You've got the truck. The authority is active or almost active. A broker packet lands in your inbox, and suddenly “just get insurance” turns into a stack of questions that don't have simple answers. You find one quote that satisfies the law, another that's much higher, and a third that includes coverages you weren't planning to buy. At that point, most Florida truckers realize the hard truth. Insurance isn't just a permit to operate. It's a filter that decides whether you can book freight, protect equipment, and stay in business after a bad day.

That confusion is common in Florida. A new owner-operator may be legal on paper and still get rejected by a broker. A fleet manager may have the right liability limit but still carry avoidable gaps around cargo, physical damage, or non-owned trailer exposure. The state's insurance rules, federal filings, contract requirements, and premium pressure all collide fast.

That's where a practical guide helps. The goal isn't to throw policy jargon at you. It's to show what matters, where truckers usually get tripped up, and how to make coverage decisions that support revenue instead of blocking it.

Table of Contents

- Your Guide to Trucking Insurance in Florida

- Navigating Florida and Federal Trucking Insurance Rules

- Essential Trucking Insurance Coverage Types Explained

- Owner-Operators vs Fleets A Tale of Two Policies

- What Determines Your Florida Trucking Insurance Cost

- Practical Tips to Lower Your Trucking Insurance Premiums

- Get the Right Coverage with Select Insurance Group

Your Guide to Trucking Insurance in Florida

A lot of trucking insurance problems in Florida start the same way. A carrier asks for a certificate by the end of the day. The trucker has a quote in hand, but it's not clear whether that quote is enough for the freight they want to haul. One policy satisfies registration and filings. Another looks more expensive but may be the one that qualifies them for the load.

Florida makes that tension sharper. Truckers deal with dense traffic, aggressive claim environments, and contract terms that often go beyond the bare legal standard. If you're shopping for trucking insurance in Florida, you're not just buying compliance. You're trying to protect cash flow, equipment, and access to freight.

What truckers usually get wrong first

The first mistake is assuming the cheapest legal option is the practical option. It often isn't.

The second mistake is treating insurance like a single number. Liability matters, but so do cargo terms, physical damage deductibles, bobtail exposure, driver schedules, and how the policy matches the way the truck runs. A local box truck, a dump truck in construction zones, and a long-haul tractor won't be underwritten the same way.

Legal doesn't always mean contract-ready. In Florida trucking, that gap causes more frustration than most new operators expect.

A strong policy starts with the operation itself. What do you haul? Who drives? Are you under your own authority or leased on? Do you need coverage for dispatch and non-dispatch miles? Those answers shape the right policy faster than any online shortcut.

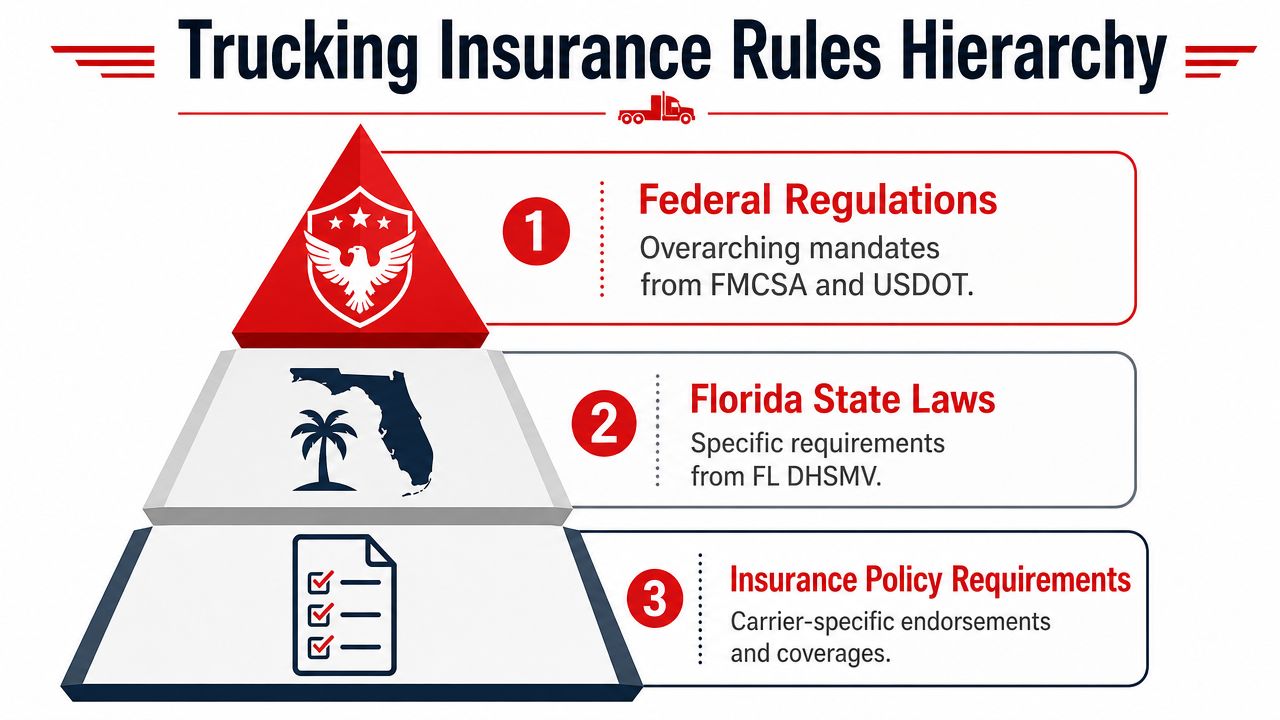

Navigating Florida and Federal Trucking Insurance Rules

A Florida carrier can be legal on paper in the morning and still lose a load by lunch because the insurance certificate does not meet the broker's requirement. I see that gap all the time. The state minimum may satisfy one rule. The freight market usually expects more.

Florida trucking insurance works in layers. Federal filing rules apply to many for-hire interstate carriers. Florida adds vehicle-based financial responsibility rules. Then contracts add a third layer, and that is often where owner-operators get caught short.

Federal limits set the legal floor

For many interstate for-hire operations, federal financial responsibility starts at $750,000 in liability for general freight. Oil hauling can require $1,000,000, and certain hazardous materials can require $5,000,000, according to this Florida trucking insurance requirement overview.

Those numbers matter for authority and filings. They do not guarantee access to freight.

In practice, many brokers and shippers want to see $1 million in liability before they will tender a load. That extra limit is where compliance and profitability start to separate. A carrier that buys only to the legal minimum may save premium upfront and still miss better-paying opportunities because the certificate does not qualify.

Florida rules still matter

Florida also applies state financial responsibility rules based on vehicle weight, and commercial vehicles can carry separate state requirements such as Personal Injury Protection and Property Damage Liability, as noted in the source above. For intrastate operators, local fleets, and trucks that are not running under the same authority structure as an interstate carrier, those state rules still need to be set up correctly.

Policy details matter. The named insured has to match the business entity. The unit schedule has to match the truck on the road. The operating radius, commodity type, and use of the vehicle have to match the work you do. If any of that is off, a certificate can get rejected or a claim can turn into a coverage dispute.

The practical standard is higher than the legal standard

Here is the clearest way to handle this. Build the policy for the freight you want to haul, not just the minimum needed to stay legal.

For many Florida truckers, that means asking four questions before buying coverage:

- Are you running interstate, intrastate, or both?

- Are you hauling general freight, regulated commodities, or hazmat?

- Will brokers or shippers require $1 million in liability?

- Do your contracts also require cargo coverage, trailer interchange, or other supporting terms?

If cargo is part of the contract, review how those requirements usually work before binding coverage. Our guide to cargo insurance for truckers helps clarify what brokers and shippers often expect beyond liability alone.

Legal minimums keep the authority in line. Contract-ready coverage keeps the truck loaded. The difference affects revenue, not just compliance.

Essential Trucking Insurance Coverage Types Explained

A trucking policy only works if it protects the operation you run. The legal minimum gets the conversation started, but the coverage mix determines whether you can survive cargo damage, equipment loss, off-dispatch driving, or a contract review from a broker.

Coverage that keeps a trucking business standing

Primary liability is the core policy piece. It responds when your truck causes bodily injury or property damage to others in a covered accident. If you're hauling for hire, this is the coverage everyone asks about first because without it, you won't get very far in the market.

Cargo insurance protects the freight you're transporting, subject to the policy's terms and exclusions. This becomes a real issue the moment a load is damaged, stolen, or compromised in transit. If you haul freight under contracts that require cargo protection, this isn't optional in practical terms. If you need a deeper look at how cargo works in a trucking policy, review this guide to cargo insurance for truckers.

Physical damage covers your truck, and often your trailer if scheduled, for covered collision and losses from incidents other than collision. This is what keeps a lender satisfied and helps you recover when the damage is to your own equipment rather than someone else's property.

Bobtail or non-trucking liability matters most for leased owner-operators. If your motor carrier's coverage only applies while you're under dispatch, there may be a gap during certain non-dispatch use. That gap is where many truckers wrongly assume they're covered.

Occupational accident coverage comes up when an owner-operator doesn't have workers' compensation protection through another structure. It's often part of the broader risk discussion for independent truckers who need a backstop for injury-related costs.

The million-dollar gap that stops loads

One of the biggest blind spots in trucking insurance Florida buyers face is the difference between what the law allows and what the market expects. A key friction point is that most brokers require $1,000,000 in auto liability regardless of the legal floor, even though federal mandates may range from $750,000 to $5,000,000 depending on cargo, according to this Florida commercial insurance requirements analysis.

That gap is where many new ventures stall. They buy enough insurance to be legal, then discover they still can't get approved for the freight they were planning to haul.

Strategic planning is important. Buying to the lowest legal number can reduce upfront premium, but it can also reduce earning options. Buying blindly to the highest number without reviewing your operation can mean overpaying for the wrong structure. The better move is to line up liability limits, cargo needs, and certificate expectations with the type of freight and broker relationships you intend to pursue.

If your policy passes compliance but fails the broker packet, it's not really ready for the road.

Florida Trucking Insurance Coverage at a Glance

| Coverage Type | What It Protects |

|---|---|

| Primary Liability | Injury or property damage claims you cause to others in a covered accident |

| Cargo | Freight loss or damage during covered transit |

| Physical Damage | Your truck or trailer for covered collision and non-collision loss |

| Bobtail or Non-Trucking Liability | Certain liability exposure outside dispatch, depending on lease and policy wording |

| Occupational Accident | Injury-related protection often considered by independent operators |

Owner-Operators vs Fleets A Tale of Two Policies

The insurance conversation changes fast depending on whether you run one truck or manage several. The exposure is different. The paperwork is different. The mistakes are different too.

The independent owner-operator problem set

An owner-operator running under their own authority usually feels the pressure first in premium and contract access. The policy has to satisfy filings, equipment protection, and day-to-day survival, all while leaving enough margin to run the business. The wrong deductible, a missing coverage line, or a bad assumption about non-dispatch miles can hurt quickly.

The biggest divide for solo operators is often this question. Are you leased on to a motor carrier, or are you running independently? If you're leased on, the carrier's insurance may cover certain dispatched operations, but it may not cover every mile you drive. If you're independent, the policy has to stand on its own across liability, equipment, cargo, and certificates.

For truckers in that lane, this guide to owner-operator semi-truck insurance is useful because it frames the decision around how the truck is operated, not just what kind of truck it is.

What changes for fleets

Fleet managers have a different job. They aren't just insuring vehicles. They're managing driver quality, unit schedules, internal controls, and claim frequency across the whole account.

A fleet policy tends to become a management tool. Clean driver onboarding, documented safety expectations, and clear equipment assignments can make the account easier to place and easier to defend during renewal. A small fleet with disciplined operations often presents better than a loosely managed fleet with inconsistent records.

Here's the simple contrast:

- Owner-operators: Coverage choices are tightly connected to personal income, loan obligations, and whether one truck can keep producing.

- Fleets: Coverage decisions affect staffing, scheduling, claims handling, and how insurers view the account over time.

- Both: The policy has to reflect the actual operation, not the shortcut version used to get a quick quote.

What Determines Your Florida Trucking Insurance Cost

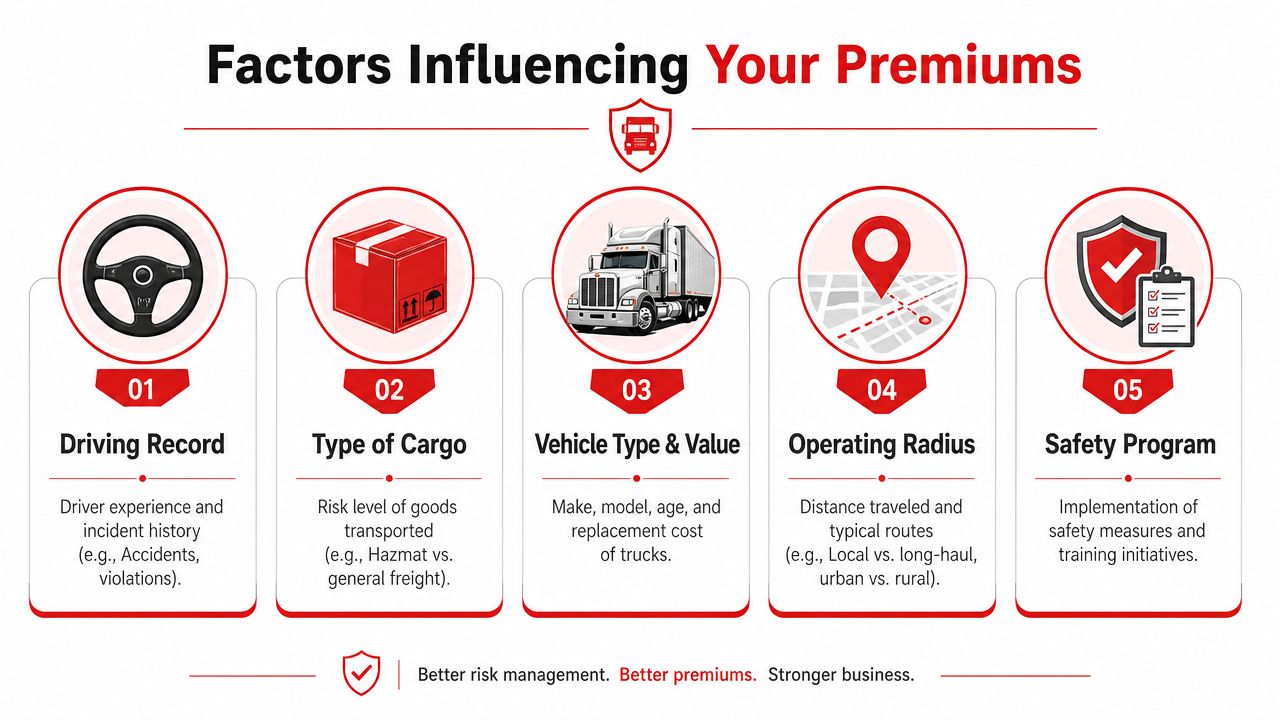

Florida pricing is rarely driven by one thing. Underwriters look at the whole file, then decide how much exposure they're taking on. Route type, vehicle type, cargo, authority status, driver profile, and claims history all pull on the premium at the same time.

Why Florida pricing stays tough

Florida consistently ranks among the states with the highest commercial truck insurance premiums. Owner-operators pay an average of $12,872 annually for local routes and $19,480 for national coverage in 2026, and insurance costs per mile increased 43% from 2019 to 2025, according to this commercial truck insurance cost analysis.

That pressure shows up differently depending on the account. A trucker with local lanes may still face heavy pricing if the garaging location, unit type, and driver file concern the underwriter. A long-haul operator may see cost move for radius and exposure alone. Premium isn't random, but it can feel that way when buyers don't know what the insurer is reacting to.

The underwriting levers that move your premium

The most important cost drivers usually look like this:

- Driver history: A clean, stable driver file gives underwriters more confidence than a file with recent issues or thin experience.

- Cargo profile: General freight is one thing. More specialized or sensitive hauling is another. The type of commodity changes both liability and cargo concerns.

- Vehicle and equipment value: Expensive equipment means more physical damage exposure. Specialized units can also narrow the number of carriers willing to write the risk.

- Operating radius and territory: Local, regional, and national runs don't produce the same exposure pattern. Dense urban driving can also affect how the account is viewed.

- Safety controls: Documented procedures, telematics, dashcams, and active driver oversight can improve how an underwriter reads the file.

If you want a broader breakdown of pricing logic, this overview of the average truck insurance cost helps frame what changes from one account to another.

Premium follows exposure. The fastest way to improve pricing is to make the operation easier to understand and easier to trust.

Why dump trucks often price differently

Dump truck buyers in Florida run into a separate problem. The premium can look high relative to the vehicle itself, and the explanation they get is often too vague to be useful.

One documented example is that dump truck insurance in Florida averages $15,000 annually for an $80k vehicle, while the national average for new transport trucks is described as $746 to $954 per month, according to this Florida truck insurance overview. The practical takeaway isn't just the number. It's that vocational trucking in Florida often gets priced on a different risk profile than standard freight movement.

Why? Usually because the operation itself looks different to the insurer. Construction-zone driving, rollover exposure, stop-and-go work, and a narrower market for higher-risk vocational units all affect appetite. That's why truckers comparing a dump truck to a highway tractor often feel like they're shopping in two different insurance markets.

Practical Tips to Lower Your Trucking Insurance Premiums

Florida trucking insurance is expensive, but expensive doesn't mean uncontrollable. Many buyers treat premium as fixed. It isn't. You may not be able to change the state, the legal environment, or the insurance market, but you can change how your account looks to underwriters.

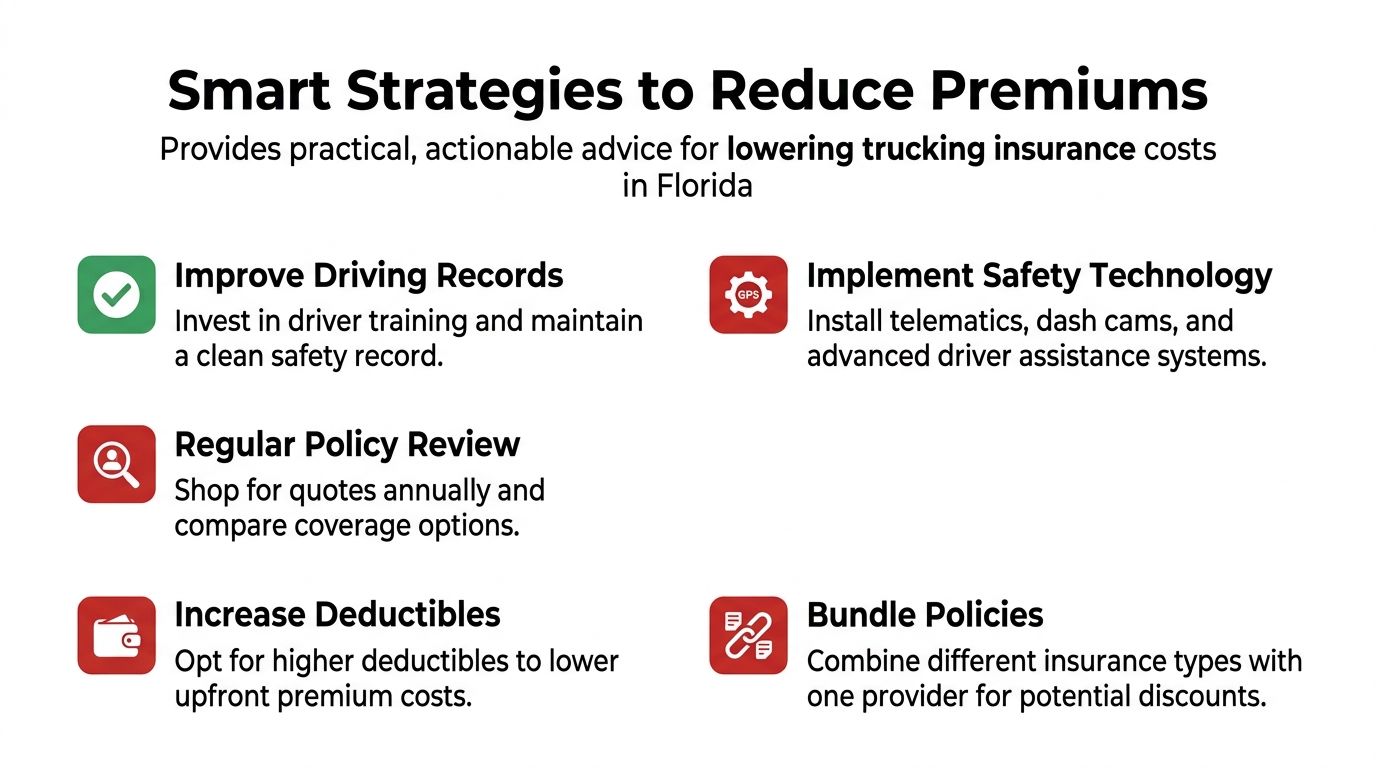

Control the parts underwriters can actually reward

Start with operations, not shopping. If the driver list is weak, the truck schedule is sloppy, and the loss story is unclear, quote comparisons won't solve the problem.

- Improve driver quality: Clean hiring standards and ongoing driver accountability matter. Underwriters pay attention to who's behind the wheel.

- Use safety technology: Dashcams, telematics, and active monitoring can strengthen the account story when they're used, not just installed.

- Review the policy before renewal pressure hits: A rushed submission often produces rushed options. Good quote prep gives more room to fix issues before the deadline.

Lower premium without creating a bad policy

Some savings moves help. Some only look good until a claim happens.

A higher deductible can reduce premium, but only if the business can comfortably absorb that out-of-pocket hit. If a deductible saves money on paper but creates cash stress after a loss, it wasn't a smart savings move. The same goes for stripping out useful coverage to make the quote look cheaper.

A better approach is to match the policy to the operation with discipline:

- Bundle where it makes sense: Keeping related business coverage with one provider can simplify servicing and may help the overall account.

- Pay attention to dispatch and non-dispatch exposure: Don't remove a coverage line just because you haven't used it yet.

- Fix the submission quality: Complete driver details, accurate unit values, and clear operating descriptions can prevent avoidable pricing friction.

A cheap trucking policy is expensive if it blocks freight, misses a contract requirement, or leaves your truck uncovered after a loss.

Get the Right Coverage with Select Insurance Group

Florida trucking insurance is difficult for three reasons. The rules are layered, the premiums are high, and the market often expects more than the law requires. The trucker who only shops for the lowest number usually finds that out after a broker rejects the certificate or after a claim exposes a gap.

That's why the quote process has to start with the actual operation. Not a rough summary. Not a guessed radius. Not “general freight” as a catch-all answer for everything. The more accurately the policy reflects the trucks, drivers, authority, cargo, and contract demands, the better chance you have of getting coverage that works in real life.

Select Insurance Group, Inc. helps truckers and fleet operators compare options from 20 to 40 leading carriers, offers over 30 years of experience across the Southeast market, and provides bilingual support for customers who want guidance in English or Spanish. That combination matters when you need speed, competitive options, and someone who understands how Florida trucking accounts are underwritten.

Before requesting a quote, have these items ready:

- USDOT and MC information: If applicable to your operation

- Driver details: Names, license information, and background details relevant to underwriting

- Vehicle information: Year, make, model, VIN, values, and garaging address

- Cargo and route details: What you haul and where you run

- Current policy or renewal paperwork: If you're replacing existing coverage

- Any broker or shipper insurance requirements: So the quote can be built correctly from the start

If you need trucking coverage that matches Florida rules, broker expectations, and the way your business runs, contact Select Insurance Group, Inc. for a fast, free, no-obligation quote. Their team can review your USDOT details, driver information, vehicle schedule, and coverage needs, then help you compare practical options without wasting time on policies that won't fit your operation.