Most homeowners can expect mobile home insurance cost to fall in a broad range of $700 to $1,500 per year. But that number can mislead you fast, because your actual price depends heavily on where the home sits, how it's built, and whether your policy pays on an actual cash value or replacement cost basis.

If you're shopping for coverage right now, you're probably seeing quotes that don't line up neatly. One looks affordable but thin. Another costs more, and it's not obvious whether you're buying better protection or just extra wording. That's where many mobile homeowners get stuck.

A mobile home policy isn't one fixed product with one fair price. It's more like choosing a toolbox. You can keep only the basics, or you can add the tools that matter most for your risks. In the Southeast, that difference matters even more. A home in inland Georgia doesn't face the same insurance math as a home near the Florida coast or in a storm-prone part of the Carolinas.

The smartest question usually isn't, "What's the cheapest policy?" It's, "What am I really getting for the money?" That shift changes how you read a quote, compare options, and decide what belongs in your budget.

Table of Contents

- Understanding Your Mobile Home Insurance Cost

- What Mobile Home Insurance Actually Covers

- Key Factors That Determine Your Mobile Home Insurance Cost

- How Much Does Mobile Home Insurance Cost A Look at Real Scenarios

- Smart Ways to Lower Your Mobile Home Insurance Cost

- Frequently Asked Questions About Mobile Home Insurance

- Get Your Fast Free Mobile Home Insurance Quote Today

Understanding Your Mobile Home Insurance Cost

If you've just bought a manufactured home, the first quote you get can feel oddly random. One carrier may price the home modestly, another may come in far higher, and both might be looking at the same address. That happens because insurers aren't only pricing the home. They're pricing the total loss picture.

A useful baseline is that major U.S. estimates for annual cost tend to cluster around $700 to $1,500, with other consumer-facing summaries placing the average around $750 to $1,600 or $800 to $2,000, depending on coverage assumptions and policy structure, as explained in this overview of mobile home insurance cost ranges and coverage assumptions.

That broad spread tells you something important. Insurance for a mobile home isn't a shelf item with a universal price tag. It's customized around risk.

Practical rule: Treat the national average like a map, not a quote.

Two homeowners can own homes with similar market value and still see different premiums. One may choose a lower-cost policy that pays for older items after depreciation. Another may choose stronger protection that costs more up front but leaves less financial pain after a loss.

The more helpful way to think about mobile home insurance cost is this:

| What affects price | Why it matters |

|---|---|

| Location | Storm, wind, hail, and other local hazards change the risk of a claim |

| Home condition | Older or less resilient homes can cost more to insure |

| Coverage design | Actual cash value, replacement cost, and optional endorsements change both premium and payout |

| Deductible and limits | What you keep versus what you transfer to the insurer changes the price |

If you're in the Southeast, this matters even more because weather exposure varies sharply from one ZIP code to the next. Coastal counties, high-wind zones, and areas with repeated severe storms don't price the same way as more sheltered inland areas.

A better quote comparison starts when you stop asking only, "How much is it?" and start asking, "What would this policy do for me if something bad happened?"

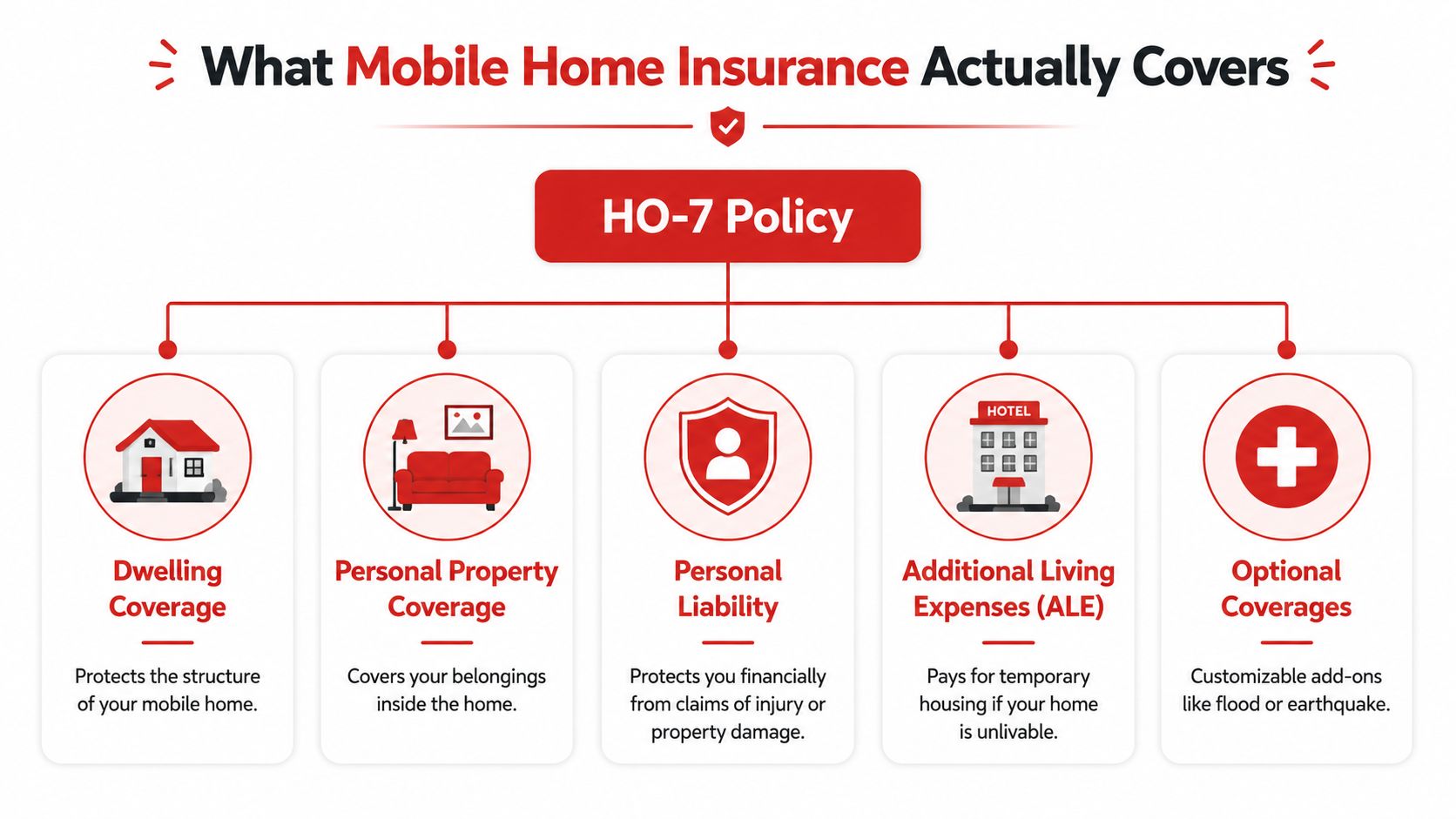

What Mobile Home Insurance Actually Covers

The HO-7 policy as a protection toolkit

Most mobile home insurance is written on an HO-7-style policy. Think of that policy like a protection toolkit. Each tool handles a different kind of problem.

One part protects the structure itself. That's the section that helps if the home is damaged by a covered peril. Another part covers your belongings inside, such as furniture, clothes, and electronics. There's also liability protection, which can help if someone is hurt on your property or if you accidentally cause damage to someone else's property. Many policies also include loss-of-use coverage, often called additional living expenses, which can help if a covered loss makes the home temporarily unlivable.

Policy design matters because HO-7 coverage usually includes structure, personal property, liability, and loss-of-use, but the payout basis can be actual cash value, replacement cost, or a stated amount, as outlined in this explanation of how mobile home insurance policy structure changes cost.

Here's a simple way to picture it:

- Dwelling coverage protects the home itself.

- Personal property coverage protects what's inside.

- Liability coverage protects your finances if someone brings a claim.

- Additional living expenses help with temporary housing after a covered loss.

- Optional endorsements fill gaps that a standard policy may leave open.

If you live in a wooded area, maintenance outside the home can matter too. Tree-related damage is a common point of confusion, and this guide on Preventing tree damage insurance issues is a useful companion if you're trying to understand where prevention ends and insurance begins.

Actual cash value vs replacement cost

Many shoppers make a decision at this stage without realizing how big it is.

Actual cash value, often shortened to ACV, pays after depreciation. Think about it like selling a used car. You may have paid much more when it was new, but its value today is lower because of age and wear. Insurance using ACV applies a similar idea to parts of your home and to your belongings.

Replacement cost, often shortened to RCV, aims to pay what it costs to repair or replace with new materials of like kind and quality, without subtracting depreciation in the same way.

A quick analogy helps. Suppose a storm destroys a ten-year-old recliner. Under ACV, the insurer may look at what that older chair was worth right before the loss. Under replacement cost, the payout is designed around what it takes to buy a comparable new one, subject to policy terms.

A cheap premium can feel great until you discover the claim payment was priced like a yard sale.

That doesn't mean ACV is always wrong. It may fit some budgets and some homes. But it often leaves owners of older mobile homes with a bigger out-of-pocket surprise after a serious loss.

What standard policies often leave out

Some homeowners assume a standard policy covers every big disaster that could hit the home. It usually doesn't.

Common gaps often include:

- Flood coverage, which is generally excluded from the standard policy

- Earthquake coverage, which often requires separate endorsement or separate coverage

- Sewer backup coverage, which may need to be added

- Transit exposure, because a standard policy often doesn't cover the home while it's being moved

That last point catches people off guard. Mobile homes are movable in theory, but that doesn't mean your regular insurance automatically follows the home during transport.

When you read a quote, don't just skim the premium. Check how the home and contents are valued, what perils are excluded, and whether any important local risk needs separate handling. That's often the difference between a policy that merely exists and one that works as intended.

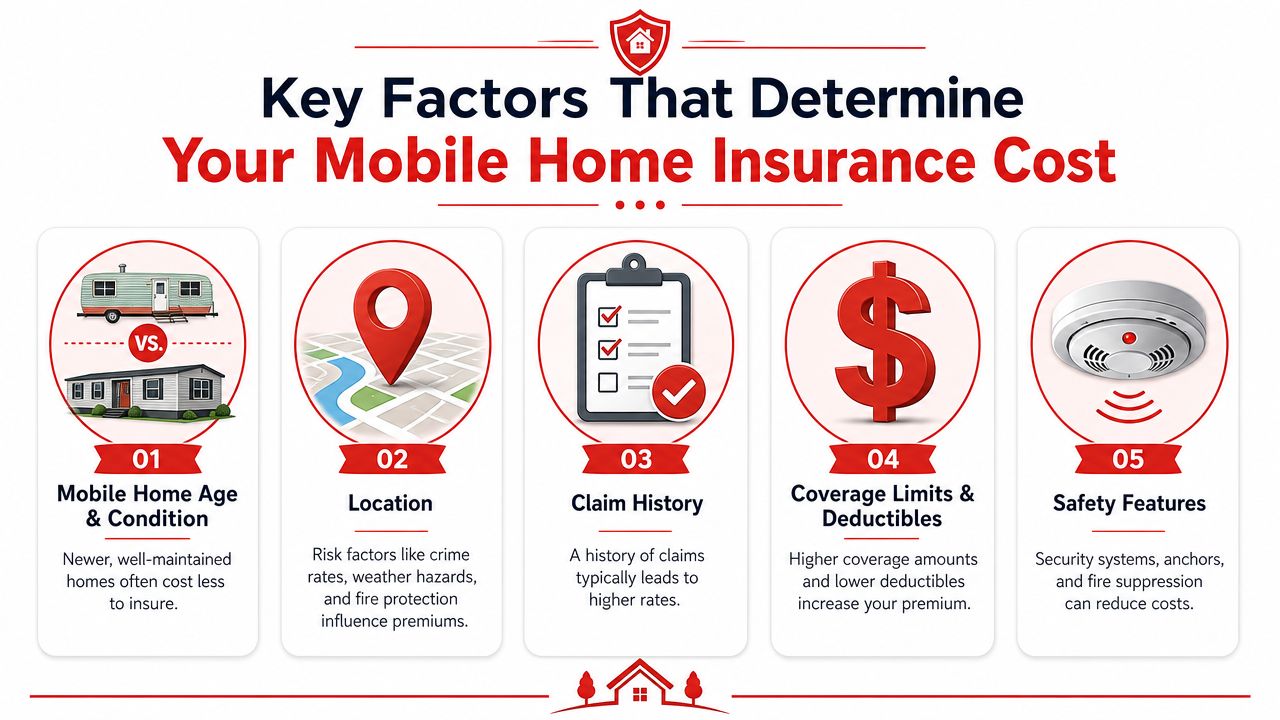

Key Factors That Determine Your Mobile Home Insurance Cost

Mobile home insurance is often priced around $700 to $2,000 per year, and one insurer is cited at an average of about $1,267 annually. That broad band reflects underwriting variables like location-specific catastrophe exposure, home age, replacement cost, coverage limits, deductible choice, and claims history, according to this review of mobile home insurance pricing factors.

The key word there is underwriting. Insurers are asking one question over and over in different ways: how likely is a loss here, and how costly would it be?

Location and catastrophe exposure

Location usually drives the biggest swings.

In the Southeast, a home near the coast can face a very different premium than one farther inland. Wind exposure, storm patterns, local building environment, and regional claim history all shape the quote. A carrier isn't only looking at your street address. It's looking at the hazard profile wrapped around that address.

For homeowners near the South Carolina coast, the difference between ordinary property risk and coastal wind exposure is significant. This overview of coastal home insurance in Charleston SC shows why coastal placement changes the insurance conversation.

A simple way to understand the insurer's logic is to ask, "If a severe storm hits this area, how vulnerable is this home compared with other homes?"

The home's age and physical condition

Older homes can cost more to insure because older materials, systems, and construction methods may create more claim risk. Condition matters just as much as age. A well-maintained older home may present a different risk than a poorly maintained one with deferred repairs.

Insurers often care about things like:

- Roof condition because roof failures often turn one problem into many

- Electrical and plumbing updates because outdated systems can raise fire or water-loss concerns

- Foundation and anchoring because physical stability matters in high wind

- General upkeep because visible wear can signal hidden loss exposure

A mobile home is also structurally different from many site-built homes. That can affect how it responds to wind, hail, and severe weather.

Coverage choices and deductible decisions

You control part of the price by deciding how much risk to keep and how much to transfer.

The biggest choices usually include:

| Choice | Lower premium version | Higher premium version | Main trade-off |

|---|---|---|---|

| Valuation | Actual cash value | Replacement cost | Lower upfront cost vs stronger claim payout |

| Deductible | Higher deductible | Lower deductible | More out of pocket after a loss vs more monthly or annual premium |

| Coverage limits | Lower limits | Higher limits | Less premium vs greater protection |

| Optional endorsements | Fewer add-ons | More add-ons | Simpler, cheaper policy vs broader protection |

Many people accidentally compare two unlike quotes. One quote may be cheaper because it insures less, excludes more, or pays on a more limited basis.

If one quote is far lower than the others, check the valuation method before you celebrate.

Claims history and personal risk profile

Insurers also look at your prior claims and broader risk profile. From their perspective, past claims can indicate future claim probability. That doesn't mean every claim hurts the same way, but it does mean your insurance history can influence the price.

This is one reason some homeowners feel frustrated when they haven't changed homes but still get a different quote from one renewal or application to the next. The insurer may be seeing updated information about prior losses, local risk, or how your profile fits its guidelines.

Safety features and risk reduction

Some upgrades make the home safer to live in and more attractive to insure. Carriers often view protective features as signs that the homeowner is reducing preventable loss.

Helpful features may include:

- Anchoring or tie-down improvements that help with wind resilience

- Smoke detectors and fire safety equipment that reduce fire severity

- Security systems that can help limit theft risk

- Maintenance upgrades that correct known trouble spots before they become claims

In practical terms, insurers reward homes that look less likely to generate avoidable losses. That's especially relevant in parts of Florida, Georgia, the Carolinas, and coastal-adjacent areas where weather can turn a small weakness into major damage.

How Much Does Mobile Home Insurance Cost A Look at Real Scenarios

Numbers become more useful when you attach them to real-life situations. The same home can price very differently depending on place, age, and policy structure.

Location-driven catastrophe risk can push cost well above the typical national range. In higher-risk states such as Florida and California, one consumer source reports average premiums around $1,800 a year, while Texas can run from $1,500 to $2,700 a year, as noted in this look at mobile home insurance costs in disaster-exposed markets.

Scenario one coastal Florida retiree

A retiree owns an older single-wide near the coast in Florida. The home is modest, but the exposure isn't. Wind risk is a major concern, and the owner is deciding between a cheaper ACV policy and a more protective replacement cost setup with broader add-ons.

This is the classic sticker-shock scenario. The homeowner expects the quote to match the home's age and modest value. Instead, the coastal location pulls the premium upward because the insurer is pricing the chance of a severe weather loss, not just the home's resale appeal.

If you're comparing manufactured home options in this market, a local page like manufactured home insurance in Kissimmee FL can help frame what insurers tend to focus on in Florida placements.

Scenario two suburban Georgia family

A young family buys a newer double-wide in suburban Georgia. The home has updated systems, solid upkeep, and useful safety features. The area still gets storms, but it doesn't carry the same coastal exposure as parts of Florida or the Carolinas.

This homeowner may still see a meaningful premium, but the overall risk profile is more balanced. The family might choose replacement cost because they want the policy to help them rebuild their daily life, not just reimburse depreciated value after a major loss. That choice usually costs more up front, yet it often makes the quote easier to live with emotionally because the protection is clearer.

For families who also own an RV or travel trailer, it's worth noticing how insurance pricing changes when the property can move and is used differently. This breakdown from Motor Sportsland's RV insurance guide helps show how use, movement, and exposure can change the risk logic across different policy types.

Scenario three rural Tennessee homeowner

A homeowner in rural Tennessee owns a mid-range manufactured home in a scenic area with trees and uneven weather. The risk picture is different here. Coastal wind isn't the main concern, but storms, debris, and property-specific hazards may matter more.

The quote may land closer to the broad national range if the home's condition is good and the insurer sees manageable risk. But choices still matter. A lower premium ACV quote may look attractive until the homeowner thinks through a total-loss situation and realizes depreciation could leave a large gap.

These examples point to the same lesson. A quote isn't only a price. It's a prediction about risk plus a promise about how the claim will be valued if something goes wrong.

Smart Ways to Lower Your Mobile Home Insurance Cost

Lowering your premium doesn't have to mean stripping away protection. The best savings usually come from making the home less risky and the policy more intentional.

Change the policy without gutting protection

Start with the levers that affect price directly.

- Raise the deductible carefully. A higher deductible can lower premium, but only if you can comfortably handle that out-of-pocket cost after a claim.

- Review your coverage limits. Make sure the policy reflects what you need to protect. Overinsuring and underinsuring both create problems.

- Ask how your belongings are valued. This isn't about chasing the lowest number. It's about understanding what you're giving up if you switch to a cheaper valuation method.

Make the home less risky to insure

Carriers tend to favor homes that show attention to prevention.

Some practical improvements include:

- Upgrade critical systems if electrical, plumbing, or roofing issues are present

- Add protective devices such as smoke detectors, security features, and other loss-reduction measures

- Improve wind readiness where appropriate, especially in storm-prone Southeastern areas

- Stay ahead of maintenance so small issues don't become claim-sized issues

A home that is easier to defend from fire, theft, and weather is often easier to insure at a better value.

Good insurance pricing often starts with boring home maintenance.

Review the policy like a homeowner not a shopper

The best annual habit is a plain-language policy review. Don't only ask whether your premium changed. Ask whether the policy still matches the home you live in now.

Use a quick checklist:

| Review item | What to ask |

|---|---|

| Home updates | Did you improve the roof, systems, or safety features? |

| Coverage basis | Are you still comfortable with ACV, or do you want replacement cost? |

| Belongings | Have your contents changed enough to revisit limits? |

| Exclusions | Do you need to revisit flood or other add-ons based on your area? |

The goal isn't to buy more every year. It's to avoid paying for the wrong thing while staying protected where losses would hurt most.

Frequently Asked Questions About Mobile Home Insurance

Some questions only come up after you've looked at a few quotes and noticed how different they can be. These are the points that deserve a slower, more practical answer.

A good example is this question: Is the cheapest premium the best value for a manufactured home, especially if a loss is total or if the home is older? That trade-off matters because manufactured homes are often more expensive to insure than site-built homes due to higher wind, hail, theft, and disaster exposure, and the gap between lower premiums and underinsurance risk is especially important, as discussed in this guide to mobile home insurance value versus price.

Is replacement cost worth it on an older mobile home

Sometimes yes, sometimes no.

If you own an older home and your budget is tight, ACV may seem like the only realistic option. But the older the home, the more depreciation can affect a claim. That means the cheaper premium can produce a much smaller payout than you expected after a serious loss.

A useful question is not "Is replacement cost more expensive?" It usually is. The better question is "Could I handle the gap if the claim payment reflects age and wear instead of today's rebuild or replacement reality?"

Does mobile home insurance cover the home while it's being moved

Often, standard coverage does not automatically cover transit exposure. That's one of the most misunderstood gaps in mobile home insurance.

If a move is planned, ask directly about transport-related risk before the move happens. Don't assume the existing policy follows the home just because the home can be relocated.

Why can a quote come in much higher than expected

Usually because the insurer sees a risk layer you weren't focusing on.

That layer might be storm exposure, the home's age, a prior claims issue, or a policy design choice that improves the claim payout. Many homeowners compare quotes by premium first, but insurers compare them by expected claim cost first. Those are two very different views of the same policy.

Is the cheapest premium actually the best value

Often, no.

If the lower quote relies on heavier depreciation, smaller limits, or more exclusions, it may only be cheaper because it promises less when you need it most. That doesn't make it worthless. It just means a proper comparison should include the claim experience, not only the bill.

For homeowners who want to prepare for the claim side of things before anything bad happens, this article with expert tips for Phoenix homeowners offers a practical look at documentation and claim handling habits that can help in any market.

Buy the policy you can still live with after a loss, not just the one you can live with before one.

Get Your Fast Free Mobile Home Insurance Quote Today

By now, the big idea should be clear. Mobile home insurance cost is never just a price question. It's a value question. The premium reflects your home's location, condition, and risk profile, but it also reflects the kind of recovery the policy is built to support.

That matters a lot in the Southeast, where storm patterns, wind exposure, and local underwriting rules can make one quote look very different from another. A lower number isn't automatically better, and a higher number isn't automatically overpriced. The right policy is the one that fits your home, your budget, and the way you want a future claim handled.

If you want help sorting through those trade-offs, it helps to work with an independent agency that can compare multiple options instead of pushing one standard answer. That gives you a better chance of seeing how coverage structure changes the quote, not just how the premium changes.

For homeowners in Alabama, Florida, Georgia, North Carolina, South Carolina, Tennessee, and Virginia, getting a personalized quote is the practical next step. You can start with a simple request through Select Insurance Group's quote page and compare options based on the protection you want.

A good quote review should answer plain questions. What does this policy cover? How does it value my home and belongings? Which risks are excluded? What would I likely pay out of pocket after a claim? Those answers matter more than any national average.

If you're ready to compare coverage with a local independent agency, contact Select Insurance Group, Inc.. Their team serves homeowners across the Southeast and can help you review mobile home insurance options, understand coverage trade-offs, and request a fast, free quote with no obligation.