You bought the cabin for the mornings. Fog lifting off the ridgeline. Coffee on the deck. A stone fireplace that makes every long weekend feel earned.

Then the insurance questions start, and the easy part ends.

You might use the place yourself most of the year, let family stay there over holidays, and rent it out on a few peak weekends to help cover costs. That sounds simple. On an insurance application, it usually isn't. In the Blue Ridge market, the line between second home, vacation home, and short-term rental gets blurry fast, and that's where expensive mistakes happen.

A mountain property that sits empty for stretches doesn't behave like your primary home. A cabin that earns rental income doesn't fit neatly inside a standard second-home policy. A house that does both needs even closer review. That's why Secondary residence insurance Blue Ridge Mountains isn't just about finding a policy. It's about matching the policy to how the property is used.

Your Blue Ridge Cabin Dream and Its Insurance Reality

A common Blue Ridge scenario goes like this. You buy the cabin for personal use, stock the kitchen, add a smart lock, and plan to enjoy it with family. Then leaf season approaches, a friend asks for the booking link, and you decide to rent a few weekends to offset expenses. That decision can change the insurance answer faster than many owners expect.

While it may feel casual and low risk, underwriters treat that shift as a material change in use. A cabin that is owner-occupied part of the time, vacant part of the time, and rented to paying guests on select dates does not fit neatly into the same box as a pure second home.

That gray area causes trouble. Owners often describe the property as a vacation home because that is how they see it. The carrier reviews who stays there, how often it sits empty, whether money changes hands, and whether a guest injury or a canceled booking could create a claim that a standard second-home form was never built to handle. For a plain-language overview of baseline homeowners insurance categories, the Pinnacle Property Media homeowner insurance guide is a useful starting point.

The mistake usually happens before the claim.

An owner accepts a few short-term bookings, lets unrelated guests use the property, or leaves the cabin unoccupied between visits for long stretches. Those facts can trigger different underwriting rules, different liability expectations, and different questions about loss of rental income. If the policy was written for personal secondary use only, the gap may not show up until water damage, a guest fall, or a fire forces the issue.

Where owners get tripped up

These are the problem areas I see most often with mountain cabins:

- Mixed-use confusion: The owner uses the home personally, so they assume all rental activity is incidental.

- Limited-booking assumptions: A handful of peak-season rentals still counts as rental use to many carriers.

- Vacancy exposure: A leak or storm loss can get worse when no one checks the property for days or weeks.

- Label-based buying: Policy names sound broad, but the actual form may leave out business-liability or rental-income protection.

A Blue Ridge cabin can be a retreat, an investment, or both. Insurance has to be written for the actual pattern of use, not the original plan you had at closing.

Understanding Secondary Residence Insurance

A Blue Ridge owner closes on a cabin for family weekends, then lists a few peak foliage dates to offset costs. That single change can put the property in a different insurance category, even if the house still feels like a personal retreat.

That is why secondary residence insurance needs a closer read than many owners expect.

What this policy is actually built for

Secondary residence insurance is usually written for a home you own and use personally, but do not live in full time. Typical examples include a weekend cabin, a seasonal mountain house, or a property you keep for family use during part of the year. Carriers focus on how often the home sits empty, who uses it, and whether anyone is paying to stay there.

That last point causes trouble in the Blue Ridge market. Owners often treat occasional short-term rental income as a small side use, while the carrier may treat paying guests as a business exposure. Once money changes hands, liability, property damage, and loss-of-income questions start to look different from a pure second-home risk. A policy can still say "secondary residence" on the paperwork and leave the owner exposed if the actual use includes guest turnover, rental income, or periods of no occupancy between bookings.

If you want a basic overview of how home insurance categories fit together before comparing mountain-specific options, the Pinnacle Property Media homeowner insurance guide is a useful starting point.

Two terms worth understanding

These two policy terms shape how a claim gets handled:

| Term | Plain-English meaning | Why it matters for a mountain second home |

|---|---|---|

| Named peril | The policy covers only causes of loss specifically listed | If the source of damage is not listed, the claim may be denied |

| Open peril | The policy covers causes of loss unless they're specifically excluded | You still have to read the exclusions closely, especially for rental activity, water, and vacancy-related limits |

I tell cabin owners to read this part with one question in mind. What happens if the home is empty for stretches, then occupied by guests, then empty again?

Where the classification starts to shift

A true second-home policy usually works for a cabin used only by the owner, relatives, and unpaid guests. Problems start when the use pattern changes but the policy does not.

A few examples:

- Personal-use only: Usually fits a second-home policy.

- A handful of paid weekend bookings: Often triggers underwriting questions many owners never asked at purchase.

- Regular Airbnb or Vrbo use: Usually needs a rental-focused policy structure or a carrier that clearly accepts mixed use.

- Personal use plus seasonal rentals: This is the gray area where coverage mistakes happen most often.

The practical issue is not the title of the policy. The practical issue is whether the carrier agreed to the actual occupancy, guest use, and income activity at the cabin.

That distinction matters more in the Blue Ridge Mountains because so many owners move back and forth between private retreat and short-term rental without updating their insurance until after a claim.

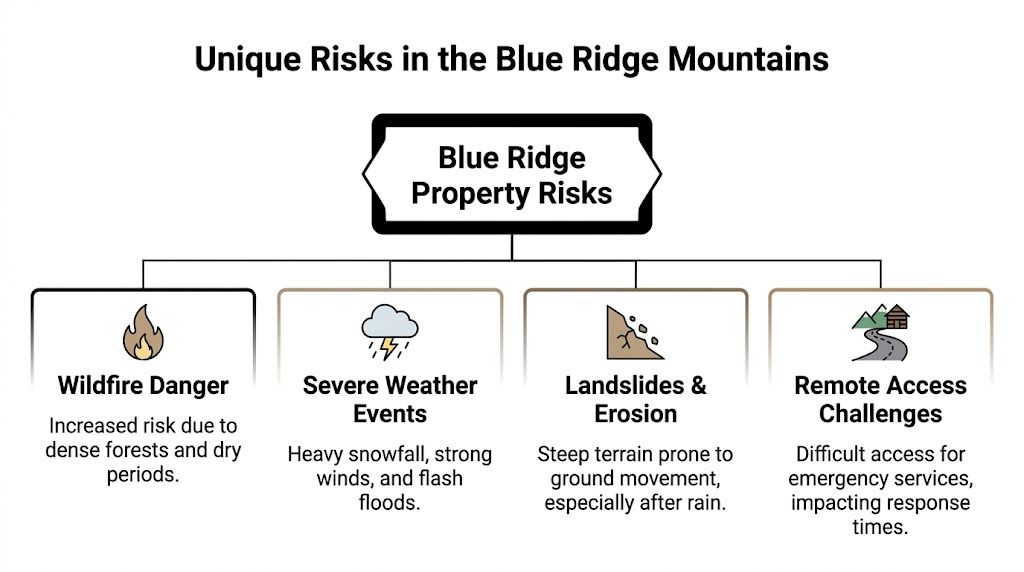

Special Insurance Risks in the Blue Ridge Mountains

A Blue Ridge cabin can sit empty for two weeks, take a hard rain through a lifted shingle, and then open its doors to weekend guests before anyone realizes water has been working behind the wall. That is a different insurance problem than a primary home with daily occupancy. It is also why mountain properties get closer scrutiny in underwriting.

Vacancy affects claims long before it affects maintenance

Carriers treat extended vacancy as a pricing and claims issue because small losses often turn into expensive ones when no one is there to catch them early. In the Blue Ridge, that usually means water, storm damage, frozen pipes, theft, or vandalism that sits undiscovered until the next visit, cleaner check, or guest arrival.

The point owners miss is timing.

If the cabin is empty most weekdays, owner-occupied on some weekends, and rented during peak leaf or ski season, the property still has long periods where damage can spread unnoticed. That use pattern matters even before the short-term rental question comes up, because the insurer is looking at response time, condition checks, and how fast mitigation starts after a loss.

Some carriers ask for more detail than owners expect. They want to know how often the home is inspected, whether there are leak sensors or low-temperature alarms, and how winterization is handled if the house is vacant in cold weather. Those answers can affect pricing, eligibility, and the carrier's comfort level with mixed personal and guest use.

Weather losses get more expensive in the mountains

Blue Ridge weather creates a lot of delayed-loss claims. Wind lifts roofing. Ice backs up at the eaves. Heavy rain finds flashing failures and drainage problems. A downed branch breaks a window or punches a small opening in the roof. If no one gets there quickly, the first loss becomes a second and third loss.

That sequence is what carriers focus on.

From an underwriting standpoint, mountain weather is tied to occupancy. A storm at a full-time residence may lead to a same-day tarp, plumber call, or water shutoff. The same storm at a cabin an hour or two away can sit for days, especially if the road is steep, muddy, or blocked by debris.

Common trouble spots include:

- Ice and snow: frozen plumbing, roof stress, ice damming, and delays getting repair crews on site

- Wind-driven rain: water intrusion through small openings that keeps spreading while the home is empty

- Power outages: failed heat, failed sump or well systems, and no immediate notice unless remote monitoring is installed

- Post-storm access problems: owners, cleaners, and contractors cannot reach the cabin fast enough to limit damage

A mountain claim often gets expensive because of delay, not because the original event was catastrophic.

Wooded lots raise fire and liability concerns

Tree cover, privacy, and seclusion are part of the appeal in the Blue Ridge. They also change how an insurer looks at the property. Carriers often evaluate defensible space, roof condition, brush near the structure, and whether emergency vehicles can get in and out without losing time.

That matters for more than wildfire.

Falling limbs, blocked driveways, and poor visibility on narrow roads all increase the chance of property damage or injury. If guests, contractors, or delivery drivers use the property, access conditions can become part of a liability claim. Owners who use the cabin personally may accept a steep gravel drive or uneven stone steps. A paying guest who slips on those same steps creates a different claim environment, even if the house is only rented a few weekends a year.

Steep terrain makes rebuilding harder and sometimes more expensive

Slope changes the repair math after a loss. Debris removal can require specialized equipment. Foundation and drainage issues may show up once crews start demolition. Retaining walls, narrow mountain roads, and limited staging space can slow a project before reconstruction even begins.

Replacement cost estimates are often where owners feel this gap. A policy that looked adequate on paper can come up short if site access, hauling, and hillside work drive the rebuild higher than expected. Mountain homes also tend to have features that cost more to replace, including large decks, custom windows, stonework, and long private drives.

A simple comparison helps:

| Risk category | What owners focus on | What carriers focus on |

|---|---|---|

| Vacancy | Time between visits | How long damage can go undetected |

| Weather | The storm itself | Secondary damage before mitigation starts |

| Wooded setting | Privacy and views | Fire spread, falling trees, and emergency access |

| Terrain | Seclusion and slope | Rebuild logistics, drainage, and repair cost |

This is why I tell Blue Ridge owners to insure the actual use and actual setting of the cabin. The weak point is often not one major hazard. It is the combination of vacancy, weather, difficult access, and occasional guest occupancy that pushes a standard second-home setup past what it was built to cover.

When Your Cabin Becomes a Business Rental Coverage

The biggest insurance mistake I see with Blue Ridge cabins is owners treating rental use like a side note. They'll say, “It's mostly for us,” then mention the property is on Airbnb for peak weekends, Christmas, and a few summer stretches. From the carrier's perspective, that detail can be the whole story.

Once you accept paying guests, the house stops being only a personal retreat.

Why occasional renting still changes the risk

A guest doesn't use your cabin the way you do. They don't know which door sticks in damp weather. They may overload parking areas, use fireplaces incorrectly, bring extra visitors, or report damage after it has already spread. Liability changes too, because guest injury claims are different from a friend slipping while visiting informally.

That's why the line between personal use and business use matters so much. Standard second-home coverage often isn't built for the commercial exposure created by short-term rentals.

In mountain markets, insurers are tightening underwriting around short-term rentals, and homeowners often don't realize that unreported Airbnb or VRBO activity can lead to claim denials or policy cancellation, as explained in this North Carolina second-home insurance discussion of short-term rental underwriting.

The blurry line owners need to take seriously

The hardest part is that there isn't one universal line that works the same way with every carrier. Some owners want a simple answer like, “If I rent it only a few times, I'm safe under a second-home policy.” Insurance doesn't work that neatly.

What matters is disclosure and policy form. Carriers may ask:

- How often is the home rented

- Whether guests are booked through platforms

- If rental income is being generated

- Whether the property is owner-occupied part of the year

- How the home is managed between guest stays

If your current policy was written around personal use and you later add rental activity without updating the carrier, you've created a coverage problem before any claim is filed.

What owners should do instead

Don't try to outguess how much rental activity is “too much.” Ask for the carrier's position in writing.

Use this framework:

Be exact about use

Tell the agent whether the cabin is never rented, occasionally rented, or actively booked.Disclose platform activity

If the property appears on Airbnb, VRBO, or a local vacation-rental site, say so.Ask whether the policy contemplates income loss and guest liability

If it doesn't, keep digging.

If the cabin earns money, the insurance needs to acknowledge that fact directly. Silence is not protection.

Owners usually don't get into trouble because they intended to hide something. They get into trouble because they thought “just a few rentals” wouldn't count. In the Blue Ridge short-term rental market, that assumption is where claims start to unravel.

Essential Coverages and Endorsements for Your Policy

A solid mountain-home policy isn't defined by the base form alone. It's defined by the details that deal with how Blue Ridge cabins are used. The best coverage setup usually connects directly to the property's occupancy pattern, location, and rental exposure.

The easiest way to judge a policy is to ask what problem each coverage solves.

Coverages that do real work for mountain properties

Start with the basics, but don't stop there.

- Dwelling coverage: This is the core protection for the structure itself. For mountain homes, the important question isn't whether you have it. It's whether the limit reflects what it would take to rebuild a cabin in a more difficult location.

- Liability coverage: This matters whether you use the property personally or allow others to stay there. It becomes more important the moment guests, service providers, or renters use the property.

- Contents coverage: Many Blue Ridge cabins are furnished and ready to use. That means the furniture, appliances, décor, cookware, electronics, and linens inside the home deserve more attention than owners often give them.

Endorsements worth discussing line by line

A good review with an agent should include optional protections and restrictions, not just price.

| Coverage or endorsement | Why it matters for a Blue Ridge cabin |

|---|---|

| Water-related protection | Helps address the kind of damage that can worsen when a home sits empty between visits |

| Ordinance or law coverage | Important when rebuilding requires compliance with current codes, which can complicate mountain repairs |

| Loss-of-rents or rental-income protection | Relevant if the property generates income and becomes unusable after a covered loss |

| Rental liability extensions | Important when guest use creates exposure beyond ordinary personal occupancy |

If your cabin has any rental component, it helps to compare your policy against a broader discussion of comprehensive coverage for rental properties, especially for liability, income protection, and tenant- or guest-related exposures.

What to ask before you bind coverage

Don't ask only, “Is this covered?” Ask, “Under what conditions is it not covered?”

That leads to better answers.

- Ask about occupancy language: If the property is empty for stretches, have the agent identify the clause that addresses vacancy or unoccupancy.

- Ask about guest use: If non-family guests stay there, confirm whether the policy contemplates that use.

- Ask about water claims during off-season periods: Mountain owners often focus on wind and trees, but water losses are the ones that can turn ugly.

- Ask whether income protection is included or excluded: If you advertise the home, this matters.

One practical option in multi-state mountain markets is to work through an independent agency that can compare different carriers' approaches to second homes and rental use. For example, Select Insurance Group, Inc. compares quotes from multiple carriers, which is useful when one company is comfortable with seasonal occupancy and another is not.

The strongest policy is usually the one that answers your awkward questions clearly before a loss, not after one.

Price matters. But a lower premium can be expensive if the policy is built around a cleaner occupancy story than the one you're living.

A Homeowner's Checklist for Securing Your Policy

Shopping for mountain-home coverage goes better when you prepare like an underwriter, not just a buyer. The more precisely you describe the property, the easier it is to place it correctly.

Many secondary-home policies include occupancy clauses that can trigger exclusions when the home is vacant for more than 30 days, which is why owners need to clarify that language before a claim ever happens, as explained in this specialty dwelling insurance overview on vacancy clauses.

Before you request quotes

Gather the facts a carrier will ask for anyway.

- Property use details: Write down whether the home is personal-use only, family-use only, occasionally rented, or regularly booked.

- Occupancy pattern: Note the longest stretches the home sits empty during the year.

- Protection features: List alarm systems, cameras, water sensors, smart thermostats, and any active monitoring.

- Access and site details: Be ready to describe road access, slope, wooded surroundings, and general remoteness.

During the insurance conversation

Many owners get too vague at this stage. Be specific.

Ask these questions directly:

- How does this policy define occupied, unoccupied, and vacant?

- What happens if the cabin sits empty beyond the policy threshold?

- Are inspections, winterization, or monitoring required during those periods?

- Does the policy change if I allow paying guests even occasionally?

- Is rental-income protection available if the home is used as a short-term rental?

A short checklist like that can prevent a long claims dispute later.

Documents and proof to keep handy

You don't need a huge file, but you do need usable records.

- Photos of the property and interior contents

- Receipts for major updates or repairs

- A written summary of security and maintenance routines

- Any listing information if the property is advertised for guest stays

Bring the uncomfortable facts into the application. A policy is more durable when the carrier knows exactly what it's insuring.

Owners sometimes think full disclosure makes coverage harder to get. Sometimes it changes the quote, yes. But it also gives you a much better chance of having coverage that responds the way you expect.

How to Get Quotes and Finalize Your Coverage

Blue Ridge cabin insurance goes sideways when owners shop by label instead of by use. “Second home” sounds close enough, so they pick the cheapest option and move on. That approach works until the house sits empty too long, a guest gets hurt, or a water claim arrives after an off-season closure.

A better process is simple.

First, give the same fact pattern to every agent or carrier. Describe occupancy, vacancy stretches, guest use, platform listings, and monitoring systems the same way each time. If the story changes from quote to quote, the comparisons won't mean much.

Second, ask for the policy differences in plain English. Don't settle for “yes, that should be covered.” Ask how the form handles unoccupancy, rental activity, liability, and any loss tied to the property being used for income.

Third, use an independent agent when the property doesn't fit a clean box. That matters in the Blue Ridge region because mountain homes often blend seasonal personal use with occasional rental activity. An independent agency can compare carrier appetite instead of forcing every property into a single underwriting model.

The goal isn't just to get insured. It's to make sure the coverage still makes sense after your cabin starts being used the way most Blue Ridge cabins eventually are. A little more planning on the front end is much cheaper than finding out after a claim that the policy was written for a simpler property than the one you own.

If your cabin in Blue Ridge is part getaway and part income property, talk it through before you bind coverage. Select Insurance Group, Inc. can help you compare policy options across multiple carriers and sort through how occupancy, vacancy, and short-term rental use affect the coverage fit for your property.