The letter shows up, and your eyes go straight to the part that says your license won't be reinstated until you file an SR22A. Most drivers in that moment aren't wondering about insurance theory. They want to know what this form is, why Georgia is asking for something different from a regular SR-22, how much money they need right now, and what to do next without making the problem worse.

That's the right way to look at it. With SR22A insurance for repeat offenders, the hard part usually isn't the paperwork itself. It's the combination of timing, upfront payment, and keeping the policy active long enough to get through the state requirement without another lapse. If you understand those pieces early, you can avoid wasting time on the wrong quote, the wrong filing, or a policy setup that doesn't fit your budget.

Table of Contents

- Facing a License Suspension Understanding SR22A Insurance

- What Is an SR22A and Why Do Repeat Offenders Need It

- SR22A vs SR-22 The Critical Differences

- SR22A Requirements in the Southeast A State-by-State Look

- How to Get and File SR22A Insurance and What It Costs

- Managing Your SR22A Policy and Getting Back to Standard Rates

Facing a License Suspension Understanding SR22A Insurance

A common version of this problem looks like this. A driver has already dealt with the ticket or court date, assumes the worst part is over, then finds out the main bottleneck is administrative. The state won't move forward until the correct filing is on record and active.

That catches people off guard because SR22A sounds like a policy, a penalty, and a court form all at once. It isn't that complicated once you strip the jargon away. It's a state-required insurance filing tied to reinstatement, and if Georgia requires SR22A insurance for repeat offenders, the state is signaling that a standard approach won't satisfy the requirement.

For many drivers, the suspension issue also overlaps with a DUI case or another serious driving event. If you're still sorting out how the suspension side works apart from the criminal or traffic side, this breakdown of administrative license suspension explained is a useful companion because it helps separate the court process from the licensing process.

What usually goes wrong first

Most mistakes happen before the filing is ever submitted.

- Drivers ask for the wrong form: They call around for an SR-22 because that's the term they've heard, even when Georgia requires SR22A.

- They focus only on the filing: The filing matters, but reinstatement also depends on having the right underlying policy in place.

- They underestimate the cash need: The up-front payment rule can stop the process before it starts.

Practical rule: Before you compare prices, confirm the exact filing the state wants. If Georgia requires SR22A, a regular SR-22 quote doesn't solve the problem.

The practical mindset that helps

Treat this like a compliance project, not a shopping project. Speed matters, but accuracy matters more. The right question isn't “Who can sell me any policy today?” It's “Who can place the right policy, collect the required payment, and file the correct certificate without a gap?”

Drivers who approach it that way usually get back on track faster and with fewer expensive resets.

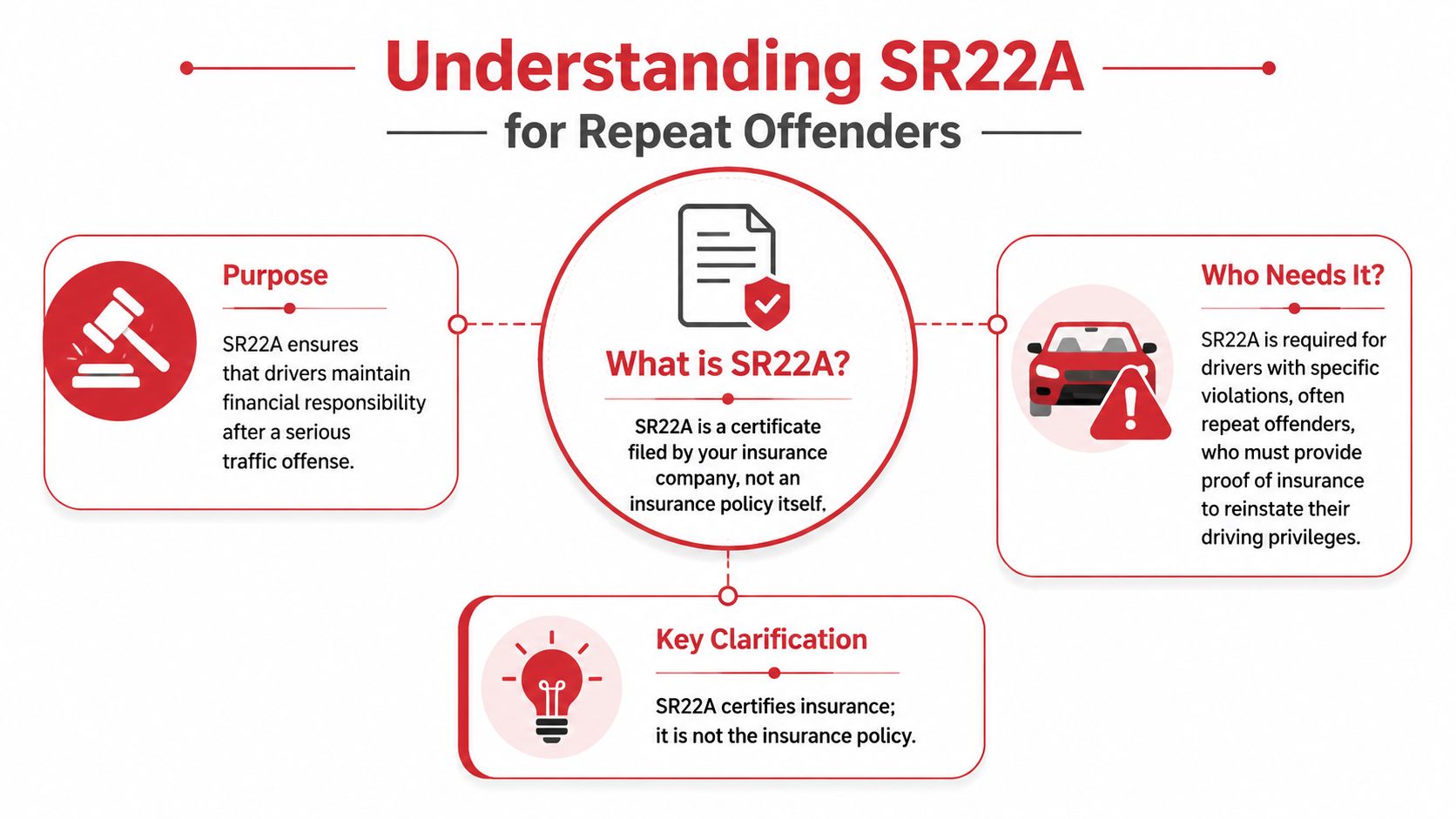

What Is an SR22A and Why Do Repeat Offenders Need It

An SR22A is not an insurance policy by itself. It's a certificate your insurance company files with the state to show that you have the required liability coverage in place and that the filing matches the state's reinstatement requirement.

Think of it as a compliance certificate attached to your auto policy. The policy provides the coverage. The SR22A tells the state that the coverage exists in the form the state wants.

Why repeat offenders get this requirement

Georgia draws a sharper line when the issue involves repeated no-insurance violations. The Georgia Department of Driver Services says that drivers convicted of a second or subsequent no-insurance citation must purchase and maintain an SR-22A policy, and that requirement still applies if the driver doesn't own a vehicle, in which case a non-owner SR-22A is required, according to the Georgia DDS no insurance FAQ.

That point matters because many drivers assume not owning a car gets them out of the filing requirement. In Georgia, it doesn't if the state has ordered a non-owner SR22A.

What the state is really trying to verify

This filing exists to prove financial responsibility after the state has decided your driving or insurance history requires closer monitoring. The filing itself isn't the punishment. It's the mechanism the state uses to make sure coverage stays in place while your driving privilege is being restored.

A few practical consequences follow from that:

- The insurer becomes part of the compliance chain: If coverage ends, the state can be notified.

- Your policy has to match your ownership status: Owner policy if you own a car. Non-owner policy if you don't and you qualify for that type of coverage.

- The filing has to be exact: A policy can be active and still fail to solve the problem if the wrong certificate gets filed.

A lot of stress comes from treating SR22A like a mystery product. It's usually simpler than people think. The real challenge is getting the filing type and policy structure right the first time.

What SR22A does not mean

It doesn't automatically mean you need special coverage beyond what the state requires for liability. It also doesn't mean every insurer will handle the filing the same way, or that every payment plan will work for your situation.

Most important, it doesn't mean “any high-risk policy” is acceptable. If the state says SR22A, the filing must be SR22A.

SR22A vs SR-22 The Critical Differences

The confusion between these two filings costs drivers time. A regular SR-22 and an SR22A both relate to proof of financial responsibility, but they are not interchangeable in Georgia when the state specifically requires SR22A.

The biggest issue isn't vocabulary. It's budgeting.

SR-22 vs SR22A at a glance

| Feature | Standard SR-22 | SR22A |

|---|---|---|

| What it is | A certificate filed by the insurer to show required liability coverage is in place | A certificate filed by the insurer to show required liability coverage is in place |

| Who commonly needs it | Drivers with a high-risk filing requirement | Repeat offenders in Georgia who fall under the stricter filing rule |

| Georgia payment structure | Standard billing may be available depending on carrier setup | Six months of premium prepaid in full is the key technical difference in Georgia |

| Practical budgeting impact | Lower upfront cash burden in many cases | Much heavier upfront cash need before filing can move forward |

| Compliance pressure | Coverage still must stay active | Coverage must stay active, and the upfront collection is designed to reduce nonpayment risk |

Why the payment rule matters more than most guides admit

In Georgia, the key technical difference is that SR22A requires six months of premium prepaid in full, and the standard monitoring period is generally three years, as explained in this summary of Georgia SR-22 and SR22A requirements.

That changes the conversation immediately. A driver who can handle a monthly payment on a normal high-risk policy may still get stuck if the carrier requires six months up front before filing the SR22A.

Many people often lose time. They ask for a quote, hear a monthly figure, assume they can start with the first installment, then learn later that Georgia's SR22A structure requires a larger initial payment. At that point, the quote wasn't wrong. It just wasn't framed around the part that matters most.

What works and what doesn't

What works is asking these questions before you start an application:

- Is this quote for SR22A or only a regular SR-22?

- Is the six-month prepaid amount required before filing?

- Can this filing be submitted promptly once payment is made?

- Does the policy type match my situation, owner or non-owner?

What doesn't work is assuming the lower-looking option is usable. If it doesn't satisfy the state requirement, it isn't a real option.

The practical difference between SR-22 and SR22A isn't academic. For many drivers, it's the difference between needing a manageable start-up payment and needing enough cash to prepay a much larger portion of the policy.

If your issue is in another state and tied to a DUI-related filing with stricter liability requirements, this overview of Florida FR-44 insurance for DUI convictions helps clarify why a different form may apply there instead.

SR22A Requirements in the Southeast A State-by-State Look

Drivers across the Southeast often hear these filing terms from friends, court clerks, tow-yard conversations, or online searches. That's where confusion starts. SR22A is not the standard high-risk filing across the region. It's mainly a Georgia-specific issue.

Where SR22A fits and where it doesn't

If you live in Georgia and the state has ordered SR22A, you need to deal with that exact filing. Drivers in neighboring states often need a high-risk filing too, but usually under a different name.

Here's the practical regional breakdown:

- Georgia: SR22A can apply in repeat no-insurance situations.

- Alabama, South Carolina, North Carolina, and Tennessee: The filing drivers usually encounter is the standard SR-22.

- Florida and Virginia: DUI-related reinstatement issues may involve FR-44 instead of SR-22 or SR22A.

That distinction matters because shopping for the wrong filing wastes time and can delay reinstatement.

The mistake many drivers make after moving or comparing states

A driver may move, or may have a violation in one state and now live in another. Then they search online and assume any article about SR-22 applies to them. Sometimes it does. Sometimes it doesn't.

The better approach is to anchor the decision to the state that imposed the requirement. The state record controls the filing obligation. The filing name matters because each one points to a specific compliance standard.

A driver in Georgia asking for FR-44, or a driver in Florida asking for SR22A, is usually solving the wrong problem.

A quick regional reference

| State | Filing drivers commonly need in high-risk reinstatement situations |

|---|---|

| Georgia | SR22A in the repeat-offender scenario discussed here |

| Alabama | SR-22 |

| North Carolina | SR-22 |

| South Carolina | SR-22 |

| Tennessee | SR-22 |

| Florida | FR-44 may apply for DUI-related cases |

| Virginia | FR-44 may apply for DUI-related cases |

If your issue is in North Carolina rather than Georgia, a same-day filing question is better answered through a resource focused on immediate SR-22 filing in North Carolina, because the document and processing expectations are different.

The practical takeaway for Southeast drivers

Don't shop by abbreviation alone. Shop by state requirement. The state notice, court instruction, or reinstatement order should drive the conversation with the agency. When the filing type is right from the beginning, the rest of the process becomes much easier to manage.

How to Get and File SR22A Insurance and What It Costs

You get the reinstatement notice, call for a quote, and assume the hard part is finding a company willing to file the form. Then the main issue shows up. Georgia often requires the SR22A policy to be paid six months in advance, so the amount due to start coverage can be much higher than drivers expect.

That budgeting detail is what trips up many repeat offenders. The filing itself is usually straightforward. Coming up with the money to start the policy is often the harder part.

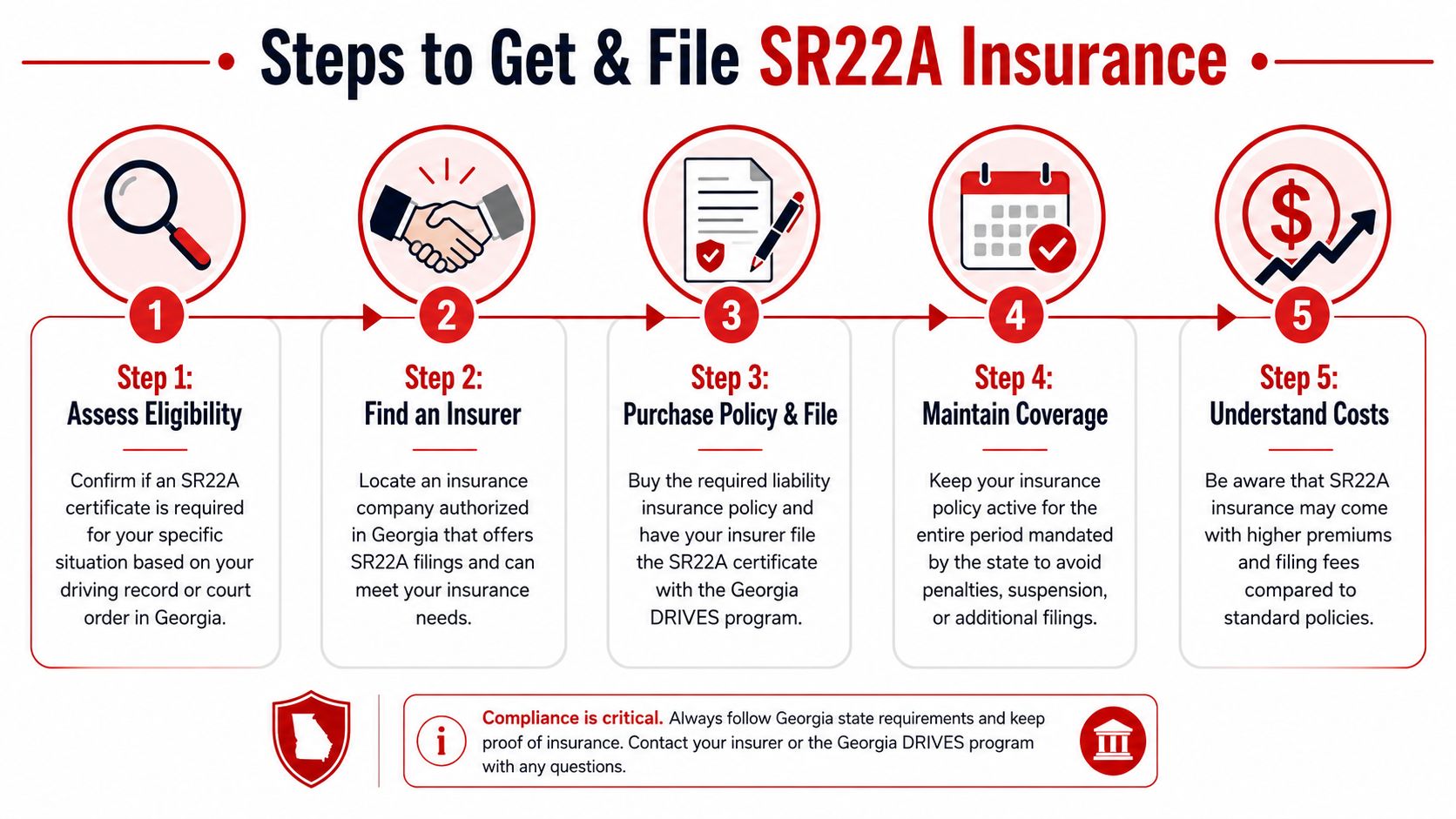

The filing process step by step

Confirm the exact filing on your reinstatement notice

Read the state notice line by line. If it says SR22A, ask for SR22A. A regular SR-22 may not satisfy the requirement, and fixing that mistake can cost you time and another round of paperwork.Work with an agency or insurer that handles high-risk filings

Some carriers do not write these policies, and some quote systems are set up for standard auto insurance only. You need a policy that meets the state's requirement and an agency that can submit the filing correctly.Choose the right policy type

If you own a car, the policy needs to reflect that. If you do not own a vehicle, a non-owner policy may fit, but only if it matches your situation and the state's requirement. I have seen reinstatements stall here because a driver assumed no car meant no filing.Get the upfront payment amount before you agree to anything

This is the SR22A issue that deserves the most attention. In Georgia, repeat offenders are commonly dealing with a six-month prepayment requirement. Ask one direct question early. "What do I have to pay today to start this policy and get the SR22A filed?"Start the policy and have the filing submitted

The filing cannot go in until the policy is active and paid as required. After submission, verify that the state received it. Do not assume the record updated just because you made the payment.

What you are really paying for

Drivers often focus on the filing fee first. That fee is usually modest.

The larger cost is the policy itself, especially after serious violations. With SR22A, the practical problem is not just that premiums are higher. Georgia can compress six months of premium into the first payment, which changes the whole conversation from monthly affordability to upfront cash flow.

That is the difference many guides miss. A standard SR-22 discussion often centers on filing requirements and rate increases. SR22A in Georgia also forces you to plan for the first payment in a very specific way.

How to budget for SR22A without creating a second problem

Start with the amount due now, not the advertised monthly number. If the deposit or six-month prepay is out of reach, the quote is not workable yet.

Ask these questions before you bind coverage:

- How much is due today to activate the policy?

- Is this quote built for SR22A in Georgia, not a regular SR-22?

- Is this an owner or non-owner policy, and why?

- What could cause the filing to be rejected or delayed?

The cheapest quote on paper can still be the wrong choice if the policy structure does not fit the state requirement or the upfront payment is unrealistic for your budget.

Common delays that cost drivers time

- Waiting too long to gather the six-month payment: The filing cannot help you until the policy starts.

- Buying the wrong policy type: Owner and non-owner mistakes are common.

- Failing to confirm receipt with the state: Submission and processing are not the same thing.

- Shopping by monthly payment only: For SR22A, the first payment matters more than the monthly number.

One more point matters here. Serious violations can affect your rates well beyond the filing period, so it helps to understand how long traffic tickets can affect insurance premiums while you plan for the full cost of getting back on the road.

A good SR22A setup does two things. It gets the filing submitted correctly, and it gives you a payment structure you can carry long enough to keep your license on track.

Managing Your SR22A Policy and Getting Back to Standard Rates

Filing the SR22A gets you started. Keeping it active is what gets you through.

The ongoing risk isn't abstract. If the policy lapses, the insurer notifies the state, and that can lead to another suspension. The broader rule for these filings is that the obligation usually lasts about three years, and continuity is the part that matters most because lapses are treated as compliance failures and can restart the process or create new reinstatement problems, as noted earlier in the article.

How drivers protect themselves during the filing period

The best strategy is boring. That's a good thing.

- Use automatic payments if the carrier offers them: A missed due date is one of the fastest ways to create a new problem.

- Open every renewal notice: Don't assume the policy will roll over the way a standard policy might.

- Call before making changes: Vehicle changes, address changes, or switching carriers can all affect the filing.

- Review pricing at renewal: Shopping the policy responsibly can help, but only if the new coverage starts before the old one ends.

If you're wondering how long violations can influence your premium even after the filing issue is gone, this guide on how long traffic tickets affect insurance gives useful context.

What helps rates improve over time

You usually won't fix this with one clever move. What lowers cost over time is consistency.

Keep coverage in force. Avoid new violations. Make every payment on time. Ask for a review at renewal instead of assuming your current rate is the best available. The filing requirement eventually ends, but the way you manage the policy while it's active affects how quickly you move back toward more ordinary pricing.

The drivers who recover fastest are usually the ones who stop treating the filing as a short-term annoyance and start treating it as a fixed compliance obligation with a clear end point.

What not to do

Don't cancel early because you think enough time has passed. Don't switch carriers without overlap. Don't ignore mail from the insurer or the state. And don't assume a clean month or two means you can relax.

The filing period is survivable. Many drivers get through it cleanly. The difference usually comes down to planning for the payment structure, respecting the state requirement, and staying organized long after the initial stress fades.

If you need help sorting out an SR22A requirement, comparing owner versus non-owner options, or figuring out what payment setup is realistic before you file, Select Insurance Group, Inc. offers quotes for high-risk auto filings and can help you start the process with the right information in hand.