You open the mail, read the notice twice, and feel the same knot in your stomach most drivers feel at this point. You need an ignition interlock device to keep driving. That means one more requirement, one more expense, and one more reminder that the DUI is going to follow you into places you didn't expect, including your auto insurance.

The question that comes up fast is simple: if the device proves you're driving sober, can it at least lower your premium?

Sometimes, but rarely. That's the honest answer.

A lot of people come in hoping the IID will function like a safety feature discount. Practically, the DUI surcharge is the primary financial problem, and the IID is usually a compliance tool that helps you stop things from getting worse. If you're in Texas and still sorting out the legal side of installation and driving privileges, this guide to Texas car breathalyzer requirements gives a useful plain-English overview.

What matters now is using the IID the right way, talking to insurers the right way, and rebuilding your insurability step by step.

Table of Contents

- Your Guide After a DUI and IID Mandate

- The Truth About IID Insurance Discounts

- Understanding the Real Financial Impact

- IID Insurance Rules in the Southeast

- How to Qualify and Claim a Potential Discount

- Managing High-Risk Insurance with Select Insurance Group

- Frequently Asked Questions About IIDs and Insurance

Your Guide After a DUI and IID Mandate

The first thing to understand is that an IID requirement changes your insurance conversation, but it doesn't define the whole outcome. The device matters. Your documentation matters. Your timing matters. But the carrier is still looking at the conviction, your license status, your filing requirements, and whether you've stayed continuously insured.

Most drivers in this spot are dealing with three pressures at once. They're trying to keep driving legally, keep monthly costs from spiraling, and avoid making a paperwork mistake that creates a new suspension or a policy cancellation.

That's why the right approach is practical, not hopeful.

Start with the parts you can control

You can't undo the conviction by arguing with the underwriter. You can control whether your IID is installed on time, whether your policy stays active, and whether your paperwork is clean. Those details matter because insurers are much more willing to quote a difficult risk when the driver looks organized and compliant.

A sloppy file makes you look harder to insure. A complete file gives an agent something to work with.

Practical rule: Treat your IID paperwork the same way you'd treat proof of insurance after an accident. Keep every document, every compliance notice, and every reinstatement record in one place.

Focus on the next renewal, not just today

A lot of drivers spend all their energy looking for one immediate discount. I understand why. Money is tight after a DUI. But the better question is often, “What will make me easier to insure at my next renewal?”

That mindset changes your decisions. You stop chasing rumors and start building a clean record of compliance. That's where the IID helps most. It supports the story you need your insurance file to tell: this driver had a serious problem, accepted the requirements, and has stayed on track.

The Truth About IID Insurance Discounts

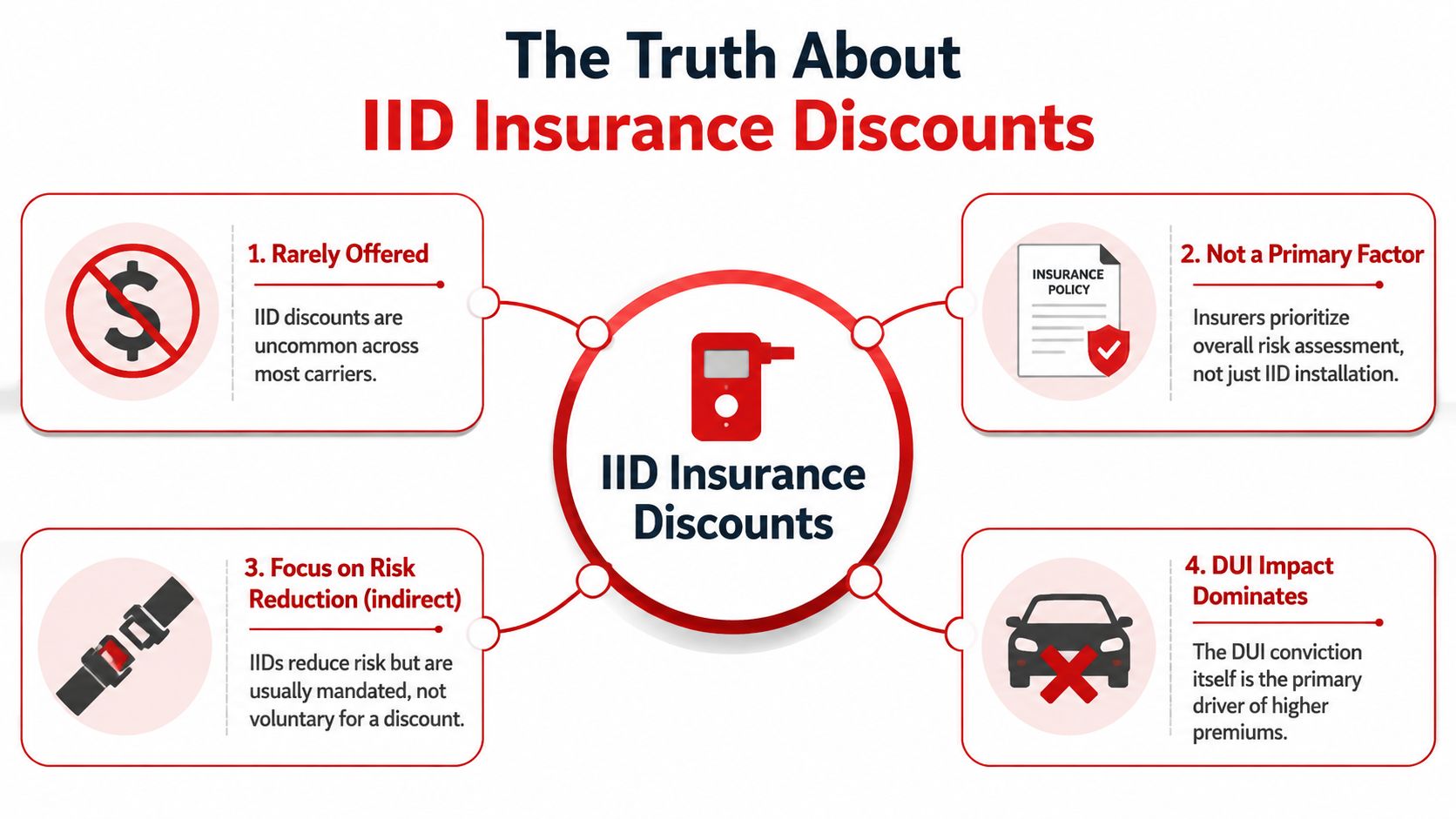

Here's the part many websites soften. Ignition interlock device insurance discounts are not standard. They exist in limited situations, but most drivers with a court-ordered device won't see an automatic premium credit.

According to industry summaries of IID discount practices and state laws, all 50 states and Washington, D.C. have ignition-interlock laws, but most carriers still don't automatically give a premium credit for installing one. That same explanation gets to the core underwriting issue: the device may show compliance, but the DUI conviction itself is what usually drives the rate increase.

Why insurers look at it this way

From the insurance side, a court-ordered IID is different from a voluntary safety feature. Anti-theft systems and some vehicle safety equipment may fit neatly into established discount categories. An IID after a DUI usually does not.

Why? Because the carrier sees the device in context. It's there because you were already placed into a high-risk category.

That means the device often works as a risk-management marker, not a pricing trigger. It tells the insurer you're complying with legal requirements. That's helpful. But it doesn't erase the loss history signal created by the conviction.

What usually works and what usually doesn't

There are two common mistakes drivers make here.

- Expecting an automatic credit: Most insurers won't add one just because the device appears on your record.

- Assuming the IID is irrelevant: It still matters, just not in the way people expect.

What tends to help is using the IID as part of a larger file that shows responsibility. What tends not to help is calling a carrier and asking only, “Do you have an interlock discount?” with no supporting documents and no broader review of the policy.

The IID is usually a tool for mitigation, not a magic discount coupon.

The more useful question to ask

Instead of asking only about an IID discount, ask your agent questions like these:

- Can this carrier write DUI business with active compliance requirements?

- Does this company treat voluntary installation differently from court-ordered installation?

- Are there any safety-device, filing, or policy-structure credits that could apply alongside this situation?

- What would make me look better at renewal if I stay violation-free?

That line of questioning gets you closer to real savings than chasing a discount category that often isn't there.

Understanding the Real Financial Impact

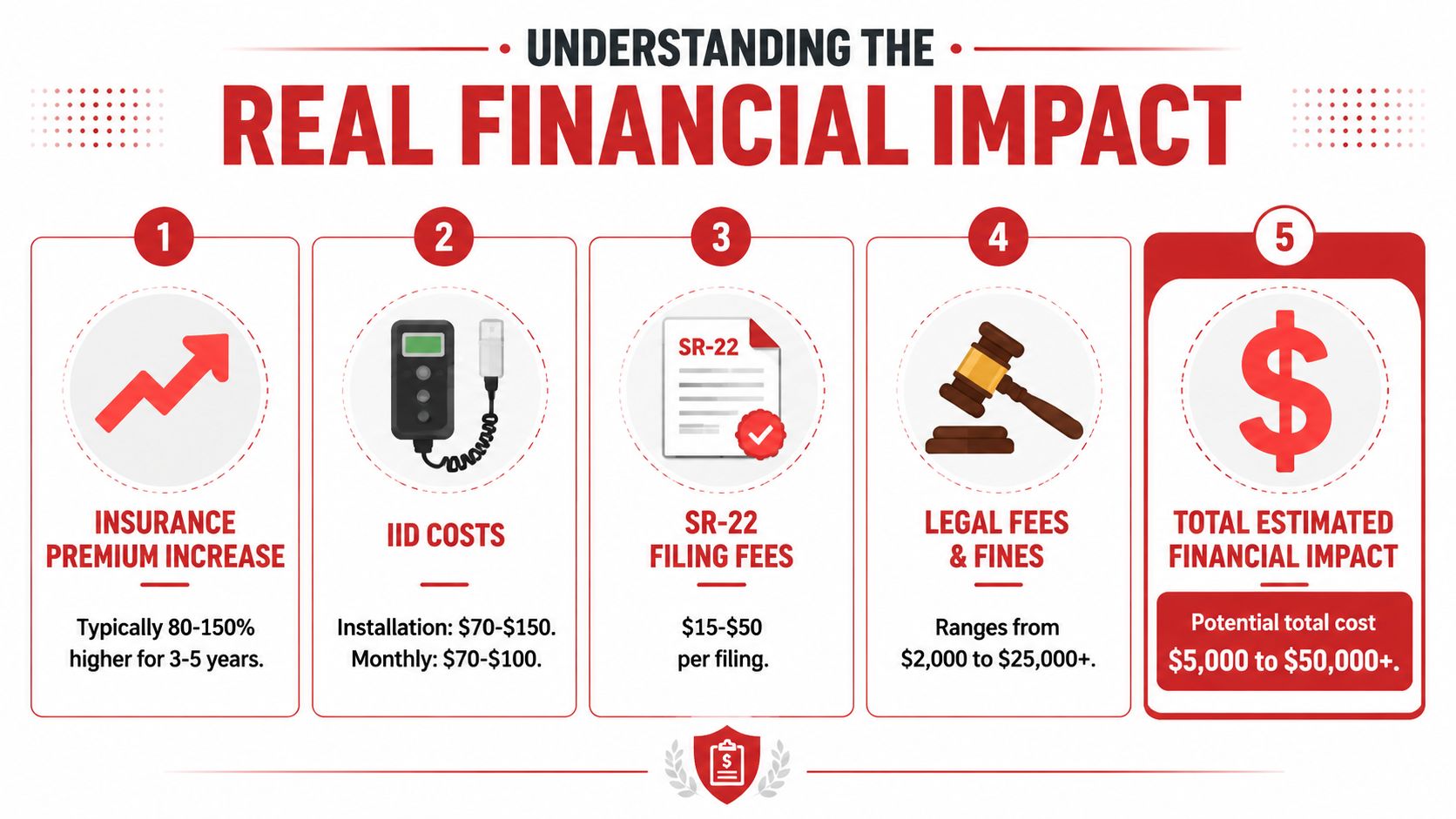

A typical post-DUI conversation goes like this: a driver calls hoping the IID will knock the premium back down, then sees the quote and realizes the device barely changes the number, if it changes it at all. The hard cost is usually the DUI surcharge, the filing requirement, and the smaller pool of carriers still willing to write the policy.

Published insurer guidance shows how uneven that math can be. Post-DUI premium increases can run roughly 50% to 300%, while any IID-related credit, if a carrier offers one, is often modest and case-specific, as summarized in this overview of DUI surcharges and limited IID credits.

That gap matters.

If your premium jumped because of the conviction, a small IID credit will rarely fix the budget problem by itself. The device still has value. It helps you stay legal, keep the policy active, and show a future underwriter that you followed the rules. That is often worth more than a small line-item discount.

Why the surcharge hits harder than the IID helps

Insurance companies usually price the conviction first and the interlock second. From the underwriting side, that makes sense. The DUI changes how the risk is classified. The IID shows compliance, but it does not remove the event that triggered the surcharge.

I tell clients to focus on three money decisions right away:

- Keep coverage in force: A lapse after a DUI can shrink your carrier options fast.

- Handle every filing on time: Missed paperwork can create a bigger problem than the IID itself.

- Stay violation-free during the IID period: Clean time is what gives you a better shot at a less painful renewal.

That is the financial use of the device. It is a mitigation tool.

Why insurers still care more about the conviction than the device

Safety research on interlocks is encouraging, and that matters from a public safety standpoint. In pricing, though, carriers still look at the full file. They underwrite the DUI, prior violations, reinstatement requirements, coverage history, and whether the policy has stayed active without interruptions.

That is why a driver with an IID and clean compliance can still pay high-risk rates. It is frustrating, but it is common. The device can help prevent the situation from getting worse. It does not usually erase the rating impact already on the record.

If you want a broader view of how insurers weigh driving history over time, this article on how long traffic tickets affect insurance helps explain the rating timeline. For another plain-language example of managing car insurance premiums after a DUI, it also helps to see how attorneys describe the budgeting pressure that follows a conviction.

The biggest financial win usually sounds less dramatic than people expect: keep the policy active, meet every requirement, avoid another violation, and give yourself a better chance at a cleaner renewal later.

IID Insurance Rules in the Southeast

State law drives the IID process, and state insurance rules shape what happens after. That's why drivers in the Southeast can't rely on generic advice. The legal trigger for the device may look familiar from one state to another, but the insurance market response can still differ.

Here's the practical view for the seven states many of our clients ask about.

Southeast state IID insurance overview

| State | Typical IID Mandate Trigger | Known Insurance Discount Availability |

|---|---|---|

| Alabama | DUI-related license reinstatement or court requirement | Rare and not typically automatic |

| Florida | DUI conviction with reinstatement conditions and related filing requirements | Rare, with focus usually on compliance rather than discounting |

| Georgia | DUI-related reinstatement or court-ordered installation | Limited and case-specific |

| North Carolina | DUI-related restricted driving or restoration conditions | Uncommon |

| South Carolina | DUI-related requirement tied to legal driving privileges | Uncommon |

| Tennessee | DUI conviction and reinstatement compliance | Limited and inconsistent |

| Virginia | DUI-related restricted license or reinstatement requirement | Rare and generally not automatic |

For Florida drivers, the filing piece often matters as much as the IID itself. If you're dealing with that side of the process, this overview of Florida FR-44 insurance for DUI convictions is worth reviewing before you shop.

Alabama

Alabama drivers usually run into insurance trouble when the IID requirement arrives alongside reinstatement questions. The carrier isn't only asking whether the device is installed. It's also looking at whether you're legally eligible to drive and whether all required forms are in place.

On the pricing side, expect the DUI to dominate the quote. The IID can support a cleaner presentation to underwriters, but discounts are not something most drivers should assume.

Florida

Florida is often tougher in practice because the insurance filing requirement can become the center of the transaction. Drivers focus on the device, but many premium shocks come from the broader DUI classification and the state-specific proof of financial responsibility requirements.

In real terms, Florida drivers usually benefit most from accuracy and speed. If your filing, effective dates, and reinstatement timing don't line up, the quote process gets messy fast.

In Florida, the cheapest mistake is often the one you prevent by getting the paperwork right the first time.

Georgia

Georgia drivers often ask whether showing compliance early helps. It can help the shopping process because a complete file tends to make underwriting smoother. It just usually doesn't convert into a clean, named IID discount.

The best move in Georgia is to ask for a full market check after installation is complete and your documents are ready. Partial information leads to partial answers.

North Carolina

North Carolina tends to reward careful policy management more than aggressive discount hunting. If you've got an IID requirement, keep your policy active, keep your address and vehicle information current, and make sure the insurer has what it needs.

A lot of frustration here comes from drivers assuming the device itself changes everything. It doesn't. It supports the bigger goal of showing stable, lawful driving status.

South Carolina

South Carolina drivers should be cautious about treating informal advice as fact. Insurance outcomes can depend heavily on license status, driving record details, and how the carrier handles high-risk business.

The practical expectation is similar to nearby states. The IID may help as evidence of compliance, but don't budget around a promised credit unless it's confirmed in writing.

Tennessee

Tennessee clients often do best when they separate the legal requirement from the insurance strategy. The legal side tells you what must be installed and when. The insurance side asks how that requirement affects market access, renewals, and premium levels.

That distinction matters because many drivers think compliance alone should improve rates immediately. Usually, it improves your position, not necessarily your current premium.

Virginia

Virginia can be very detail-sensitive. Restricted driving privileges, reinstatement conditions, and vehicle use all need to line up. If they don't, insurance problems show up quickly.

What helps in Virginia is a complete submission package. When the underwriter can clearly see the conviction, the current legal driving status, and the IID compliance record, the case is easier to place than one with missing pieces.

How to Qualify and Claim a Potential Discount

The call usually goes the same way. A driver asks whether the interlock gets them a discount, the carrier says no, and the conversation ends too early.

That approach misses an important opportunity. After a DUI, the expensive part is usually the surcharge and the limited carrier options. The IID helps by showing compliance, reducing underwriting concern, and making your file easier to place. In a few cases, that can lead to a credit. More often, it helps you avoid worse pricing or opens the door to a better renewal offer.

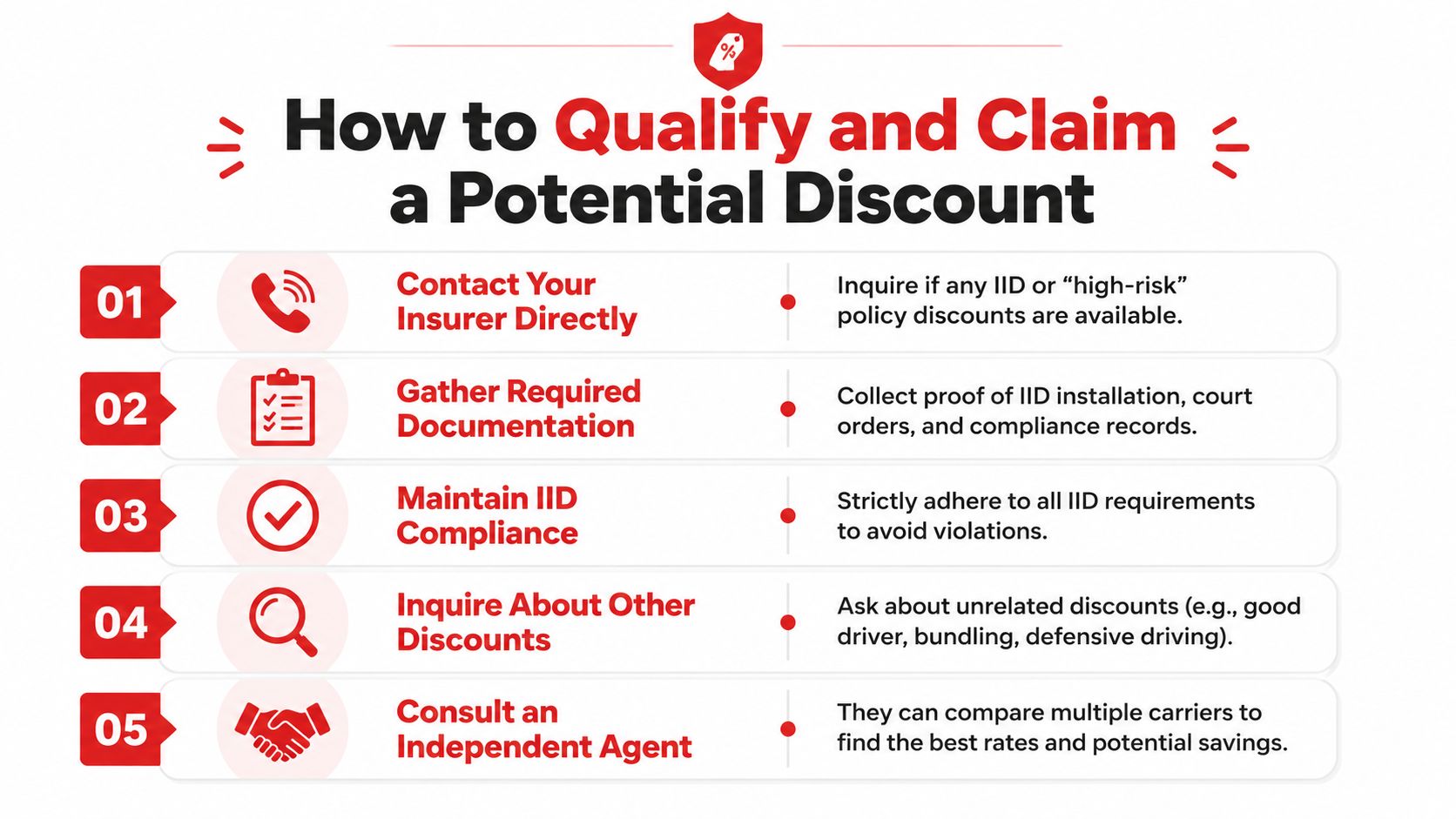

What to gather before you call

Have your paperwork in front of you before you talk to an agent or insurer. A clean file changes the conversation.

- Installation proof: The certificate from an approved IID provider

- Court or DMV paperwork: The order, license restriction, reinstatement notice, or other official requirement

- Compliance records: Reports showing you followed the program rules

- Current policy information: Renewal date, coverage limits, vehicle list, and any filing requirement such as an SR-22 or FR-44

- Proof of continuous insurance: Declarations page or billing history if you have stayed covered

If those documents are missing, the answer is usually vague. If they are ready, an agent can check whether the carrier has a credit, whether underwriting will make a favorable exception, or whether it makes more sense to shop the policy.

How to ask the question so you get a useful answer

Ask for more than a yes-or-no discount check.

A better version is: “I have an IID installed, I'm in compliance, and I need to know whether that affects underwriting, available credits, or my options at renewal.” That wording gets to the point. It tells the person reviewing your policy that you are not asking for a favor. You are asking them to evaluate a documented risk change.

I also tell clients to ask one follow-up question: “What specific documents do you need from me to review this properly?” That keeps the conversation from stalling out in generalities.

What actually helps your case

These steps tend to matter more than the device by itself:

- Stay in full compliance. Any lockout, missed calibration, or program violation weakens the file.

- Keep your policy active. A lapse can cost more than any IID-related savings you were hoping to get.

- Review every other discount category. Multi-car, homeowners or renters bundling, paid-in-full, autopay, mileage, and defensive driving credits often produce more savings than the IID.

- Time the review around renewal when possible. Carriers are often more willing to re-rate or rewrite a policy at renewal than in the middle of a term.

Ask for a policy review based on your full risk profile, not just the interlock.

That is the practical move. The IID is one piece of a larger recovery plan.

When shopping around is the smarter move

If your current carrier gives you no room to improve, get other quotes. Do it carefully. Price matters, but so do filing accuracy, license status, and whether the policy is set up correctly for restricted driving.

Drivers who are still dealing with reinstatement issues often need more than a basic quote. They need someone to sort out paperwork, timing, and eligibility before a small mistake turns into another suspension problem. That is why some clients start with coverage options for drivers dealing with suspended-license insurance issues.

The goal here is not to chase a magic discount. It is to use the IID, your compliance record, and clean documentation to improve your insurability step by step. That is how you put yourself in position for better options later.

Managing High-Risk Insurance with Select Insurance Group

A lot of drivers call after a DUI expecting the IID to be the main insurance issue. It usually is not. The bigger cost is the DUI surcharge and the smaller pool of carriers willing to write the policy cleanly.

What matters now is getting coverage set up correctly. That means a policy that matches your current license status, includes any required filings, and stays active while you work through the IID period. One paperwork mistake, one missed payment, or one policy mismatch can create a much more expensive problem than the loss of a small discount.

Drivers dealing with reinstatement issues or restricted driving status often need more than an online quote. They need someone to review the details before the policy goes live. If that sounds like your situation, start with auto insurance for drivers with suspended licenses, because those cases often overlap with IID requirements and license reinstatement steps.

I tell clients to focus on four things.

- Fix any licensing or filing gaps first.

- Keep the current policy active until the replacement is confirmed.

- Shop before renewal, not after a cancellation notice.

- Ask what improves your placement over the next six to twelve months, not just whether the IID gets a credit today.

That last point matters. An IID can help show compliance and risk control, but it rarely wipes out the financial hit from a DUI. What improves your position is a clean stretch of coverage, no lapses, accurate filings, and time.

That is how high-risk insurance becomes manageable. You stop reacting to the last problem and start building a record that gives underwriters fewer reasons to say no.

Frequently Asked Questions About IIDs and Insurance

Does a voluntary IID help more than a court-ordered one

Sometimes it can, because a voluntary installation may look more like proactive risk management than legal compliance. But you still shouldn't assume a discount exists. Ask whether the carrier views voluntary installation differently and get the answer documented in writing if any credit applies.

Will my rates drop right after the IID is removed

Usually, not immediately. Removal of the device can close out one chapter of the file, but the insurer still sees the DUI history until it no longer affects underwriting under that carrier's rules. The practical benefit of successful removal is that it gives you one more sign of completed compliance when you shop or renew.

Should I tell a new insurer about the IID if they don't ask directly

Yes. Full disclosure is safer. If the carrier learns later that your driving status, legal requirements, or compliance details were left out, you can create problems at renewal or during a claim review. When your record is already under scrutiny, transparency protects you.

If you're dealing with a DUI, an IID requirement, or a difficult renewal, Select Insurance Group, Inc. can help you review your options, check filing requirements, and compare coverage paths that fit your current driving status. The goal isn't false hope about a big interlock discount. It's getting legal, staying insured, and putting yourself in a better position for the next renewal.