In North Carolina, State Farm often shows up as the cheapest homeowners insurer, with one analysis putting it at $1,274 per year, which is 66% below the state average of $3,747. But that headline only tells part of the story, because the cheapest company for your house can change fast based on your ZIP code, dwelling coverage, deductible, roof age, and claims history.

That's the part most homeowners miss. They hunt for one magic company name, click a “cheapest” list, and assume they're done. In North Carolina, that's how people end up underinsured, overpaying, or both.

We've seen this over and over. A homeowner in one part of the state can get a very different answer than someone with the same house value somewhere else. Change the coverage amount, and the ranking can shift again. Add a recent claim, and the old front-runner may not even be competitive anymore. If you want the cheapest homeowners insurance in North Carolina, stop looking for a universal winner and start using a disciplined comparison process.

That process is what saves money.

Table of Contents

- Why North Carolina Home Insurance Rates Are Rising

- Decoding Your North Carolina Homeowners Policy

- Actionable Tactics to Lower Your Premium Now

- The Smart Way to Shop and Compare Quotes

- Looking Beyond the Price Tag on Your Insurance Quote

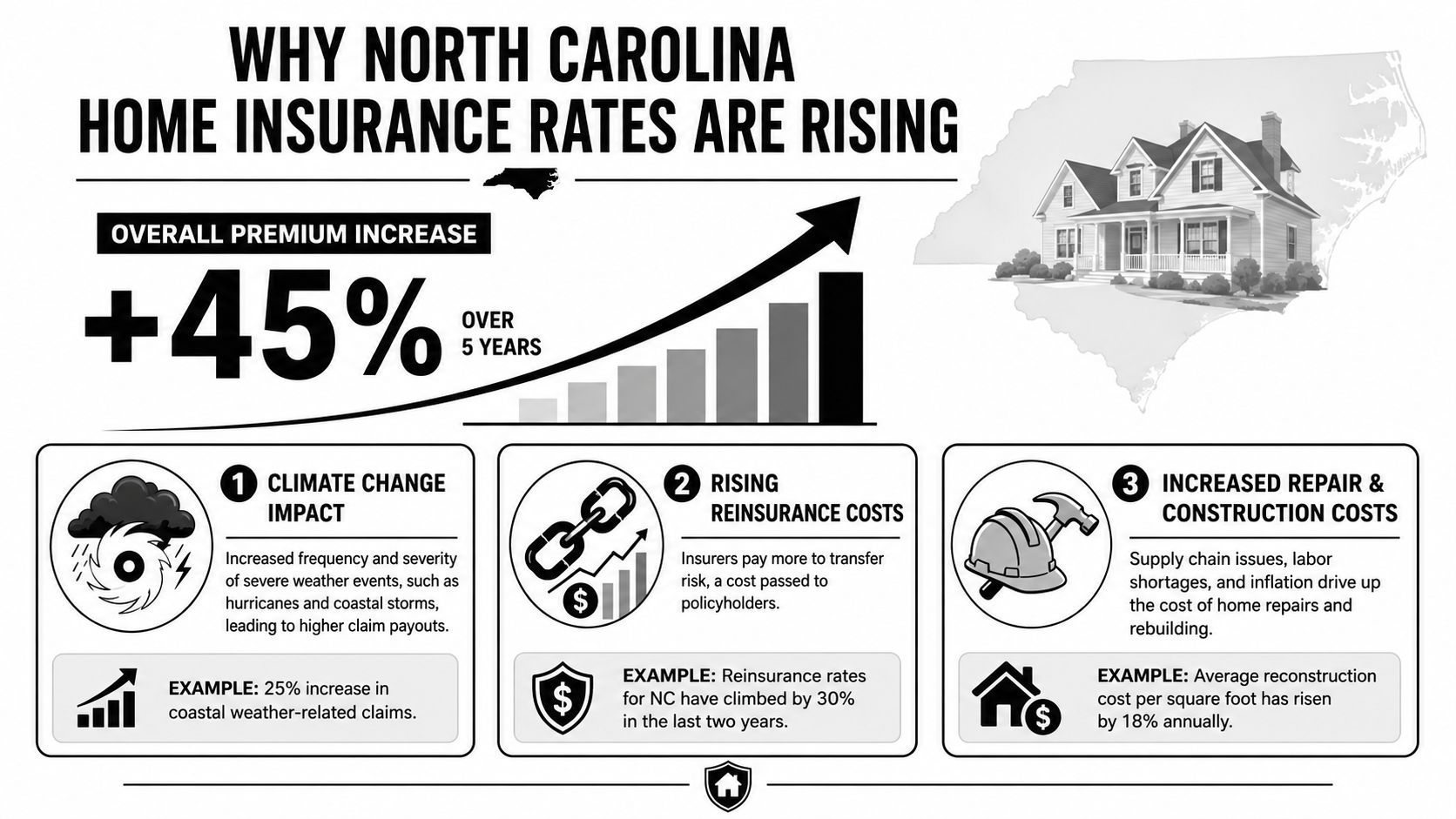

Why North Carolina Home Insurance Rates Are Rising

North Carolina homeowners have a right to be frustrated. From 2018 through 2023, the state's average homeowners insurance rate increased by more than 36%, slightly above the national increase of about 34% over the same period, according to the UNC Kenan Institute's North Carolina home insurance analysis.

The rate pressure is real

Homeowners usually think their premium should stay stable if they haven't filed a claim. That's not how this market works. Insurers price risk across whole regions, not just one address. If storms, rebuilding costs, and large losses keep climbing around the state, your renewal can rise even when your personal record is clean.

That's why we tell people to stop taking rate hikes personally. The smarter move is to understand what's driving them, then focus on the pieces you can influence.

Why the state gets hit from multiple angles

North Carolina has a pricing problem because it has a geography problem. Coastal homes deal with hurricane and wind exposure. Inland homes still face severe weather, including major storms that damage roofs, siding, windows, and outbuildings. The risk isn't limited to beach communities.

Then there's rebuilding cost. When a carrier looks at your home, it isn't asking what your house would sell for. It's asking what it would cost to repair or rebuild after a covered loss. Labor, materials, and contractor demand all push that number higher, especially after widespread storm activity.

A simple reality check helps here:

| Pressure point | Why it raises premiums |

|---|---|

| Coastal storm exposure | Carriers price for hurricane and wind losses in exposed areas |

| Inland severe weather | Roof and exterior claims still drive losses away from the coast |

| Higher rebuild costs | Repairs cost more, so insurers need more premium to support the risk |

North Carolina isn't one insurance market. It's several smaller risk markets stitched together.

That's why statewide averages can mislead you. If you want a broad view of available protection, it helps to review actual North Carolina home insurance options instead of relying on one statewide number.

What you can control and what you can't

You can't control hurricane tracks or regional claim trends. You can control how your policy is built.

That matters because the state shows huge pricing variation by location. One North Carolina dataset found a statewide average premium of $1,166 per year, with the cheapest ZIP code averaging $863 per year in Alexander County, while Wilmington averaged $7,015 per year and New Hanover County averaged $6,651 per year, according to The Zebra's North Carolina homeowners insurance analysis. Another data set found a low-cost ZIP at about $1,744 annually and a high-cost ZIP at $29,676 annually, which shows just how much location can overwhelm every other factor in pricing.

So yes, rates are rising. But no, that doesn't mean you're stuck. It means your shopping process has to be tighter, more local, and more precise than the average “cheapest company” article makes it sound.

Decoding Your North Carolina Homeowners Policy

If you don't understand the policy, you can't judge the price. That's where many homeowners go wrong. They compare premiums without checking whether they're comparing the same coverage.

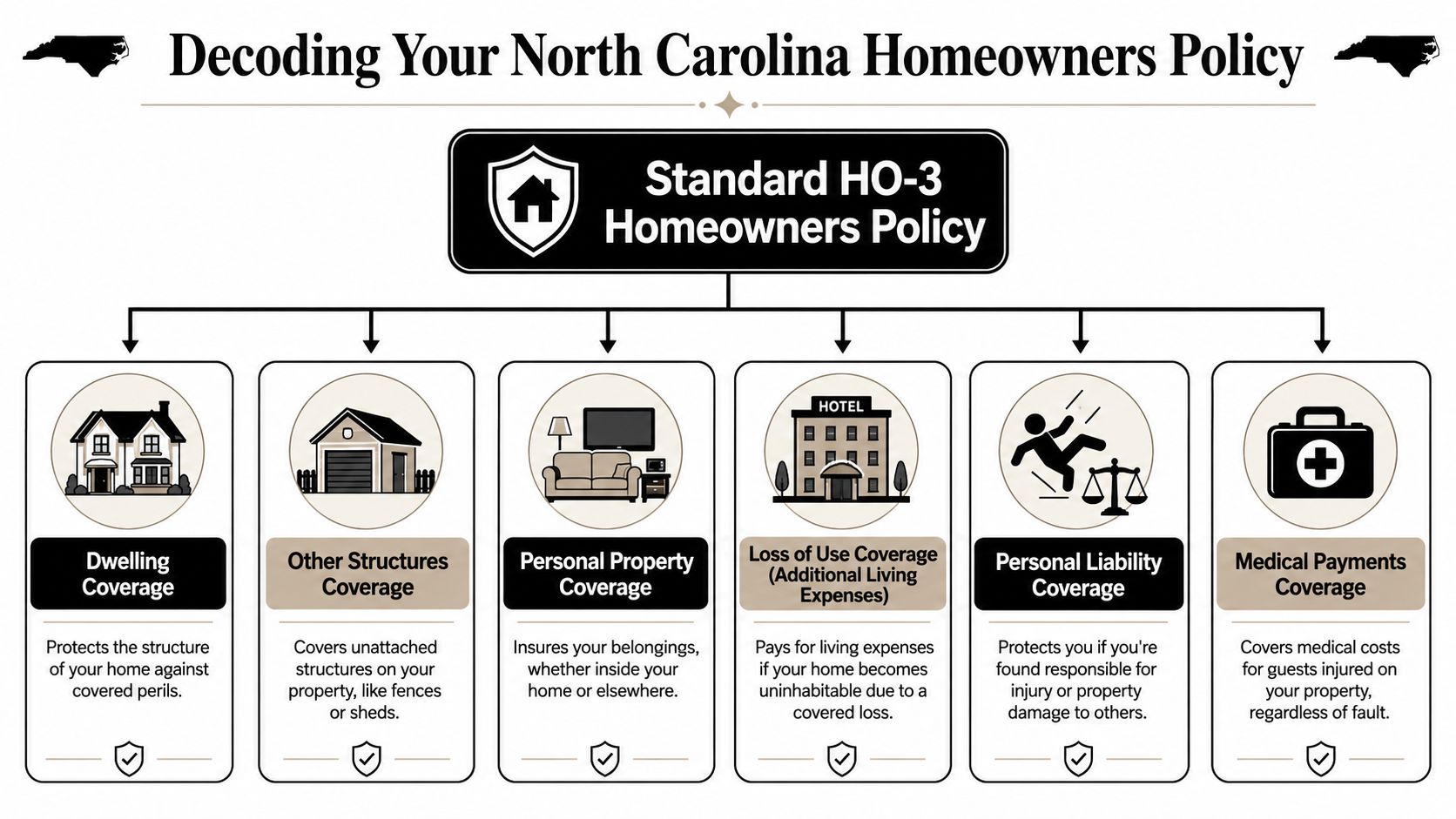

What the main coverages actually do

A standard homeowners policy usually includes several core parts. You don't need to memorize insurance jargon, but you do need to know what each piece protects.

- Dwelling coverage protects the main structure of your home. If a covered loss damages the house itself, this is the coverage that pays to rebuild or repair it.

- Other structures coverage applies to things like a detached garage, fence, or shed.

- Personal property coverage helps replace your belongings, such as furniture, clothes, and electronics, if they're damaged by a covered loss.

- Loss of use coverage helps with temporary living expenses if a covered claim makes your home unlivable.

- Personal liability coverage protects you if someone claims you caused injury or property damage.

- Medical payments coverage helps with smaller guest injury expenses, regardless of fault.

A practical example makes this easier. If a storm drops a tree on your detached garage, that may involve other structures coverage. If roof damage forces you out during repairs, loss of use may matter more than you expected. If a guest slips on your steps, liability and medical payments are what you'll care about.

Why dwelling coverage changes who looks cheapest

The biggest pricing lever is usually dwelling coverage, which is why “cheapest homeowners insurance in North Carolina” becomes slippery. One analysis found the cheapest carrier in North Carolina at $994 for $200,000 in dwelling coverage and also $2,323 for $1 million in coverage, which proves the cheapest carrier is not a fixed attribute. It changes with the protection level you choose, as shown in Insure.com's North Carolina homeowners insurance comparison.

Here's the mistake we see all the time. A homeowner lowers the dwelling amount to make one quote look attractive, then compares it against another quote built on better protection. That's not savings. That's a bad comparison.

Practical rule: Don't compare homeowners quotes until the dwelling amount, liability limit, and deductible match.

This is even more important with older houses, where rebuild details can be trickier and replacement estimates need extra attention. If that's your situation, review homeowners insurance for older homes in North Carolina before assuming the lowest premium is the right fit.

Where homeowners get tripped up

Storm claims expose weak policies fast. After roof or wind damage, homeowners often discover they didn't understand their deductible, exclusions, or repair process. If you're dealing with storm-related property issues, Superior Home Improvement's storm claim help is a useful resource for understanding the repair side before claim confusion gets worse.

Watch these trouble spots when reviewing a quote:

| Policy area | Why it matters |

|---|---|

| Deductible | A lower premium can hide a deductible you won't like during a claim |

| Coverage limits | Lower limits make quotes look cheaper but reduce protection |

| Special endorsements | Some homes need added protection for specific risks or property types |

Cheap only counts if the policy still works when your roof leaks, your kitchen burns, or your house is unlivable after a storm.

Actionable Tactics to Lower Your Premium Now

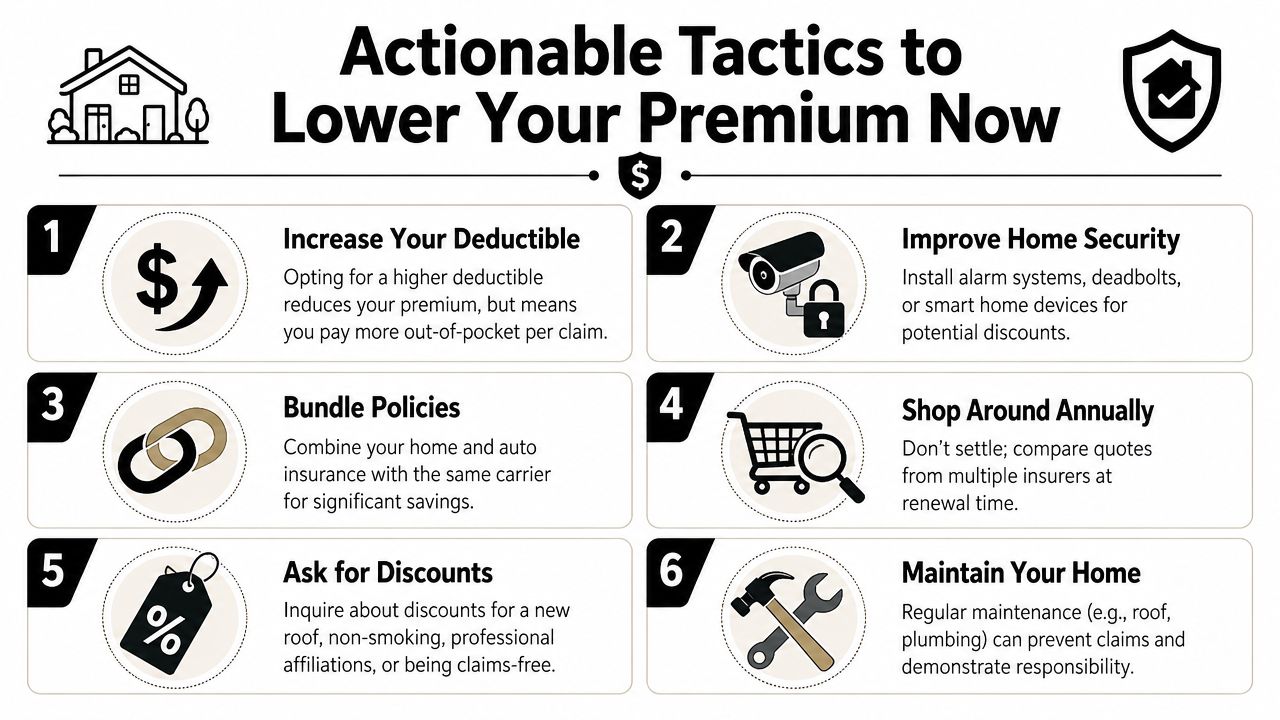

You don't need gimmicks to cut your premium. You need a short list of moves that affect pricing. Some are easy. Some require tradeoffs. All of them are worth discussing before your next renewal.

Start with the discounts that matter

Bundling is one of the few discounts that can move the needle. In North Carolina, one analysis estimated that bundling home and auto insurance can reduce homeowners costs by 13%, according to The Zebra's review of North Carolina home insurance pricing and discounts.

That said, don't get hypnotized by the word “discount.”

A big discount on an overpriced policy is still an overpriced policy.

That's why we compare the final premium, not the marketing language. A carrier with no flashy bundle pitch can still beat a carrier offering multiple discounts if the base rate starts lower.

Other credits may come from home features and condition. Ask about them directly. Don't assume they were automatically applied.

- Roof updates often matter because newer roofs generally present less claim risk.

- Security features like monitored alarms or certain protective devices can help.

- Claims-free history may improve pricing if your record is clean.

- Home maintenance matters more than people think. Moisture issues, long-term leaks, and neglected repairs can work against you during underwriting. If you're dealing with damp subfloor conditions or persistent humidity under the home, these crawl space moisture solutions can help you address a problem that often turns into bigger repair and insurance headaches.

Use deductibles carefully

Raising a deductible is a valid way to lower premium, but only if you can afford that deductible after a loss. We've had plenty of homeowners ask for the lowest possible premium, only to regret it when a claim happens and they realize the out-of-pocket cost is more than they can comfortably handle.

A better approach is to ask one blunt question: “If I have a claim next month, could I pay this deductible without going into debt?” If the answer is no, the cheaper premium isn't worth it.

Keep your thinking practical:

- Choose a deductible you can fund from savings. Not one you hope you'll figure out later.

- Review any wind or hurricane deductible language carefully. Don't assume all losses hit the same deductible.

- Balance premium savings against claim reality. A policy that looks cheap on paper can feel expensive the day you use it.

Ask better questions before renewal

Most homeowners ask, “Can you make it cheaper?” That's too vague. Ask questions that force a real review.

Try these instead:

- Can we re-shop this with the same coverage limits? That keeps the comparison honest.

- Are all available home, auto, roof, and protective-device credits applied? Missing discounts are common.

- Is my dwelling amount still accurate? Too low is dangerous. Too high can waste money.

- Did anything about my home profile trigger higher pricing? Roof age, claim history, and construction details all matter.

- Would a different deductible improve the premium enough to justify the risk? Sometimes yes. Sometimes not.

One North Carolina analysis priced policies at $300,000 dwelling, $100,000 liability, and a $1,000 deductible and found the cheapest carrier at $1,401 per year. That same source makes the bigger point: standardized inputs are what make a comparison useful. If you change the inputs, the rankings can change too. That's the shopping discipline homeowners need if they want the cheapest homeowners insurance in North Carolina without gutting the policy.

The Smart Way to Shop and Compare Quotes

Homeowners don't always have a rate problem. They have a comparison problem.

The same house can produce very different prices depending on how and where you shop. One analysis found State Farm cheapest at $1,274 per year, which was 66% below the state average, but other studies show different figures under different assumptions. That's why the “cheapest” insurer is a moving target, as shown in MoneyGeek's North Carolina homeowners insurance comparison.

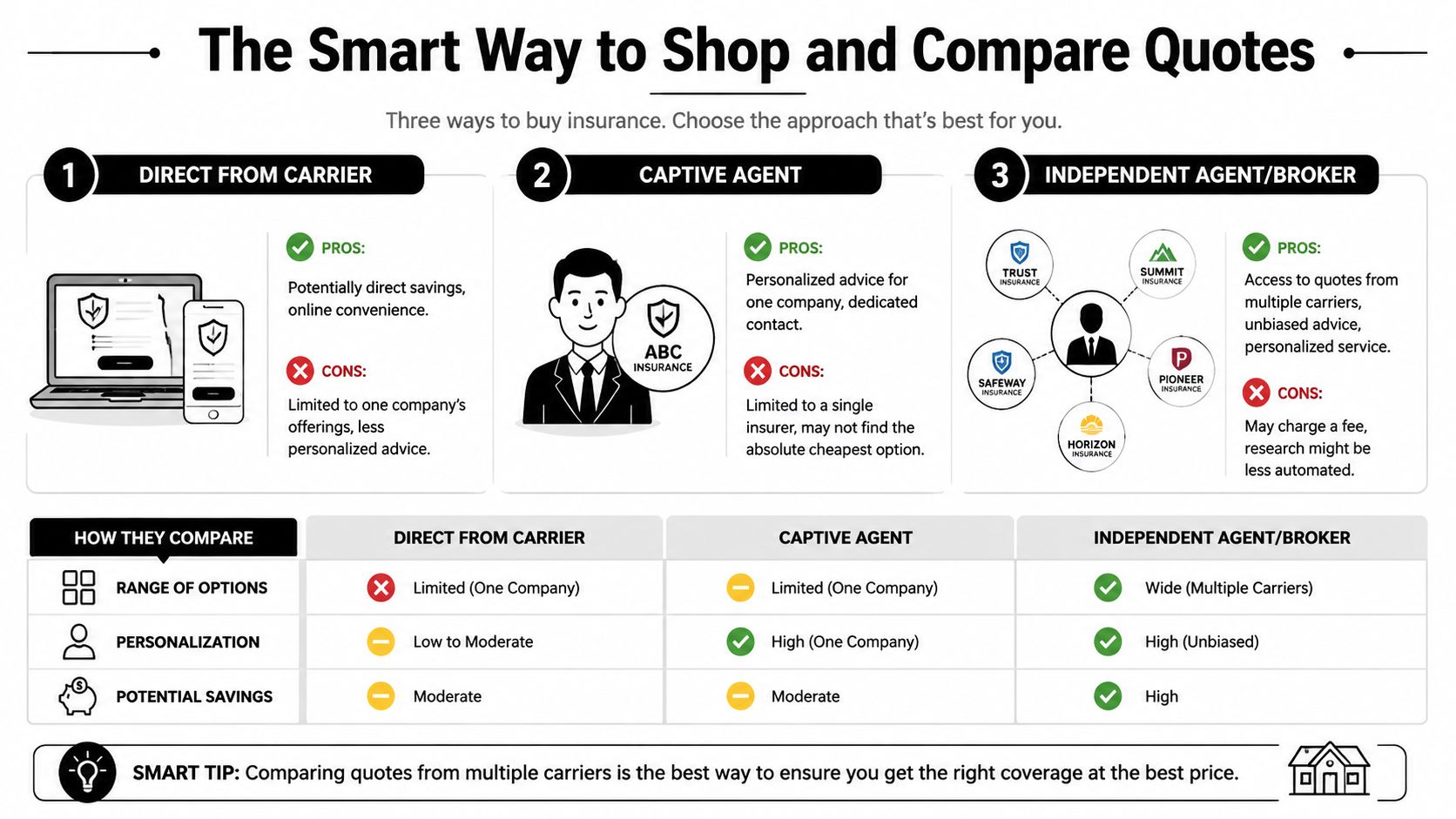

Three ways to buy and why one works better

You can buy homeowners insurance three basic ways.

| Shopping path | What you get | Main limitation |

|---|---|---|

| Direct | Fast access to one carrier's quote flow | You only see one company's answer |

| Captive agent | Advice tied to one insurer's products | Still limited to one market |

| Independent agent | Multiple carrier options under one review | Quality depends on how disciplined the comparison is |

If your house is straightforward and you like doing all the legwork yourself, direct shopping can work. If you already know you want one specific carrier, a captive path can be fine.

But North Carolina is not a market where one-size-fits-all shopping works well. Location, coverage amount, roof details, age of home, and claims history can all swing the result. That's why we think an independent comparison is the most efficient route for most homeowners.

Select Insurance Group, Inc. offers a homeowners insurance quote process that compares multiple carriers rather than locking you into one company's pricing. That kind of setup is useful when your goal is to find your personal cheapest policy, not just the cheapest headline rate from a generic list.

What to have ready before you shop

A clean comparison starts before the first quote.

Bring these details together first:

- Current declarations page so the coverages and deductibles can be matched

- Basic home details including year built, roof age, square footage, and construction type

- Claim history because prior losses can affect both price and availability

- Any recent upgrades such as a roof replacement, wiring update, plumbing update, or security installation

If you don't have your current policy in front of you, you're more likely to compare mismatched coverage and think you found savings when you stripped protection.

The apples-to-apples quote checklist

When we review quotes, we don't start with premium. We start with structure. Here's the checklist that matters most.

- Match dwelling coverage exactly. If one quote insures the home for less, it's not a fair comparison.

- Match liability limits. Lower liability can make a quote look better while exposing your assets.

- Match deductibles. A lower price can disappear once you notice the higher out-of-pocket cost.

- Ask about exclusions and endorsements. The cheapest quote may have tighter terms.

- Review the home characteristics entered into the application. Bad data creates bad quotes.

Shop for homeowners insurance the same way you'd compare mortgages. If the terms differ, the rate comparison is worthless.

This is the part homeowners usually skip because it takes effort. It's also the part that saves the most money over time.

Looking Beyond the Price Tag on Your Insurance Quote

A cheap quote can still be a bad deal.

The first number you should look at is the premium. It is not the last number you should care about. A policy has to hold up after a real loss, during repairs, and at the next renewal.

Cheap today can be expensive later

Post-claim affordability is one of the most overlooked parts of buying homeowners coverage. For North Carolina homeowners with a recent claim, the list of cheapest insurers changes sharply. In that group, Lititz Mutual and North Carolina Farm Bureau were both listed at $1,535 annually, while Travelers was listed at $2,285, according to NerdWallet's North Carolina homeowners insurance comparison for standard and post-claim scenarios.

That matters because the cheapest option before a claim may not be the cheapest after one. In some cases, it may not be your best long-term fit at all.

What to review before you say yes

Don't stop at the premium. Review the insurer's financial strength rating, read the policy for exclusions that matter to your home, and ask how claims are handled in practice. You want a company that can pay claims and a policy that won't surprise you when the damage is already done.

Use this short review list before you bind coverage:

- Financial strength so you're not betting your house on a weak carrier

- Claims handling reputation because service matters most when you're displaced or under stress

- Deductible structure especially if wind or storm losses are a concern for your property

- Renewal stability because a cheap first-year premium isn't helpful if it becomes painful after one loss

If you're trying to find the cheapest homeowners insurance in North Carolina, think beyond the first-year sticker price. The right policy is affordable now, realistic at claim time, and still workable after life gets messy.

If you want help running a true apples-to-apples comparison, Select Insurance Group, Inc. can review your current policy, match the important coverages, and help you compare real options without guessing from statewide averages.