You've found a house near the water, the inspection looks manageable, and then the insurance quotes arrive. That's usually the moment Georgetown starts feeling less like a postcard and more like a risk map.

New homeowners here run into the same questions fast. Does the policy cover wind from a hurricane? Is flood separate? Why is one quote so different from the next? If the house needs roof work, does that change what an insurer will offer? If you're sorting through that now, it helps to see how other storm-prone areas handle roof-related claims and documentation. This overview of Western Washington roof insurance info is useful because the claim habits are similar even if the weather patterns aren't.

Georgetown SC home insurance is workable, but it isn't something to buy casually. Coastal location, flood exposure, older housing stock, and storm deductibles all change the decision. The right approach is to build coverage around the actual way Georgetown homes get damaged, not around a generic checklist.

Table of Contents

- Protecting Your Home in Georgetowns Unique Coastal Setting

- What a Standard Georgetown Home Insurance Policy Covers

- Navigating Coastal Risks Hurricane Wind and Flood

- Why Georgetown Home Insurance Costs What It Does

- Essential Optional Coverages You Should Seriously Consider

- How to Lower Your Georgetown Home Insurance Premiums

- Finding the Best Coverage with Select Insurance Group

- Frequently Asked Questions about Georgetown Home Insurance

Protecting Your Home in Georgetowns Unique Coastal Setting

Georgetown has a different insurance profile than most inland South Carolina towns. The appeal is obvious. Marsh views, river access, historic neighborhoods, and easy access to the coast. The insurance side is less obvious until you start reading exclusions and deductibles.

A new resident often assumes a homeowners policy works the same way it did in a previous city. Then they learn that coastal coverage depends on the exact address, how close the home sits to water, whether wind coverage is included, and whether the property falls into a flood-prone area. Two houses with similar sale prices can produce very different insurance results because the policy is priced around rebuilding risk, not curb appeal.

Georgetown buyers usually don't need more jargon. They need someone to translate the policy into one simple question: if a storm hits this specific house, what exactly gets paid and what does not?

That's the lens that matters. Not the marketing language. Not the lowest starting premium. The true test is whether your coverage lines up with how losses happen here. In Georgetown, that means paying close attention to flood, wind, roof condition, construction details, and how much you'd have to pay out of pocket before insurance responds.

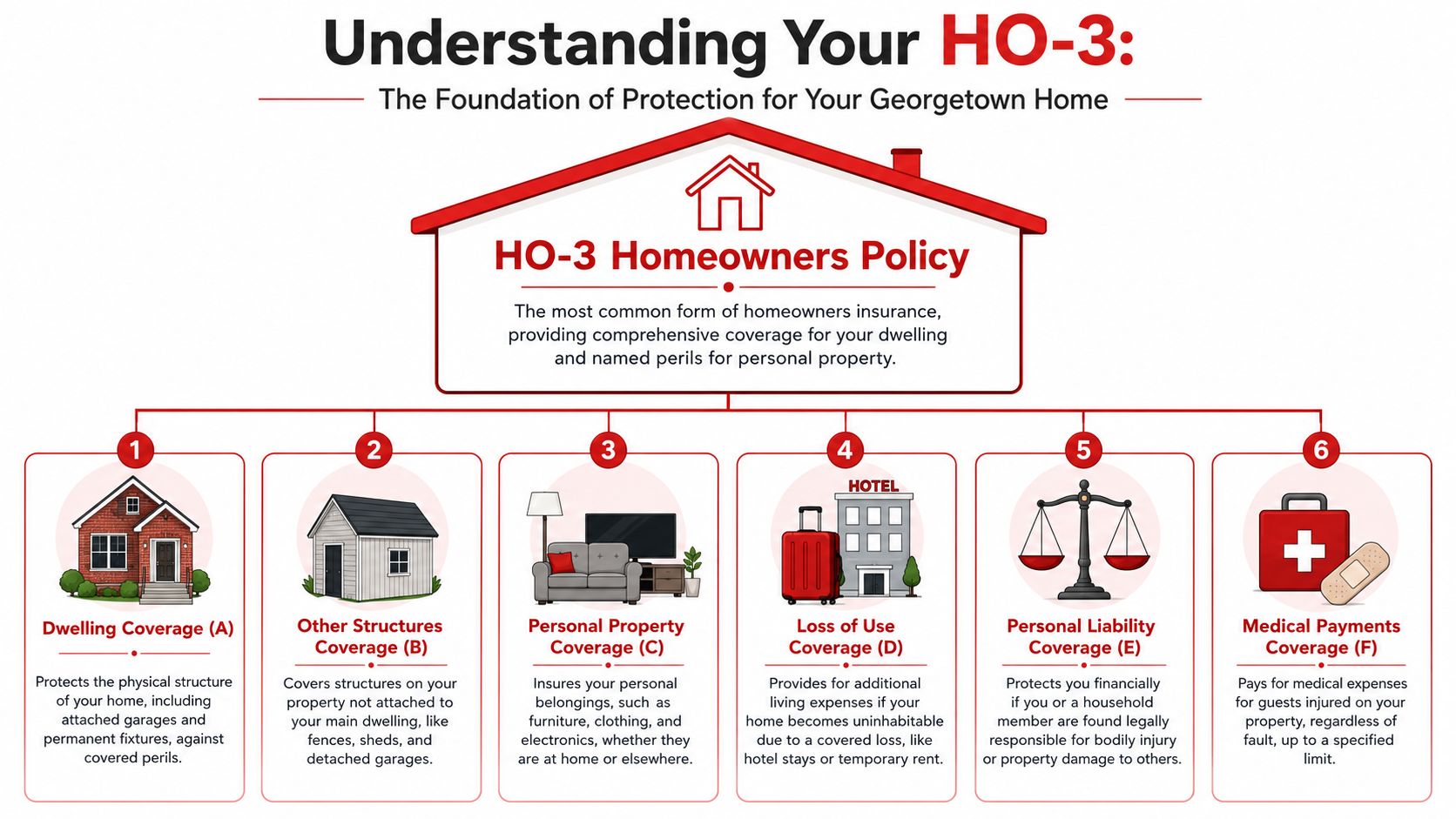

What a Standard Georgetown Home Insurance Policy Covers

A standard homeowners policy is best understood as a financial toolkit. It gives you several different protections under one contract, but it doesn't cover every coastal risk automatically.

The six parts most homeowners rely on

Most Georgetown homeowners carry an HO-3 style policy. That policy commonly includes these core pieces:

- Dwelling coverage pays to repair or rebuild the house itself after a covered loss.

- Other structures coverage applies to detached items like a shed, fence, or separate garage.

- Personal property coverage helps replace belongings inside the home.

- Loss of use coverage helps with temporary living expenses if a covered claim makes the home unlivable.

- Personal liability coverage helps if someone claims you caused bodily injury or property damage.

- Medical payments coverage can help with smaller guest injury expenses, regardless of fault.

That sounds broad, and in many ways it is. Fire, certain types of accidental water damage, theft, liability claims, and several common property losses usually fall within the normal framework of the policy.

For a Georgetown homeowner, though, the basic structure is only the start. The bigger question is how each part is valued and where the policy stops.

Where homeowners get surprised

The first surprise is valuation. The difference between actual cash value and replacement cost matters more than many buyers realize. With actual cash value, depreciation gets deducted. With replacement cost, the policy is designed to pay what it takes to replace covered property at today's cost, subject to policy terms. That distinction is frequently misunderstood, and standard policies often cover personal belongings at only 50% of the dwelling limit, which can be too low for higher-value coastal homes, as explained in this breakdown on actual cash value, replacement cost, and standard personal property limits.

The second surprise is what the standard policy does not cover. Flood is the clearest example. Rising water from storm surge, overflowing water, or runoff is not something you should assume a homeowners policy handles.

Practical rule: If the damage comes from water rising from the outside in, treat flood coverage as a separate decision until someone proves otherwise in writing.

A third issue is sublimits. Jewelry, water backup, detached structures, special collections, and ordinance-related rebuilding costs may not be covered the way an owner expects unless they review endorsements closely.

A strong policy isn't just a policy with a high dwelling number. It's one where the valuation method, coverage parts, and exclusions all make sense for the house you own.

Navigating Coastal Risks Hurricane Wind and Flood

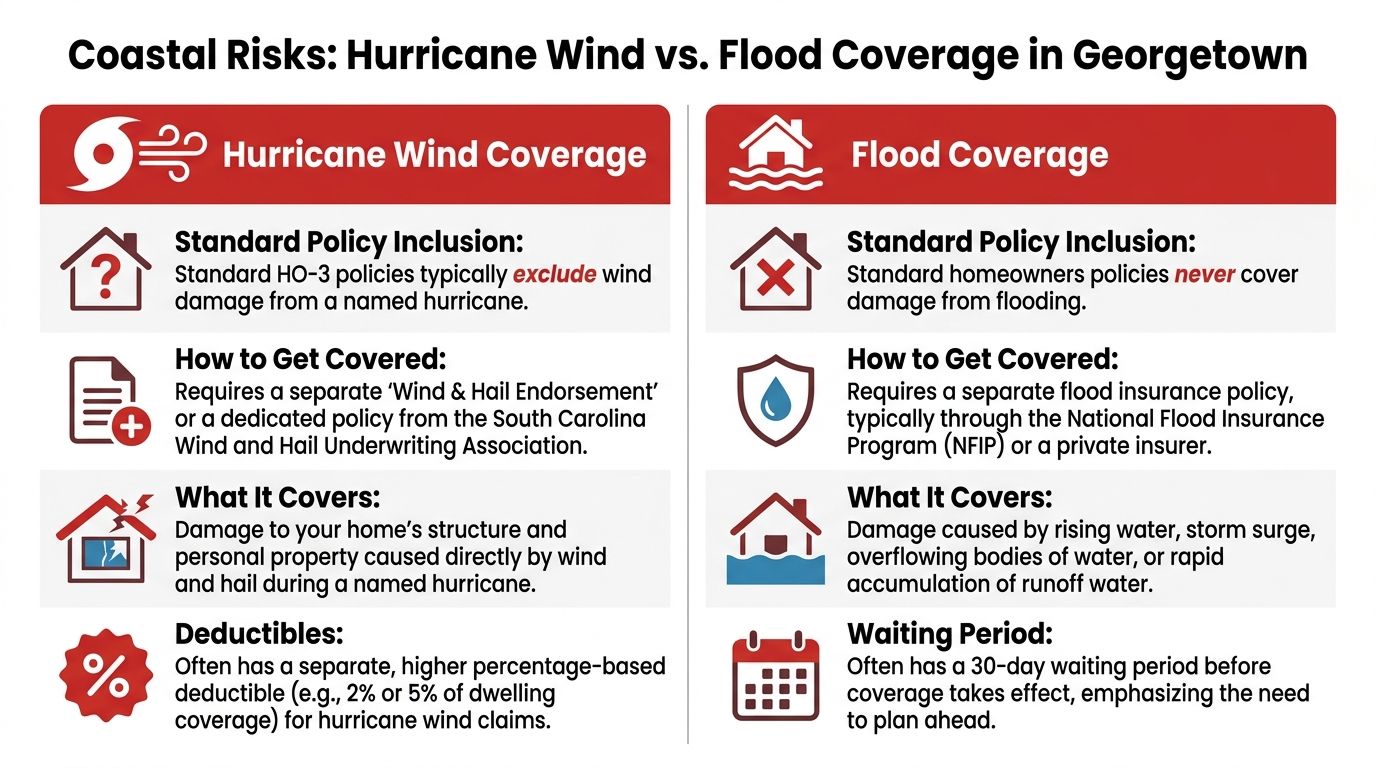

In Georgetown, the most expensive misunderstandings usually happen when homeowners treat hurricane wind and flood as one problem. They aren't. They are handled differently by insurers, and claims often turn on that difference.

Wind and flood are not the same claim

Wind damage may be covered through your homeowners setup, but coastal policies often handle it with stricter terms, separate endorsements, or a separate wind and hail arrangement. Flood is different. Standard homeowners insurance does not cover it.

That distinction matters after a storm. If wind tears shingles off a roof and rain enters through that opening, the claim analysis is different from water that rises across the lot and enters through doors or foundation vents. The damage can happen during the same event, but the policies responding to each cause can be separate.

Another issue is the hurricane deductible or named storm deductible. Instead of a flat deductible, many coastal policies use a percentage-based deductible tied to the home's insured value. That means your out-of-pocket cost after a hurricane claim can be much larger than homeowners expect. This is one of the first figures I tell Georgetown buyers to verify before they bind coverage, because it changes how much emergency savings they should keep available.

If storm damage does happen, cleanup and drying need to move quickly. Homeowners trying to understand the sequence after a major loss often benefit from reviewing Purified Air Duct Cleaning's restoration guide, because it lays out the practical order of response after property damage.

Why Georgetown owners need to think ahead

The market is reacting to climate exposure, not just to isolated claims. Georgetown County is projected to face a 199% increase in home insurance premiums, approximately $7,100 annually, by 2035 under a medium climate risk scenario, according to reporting on the county's projected climate-driven premium spike. That projection doesn't mean every policy will look the same, but it does show why coastal underwriting has become stricter.

For homeowners, the practical takeaway is simple:

- Review wind wording carefully so you know whether wind is included, limited, or written elsewhere.

- Buy flood before you need it because flood policies often involve a waiting period.

- Match deductible to savings so a claim doesn't create a cash-flow problem.

- Price the coast realistically by comparing local options, including resources focused on coastal home insurance in Charleston SC, since nearby coastal markets often reveal how carriers think about shoreline risk.

A Georgetown house can be well insured, but only if the owner separates the storm into its real components instead of assuming one policy handles everything.

Why Georgetown Home Insurance Costs What It Does

Homeowners usually ask one fair question after seeing quotes. Why does this cost what it costs?

Part of the answer is that Georgetown sits in a coastal risk environment, but the local pricing story is more nuanced than many people expect. The average isn't one fixed number because coverage choices and home characteristics change the premium quickly.

What the local price range tells you

One published estimate places Georgetown homeowners at an average of $101 per month, or about $1,212 annually, while noting that some sources place the local average closer to $1,822 annually. That same source shows Georgetown below coastal Charleston at $159 per month and below Greenville at $149 per month, which highlights how much pricing can vary by market and policy setup. You can review those Georgetown comparisons in this summary of South Carolina homeowners insurance costs.

Those figures don't contradict each other as much as they seem to. They show what experienced agents see every day. A policy quote changes based on the home's age, build quality, distance to water, deductible, endorsements, prior claims, and replacement cost assumptions. Two Georgetown homeowners can both say they have “home insurance” and still have very different pricing because they are insuring different risk profiles.

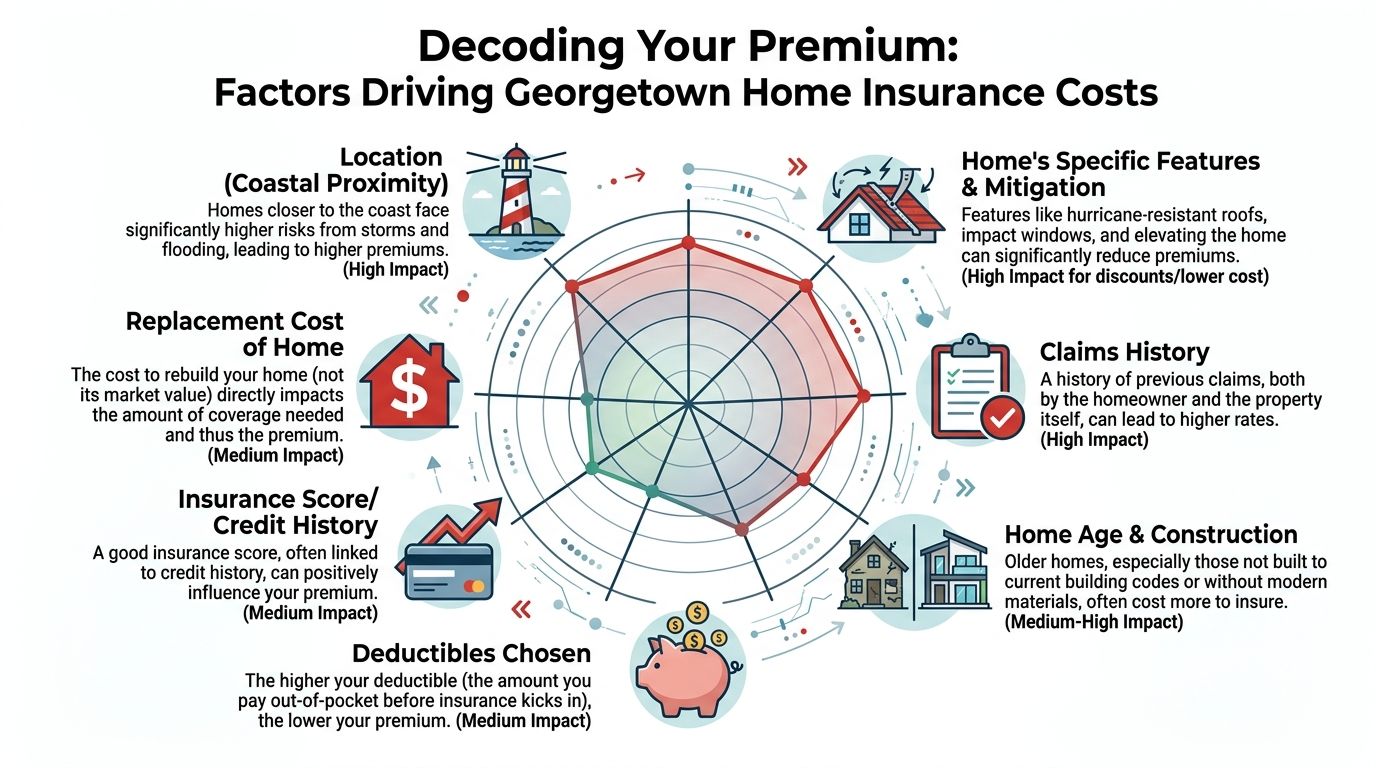

The rating factors that matter most

The most important drivers tend to be local and structural:

- Coastal proximity affects exposure to wind, storm surge, and moisture-related loss.

- Flood zone placement changes whether separate flood coverage is merely wise or effectively required.

- Age of the house matters because older roofs, wiring, plumbing, and code issues can concern underwriters.

- Construction details matter a lot in coastal towns. Foundation type, roof shape, opening protection, and wind resistance can all influence price.

- Fire protection and access can affect how a carrier rates the property.

- Rebuild cost matters more than market value. Insurance is pricing what it would take to repair or reconstruct the structure.

Lower than Charleston doesn't automatically mean inexpensive. In Georgetown, a quote can look reasonable until you notice what it leaves out.

That's why Georgetown SC home insurance has to be compared on more than premium alone. The useful comparison is premium plus deductible plus exclusions plus the quality of the rebuild assumptions behind the policy.

Essential Optional Coverages You Should Seriously Consider

“Optional” is a misleading word for coastal property insurance. Some add-ons aren't luxuries. They're the parts that close the exact gaps most likely to matter in Georgetown.

Flood insurance for rising water exposure

If your home has any meaningful flood exposure, separate flood coverage belongs near the top of the list. Standard homeowners insurance doesn't step in for rising water losses. Buyers sometimes delay this purchase because the house hasn't flooded before or because the lender didn't require it. That's a weak filter for risk.

If you're comparing how flood protection fits into a broader coastal insurance plan, this overview of flood insurance options and considerations is a useful starting point.

Wind and hail protection when the base policy falls short

Some coastal homeowners need dedicated wind and hail protection or an endorsement that changes how wind damage is covered. The key is not to assume. Confirm whether the policy includes named storm wind, what deductible applies, and whether roof settlement will be handled on a replacement cost basis or with depreciation.

Condo owners have a parallel issue. Their association's master policy may insure the building differently than they expect, which is why unit owners often need HO-6 coverage for their interior responsibility, belongings, liability, and certain loss assessment exposures.

Builders risk for homes under construction or renovation

This one gets missed often in waterfront and renovation-heavy areas. Standard policies often exclude damage during construction. That makes builder's risk, also called dwelling under construction coverage, important for new builds, major remodels, and homes being repaired after a storm. The South Carolina Department of Insurance notes the importance of shopping carefully for property coverage, and this page on South Carolina homeowners insurance guidance is the right place to start when you're assessing gaps around construction-related exposure.

If you're renovating an older Georgetown property, don't assume your current policy follows the project automatically. Ask exactly when coverage changes, who insures materials on site, and whether flood or wind damage during construction is addressed anywhere in writing.

How to Lower Your Georgetown Home Insurance Premiums

The cheapest policy usually isn't the best value. The smarter move is to lower cost without creating a dangerous coverage gap.

The savings moves that usually help first

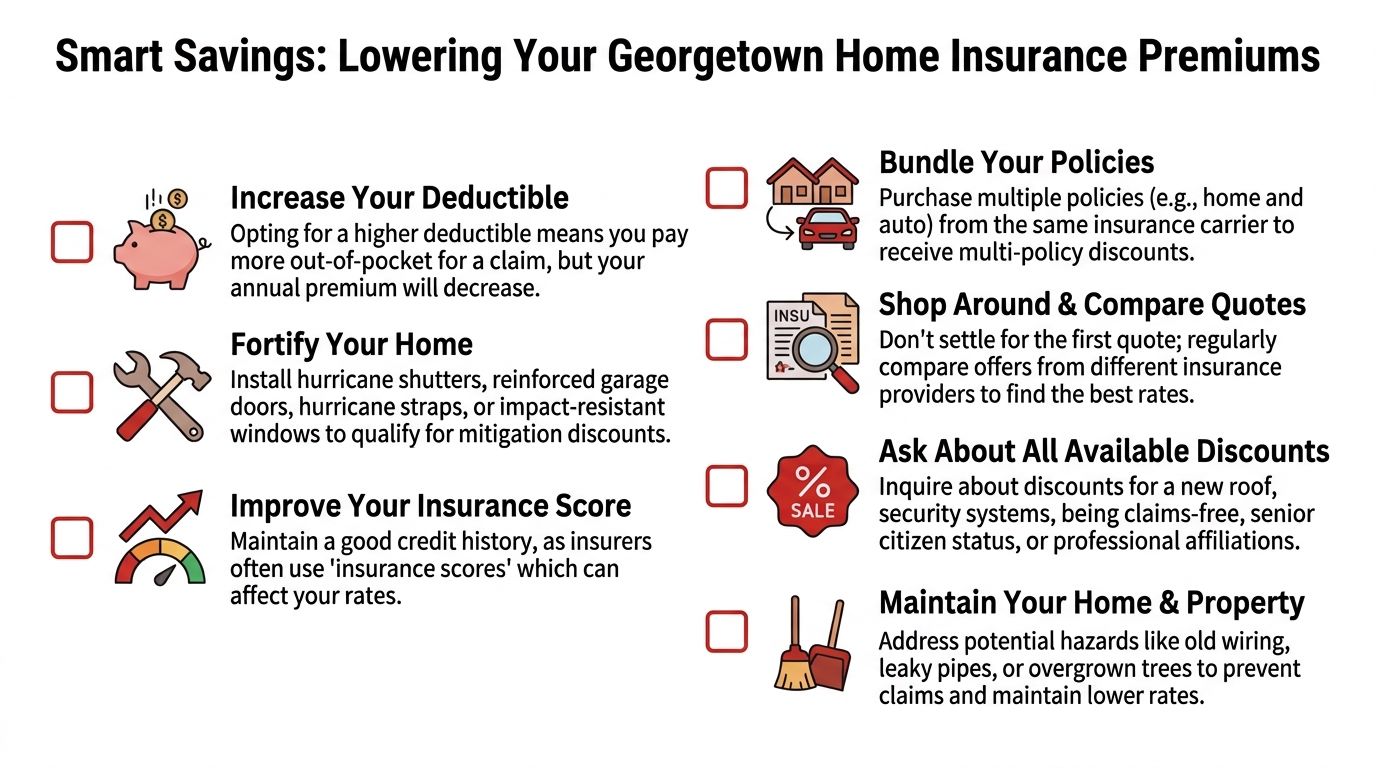

Start with the decisions that don't change the structure of the house:

- Raise the deductible carefully if you have enough reserve cash to handle a claim.

- Bundle policies when the numbers work rather than buying each line separately by habit.

- Ask about every available discount for claims-free history, alarms, newer roof features, or policy packaging.

- Shop regularly because one carrier may price your exact address and construction style more favorably than another.

These are the easy wins. They don't require a contractor, and they can improve the premium picture fairly quickly.

Improvements that can earn better pricing

The bigger long-term savings often come from mitigation. The South Carolina Department of Insurance confirms that premium determinants include construction type and fire protection, and that homeowners can earn significant credits by making their homes more resilient to wind damage. That point appears in the department's guidance discussed earlier.

In practical terms, that means features such as fortified roof components, better opening protection, and other wind-resistance improvements can matter. The exact credit depends on the carrier and the home, but the principle is consistent. Homes that are harder to damage are often less expensive to insure.

A few habits also help indirectly:

- Maintain the property so small leaks, tree hazards, or electrical issues don't become claims.

- Document upgrades with permits, invoices, and photos.

- Review replacement cost after improvements so the insured value stays aligned with the actual house.

Finding the Best Coverage with Select Insurance Group

Good coastal insurance advice usually comes down to one thing. Someone has to look at the full picture, not just the premium.

That means checking whether the dwelling value reflects rebuild cost, whether wind is covered in the expected way, whether flood should sit beside the homeowners policy, and whether the deductible fits your budget. It also means thinking ahead to claim time. When a storm hits, homeowners don't want to argue over what they thought they bought. They want the paperwork to match the true risk.

For people who want help comparing options across more than one carrier, multi-state insurance agency support for home and flood coverage can make the process easier to evaluate. Select Insurance Group, Inc. works as an independent agency that compares quotes across multiple carriers, including homeowners and flood coverage, which is often more useful in a coastal market than relying on a single-company option.

The right next step is simple. Get quotes built around your exact property details, then review the quote forms line by line. In Georgetown, that review matters as much as the price.

Frequently Asked Questions about Georgetown Home Insurance

Some questions come up in almost every coastal home purchase. Here are the ones that usually matter most once you're past the first quote.

| Question | Answer |

|---|---|

| What does an HO-6 policy cover in Georgetown? | HO-6 is designed for condo owners. It usually covers your personal belongings, personal liability, additional living expenses after a covered loss, and the interior portions of the unit that the condo association's master policy doesn't insure. The exact boundary depends on the association documents, so read those before choosing limits. |

| Is flood insurance included in a standard homeowners policy? | No. Standard homeowners insurance does not cover flood damage from rising water. If the property has flood exposure, you should review a separate flood policy. |

| How is a hurricane deductible different from a normal deductible? | A normal deductible is often a flat dollar amount. A hurricane or named storm deductible is commonly percentage-based and tied to the insured value of the home. That means your out-of-pocket cost can be much higher after a hurricane loss. |

| Why are two Georgetown quotes so far apart? | Quotes can differ because carriers rate location, construction, roof age, deductible choice, wind terms, prior claims, and replacement cost differently. One quote may also include coverage that another quote excludes or limits. |

| Does a new roof help with Georgetown SC home insurance? | It often can. Newer, more wind-resistant roof systems may improve eligibility or pricing, especially when the work is well documented and meets current standards. |

| Do I need builder's risk coverage for a major renovation? | Often, yes. If the home is under construction or undergoing a substantial remodel, standard homeowners coverage may not fully protect the project. That gap should be checked before work begins. |

| Should I choose actual cash value or replacement cost? | For most homeowners, replacement cost offers stronger protection because actual cash value deducts depreciation. The right fit depends on budget and how much out-of-pocket risk you're willing to accept after a loss. |

A good Georgetown insurance decision usually comes from asking better questions, not just collecting more quotes. Ask what's excluded. Ask how wind is handled. Ask whether flood is separate. Ask how the claim would be settled if the house had major roof, water, or interior damage after a storm.

That's how you avoid the common coastal mistake. Buying a policy that looks acceptable until you need it.

If you want help reviewing Georgetown SC home insurance options for your home, Select Insurance Group, Inc. can help you compare coverage choices, including homeowners and flood, and sort through the local coastal details before you bind a policy.