You open your mail and see a non-renewal notice. Or you run an online quote after a DUI, a lapse in coverage, or a couple of ugly tickets, and the price is far higher than you expected. That moment catches a lot of riders off guard.

In South Carolina, getting labeled high-risk doesn't mean you're uninsurable. It means the process changes. Fewer carriers want the account, underwriting gets stricter, and the cheapest option on paper can become the most expensive mistake after a claim.

The practical question isn't whether you can still get coverage. Usually, you can. The core question is how to get legal again, how to avoid bad policy choices while you're under pressure, and how to work your way back toward standard rates.

What Makes a Rider High-Risk in South Carolina

Most riders don't call themselves high-risk until an insurer does it for them. That usually happens after a rate jump, a declination, or a notice that the carrier won't renew your policy.

A high-risk rider in South Carolina is typically someone with one or more underwriting triggers that make an insurer expect a higher chance of a claim. Sometimes that's obvious, like a DUI or multiple violations. Sometimes it's less obvious, like a long insurance lapse, being under 25, or riding a high-performance sport bike.

The triggers that usually push you into high-risk pricing

Insurers commonly look at a mix of these factors:

- Major violation history like a DUI or DWI. This is one of the fastest ways to move from standard pricing into a much tougher underwriting tier.

- Multiple tickets such as repeated speeding citations, reckless driving, or other moving violations.

- At-fault accidents or prior claims that show a recent pattern of loss.

- A lapse in coverage because insurers often read a gap as a sign of instability or uninsured driving exposure.

- Age under 25 since younger riders are often priced more aggressively.

- Bike type because a sport or high-performance motorcycle can raise concern even before a carrier reviews the rest of your file.

The frustrating part is that riders often focus only on the violation and miss the stack of factors. A rider with one DUI, a lapse, and a sport bike is a different underwriting file than a rider with one old violation and continuous coverage.

Practical rule: If you've had a DUI, a non-renewal, or a lapse, assume you need to shop the nonstandard market first, then see later whether a standard carrier will take you back.

Why insurers in SC look at riders this way

South Carolina has a real motorcycle risk problem, and insurers know it. The state only requires helmets for riders under 21, and in 2021, 64% of motorcyclists killed in South Carolina were not wearing a helmet, according to South Carolina motorcycle crash reporting summarized by Enjuris.

That fact matters even if you always wear a helmet. Insurers price within the state environment they operate in. If the overall severity profile is worse, especially for riders already carrying underwriting red flags, premiums tend to reflect that.

What high-risk really means for you

It usually means three things.

First, fewer companies will quote you. Second, the companies that do quote may ask more questions about your record, your bike, and how often you ride. Third, you'll need to think harder about coverage structure, not just price.

That last part matters most. When riders feel cornered, they often buy the first legal policy they can find. That solves the DMV problem for today, but it can leave major gaps if there's another accident.

Navigating SC Insurance Requirements and SR-22 Filings

If your license situation or court paperwork mentions an SR-22, don't confuse that with a special insurance policy. It isn't a policy. It's a filing your insurer sends to the state to show you carry the required liability coverage.

South Carolina's legal minimum is low. The state requires $25,000 bodily injury per person, $50,000 per accident, and $25,000 property damage, but with over 2,000 motorcycle crashes annually in the state, guidance for riders commonly recommends at least 100/300/100 instead, as explained in South Carolina motorcycle liability guidance from Davis Insurance.

SC minimum versus what many high-risk riders should actually carry

| Coverage Type | SC State Minimum | Recommended for High-Risk |

|---|---|---|

| Bodily Injury per Person | $25,000 | $100,000 |

| Bodily Injury per Accident | $50,000 | $300,000 |

| Property Damage | $25,000 | $100,000 |

Minimum coverage keeps you legal. It does not necessarily protect your savings, wages, or future income if a serious injury claim blows through those limits.

Buying the minimum after a DUI often feels like a money-saving move. It's usually just a way to keep the premium down while increasing the financial risk you carry yourself.

How the SR-22 process usually works

If you've never dealt with one before, the cleanest way to think about an SR-22 is as an administrative requirement attached to your insurance.

The usual path looks like this:

- Find out exactly what the state requires. You need to confirm whether you must file an SR-22 and when it must be active.

- Get a policy with a carrier that will support the filing. Not every company wants this business.

- Have the insurer file the SR-22 on your behalf. You don't usually file it yourself.

- Keep the policy active without interruption. A cancellation can create a new problem fast.

- Verify reinstatement status if your license or registration was affected. Don't assume the filing alone fixes everything.

What riders get wrong after a violation

The most common mistake is treating the SR-22 as the whole job. It isn't. It's just one requirement. You still need the right effective date, enough liability, and a carrier that won't leave you scrambling again at the next renewal.

The second mistake is trying to force the account into a standard carrier that clearly doesn't want it. That wastes time when you may need coverage immediately. If you've been declined, non-renewed, or told the company can't file what you need, move on quickly.

A third mistake is setting limits too low because the premium already hurts. For high-risk riders, that short-term decision can become the most expensive choice on the policy.

How to Compare Quotes for High-Risk Motorcycle Insurance

The quote process changes once you have a DUI, a bad driving record, or a lapse. Standard online forms may give you a teaser price, then collapse once underwriting reviews the details. That's why high-risk riders need a more deliberate approach.

In South Carolina, high-risk motorcycle policies are commonly 50% to 200% more expensive than standard rates. A policy that might cost a low-risk rider $700 per year could cost a high-risk rider $1,200 to over $2,000, according to high-risk motorcycle insurance pricing guidance from NHC Insurance.

Gather your file before you shop

You'll get better quotes, and fewer surprises, if you have your information ready up front.

Bring together:

- License details including your current status and any reinstatement requirements.

- Motorcycle VIN and bike information because carriers price heavily off the unit you ride.

- Violation and accident details with dates, whether alcohol was involved, and whether there was property damage or injury.

- Current or prior insurance information including whether you've had a lapse.

- Usage details such as commuting, pleasure riding, or occasional weekend riding.

- Any court or DMV paperwork if an SR-22 or other filing is involved.

If you leave out something important, the quote often changes later. For high-risk riders, that usually means one direction only.

Know which market you're shopping

There are three practical buckets.

Standard carriers work well when the issue is minor, older, or isolated. Some riders still qualify there, especially if the rest of the file is strong.

Nonstandard carriers are where many high-risk accounts land. These companies are used to violations, lapses, and tougher underwriting histories.

Specialty motorcycle carriers can be useful when the bike itself is part of the problem, especially if you ride a performance-oriented model or need a more customized package.

The mistake is assuming every company is looking at your file the same way. They aren't. One carrier may punish the lapse hardest. Another may care more about the DUI. A third may dislike the bike model more than anything else.

Compare policies line by line, not just by premium

A serious quote comparison should include:

- Liability limits because two quotes can look similar until you see one is bare minimum.

- Uninsured and underinsured protection since motorcycle injury claims can get expensive fast.

- Deductibles because a lower premium can mean a higher out-of-pocket burden later.

- Coverage for the bike itself if collision or other physical damage protection matters to you.

- Filing capability if you need SR-22 support.

- Payment terms because an affordable monthly option can matter if cash flow is tight after a violation.

If a quote is dramatically cheaper, check what got removed. In this market, low price often means low limits, missing coverages, or a carrier that may not be a fit at renewal.

One practical option is working through an independent agency that can access multiple markets. Select Insurance Group, Inc. compares quotes from multiple carriers, which is the kind of setup that can help when one company declines and another will still consider the account.

Actionable Tactics to Lower Your High-Risk Premiums

You probably won't erase high-risk pricing overnight. You can, however, stop making it worse and start improving how underwriters see the account.

One of the most overlooked rating factors is simple exposure. Insurers use annual mileage and riding frequency as direct pricing inputs, and documenting that you're a weekend-only rider rather than a daily commuter can materially lower your rate, based on motorcycle underwriting guidance on riding habits from AAAA Insurance.

What actually helps

Some changes move the needle more than others.

- Keep coverage continuous. A lapse is expensive enough the first time. Don't create a second one while you're already in a tougher rating tier.

- Take a certified safety course if the carrier recognizes it. This can help both from a discount perspective and from an underwriting perspective.

- Choose a less aggressive bike if you're in a position to switch. The underwriting response to a cruiser or standard bike is often easier than the response to a high-performance sport model.

- Store the bike securely and ask about anti-theft, garage, or safe-rider discounts where available.

- Bundle policies when it makes sense. It won't rescue a bad file, but it can help trim cost.

- Be accurate about mileage and use. If you only ride on weekends, say so and be prepared to support that.

What usually doesn't work

Riders often ask if lowering limits to the floor is the best way to save money. Sometimes it saves premium, but it's usually the wrong kind of savings for a rider already in a vulnerable position.

Another weak strategy is quote-chasing with different information on every application. Underwriters notice inconsistencies. That can lead to corrected premiums, rescinded offers, or a lot of wasted time.

A better approach is to present a stable file. Same address. Same riding pattern. Clear explanation of the violation if needed. Evidence that the problem was isolated and that your behavior since then has changed.

The underwriting mindset to keep in view

Underwriters are trying to answer one question. Is this rider becoming safer, or staying risky?

A clean stretch after an incident matters. Conservative riding habits matter. Lower mileage matters. Continuous insurance matters. If your actions line up with a lower-risk profile, your options usually improve at renewal.

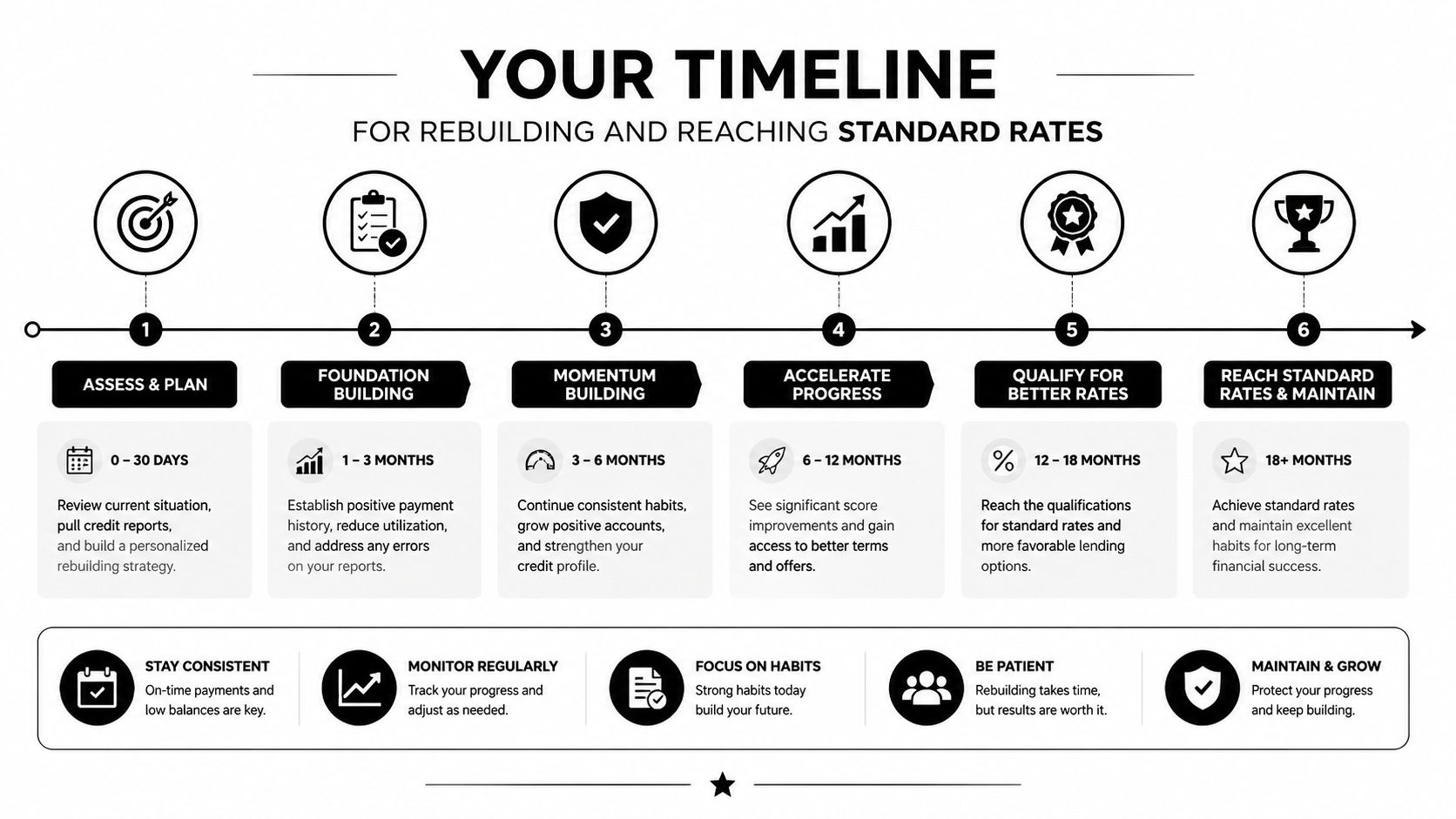

Your Timeline for Rebuilding and Reaching Standard Rates

Most riders want one answer here. How long am I stuck with this?

The honest answer is that there isn't one universal calendar. The timeline depends on what put you into high-risk status, how recent it was, whether you've kept coverage in force, and whether your record stays clean after the incident. But the path back is usually steady, not mysterious.

The first phase after a DUI or bad record

Right after a major violation, your job is basic but important. Get insured correctly. Keep the policy active. Meet every filing or reinstatement requirement. Don't add another ticket while you're trying to clean up the first problem.

This is also the period where riders make desperate decisions. They cancel because the premium hurts, they miss an installment, or they buy the cheapest legal policy and forget to review it. Those choices drag out the recovery.

Clean time is what changes your file. Not intention, not frustration, not how unfair the price feels.

What progress looks like over time

The strongest signs of improvement are boring, and that's exactly the point.

- A clean driving stretch with no new tickets or claims

- Continuous coverage with no cancellations for nonpayment

- Completion of any required filing period tied to your license or insurance status

- Stable riding pattern that doesn't suggest increased exposure

- Renewal shopping instead of auto-renewing a bad policy year after year

At each renewal, ask a fresh question: is this still a nonstandard placement, or has the account improved enough for a broader market search?

How riders actually get back to better rates

It usually happens in stages.

At first, the goal is approval. Later, the goal is a cleaner nonstandard rate. After that, the goal is getting re-reviewed by carriers with tighter underwriting but better pricing. Riders who stay patient and keep the record clean often move through those stages much faster than riders who keep resetting the clock with new issues.

That's why I tell clients to think in renewals, not in weeks. Every clean renewal period helps. Every avoided lapse helps. Every avoided violation helps. If you treat SC motorcycle insurance for high-risk riders as a rebuilding project instead of a one-time emergency purchase, your options tend to expand.

Why an Independent Broker Is Your Best Ally

High-risk motorcycle insurance is hard to shop alone because the market isn't fully visible online. Many standard carriers will not accept the risk. Others will show an initial number, then revise or withdraw it once the full record comes in.

That leaves many riders in the nonstandard market, where access matters. As noted in South Carolina motorcycle insurance market guidance from BikeBound, many standard carriers will non-renew or decline high-risk riders, and an independent broker's main advantage is access to specialty carriers that riders often can't reach on their own through simple online quoting.

What a broker actually does in this situation

A good independent broker isn't magic. The record is still the record. But a broker can make the process far more efficient.

They can identify which carriers are worth approaching based on the specific issue. They can help package the application cleanly. They can spot when one quote is cheaper only because the coverage is weaker. They can also help you remarket the policy at renewal instead of letting you sit in the same overpriced placement longer than necessary.

Why this matters for the long game

If you've just had a DUI or you've got a poor driving record, speed matters first. Strategy matters right after that.

You need a policy that keeps you legal, fits your actual risk, and gives you a path to better options later. That's where an independent broker tends to be most useful. Not because they can erase the violation, but because they can shop the market you're in today and help position you for a better one tomorrow.

If you need help finding SC motorcycle insurance for high-risk riders after a DUI, tickets, a lapse, or a non-renewal, Select Insurance Group, Inc. can help you compare available options and sort through the practical next steps. The goal is simple: get you insured correctly now, avoid coverage mistakes that cost more later, and put a plan in place for better pricing at future renewals.