Homeowners insurance in Charlotte averages $1,984 per year for a policy with $300,000 in dwelling coverage, which is lower than the $2,377 national average for comparable coverage. That means Charlotte is still a relatively affordable market, but the cheapest quote on your screen isn't always the safest choice for your home.

A lot of homeowners start with the wrong question. They ask, “Who has the lowest rate?” A better question is, “What does that rate provide?” In Charlotte, that difference is often underestimated. Some low-price quotes only look attractive because they assume lower coverage limits, higher deductibles, or policy terms that leave real gaps when a claim happens.

I've seen the same pattern over and over in this market. A homeowner thinks they found affordable home insurance in Charlotte, but the quote only works because it trims protection where it hurts most. That can mean not enough dwelling coverage, a roof settlement that pays less than expected, or a deductible that feels manageable right up until a storm hits.

Charlotte still offers good value compared with many other markets, especially compared with higher-risk coastal areas. But rates have been climbing across North Carolina, and rebuild costs haven't stood still. If you want a policy that's both affordable and useful, you need to compare more than price.

Table of Contents

- Finding Affordable Home Insurance in Charlotte

- What Determines Your Charlotte Home Insurance Premium

- Decoding Your Policy What Coverage You Actually Need

- Practical Discounts and Adjustments for Lower Premiums

- The Smart Way to Compare Home Insurance Quotes

- Get Expert Help with Select Insurance Group

Finding Affordable Home Insurance in Charlotte

Charlotte gives homeowners a better starting point than many markets. For $300,000 in dwelling coverage, the city's average premium is $1,984 annually, below the $2,377 national average for similar coverage, according to Charlotte homeowners insurance rate data from Insurify. That's good news, but it only tells part of the story.

Affordable home insurance in Charlotte isn't about grabbing the lowest number and hoping for the best. It's about finding a premium that fits your budget while still protecting the home you own. If your policy falls short on dwelling, roof settlement, or loss-of-use coverage, a low premium can become a very expensive problem.

Many homeowners also assume all quotes are built the same way. They aren't. Two policies can both look “affordable,” but one may be built for real replacement needs and the other may be built to win a price comparison.

Practical rule: Treat the premium as the final result, not the starting point. First confirm the coverage, then decide whether the price makes sense.

A solid shopping process usually starts with three questions:

- What would it cost to rebuild your home? Market value and rebuild value aren't always the same.

- How is your roof being covered? This can change both price and claim payout.

- What deductible can you realistically handle? A lower premium only helps if the deductible still works for your emergency budget.

If you're starting from scratch, a local Charlotte home insurance quote option can help you compare policies built around the same coverage assumptions instead of comparing mismatched offers. That's the only way to tell whether a quote is affordable or just stripped down.

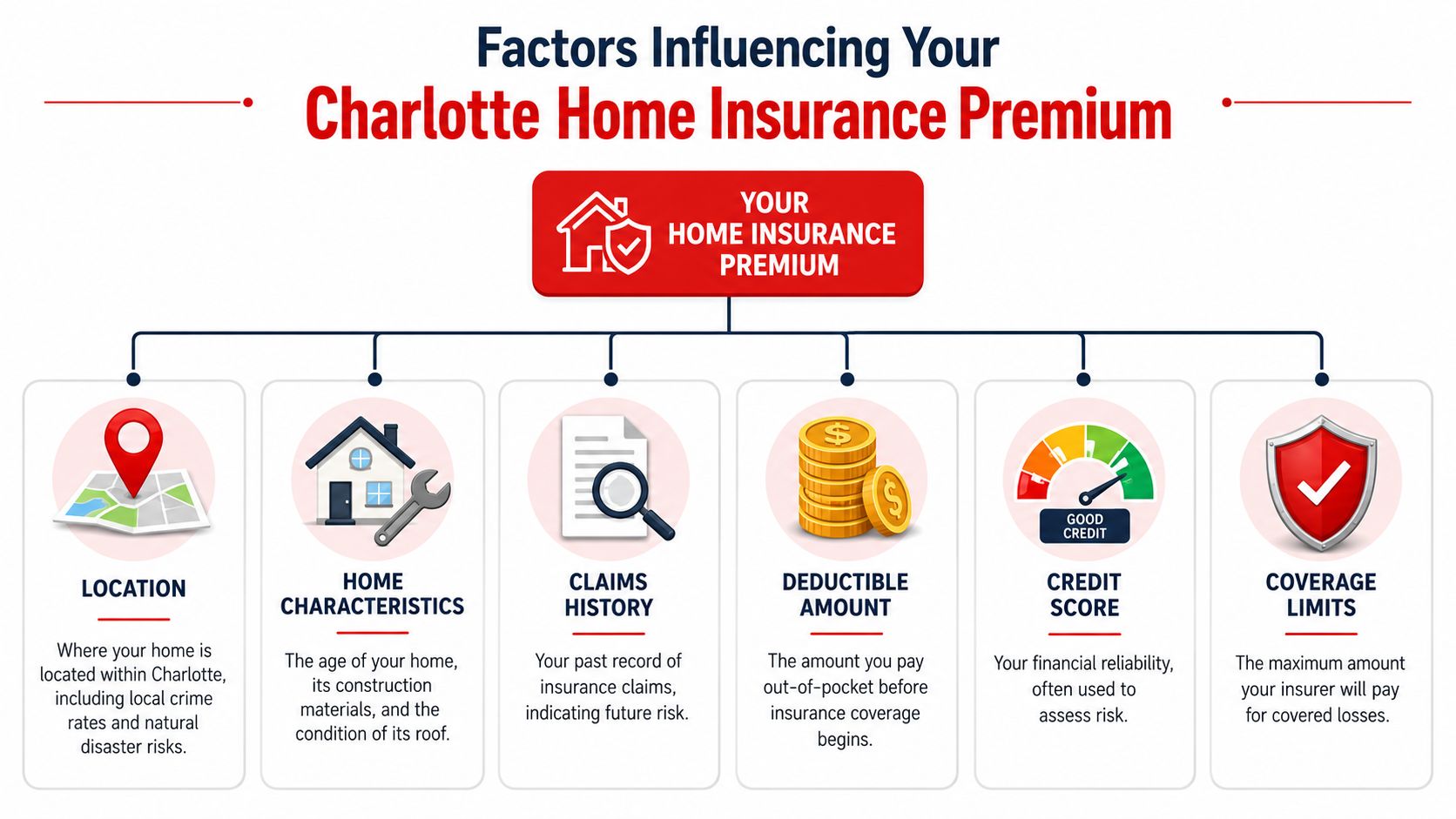

What Determines Your Charlotte Home Insurance Premium

Insurance carriers build your premium from a risk recipe. Some ingredients come from the house itself. Others come from where the property sits and how the insurer views your profile. If you know which parts move the price, you can make better decisions before you shop.

Your house sets the baseline

The home itself drives a large share of the premium. Age, condition, construction type, and updates all matter. Roof age matters a lot.

In Charlotte, insurers typically apply surcharges or switch roof coverage to actual cash value for roofs aged 15 to 20 years, and they may decline coverage for roofs over 20 years, according to local guidance on homeowners insurance near Charlotte. That means two similar homes can price very differently if one roof is newer and documented while the other is older or unverified.

This is one of the most overlooked issues I see. Homeowners remember the year the kitchen was updated. They don't always keep paperwork on the roof. For underwriting, that paperwork matters.

If you're buying a home, it's smart to look beyond the inspection summary and understand how insurers will read the property. This explanation of understanding appraisal inspection costs helps clarify the difference between what lenders review and what a buyer should examine more closely before binding coverage.

Location and personal profile shape the final number

After the house details, carriers weigh location. Even inside the Charlotte area, rates can shift based on ZIP code, local fire protection, storm patterns, and how a carrier scores that neighborhood. Charlotte's inland location helps compared with coastal parts of the state, but carriers still account for thunderstorms, wind, hail, and other severe weather exposure.

Your personal profile also affects pricing. Claims history can raise concern quickly, especially if losses suggest maintenance issues or recurring water problems. Credit-based insurance scoring can also influence what a homeowner pays, depending on the carrier's underwriting model.

Then there's the broader pricing environment. North Carolina's average homeowners insurance rate increased by more than 36% from 2018 through 2023, and base homeowners rates in the Charlotte metro area rose 7.5% on June 1, 2025, with another 7.5% scheduled for June 1, 2026, according to the Kenan Institute analysis of North Carolina's home insurance market. Even if nothing changed about your house, the market around you did.

A premium increase doesn't always mean your carrier made a mistake. Sometimes it means your roof aged another year, your area was re-rated, or statewide pressure finally hit your renewal.

Decoding Your Policy What Coverage You Actually Need

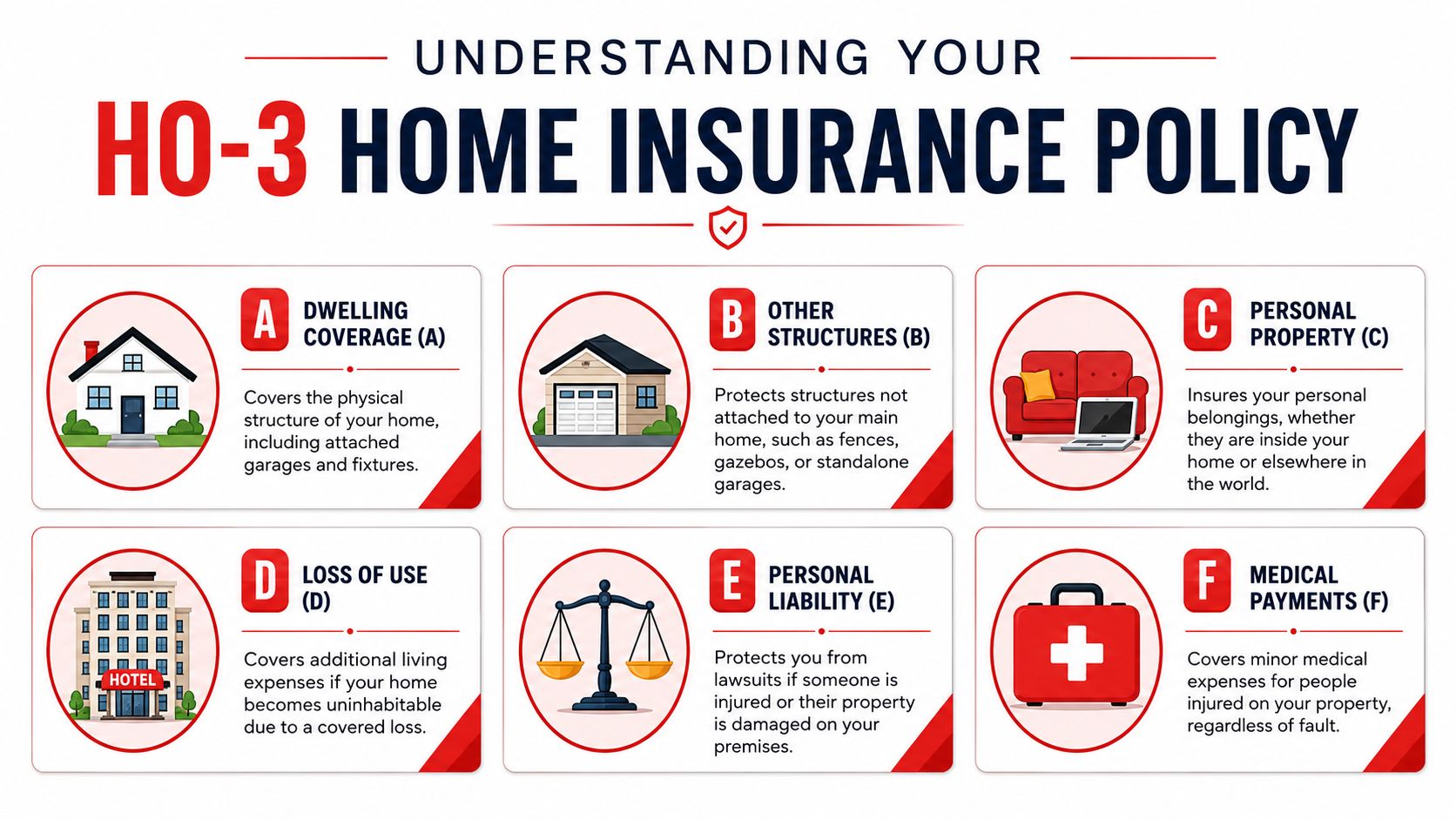

A homeowners policy is a financial safety net, but only if each part is sized correctly. Most standard policies include separate buckets for the structure, detached structures, belongings, living expenses after a covered loss, liability, and smaller guest injury payments. If one bucket is too small, the whole policy feels cheaper than it really is.

What the main coverage parts do

Dwelling coverage protects the house itself. This is the number that has to reflect rebuild reality, not wishful thinking.

Other structures coverage applies to detached items like sheds or fences. Homeowners often forget this until storm damage reaches beyond the main house.

Personal property coverage protects belongings. Furniture, electronics, clothing, and household items all live here, subject to policy terms and sublimits.

Loss of use coverage helps if a covered claim makes the home unlivable. Hotel stays, temporary rent, and related living expenses can become a major issue faster than people expect.

Liability coverage protects you if someone is injured on your property or if you cause property damage to others. Medical payments coverage is smaller in scope but can help with minor injury situations.

For a plain-English breakdown of policy language, Restore Heroes' guide to home insurance is a useful companion when you're reviewing declarations, endorsements, and settlement terms.

Why cheap quotes can become expensive mistakes

The value conversation highlights how some “cheap” Charlotte quotes look cheap because they assume about $150,000 in dwelling coverage, while low advertised premiums such as $805 can be tied to those reduced limits instead of the protection many homeowners need, according to Insuranceopedia's review of cheap homeowners insurance in Charlotte.

That gap matters because a policy doesn't need to fail completely to hurt you. It only needs to come up short when labor, materials, code upgrades, debris removal, and temporary housing all show up in the same claim.

“Affordable” should mean you can keep the policy and survive the claim. If it only helps with the first part, it isn't real value.

Another policy detail to watch is how the roof is settled. Replacement cost and actual cash value are not the same thing. Replacement cost aims to pay for a new item of like kind and quality, subject to policy terms. Actual cash value reduces the payout for age and wear. If your quote is lower because the roof settlement changed, you need to know that before you bind coverage.

Practical Discounts and Adjustments for Lower Premiums

Good coverage doesn't have to mean overpaying. The best savings usually come from tightening the policy intelligently, not gutting it. That matters even more now because rates have been under pressure statewide. North Carolina's average homeowners rate increased by more than 36% from 2018 through 2023, and Charlotte base rates increased 7.5% in 2025 with another 7.5% scheduled for 2026, as noted earlier in the statewide market analysis.

Discounts worth asking about

Some savings are simple and easy to miss if you don't ask. Carriers may offer discounts based on home features, policy history, or household profile. Availability varies by insurer, so ask each carrier to confirm what's built into the quote.

A stronger home security setup can help with both prevention and eligibility for certain credits. If you're evaluating what meaningful protection looks like in practice, Overton's guide to residential security gives helpful context on home security options and what homeowners should think through before investing.

| Discount Type | Potential Savings |

|---|---|

| Monitored security system | Varies by carrier |

| Claims-free history | Varies by carrier |

| Newer roof or documented roof replacement | Varies by carrier |

| Bundling home with auto or other policies | Varies by carrier |

| Paperless billing or automatic payment | Varies by carrier |

| New home or recent major updates | Varies by carrier |

Policy changes that can lower cost without gutting protection

If discounts aren't enough, policy structure is the next lever. Homeowners can save money through policy adjustments, but they risk weakening the policy, so each change needs a reason.

- Raise the deductible carefully. A higher deductible can lower the premium, but only if you can comfortably absorb that out-of-pocket amount after a storm or fire loss.

- Document updates before renewal. Roof replacement, electrical updates, plumbing improvements, and protective devices don't always get captured automatically.

- Bundle if the combined value works. Bundling can help, but only if both policies remain competitive and the home policy keeps the coverage you need.

- Review endorsements instead of deleting protection blindly. Some add-ons are worth keeping. Others may no longer fit your property.

- Compare rebuilt quotes on equal terms. A lower rate is meaningful only when coverage A, deductible, roof settlement, and endorsements match.

For homeowners focused on price, this North Carolina homeowners insurance comparison page can be a starting point for checking cost options. Just make sure every quote you review is built on the same coverage assumptions.

The Smart Way to Compare Home Insurance Quotes

Shopping one quote at a time is where many homeowners lose the plot. They compare a basic premium from one carrier against a broader policy from another, then assume the cheaper one is a better deal. It usually isn't.

Charlotte rates can vary sharply between carriers for the same basic profile. For a sample policy, State Farm averages $604 annually, while the citywide average runs about $1,195 to $1,424, according to The Zebra's Charlotte homeowners insurance data. That spread is exactly why quote comparison matters.

Why side by side shopping matters

The right comparison is boring on purpose. Same dwelling amount. Same deductible. Same roof settlement basis. Same liability limit. Same endorsements where possible. Once those line up, the premium difference becomes useful.

A side-by-side quote review should answer these questions:

- Is the dwelling limit consistent? If one quote cuts the structure limit, it may look cheaper for the wrong reason.

- How is the roof covered? This can change the payout more than homeowners expect.

- What endorsements are included or missing? Water backup, ordinance coverage, and similar items can differ.

- How high is the deductible? Premium savings can disappear if the deductible no longer fits your reserve cash.

A clean three step process

Start with property details. Gather the roof year, square footage, update history, and any protective devices. If you don't know the roof age, verify it before shopping.

Then decide what “good coverage” means for your household. Don't let the quote define your protection after the fact. Set your target dwelling, deductible comfort level, and liability baseline before you compare.

Finally, review at least three quotes side by side. If you're using an independent agency model, one option available in the market is access to multiple carriers through a single intake process, which can save time compared with calling separate offices individually. The key is not convenience alone. It's making sure every quote is built on the same blueprint.

The smartest shopper isn't the one who finds the lowest premium first. It's the one who catches the policy difference before a claim does.

Get Expert Help with Select Insurance Group

Affordable home insurance in Charlotte comes down to balance. You want a premium you can live with, but you also need coverage that holds up when repair bills, temporary housing costs, and policy settlement terms get tested. Price matters. So does structure.

That's where local guidance helps. A homeowner usually doesn't need more jargon. They need someone to check whether the quote is affordable because it's efficient, or affordable because it subtly reduced protection. That distinction is where a lot of costly mistakes start.

Select Insurance Group's Charlotte insurance agency page is one place to start if you want to compare home insurance options through an independent agency. The agency states that it works with 20 to 40 carriers, brings over 30 years of experience, offers digital service tools, and provides bilingual support for Spanish-speaking customers. For homeowners who want to save time without skipping the coverage review, that setup can be practical.

The goal isn't to buy the cheapest policy on the page. The goal is to buy a policy that still looks smart on claim day.

If you want help reviewing your current policy or comparing quotes for better value, Select Insurance Group, Inc. offers free, no-obligation insurance quotes. A quick review can help you see whether your current premium is genuinely affordable, or just artificially low because the coverage is too thin.