Immediate SR22 filing in North Carolina is often possible the same day if an insurer can file electronically with the NCDMV, and many insurers now do. In most cases, the fastest path is working with an independent agency that can place a qualifying policy right away and submit the filing as soon as your driver and vehicle details are confirmed.

If you're reading this with a suspension notice in your hand, you're probably not browsing for fun. You need your license back so you can get to work, pick up your kids, or stop depending on rides from other people. The good news is that this usually moves much faster than drivers expect.

The bad news is that many people waste time asking for the wrong form. In North Carolina, the problem often isn't just "I need an SR-22." A lot of drivers need a DL-123 or FS-1 instead. That one mistake can stall reinstatement before it even starts.

Table of Contents

- Your Guide to Immediate License Reinstatement in NC

- SR22 vs DL-123 vs FS-1 What North Carolina Really Requires

- The Fastest Path to an Immediate SR22 Filing

- Understanding the Costs and Coverage Requirements

- Common Pitfalls That Delay Reinstatement

- Your North Carolina SR22 Questions Answered

Your Guide to Immediate License Reinstatement in NC

A lot of drivers reach this point after a suspension, a lapse in coverage, or a serious traffic issue. If your notice says you need proof of financial responsibility, speed matters. Waiting a week to "figure it out" usually creates more stress, not less.

North Carolina filing issues also get tangled up with the reason for the suspension. If your case involved alcohol, uninsured driving, or a revoked license, you need to understand the DMV side and the insurance side at the same time. For legal context on alcohol-related cases, North Carolina DWI laws and penalties can help you understand how the violation itself affects driving privileges.

What most drivers get wrong

The common mistake is calling around asking only for an SR-22. That sounds logical, but North Carolina doesn't always treat that as the default answer. Sometimes the underlying issue is proving current insurance with a different form, and asking for the wrong one burns valuable time.

You also need your policy to match North Carolina requirements from the start. If you need a refresher on baseline rules for drivers in the state, this guide to North Carolina car insurance laws is a useful starting point.

Practical rule: Before you shop for price, confirm the exact filing your reinstatement requires.

What to do today

Start with the DMV notice, court paperwork, or reinstatement instructions. Look for the exact form name. If the paperwork isn't clear, ask an agent to review it before a policy is issued.

Then move fast on the information the insurer will need:

- Your driver details: full name, date of birth, driver's license number, and current address.

- Your violation details: suspension reason, state involved, and any reinstatement instructions.

- Your vehicle details: if you own a car, have the VIN and garaging address ready.

- Your timing: tell the agent you need immediate filing so they route you to a carrier that can send it electronically.

That last part matters. Fast reinstatement usually has less to do with the filing fee and more to do with avoiding back-and-forth.

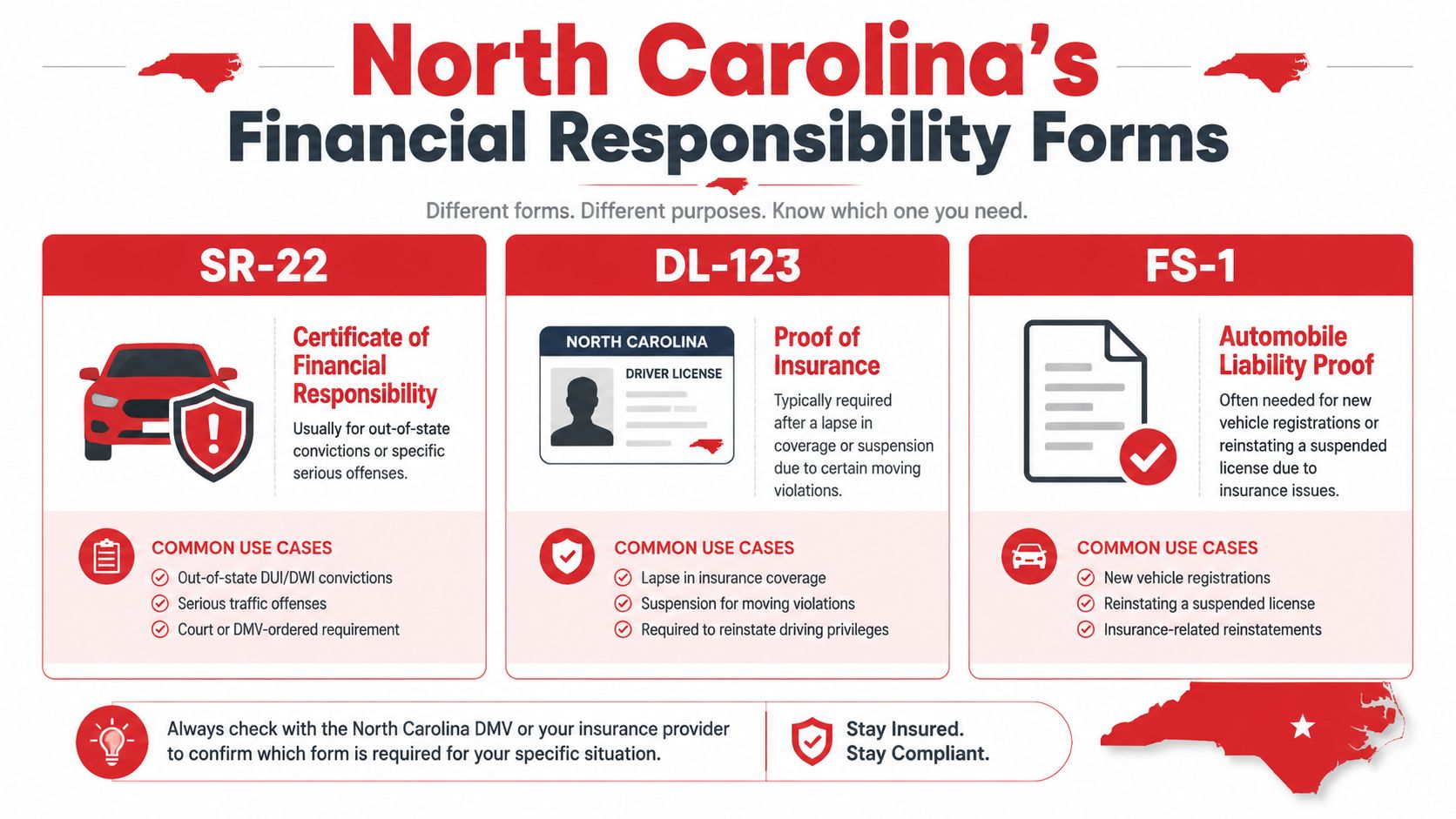

SR22 vs DL-123 vs FS-1 What North Carolina Really Requires

Many drivers in North Carolina ask for an SR-22 when they don't need one. That's the biggest source of delay I see. North Carolina drivers often need a DL-123 or FS-1 instead, and this distinction matters because the state's minimum liability requirements are changing to $50,000/$100,000/$50,000 as of 2025. The filing fee itself is usually only around $15 to $30, while the premium increase tied to the violation is the bigger cost issue, as noted by North Carolina SR-22 filing guidance.

How these forms differ

An SR-22 is a certificate of financial responsibility. It isn't an insurance policy by itself. It's a filing attached to a policy that tells the state your coverage is active and being monitored.

A DL-123 is commonly used in North Carolina to show proof of liability insurance in situations tied to licensing or reinstatement. For many in-state drivers, this is the document that matters more than an SR-22.

An FS-1 is another North Carolina proof-of-insurance form. Drivers often run into it when insurance compliance, registration, or suspension issues are involved.

If you don't own a car but still need to satisfy a filing requirement, a non-owner policy may be the answer. This overview of getting SR22 insurance without a car is useful if you're trying to reinstate a license first and buy a vehicle later.

Simple comparison table

| Form | What it does | When it commonly matters |

|---|---|---|

| SR-22 | Tracks financial responsibility through the insurer | Often tied to serious violations, out-of-state issues, or reinstatement orders |

| DL-123 | Shows active liability insurance | Often needed for licensing or reinstatement in North Carolina |

| FS-1 | Confirms automobile liability coverage | Often used for insurance compliance and registration-related issues |

Filing the wrong form doesn't get you "close enough." It usually means starting over.

Here's the advice I give drivers. Don't rely on what a friend needed, and don't rely on a general internet search. North Carolina paperwork is specific. If your notice says DL-123, don't buy a policy expecting an SR-22 to solve it. If your case involves another state, confirm whether North Carolina, the other state, or both are part of the requirement.

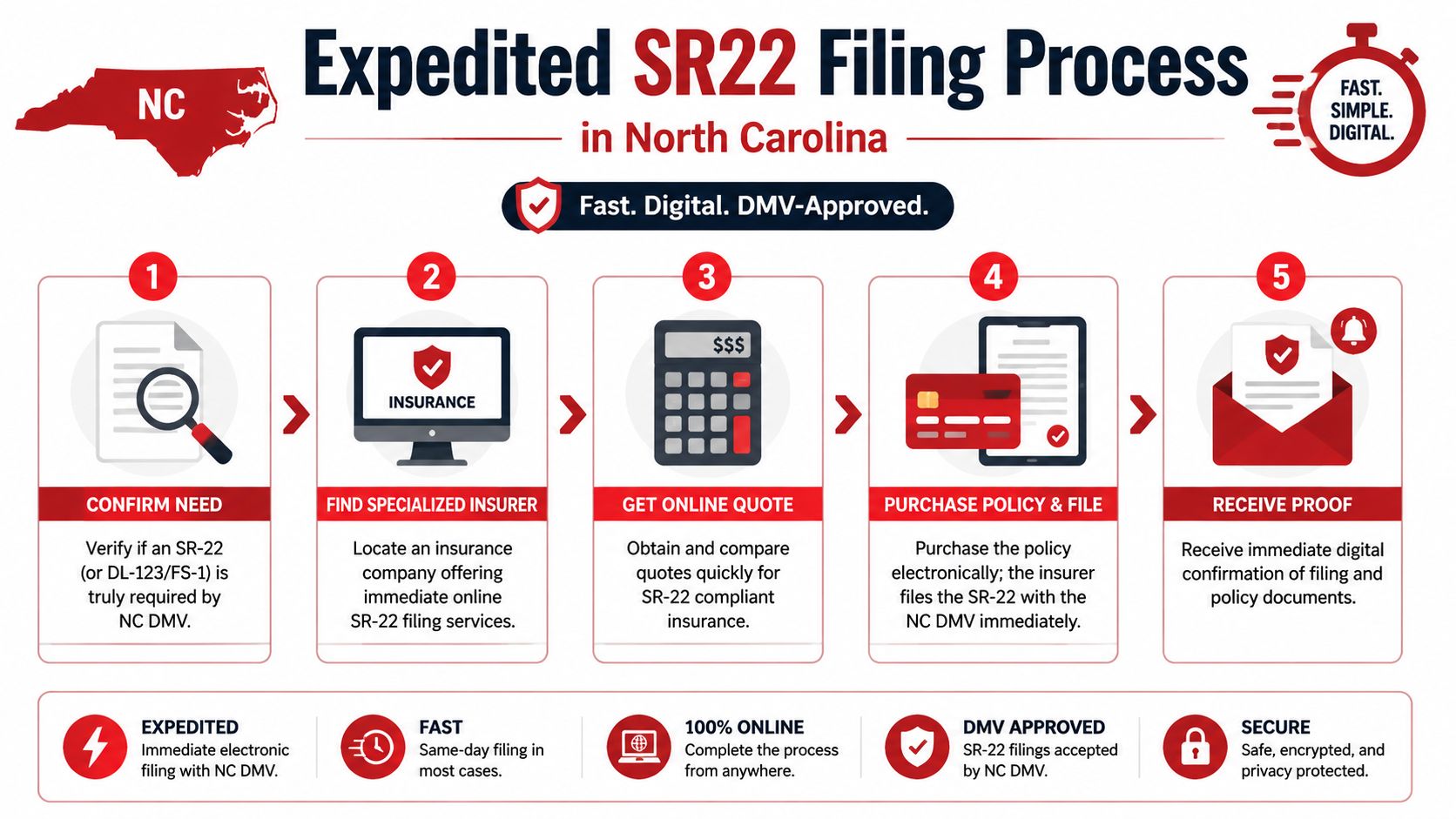

The Fastest Path to an Immediate SR22 Filing

Once you've confirmed that Immediate SR22 filing in North Carolina is the right move, the process should be quick and digital. In North Carolina, the practical workflow is to verify the required form, bind a policy, and have the insurer transmit the filing electronically to the NCDMV. Same-day electronic filing is available from specialized agencies, and that matters because if the policy lapses, the state can be notified and the reinstatement clock can restart, according to North Carolina filing workflow guidance.

Information to gather first

Have everything ready before you call or request a quote. That's what cuts hours out of the process.

Bring together:

- Identity details: your legal name, date of birth, driver's license number, and current address.

- Violation details: what triggered the filing, when it happened, and which state is requiring it.

- Vehicle details: if you own a car, have the year, make, model, and VIN.

- Reinstatement details: any DMV letter, case number, or notice telling you what form is required.

If you don't have every document, don't freeze. Start with what you do have and let the agent tell you what's missing.

What speeds up same-day filing

The fastest filings happen when the insurer can quote, bind, and file electronically without waiting for manual corrections. That means you should look for an agency that already handles high-risk placements and knows how North Carolina filings work.

This is also where an independent agency helps. Instead of forcing one option to fit, the agent can look for a carrier that accepts the violation type, the driver history, and the form requirement. If you want to start that process immediately, you can request an SR-22 quote in North Carolina and have an agent review the filing need before the policy is issued.

The fastest filing is usually the one with the fewest corrections, not the one with the shortest application.

Here's what slows people down:

- Wrong form request: asking for SR-22 when the DMV needs DL-123 or FS-1.

- Incomplete application: missing license number, violation state, or vehicle information.

- Waiting to pay: the filing usually doesn't move until the policy is bound.

- Shopping without context: if you don't mention reinstatement, the quote may not be structured correctly.

How the electronic filing works

After the policy is issued, the insurer sends the SR-22 electronically to the NCDMV. That's the key shift from the old paper process. You don't print the form and carry it to the state as a substitute for the insurer's filing.

Then you handle the remaining reinstatement items. That can include fees, court requirements, or other DMV conditions tied to your case. Filing the insurance proof is a major step, but it isn't always the only one.

My advice is simple. Ask the agent two direct questions before you pay: "Can you file electronically today?" and "What exact form are you filing for me?" If the answer isn't clear, keep asking.

Understanding the Costs and Coverage Requirements

Most drivers focus on the SR-22 filing fee first. That's understandable, but it's usually the smaller piece of the bill. In North Carolina, an SR-22 is typically required for 3 years, the filing fee is usually about $15 to $25, the policy must meet 30/60/25 minimum liability limits, and a lapse can cause that 3-year clock to restart, based on North Carolina SR-22 requirements.

What you actually pay for

Think of the cost in two buckets.

The first is the filing itself. That's usually a small administrative charge. It matters, but it usually isn't what strains your budget.

The second is the premium. That's where the actual impact shows up because the filing usually follows a violation that places you in a higher-risk category.

A lot of drivers get frustrated here because they think the SR-22 is the expensive part. It usually isn't. The violation is what changed the price of insurance.

Coverage that has to stay active

For the filing to remain valid, the policy behind it has to stay active and meet the required liability limits. Under the 30/60/25 minimums, that means:

- $30,000 bodily injury per person

- $60,000 bodily injury per accident

- $25,000 property damage

This isn't the place to gamble with a payment date or cancel mid-term because you found something else. If the policy drops, the state may be notified. That can undo progress fast.

Pay attention to the premium, but protect the continuity. That's what keeps reinstatement from turning into a second suspension.

Common Pitfalls That Delay Reinstatement

Most reinstatement delays come from avoidable mistakes, not complicated law. Drivers assume any insurer can handle the filing correctly, or that a short lapse won't matter. Both assumptions cause problems.

Mistakes that slow everything down

Don't treat a lapse like a small issue.

Do set up autopay or another payment reminder the moment the policy starts. A filing only helps if the coverage remains active.

Don't assume every carrier can handle your case.

Do confirm that the insurer is licensed in the mandating state and that the policy matches the required liability limits. Carrier eligibility and limit matching are two common failure points in a fast filing workflow, according to SR-22 filing guidance for multistate and fast-turn cases.

Don't try to "self-file."

Do let the insurer transmit the form. These filings are built around insurer submission, not DIY paperwork.

Don't ignore interstate details.

Do mention if your violation, suspension, or reinstatement requirement involves another state. That changes how the filing has to be handled.

One more inside tip. When you switch policies during a filing period, never cancel the old one before the replacement is active and confirmed. Drivers create their own gap this way, then spend weeks fixing it.

Your North Carolina SR22 Questions Answered

Some of the confusion around SR-22 filings comes from old advice. The process is faster now. Many insurers offer same-day or immediate electronic filing, and North Carolina's auto insurance market is large and competitive, with total direct premium written increasing 112% since 2015, according to Progressive's SR-22 overview. That means drivers usually have options if they move quickly and ask for the right filing.

Can I get coverage if I don't own a car

Yes, in many cases you can use a non-owner policy if your goal is to satisfy a filing requirement and reinstate your license. This is common for drivers who sold their car, share rides, or aren't ready to buy another vehicle yet.

The key is making sure the policy type matches the DMV requirement. Non-owner coverage can solve the problem, but only if the insurer files the correct form.

What if I move out of North Carolina

You still need to satisfy the original requirement properly. Don't assume moving ends it. If another state is involved, keep the insurer informed so the filing and policy remain compliant.

State differences often cause confusion. If your obligation started in North Carolina or another mandating state, handle the move as an insurance compliance issue, not just an address change.

How do I know when the filing can end

Track your requirement carefully and confirm with the DMV before asking to remove any filing. Don't guess. Removing it too early can create a new problem right when you think you're done.

Keep your documents, payment history, and reinstatement paperwork together in one place. That makes it much easier to confirm your status and avoid a preventable reset.

If you need help with Immediate SR22 filing in North Carolina, Select Insurance Group, Inc. can connect you with a licensed agent who can review your reinstatement paperwork, identify whether you need an SR-22, DL-123, or FS-1, and help place a policy with electronic filing when available. The agency works with multiple carriers, offers bilingual support, and can help you move quickly without guessing at the wrong form.