You hire your first employee in Florida, or you land a new job and need a certificate before anyone steps on site. That's usually when workers comp stops feeling like background paperwork and starts feeling urgent. Most small business owners don't struggle with the idea of protecting employees. They struggle with the rules, the timing, and the cost.

That's where Florida gets tricky. The answer depends on what kind of business you run, who counts as an employee, whether anyone has filed an exemption, and how your payroll is classified. If you get any of that wrong, you can end up with the wrong policy, the wrong price, or no policy at all when you legally need one.

The practical way to handle workers compensation insurance in Florida is simple. Figure out whether the law requires it, understand what the policy covers, gather the right business details, and work with someone who can compare options clearly. On the operations side, many owners also pair coverage with safety procedures and incident tracking so injuries are less likely to happen in the first place. A tool like Safety Space's H&S management platform can help organize that part of the process.

Table of Contents

- What Is Florida Workers Compensation Insurance

- Florida Workers Comp Rules You Must Know

- Understanding Your Coverage and Exemptions

- How Workers Comp Insurance Costs Are Calculated

- Getting Your Florida Workers Comp Policy Step-by-Step

- Navigating a Workers Comp Claim

- Penalties for Non-Compliance and High-Risk Industry Tips

- Let Select Insurance Group Handle the Details

What Is Florida Workers Compensation Insurance

Florida workers compensation insurance is a business policy that responds when an employee gets hurt or becomes ill because of work. In practical terms, it helps pay for medical care and supports wage-related benefits while the employee is out recovering. It also creates a structured claims process, which matters a lot when an injury happens on a busy jobsite or during a normal workday.

For a small business owner, this policy does two jobs at once. It protects the employee by making sure there's a system for treatment and benefits. It also protects the business by shifting a workplace injury out of an improvised, stressful conversation and into a formal insurance claim.

A lot of owners first look into workers comp because a customer asks for proof of coverage, a payroll company flags the issue, or a contractor won't release a job without a certificate. That's common. But the businesses that handle this well don't treat it as a box to check. They treat it as part of hiring, subcontractor management, and day-to-day risk control.

Practical rule: If an injury would create financial chaos for the employee or the business, workers comp isn't optional in any meaningful sense, even before you get to the legal side.

The hard part isn't understanding why the policy exists. The hard part is applying Florida's rules correctly. Construction businesses face one set of triggers. Non-construction businesses face another. Exemptions can change who must be covered, but only if they're handled properly. Cost depends on payroll, job duties, and claims history, not just a flat business type.

That's why owners need a roadmap, not a definition. You need to know when coverage is required, what's covered, what can be excluded, how insurers price the policy, and what to do when a claim happens.

Florida Workers Comp Rules You Must Know

Florida doesn't use a one-size-fits-all rule. The legal requirement depends first on your industry and then on how many employees you have.

Who has to carry coverage

According to the Florida Division of Workers' Compensation requirements, businesses in the construction industry must carry workers' compensation insurance if they have one or more employees, including the owner if the business is a corporation. Non-construction employers must provide coverage if they have four or more employees.

That sounds simple until you apply it in real life. A small office with a few staff members may not need the policy right away, but a construction business can trigger the requirement almost immediately. Owners often assume part-time help doesn't count or that a family-run business is automatically outside the rule. That's where mistakes start.

A quick threshold table

| Industry Type | Employee Threshold to Require Coverage |

|---|---|

| Construction | One or more employees |

| Non-construction | Four or more employees |

The cleanest way to think about it is this:

- Construction businesses: The threshold is low, so you should check your status before hiring or before starting a project.

- Non-construction businesses: Don't wait until payroll is already running to figure it out. If your team is growing, review the requirement early.

- Corporate owners in construction: The owner can count in ways people don't expect, especially when the business is structured as a corporation.

Where owners get tripped up

The biggest issue I see is not bad intent. It's bad assumptions. A business owner hears “I only have a small crew” and assumes workers comp can wait. Another owner pays a few people irregularly and assumes they don't count because the arrangement feels casual. Florida doesn't reward casual recordkeeping.

Here's what works better:

- Classify your business accurately. If the work is construction, treat it as construction from the start.

- Count your working people carefully. Don't rely on memory. Review payroll, owner status, and who is actively performing labor.

- Check before contracts are signed. If a customer requires proof of insurance, you don't want to discover a compliance problem the day work begins.

A lot of workers comp problems start long before a claim. They start when the business is set up informally and nobody documents who is doing what.

Another common mistake is confusing legal obligation with contract obligation. Even if your employee count hasn't triggered a requirement yet, a landlord, general contractor, or commercial client may still require a policy before they'll work with you. That's not the same question as whether Florida law requires coverage, but it matters just as much if you're trying to win and keep business.

Understanding Your Coverage and Exemptions

Once you know you need a policy, the next question is practical. What does it do for your business and your employees?

What the policy does when someone gets hurt

Think of a workplace injury in two versions.

Without coverage, the employer is suddenly trying to manage medical treatment, time away from work, reporting, documentation, and the financial pressure that follows. Emotions run high. Facts are unclear. Everyone wants answers immediately.

With a workers comp policy in place, there's a process. The claim gets reported. The carrier steps in. The employee has a path to treatment and benefits tied to the work injury. The employer isn't inventing a response in real time.

In everyday terms, the policy is built to respond to work-related injuries and occupational illnesses. It generally addresses medical care connected to the injury, rehabilitation when needed, and disability-related wage support when the employee can't work during recovery.

That's why this policy matters even for businesses with good safety habits. Careful businesses still have slips, lifting injuries, repetitive motion problems, vehicle-related incidents, and jobsite accidents. Insurance doesn't prevent those events. It gives you a system for handling them.

How exemptions actually work

Florida business owners often confuse this aspect. An exemption is distinct from deciding not to cover someone. It's an active legal step for certain people in certain business structures.

Depending on how the business is set up, some owners or officers may be able to file for an exemption. Common examples people ask about include sole proprietors, partners in an LLC, or corporate officers in a non-construction company. Whether an exemption is available depends on the person's role and the business structure. The key point is that it must be handled properly. It isn't automatic.

That distinction matters because owners sometimes say, “I'm exempt,” when what they really mean is, “I assumed I didn't need coverage for myself.” Those are not the same thing.

Use this decision lens before filing:

- Risk tolerance: If you're exempt and you get hurt, there may be no workers comp policy responding for you.

- Contract demands: Some customers want everyone involved in the operation covered, even if an exemption is legally available.

- Business continuity: If a key owner gets injured and there's no protection in place, the business can stall fast.

Owner insight: An exemption can reduce who is covered. It doesn't reduce the real-world cost of an injury.

What usually works is reviewing exemptions as part of a broader coverage strategy, not as a quick way to save money. For some owners, an exemption makes sense. For others, it creates a gap they only understand after something goes wrong.

Also remember that exemptions don't fix classification or payroll problems. If the business should be carrying a policy for its workforce, an owner exemption doesn't erase that obligation. It only affects the specific person who qualifies and properly files.

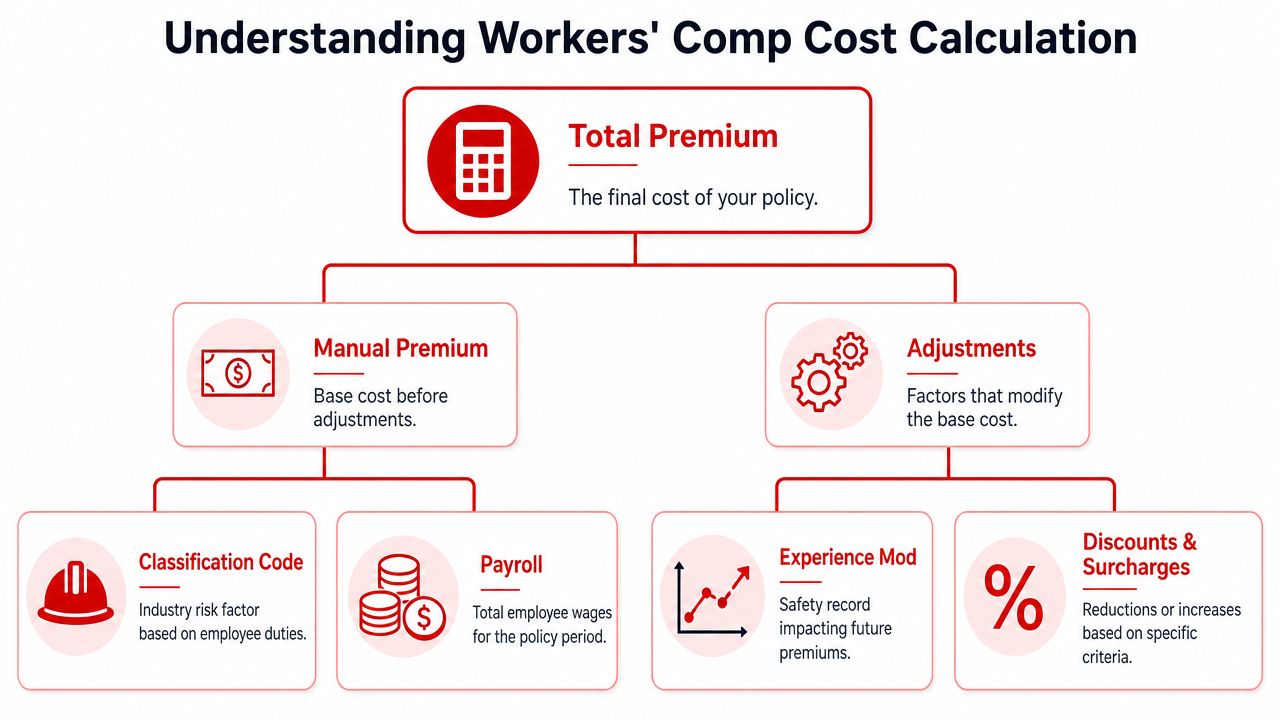

How Workers Comp Insurance Costs Are Calculated

Workers comp pricing feels mysterious until you break it into parts. Once you do that, it starts to look less like a random premium and more like a formula built from your payroll and job risk.

Think of pricing as a recipe

The usual pricing framework is easiest to understand as a recipe:

- Payroll: How much covered payroll the insurer expects during the policy period

- Classification code: The type of work employees perform

- Experience modification factor: A claims-history adjustment for eligible businesses

Those pieces combine to produce the policy's base cost, and then other adjustments can affect the final premium. If your team includes both office staff and field labor, those duties shouldn't be lumped together casually. Accurate classification matters because insurers price different job types differently.

This visual captures the structure well:

A lot of owners focus only on the premium number. The better move is to ask what assumptions built that number. Was payroll estimated correctly? Were employee duties described accurately? Was clerical work separated from field work where appropriate? Those answers often matter more than the first quote itself.

What changes the final premium

Claims history plays a role over time, which is why safety practices and early reporting matter. For businesses trying to understand how past losses can affect future pricing, this overview of experience rating vs community rating is a helpful way to understand the general concept behind rating approaches.

Florida business owners should also know that pricing conditions can shift at the state level. The Florida Office of Insurance Regulation announced a statewide average rate decrease of -5.7% for workers' compensation policies effective January 1, 2026, marking the seventh consecutive year of rate decreases. That doesn't mean every individual business will pay less. It means statewide approved rates moved downward on average, while each policy still depends on its own payroll, classifications, and loss profile.

Here's what usually raises costs unnecessarily:

- Blended job duties: Everyone gets assigned to a higher-risk classification because records are vague.

- Bad payroll estimates: The business underestimates payroll up front, then gets hit with an audit adjustment later.

- Weak claim management: Small injuries turn into messy claims because no one documented what happened or followed return-to-work procedures.

And here's what tends to work better:

- Separate roles clearly: Keep office, sales, and field duties documented.

- Track payroll by job type: Don't wait until audit time to reconstruct the year.

- Run a real safety process: Insurers can't price around preventable chaos forever.

Getting Your Florida Workers Comp Policy Step-by-Step

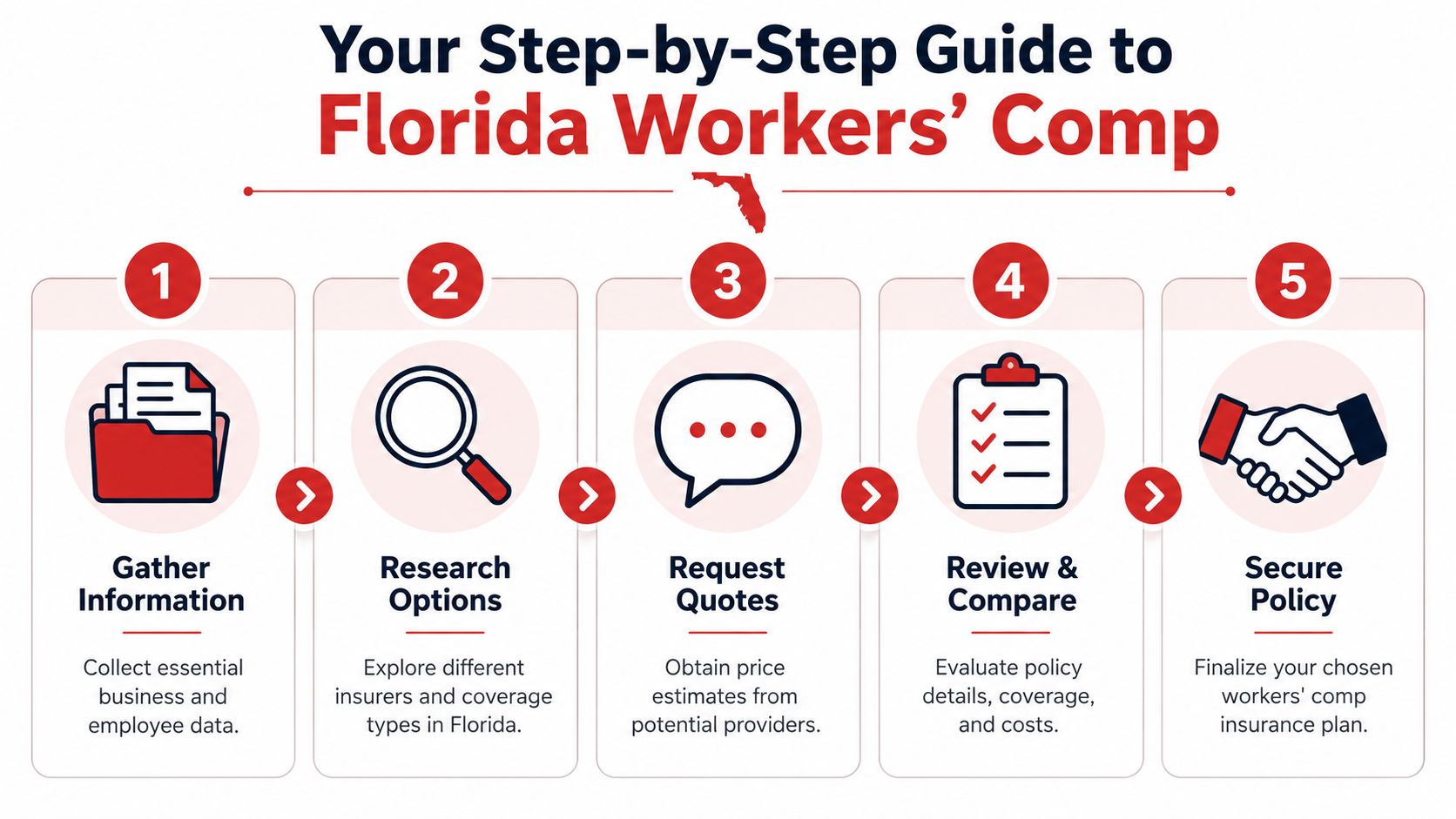

Buying the policy is usually less complicated than owners expect. The part that causes delays is missing information, unclear business descriptions, or trying to compare quotes without matching the same facts across carriers.

Step one through step three

Start by gathering the basics before you request a quote.

Gather your business details. Have your legal business name, address, federal tax ID, business structure, and a plain-English description of what the company does. If you use subcontractors, be ready to explain that too.

Build a payroll snapshot. Insurers need estimated payroll for the coming policy period, broken down by employee role. If one person splits time between office work and field work, document that carefully rather than guessing later.

Work with an independent agent. This matters more in Florida than many owners realize because different carriers may view the same operation differently. An independent agency can compare options across multiple insurers instead of forcing your business into one company's appetite. If you're reviewing broader business coverage at the same time, this guide to small business insurance in Florida can help frame how workers comp fits with your other policies. One available option is Select Insurance Group, Inc., which operates as an independent agency and compares multiple carrier quotes for business insurance needs.

The fastest quote process usually comes from the owner who can explain the business clearly in one minute and back it up with payroll records.

Step four and step five

Once quotes come in, don't look only at price.

Review the classification assumptions, named operations, included states if applicable, and any conditions tied to the quote. A cheap quote built on the wrong payroll or wrong class code isn't a bargain. It's a setup for problems at audit or claim time.

Then bind the policy and get your certificate of insurance. That certificate is often what customers, landlords, or contractors want to see. Keep it accessible because you'll likely need to send it more than once.

There's one more step many owners don't plan for. The premium audit.

At the end of the policy term, the insurer may review your actual payroll and operations to compare them against what was estimated at the start. If payroll was higher than expected or work duties changed, the premium can be adjusted. If your estimates were too high, there may be a credit. The audit isn't a punishment. It's how the carrier trues up the policy to what really happened during the year.

To make the audit easier:

- Keep payroll reports organized

- Store certificates for subcontractors

- Document role changes during the year

- Separate owners, clerical staff, and field employees cleanly where applicable

Owners who treat workers comp as a living business record, not a one-time purchase, usually have a smoother renewal.

Navigating a Workers Comp Claim

An injury at work creates confusion fast. Someone needs medical attention. Supervisors are trying to understand what happened. The employee may be shaken up or worried about missing work. A calm process proves beneficial in these moments.

The first few hours matter most

Start with care. If the injury is serious, get immediate medical attention. Once the employee is safe, gather the basic facts while they're still fresh. What was the employee doing, where did it happen, who saw it, and was any equipment involved?

Then report the injury to the carrier promptly. Florida employers are generally expected to report the injury to the insurance carrier within seven days after learning of it, as described in the background material provided for this article. In practice, sooner is better. Delay makes everything harder, especially if treatment questions or witness accounts start drifting.

A good first-response checklist looks like this:

- Get treatment arranged: Don't debate fault before care is addressed.

- Write down the facts: Time, location, task being performed, and names of witnesses.

- Notify the carrier quickly: Early reporting gives the claim a cleaner start.

- Preserve records: Photos, supervisor notes, and any incident reports should stay organized.

For employees who want a plain-language overview of the personal side of the process, this guide on what to do after a work injury can help them understand the immediate next steps.

What the carrier will need from you

Once the claim is opened, the insurer will usually want documentation and cooperation, not guesswork. That means wage details, accident information, employee identification, and any incident records you already have. If the business has return-to-work options, raise that early because modified duty can help everyone if it fits the medical restrictions.

What doesn't work is trying to “wait and see” on a claim that already looks real. Owners sometimes hope a minor injury will fade away, so they hold the report. That can create bigger disputes later, especially if the employee seeks treatment after the facts have gone cold.

Report first, sort out the details second. A claim with missing details can still be managed. A claim reported late is harder to defend and harder to administer.

The employee's role is simpler than many people think. They should report the injury, follow authorized treatment directions, and keep the employer informed about work status. The employer's role is to document, report, and cooperate. The carrier's role is to investigate the claim and administer benefits according to the policy and applicable rules.

Penalties for Non-Compliance and High-Risk Industry Tips

Ignoring workers comp usually starts as a delay. Then it turns into an expensive problem at the worst possible time.

Why waiting is a bad bet

If your Florida business is required to carry workers comp and doesn't, the state can shut operations down through enforcement action. That alone should get any owner's attention. A stop-work order can freeze revenue overnight while payroll, rent, and contract obligations keep running.

Financial consequences can follow too, and they're rarely mild. Even without getting lost in penalty math, the practical message is clear. Non-compliance costs far more than setting the policy up correctly in the first place.

For contractors and trades, the exposure is even sharper because jobs often involve site access rules, upstream contract requirements, and subcontractor oversight. If your operation falls into that category, this page on insurance for contractors is a useful starting point for thinking about workers comp alongside general liability and other jobsite coverage.

Practical habits for higher-risk businesses

Construction, trucking, and hands-on field operations usually don't get in trouble because the owners never heard of workers comp. They get in trouble because the paperwork falls behind the actual operation.

A few habits prevent a lot of problems:

- Collect subcontractor certificates before work starts: Don't chase them after an injury or after an audit notice.

- Match payroll to real duties: If someone moved from office support to field work, your records should show it.

- Run safety meetings consistently: Even simple, documented routines can improve how crews work and how claims are defended.

- Treat near-misses seriously: They often reveal the exact weakness that causes the next actual claim.

The businesses that stay out of trouble usually do boring things well. They document. They verify. They update records before the state, the carrier, or the customer asks.

Let Select Insurance Group Handle the Details

Florida workers comp isn't hard because the idea is complicated. It's hard because small errors stack up. A business gets classified loosely, payroll is estimated too casually, an exemption is misunderstood, or a certificate is needed faster than anyone expected.

That's where having an independent agency helps. Instead of treating workers comp as a standalone purchase, it's better to treat it as part of how your business hires, bids jobs, manages records, and responds to claims. If bilingual service matters for your team or ownership group, that support can also make the process smoother from quote to claim.

If you want a clearer sense of why that model matters, this explanation of what an independent insurance agency does lays out the difference in practical terms. Being able to compare carriers, explain classifications clearly, and communicate in English or Spanish is often what keeps a policy accurate and usable, not just active on paper.

The right setup lets you focus on payroll, contracts, and employees, instead of chasing insurance issues after something has already gone wrong.

If you need help putting workers compensation insurance in Florida in place, Select Insurance Group, Inc. can help you review your business details, compare carrier options, and get the coverage lined up correctly with bilingual support for Florida business owners.