The biggest mistake Alabama drivers make is chasing a company name instead of chasing the right quote setup. In one 2026 analysis, Alabama's average full coverage cost was $2,196 per year, while the cheapest listed full coverage option was $1,199 per year, a gap of nearly $997 a year according to NerdWallet's Alabama rate analysis.

That number changes how you should shop. It tells you the cheapest car insurance in Alabama isn't a fixed brand. It's a moving target that depends on your credit profile, driving history, ZIP code, car, coverage limits, and whether you're comparing identical quotes.

As an independent-agent-style rule, I'd put it this way: cheap insurance isn't about finding one magic carrier. It's about finding the carrier that likes your exact risk profile today, without stripping out protection you may need tomorrow.

Table of Contents

- Your Guide to Finding the Cheapest Car Insurance in Alabama

- What Alabama Law Requires and What It Really Costs

- What Really Determines Your Alabama Auto Insurance Rate

- Proven Tactics for Lowering Your Alabama Car Insurance Bill

- The Smart Way to Shop for Car Insurance in Alabama

- Avoiding the Pitfalls of a Too-Good-to-Be-True Premium

- Your Alabama Auto Insurance Questions Answered

Your Guide to Finding the Cheapest Car Insurance in Alabama

Alabama is usually a more affordable auto insurance market than many states, but that doesn't mean rates are simple. Two drivers on the same street can get very different prices from the same insurer. One has excellent credit and no claims. The other had a recent ticket, drives a costlier vehicle to repair, or parks in a higher-risk area. The “cheap” option flips.

That's why headline rankings only help a little. They point you toward carriers worth checking, but they don't answer the main question: who is cheapest for you once the quote reflects your profile and the coverage you need?

A lot of drivers also save money the wrong way. They lower liability limits too far, remove coverage they can't afford to lose, or compare one quote with roadside assistance to another quote without it and think they found a deal. They didn't. They changed the product.

Practical rule: If two quotes don't have the same liability limits, deductibles, and key coverages, you are not comparing price. You are comparing different policies.

The smarter approach is part math, part judgment. You want to know where Alabama pricing usually lands. You also want to know which rating factors move the needle most, and which “savings” create trouble at claim time.

That's where an experienced independent approach helps. Instead of asking which insurer is always cheapest, ask better questions:

- What profile am I being rated as

- Are the deductibles identical

- Is this quote missing collision or protection for other types of damage

- Does this carrier price my ZIP code well

- Am I paying extra for a vehicle that's expensive to repair

That process is how people find genuine savings in Alabama. Not by guessing. Not by shopping one logo. By forcing every quote into the same framework and then choosing the lowest usable premium.

What Alabama Law Requires and What It Really Costs

Alabama requires minimum liability coverage of 25/50/25. In plain English, that means bodily injury liability for one injured person, bodily injury liability for all injured people in one accident, and property damage liability for what you damage belonging to someone else.

That minimum gets you legal. It does not protect your own car from collision damage, weather, theft, or many of the repair bills that hurt people financially after an accident.

Minimum coverage is legal, not broad

A lot of drivers hear “minimum coverage” and assume it's a basic safety net. It isn't. It's a legal starting point.

If you cause a wreck, liability coverage is built to pay for the damage and injuries you cause to others, up to your policy limits. It generally does not repair your own vehicle. If your car is older and paid off, minimum coverage may be a deliberate choice. If your car is financed, leased, newer, or expensive to fix, minimum coverage can leave a large hole.

Bankrate's 2026 review puts Alabama's average minimum-liability premium at $562 per year and average full coverage at $2,155 per year, which means full coverage costs about 3.8 times the state's average minimum premium according to Bankrate's Alabama insurance review.

Here's the practical comparison:

| Coverage Type | State Minimum (25/50/25) | Recommended Coverage |

|---|---|---|

| Bodily injury liability | Meets Alabama legal minimum | Higher limits for stronger asset protection |

| Property damage liability | Meets Alabama legal minimum | Higher limits for better protection against repair and replacement claims |

| Collision | Not included | Usually worth considering if the car has meaningful value |

| Comprehensive | Not included | Important if you want protection for theft, weather, vandalism, or falling objects |

| Lender or lease compliance | Usually not enough | Often necessary for financed or leased vehicles |

If you've moved between states or insure vehicles across state lines, it helps to understand how requirements differ. For example, this guide to essential Texas car insurance information is useful because it shows how legal minimums can vary and why copying coverage from one state to another can create gaps.

You can also review Alabama policy options and quote structures through Alabama auto insurance coverage options.

Why full coverage changes the conversation

“Full coverage” typically includes liability, collision, and protection for non-collision events. It isn't a legal term, but in everyday insurance use, that's what people mean. Collision covers damage to your own car after a crash. This protection addresses losses like theft, vandalism, hail, or a falling tree that are not crash-related.

The question isn't whether full coverage costs more. It does. The better question is whether dropping it creates a risk you can comfortably absorb out of pocket.

Legal minimums protect your right to drive. They don't automatically protect your budget, your vehicle, or your lender's interest.

When I look at a policy as a practitioner, I don't start with “What's the lowest premium?” I start with “What financial hit can this driver realistically handle?” That answer tells you whether minimum coverage is a smart move, or just a cheap move.

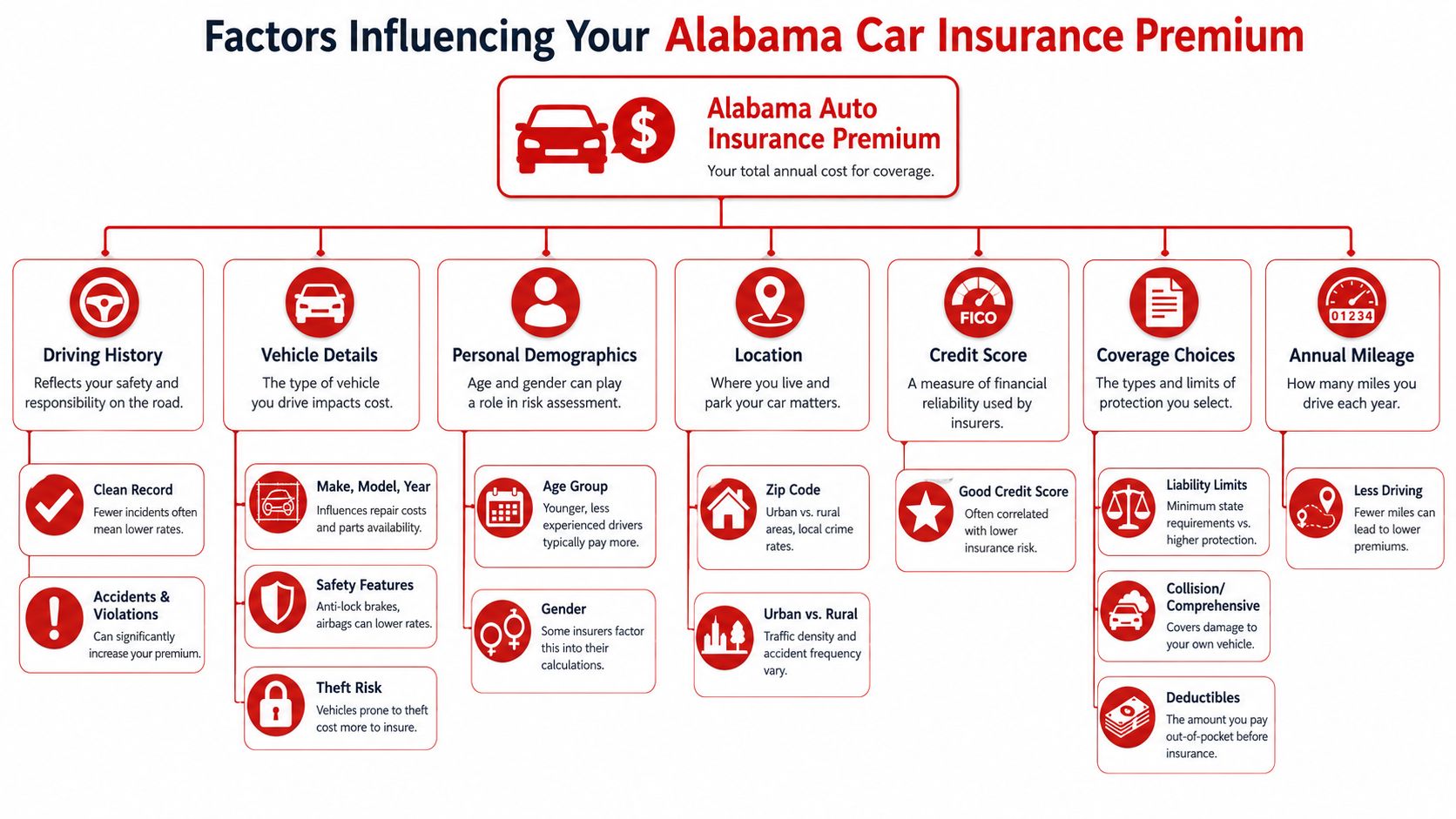

What Really Determines Your Alabama Auto Insurance Rate

The cheapest car insurance in Alabama changes because insurers don't price a person. They price a risk pattern. That's why one company can look unbeatable for one driver and average for the next.

MoneyGeek notes that risk segmentation is the most important pricing lever in Alabama. In one study, COUNTRY Financial and Travelers were among the lowest options for young adults, while for drivers with an at-fault accident, State Farm was cheapest in one dataset at $1,869 per year according to MoneyGeek's Alabama pricing analysis.

Credit and insurance scoring matter more than most drivers think

In Alabama, credit-based insurance scoring can move a quote a lot. Many drivers assume accidents or tickets are the only major price drivers. In practice, credit often reshuffles which insurer is competitive before driving history even enters the picture.

Why do carriers care? They're trying to sort policyholders into pricing groups based on expected claim behavior and loss patterns. You may not like that system, but if you're shopping in Alabama, you have to account for it.

That means two things:

- Don't rely on a friend's “cheap company” if their credit profile is different from yours.

- Re-shop after credit improvement because the carrier that wasn't competitive before may suddenly become attractive.

If you're also comparing vehicles, prior ownership details matter too. A car's background can affect repair expectations, valuation, and underwriting questions. This guide on vehicle history and insurance costs is useful when you're pricing a used vehicle before you buy it.

Driving history changes which carrier is cheapest

Shoppers often get tripped up. They read one list of cheapest insurers and assume the answer is settled. It isn't.

A clean record may put you in one pricing tier. A recent at-fault accident can move you into a very different tier. Some carriers stay relatively competitive after a blemish. Others become expensive fast. The same goes for young drivers, mature drivers, and households adding a teen.

A quote isn't cheap because the company is cheap. It's cheap because the company wants your profile right now.

That's why I tell drivers not to anchor on one headline result. A carrier that prices well for young adults may not price well for a middle-aged driver with a recent violation. A company that looks strong for minimum coverage may not be the value leader once you add collision and other physical damage coverage.

If you're weighing that trade-off, this overview of full coverage vs liability options helps frame what you're paying for and what you're giving up.

Location, vehicle, and age reshape the quote

ZIP code matters in Alabama because local claim patterns matter. Garaging location affects theft exposure, traffic density, repair costs, weather patterns, and the number of uninsured drivers an insurer expects to encounter. City pricing can differ a lot from nearby rural pricing.

The vehicle matters for similar reasons. Insurers look at repair complexity, parts cost, theft attractiveness, and how badly a given model tends to be damaged in common crashes. A modest used sedan and a newer SUV can produce very different results even with the same driver.

Age also matters, though not in a simple straight line. Younger and less experienced drivers often face higher prices. Older drivers may also see changes based on claims patterns and annual mileage shifts. But even here, age doesn't work alone. It interacts with credit, vehicle choice, and coverage elections.

If you want to understand your own rate, start with this checklist:

- Your profile. Credit, license history, claims, household drivers.

- Your car. Year, trim, repair profile, financing status.

- Your location. ZIP code and where the vehicle is kept.

- Your coverage setup. Liability limits, deductibles, and optional protections.

- Your usage. Commute, annual mileage, business use, or pleasure use.

That's the engine behind Alabama auto insurance pricing. Names come later. Profile comes first.

Proven Tactics for Lowering Your Alabama Car Insurance Bill

Reducing insurance costs often begins with removing coverage. That's backward. The best savings usually come from improving the structure of the quote before you strip protection out of the policy.

Fix the quote before you try to beat the quote

Start with quote accuracy. A wrong annual mileage estimate, omitted driver, wrong garaging address, or mismatched deductible can make one premium look lower when it really isn't.

Use this order:

- Standardize the policy first. Same limits, same deductibles, same vehicles, same drivers.

- Correct the usage details. Commute, pleasure use, business use, and estimated mileage should be honest and consistent.

- Check optional coverages. Roadside, rental reimbursement, and similar add-ons should either be included everywhere or removed everywhere during comparison.

This sounds basic, but it's where a lot of fake savings come from.

Use deductibles and extras carefully

Raising a deductible can lower your premium. It can also create a bad surprise if you choose a deductible you cannot pay after a loss. The right deductible is one that lowers cost without forcing you into a financial scramble during a claim.

A cleaner way to think about it is this: if your deductible would feel painful but manageable, it may be reasonable. If it would push you to borrow money or delay repairs, it's too high.

The same principle applies to add-on coverages. Some are useful. Some are easy to cut. Don't remove them blindly. Ask whether the protection fills a real gap in your household.

- Rental reimbursement can matter if your family depends on one vehicle.

- Roadside assistance may be unnecessary if you already have it elsewhere.

- Physical damage coverage may be worth keeping on a car you can't easily replace.

- Low-value vehicle coverage may need a fresh look if the car's value has dropped.

Ask for discounts the right way

Drivers often ask, “What discounts do you have?” That's too broad. A better question is, “What discounts are available for my household and which ones are already applied?”

That gets you a real answer.

Common discount areas include bundling, multi-vehicle households, safe driving programs, student-related discounts, military-related eligibility, autopay, paperless enrollment, and vehicle safety features. But discounts don't all stack the same way, and they don't matter if the base rate is bad.

Discount chasing doesn't fix an overpriced carrier. First make sure the insurer is competitive for your profile. Then optimize the discount stack.

A policy with fewer discounts can still be cheaper than one with a long list of discounts if the underlying rate is stronger. That's why I tell drivers not to get distracted by labels. Final premium matters more than the size of any one discount.

Review your policy when life changes

A lot of Alabama savings opportunities appear after a change you didn't think to report.

Examples include:

- Your commute changed because you switched jobs or now work from home.

- A loan was paid off, so coverage choices may need review.

- A young driver left home or joined the household.

- Your credit improved, making a fresh market check worthwhile.

- You changed vehicles, and the replacement may be cheaper or more expensive to insure than expected.

Also, shop at renewal time, not after you're already frustrated with a bill. Renewal is when many pricing changes become visible and when comparison is easiest.

What doesn't work well? Blind loyalty. Waiting years to compare. Assuming your current company automatically rewards tenure. Sometimes they do. Sometimes they don't. In Alabama, profile fit matters more than habit.

The Smart Way to Shop for Car Insurance in Alabama

Good shopping is boring in the best way. It's organized, consistent, and hard for a bad quote to hide inside. That's how you find the cheapest car insurance in Alabama without creating a coverage problem for yourself.

The Alabama Department of Insurance provides an automobile premium comparison tool, and the state's guidance is useful for one big reason: a single quoting mistake, such as comparing different deductibles or leaving out a regional carrier, can hide several hundred dollars in annual savings according to the Alabama Department of Insurance premium comparison tool.

Build an apples-to-apples quote request

Before you collect quotes, write down your target structure. Don't leave it to each website or agent to choose for you.

Include:

- Liability limits

- Whether you want collision and protection for other risks

- Your deductible choices

- Any add-ons you do or do not want

- Driver list and vehicle list

- Current declarations page if you have one

This prevents one quote from sneaking in with thinner coverage and winning on price for the wrong reason.

Use a process, not random quote clicks

A simple workflow works best:

- Gather your information. License details, VIN, address, prior insurance, and driving history.

- Set your target policy structure. Decide what you want quoted before shopping.

- Collect multiple quotes. Include both major brands and regional carriers when possible.

- Compare the documents, not just the price. Check limits, deductibles, exclusions, and endorsements.

- Ask follow-up questions. Especially on claims handling, billing setup, and optional coverages.

- Confirm effective date before canceling your old policy.

If you're changing insurers, this guide on how to switch auto insurance companies covers the mechanics so you don't create a lapse.

Where an independent agency fits

If you enjoy shopping policies yourself, the state comparison tool and direct quote channels can help. If you don't, an independent agency can compress the process because one office can compare multiple carriers using the same driver and coverage setup.

Select Insurance Group, Inc. is one example. It's an independent agency that compares quotes across multiple carriers and offers bilingual support, which can be useful when you want one person to keep the quote details consistent across markets.

That consistency matters more than people realize. In Alabama, the winning carrier often changes when one variable changes. A good shopping process catches that. A rushed one usually misses it.

Avoiding the Pitfalls of a Too-Good-to-Be-True Premium

The lowest number on the screen isn't always the best policy. Cheap gets expensive fast when a claim exposes what the policy doesn't cover.

Recent data shows Alabama full coverage averages more than twice the cost of the state minimum, and that gap matters because many drivers assume minimum coverage is “good enough” even when it leaves a serious financial hole for a financed, newer, or costly-to-repair vehicle according to Experian's Alabama insurance overview.

Cheap can become expensive fast

I see three common problems in bargain policies.

First, liability limits are set so low that one serious accident can leave the driver exposed beyond the policy. Second, deductibles are chosen based only on premium reduction, not on whether the driver could pay them. Third, drivers drop collision or other physical damage coverage on vehicles they still depend on every day.

None of those choices are automatically wrong. They're wrong when the driver doesn't understand the trade-off.

The goal isn't the lowest premium. It's the lowest premium that still works on your worst realistic day.

Red flags inside bargain policies

Watch for these warning signs when a quote comes in suspiciously low:

- Coverage is thinner than requested. Lower liability limits or missing physical damage coverage.

- Deductibles jumped. The price looks great because your out-of-pocket exposure changed.

- Important extras vanished. Sometimes that's fine. Sometimes it isn't.

- Household details were rated incorrectly. A bad input can become a denied correction later.

- The policy only looks cheap upfront. Billing fees or installment structure can change the actual cost.

A good cheap policy is still a complete policy. It matches your car, your budget, and your actual exposure. If it only wins because key protections disappeared, it isn't really a savings strategy. It's a gamble.

Your Alabama Auto Insurance Questions Answered

Will a ticket raise my rate in Alabama

It can. The exact effect depends on the carrier, the violation, your prior record, and how the company prices your profile at renewal. The practical move is to re-shop after any material change instead of assuming your current insurer remains competitive.

How can young drivers find cheaper coverage

Young drivers usually get better results when the household shops broadly and compares the cost of staying on a family policy versus separate coverage. Also check every student-related and safe-driver discount available, and make sure the vehicle choice isn't making the quote harder than it needs to be.

Can I get car insurance with little money down

Some carriers offer payment structures that reduce upfront cost, but low down payment doesn't always mean low total cost. Focus on the total premium, installment fees, and whether the coverage is still adequate.

Does Alabama location really affect price that much

Yes. Local claim patterns, traffic density, repair costs, and related rating factors can all change what a carrier charges. That's why two nearby towns can produce noticeably different quotes.

Are there niche coverages people forget about

Yes. Drivers often think about collision and liability, but overlook smaller items tied to ownership costs. For example, if you've ever wondered about replacement-related protection outside standard auto coverage, this explainer on how car key insurance works for motorists is a useful example of the kind of detail worth checking before you assume something is covered.

Can I get help in Spanish

Yes. Some agencies, including bilingual independent agencies, can walk through quotes, documents, and coverage choices in Spanish. That can make a big difference when you're comparing policy details and don't want anything lost in translation.

If you want help comparing Alabama auto insurance quotes without guessing which carrier fits your profile, Select Insurance Group, Inc. can review your current setup, match quotes on an apples-to-apples basis, and help you look at price alongside deductibles, limits, and real-world trade-offs.