If you own a manufactured home in Kissimmee, you're probably dealing with the same two frustrations most local owners bring up first. The renewal jumped, and the quote options feel thin. You call one familiar national brand, they don't write it. You call another, same answer. Then hurricane season gets closer and the pressure rises.

That's not your imagination. Manufactured home insurance Kissimmee FL is a tighter, more specialized market than standard homeowners coverage. The rules are different, the underwriting is stricter, and older homes in established parks often run into the hardest roadblocks.

Protecting Your Kissimmee Home in 2026

A common situation looks like this. A homeowner in Kissimmee gets a renewal packet, sees a higher premium, and wonders whether shopping the policy will even help. Then they learn the market is smaller than they thought.

Florida's manufactured home insurance market is highly concentrated, with the largest five insurers providing 78% of all mobile home insurance policies, and major national carriers such as State Farm, Allstate, and Progressive do not offer these policies in Florida, according to Florida mobile home insurance market data. That explains why shopping can feel frustrating. There aren't as many viable carriers for this type of property.

Why Kissimmee owners feel squeezed

Kissimmee sits in a part of Central Florida where people sometimes assume inland means lower concern. Insurance companies don't look at it that straightforwardly. They still evaluate wind exposure, storm patterns, age of the home, tie-downs, roof condition, prior claims, and whether the property fits a narrow underwriting box.

Older homes in long-established parks face the most pressure. If your home is older, has updates that weren't documented well, or falls outside the build years many carriers prefer, you can spend a lot of time chasing quotes that go nowhere.

Practical rule: If you own an older manufactured home in Kissimmee, don't assume a declined quote means the home is uninsurable. It usually means that specific carrier doesn't like that risk profile.

What usually works and what doesn't

A few things usually don't work. Calling only one direct writer. Comparing price without checking settlement terms. Waiting until the last minute when the current policy is about to expire.

What does work is getting clear on the home's age, condition, roof details, and prior updates before you shop. In this market, the quality of the information matters almost as much as the home itself.

That's the practical side of manufactured home insurance Kissimmee FL. It isn't just about finding a cheap number. It's about finding a carrier that will accept the home, write usable coverage, and still be there when a claim happens.

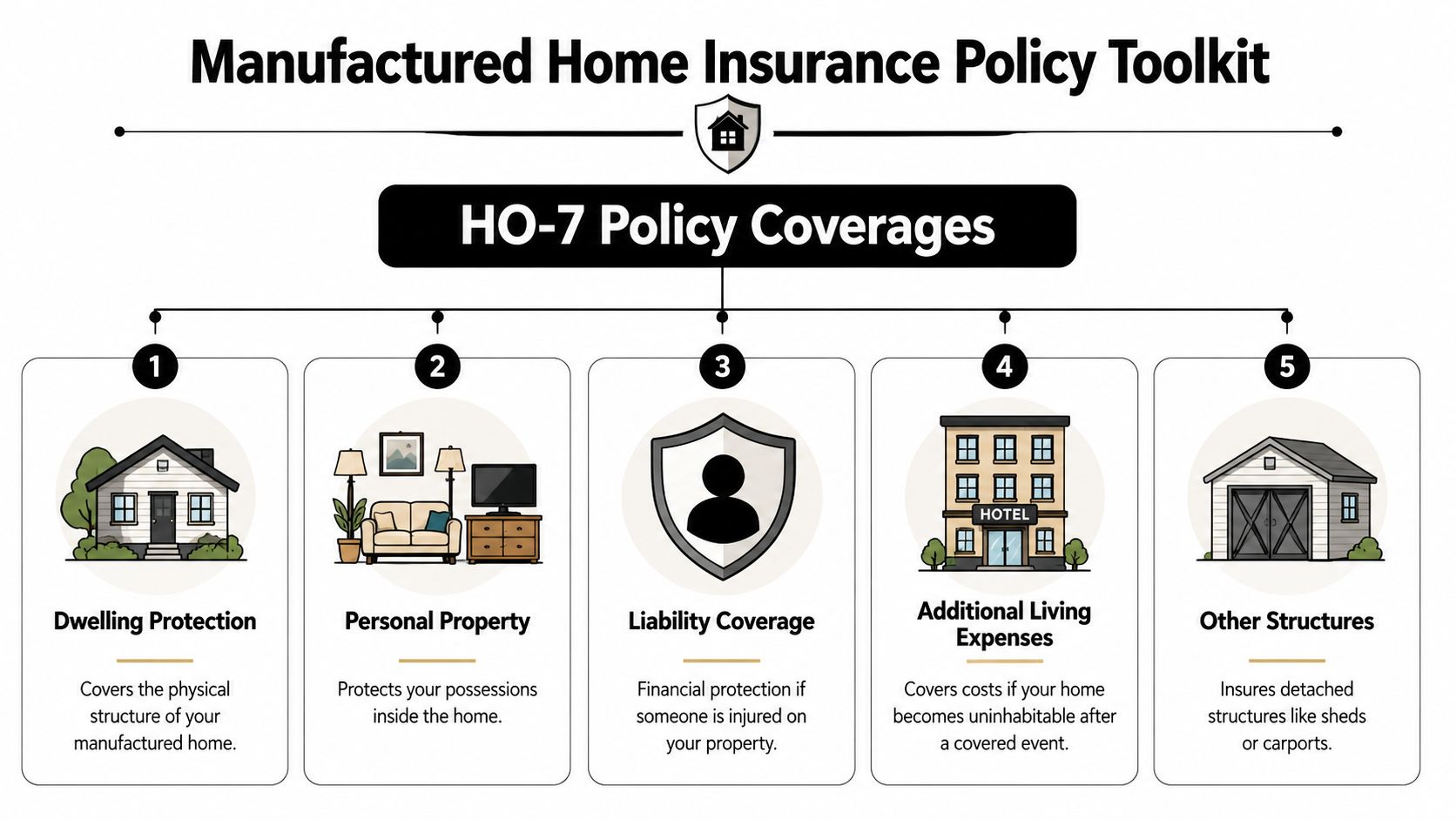

What Manufactured Home Insurance Actually Covers

Manufactured home insurance in Kissimmee typically uses an HO-7 policy, not the standard policy form many site-built homeowners carry. According to consumer guidance on Florida manufactured home coverage, the HO-7 structure includes five core coverages, and annual premiums can range from $900–$1,754 based on factors like age, size, claims history, and geographic risk.

Think of an HO-7 as a practical toolkit. Each part handles a different type of loss. If one tool is missing, the policy may look affordable on paper but leave you exposed where it hurts most.

The five core coverages

Dwelling coverage protects the physical structure of the manufactured home itself. If a covered loss damages the roof, walls, attached components, or major built-in parts of the home, this is the section that responds.

Personal property coverage helps with your belongings inside the home. Furniture, clothing, electronics, and household items usually fall here, subject to policy terms and limits.

Liability coverage matters more than many owners realize. If a guest gets hurt on the property and you're legally responsible, liability coverage can help with the financial side of that claim.

Loss of use helps when a covered loss makes the home unlivable and you need temporary living arrangements. This can be one of the most valuable parts of the policy after serious damage.

Other structures coverage applies to detached items such as certain sheds or similar structures, if they qualify under the policy.

Why HO-7 is different from a standard homeowners policy

A site-built house and a manufactured home don't present the same underwriting issues. Manufactured homes have their own construction and risk profile, so insurers use a different policy form and different pricing logic. That's why comparing an HO-7 quote to a traditional homeowners quote without looking at the form itself can lead to bad decisions.

One policy can look cheaper because it strips down coverage, changes settlement terms, or narrows what's insured.

A low premium only helps if the claim payment still makes sense after a loss.

ACV versus replacement cost

Many buyers are often surprised. Some policies settle losses on actual cash value, often shortened to ACV. That means depreciation gets deducted. Older roofs, older flooring, older cabinets, and older contents can all reduce the payout.

Replacement cost works differently. It aims to pay based on the cost to repair or replace covered property without the same depreciation treatment, subject to the policy's terms and limits. For many manufactured homeowners, this is the difference between a claim that helps and a claim that still leaves a major out-of-pocket burden.

Here's the cleanest way to think about it:

| Coverage question | ACV approach | Replacement cost approach |

|---|---|---|

| Older materials | Depreciation reduces payment | Less depreciation impact under covered terms |

| Out-of-pocket cost | Often higher | Often lower |

| Upfront premium | Usually lower | Usually higher |

If you're reviewing quotes, don't stop at the annual premium. Ask how the home is valued, how contents are settled, and whether the carrier offers replacement cost options for your property type and age.

Florida Risks That Drive Your Insurance Needs

Kissimmee owners don't deal with coastal exposure the same way a beach community does, but inland doesn't mean low-risk. It means the risk shows up differently. Wind, water, and the age of the home all shape what coverage you can buy and how the deductible works.

Inland hurricane risk is still real

Kissimmee's location in Central Florida's hurricane corridor matters. Public guidance specific to manufactured home insurance notes that standard policies often apply hurricane deductibles of 2–5% of home value for manufactured homes, and carrier appetite and pricing in Kissimmee have shifted after recent hurricane seasons, according to Florida manufactured home hurricane coverage guidance.

That deductible issue catches a lot of owners off guard. They focus on premium and miss the storm deductible until claim time. On a manufactured home, that deductible can change what a realistic out-of-pocket loss looks like after a named storm.

Flood risk is a separate conversation

Wind and flood are not the same problem. Many owners use the word “hurricane” to cover everything, but insurance doesn't. Wind damage may fall under the home policy if it's covered. Flood damage generally follows separate rules.

For some owners, especially those with lender requirements or certain carrier arrangements, flood insurance becomes part of the actual cost of protecting the home. If you're in a lower-lying area, near water, or in a location where the lender requires it, skipping that conversation is a mistake.

Older homes change the risk picture

In Kissimmee's established parks, older homes often create a second layer of difficulty. The issue isn't just whether the home can be insured. It's whether the roof, electrical system, plumbing, HVAC, tie-downs, and overall condition fit a carrier's current appetite.

A newer home with documented upgrades usually gets a smoother review. An older home with unclear updates often runs into more questions, more inspections, and fewer offers.

The same park can have two homes side by side with very different insurability. One has updated systems and paperwork. The other doesn't.

What owners should check before shopping

A strong quote starts with the right facts. Before you apply, verify:

- Roof details including age, material, and any replacement records

- Wind features such as shutters, roof-to-wall connections, and tie-down improvements

- Flood exposure based on your property location and lender requirements

- System updates for electrical, plumbing, and HVAC, especially on older homes

If you don't know those answers yet, get them first. In Manufactured home insurance Kissimmee FL, vague information usually leads to higher pricing, fewer options, or both.

Decoding the Cost of Your Policy and Finding Discounts

A common initial question is: What's this going to cost me? In Florida, manufactured home insurance is usually expensive enough that the answer affects whether someone keeps broad coverage, raises a deductible, or starts trimming parts of the policy.

According to Florida mobile home insurance pricing data, average annual premiums range from $900 to $1,400, and manufactured home coverage can cost 2.5 to 4 times more than standard homeowners insurance because of the structural vulnerabilities and weather risk tied to these homes.

Why the premium feels high

Manufactured homes aren't priced like a standard house because the exposure isn't the same. Construction method, transportability, foundation differences, weather sensitivity, and repair complexity all affect how an insurer sees the risk.

That doesn't mean every quote is inflated. It means every quote needs context. A higher premium may include better protection. A lower premium may come with a tougher deductible, actual cash value settlement, or tighter limits.

Where owners can still save

You usually won't save money by guessing. You save by making the home easier to underwrite and by comparing carriers that look at the same risk differently.

Here are the discount and savings levers worth checking:

- Wind mitigation features can help if the home has qualifying protective features and the paperwork to prove them.

- Higher deductibles can lower premium, but only choose a deductible you can realistically handle after a loss.

- Updated systems often improve insurability. Carriers pay attention to roof age, electrical updates, plumbing condition, and HVAC.

- Clean claims history matters. Even when you can't change the past, a carrier may price a home differently based on prior loss activity.

- Accurate valuation helps avoid overinsuring or underinsuring the home.

The quote comparison mistake I see most

Many homeowners compare only the annual premium line. That approach is too narrow. You need to compare what the policy does.

Use this simple review grid when you look at options:

| What to compare | Why it matters |

|---|---|

| Settlement type | ACV and replacement cost can produce very different claim results |

| Hurricane deductible | This changes your out-of-pocket exposure after a storm |

| Wind inclusion | Some owners assume wind is included without confirming |

| Personal property limit | Low contents limits can leave you short after a major loss |

If you want help reading those forms before you commit, the Restore Heroes guide to insurance policies gives a practical overview of how to read a homeowners policy without getting lost in the wording.

The biggest lever is still carrier access

In a narrow market, savings often come from getting the home in front of more than one carrier that writes manufactured homes. That's where an independent agency can make a difference. Select Insurance Group, Inc. compares quotes from 20–40 carriers and that broader market view can help when one company prices an older or more complex risk too aggressively.

The Step-by-Step Process to Get Covered in Kissimmee

Shopping gets easier when you treat it like a file-building exercise instead of a phone scramble. The cleaner your documents and property details, the better your odds of getting a workable quote.

This matters even more in Kissimmee's older parks. Most local agencies specialize in owner-occupied manufactured homes built between 1994–2023, which creates a coverage gap for homes built before 1994 or pre-1976 units that face stricter underwriting, according to Foremost mobile home eligibility guidance.

Step one, gather the home details first

Before you ask for quotes, collect the basics:

- Year built and home type. This is the first filter. Older homes often move into a narrower set of carriers.

- Ownership documents. Have proof that you own the home and know whether the land is owned or leased.

- Address and occupancy details. Owner-occupied, seasonal, rental, and vacant risks are treated differently.

- Update records. Roof work, electrical updates, plumbing replacements, and HVAC changes can all matter.

If you don't have paperwork for improvements, try to get it. Underwriters trust documentation more than verbal descriptions.

Step two, expect inspection questions on older homes

Older manufactured homes often need closer review. A carrier may ask for information that looks similar to what site-built homeowners see, but the stakes are often higher because the acceptable risk window is tighter.

Common requests can include:

- Roof condition information

- Electrical details

- Plumbing type and condition

- Heating and cooling information

- Tie-down or anchoring details

- Photos of the home, skirting, and exterior

If your home is older, don't wait for the insurer to ask what was updated. Lead with it.

Step three, prepare for storm-season underwriting

If you're shopping close to hurricane season, move early. Some carriers tighten guidelines when storm activity ramps up. Even if the home qualifies, timing can affect whether a carrier is still writing new business in that window.

That's also the right moment to prepare the property itself. For a practical homeowner checklist, the preparing your home for a hurricane resource from LuminAID is useful because it focuses on actions owners can take before a storm is on the radar.

Step four, handle older-home roadblocks directly

If your home was built before the years most agencies prefer, don't waste time asking only, “Can you insure it?” Ask better questions:

- Which carriers will still review older owner-occupied homes?

- Will they require actual cash value settlement?

- Do they want recent updates before binding coverage?

- Will a roof issue stop the quote, or just change terms?

That last point matters. Some issues kill a quote. Others change the deductible, pricing, or available options.

Step five, review the final quote like a claim would happen tomorrow

Before you bind anything, read the practical pieces. What's covered for wind? What's the hurricane deductible? How are contents settled? Is the home insured the way you expected?

The fastest way to regret a policy is to buy it as if it were a bill instead of a contract.

Get Your Free Bilingual Quote from a Local Expert

By the time most Kissimmee owners start searching, they're already tired of vague answers. They've heard broad Florida advice that doesn't address an older home in an established park, a tricky roof history, or a carrier that won't touch certain build years.

That's why local context matters so much in Manufactured home insurance Kissimmee FL. The primary challenge usually isn't understanding that storms happen in Florida. It's finding a policy that fits the actual home, the actual park, and the actual underwriting rules in front of you right now.

What smart buyers do differently

They don't assume every quote is built the same. They ask better questions. They look at deductible structure, settlement type, eligibility, and whether the carrier is comfortable with the home's age and condition.

They also understand what an independent agency does differently. If you want a plain-English explanation, this short article on what is an independent insurance agency lays out why access to multiple carriers matters when your property doesn't fit a one-size-fits-all box.

Why bilingual local help matters in Kissimmee

Kissimmee is a diverse market, and insurance gets confusing fast when policy language, inspection requests, and underwriting conditions start piling up. Being able to ask questions in English or Spanish matters. It reduces mistakes, clears up expectations, and helps owners make decisions based on coverage instead of guesswork.

The other advantage is speed. In a tighter market, delays can cost you options. A home that needs extra documentation or falls into an older-home category benefits from quicker communication and cleaner submission details.

Good insurance advice is often simple. Bring the right documents, ask the right coverage questions, and don't wait until your policy is about to lapse.

If your home has been hard to place, if your renewal got ugly, or if you just want someone to review whether the quote in front of you provides real protection, getting local help is usually the shortest path to clarity.

Need help with Manufactured home insurance Kissimmee FL? Select Insurance Group, Inc. can provide a fast, free, no-obligation quote, compare options across 20–40 carriers, and connect you with bilingual specialists backed by over 30 years of local experience in Central Florida.