What to have ready

These items usually speed up the process:

- Your lease, contract, or bid insurance requirements

- A short description of your day-to-day operations

- Estimated annual revenue

- Employee count and payroll details if requested

- Prior insurance and loss history

- Certificate holder information for the client, landlord, or property manager

For North Carolina business owners, this is not just paperwork. It is how the policy gets matched to the actual risk. That matters if a customer is injured, a property damage claim turns into a dispute, or the other side starts arguing over fault. In a pure contributory negligence state, liability cases can turn on small facts, and the wrong policy setup can leave an owner paying to sort out problems that should have been addressed before the job started.

Select Insurance Group, Inc. is one available option for North Carolina business owners seeking general liability coverage and related commercial policies.

The right policy matches how your business operates, satisfies contract requirements, and gives you a realistic layer of financial protection when a claim threatens cash flow. If you need help sorting through limits, exclusions, or quote options, contact Select Insurance Group, Inc. for a no-obligation conversation about protecting your North Carolina business.