You're probably here because a vehicle question in your business suddenly got real.

Maybe you own a catering company in Georgia and ran to pick up supplies in your personal SUV. Maybe you're a contractor in the Carolinas and your office manager uses her own car to drop off plans at a job site. Then a light turns red, brakes hit late, and a minor fender bender turns into a much bigger question: Will my insurance cover this if I was working when it happened?

That moment catches a lot of owners off guard. They aren't reckless. They're busy. They're trying to serve customers, keep crews moving, and handle one more errand before lunch. But once a car is tied to business activity, the risk changes. The insurance question changes too.

For small businesses in the Southeast, this gets even trickier. Many companies cross state lines for jobs, deliveries, or service calls. Others rely on employees using their own cars for quick business tasks. Those are exactly the situations where coverage gaps tend to hide. You don't notice them until after a claim.

Commercial auto insurance is the tool that helps close those gaps. But the phrase itself can feel broad, technical, and expensive. It helps to break it down in plain language, the same way an experienced advisor would explain it across a desk.

Table of Contents

- Your Business Is on the Move Is It Protected

- What Is Commercial Auto Insurance and Who Needs It

- Decoding Your Commercial Auto Coverage Options

- Essential Endorsements and Overlooked Risks

- How Your Commercial Auto Premiums Are Calculated

- Navigating Southeast State Requirements

- Get the Right Quotes and the Best Protection

Your Business Is on the Move Is It Protected

A small business owner leaves for the day thinking about payroll, a customer deadline, and whether the crew has the right materials. Insurance isn't on the mind. Then a routine errand turns into an accident report.

Take a simple example. A handyman in Florida drives his own pickup to grab parts for a client job. On the way back, he taps the rear bumper of another vehicle in traffic. Nobody expects a major dispute. He has personal auto insurance, after all. But the claim adjuster asks a basic question: “Were you using the vehicle for business at the time?”

That's where panic starts.

Why this catches owners off guard

Many owners assume the line between personal and business driving is obvious. It usually isn't. If the trip was connected to earning income, serving a client, transporting tools, or handling a business errand, the insurer may treat that use differently than a normal personal trip.

A lot of businesses in the Southeast operate this way every day:

- Contractors use pickups to move tools, supplies, and paperwork.

- Retail owners make local deliveries when staff is short.

- Property managers drive between buildings, vendors, and tenant meetings.

- Restaurant owners jump in their own cars to cover late orders or supply runs.

None of that feels unusual. That's exactly why the risk gets missed.

Practical rule: If a vehicle helps your business make money, protect people, move goods, or serve a customer, you should assume insurance needs a business-level review.

The real issue isn't the car. It's the liability.

Most owners focus on vehicle damage first. Can the bumper be fixed? Is the van totaled? Those are important questions, but liability is usually the bigger one. If another driver is injured, if property is damaged, or if your business gets pulled into a lawsuit, the stakes rise fast.

Commercial auto insurance exists for that reality. It's built for the way businesses use vehicles. It can protect company-owned cars, work trucks, vans, and, in some situations, the business when someone uses a personal car for work.

If you've ever thought, “We only have one truck,” or “My employees just run occasional errands,” you're exactly the kind of business that should understand this coverage before a claim forces the lesson.

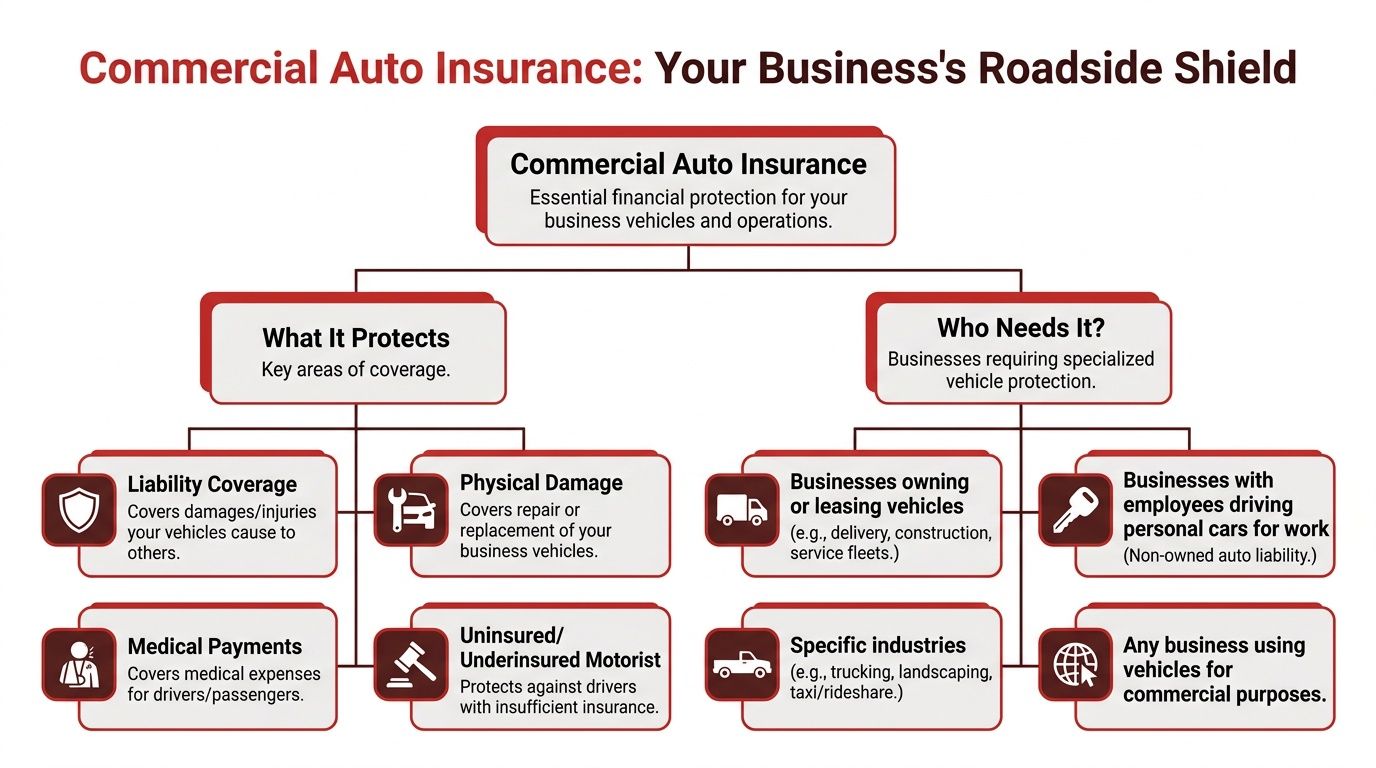

What Is Commercial Auto Insurance and Who Needs It

Commercial auto insurance is insurance for vehicles used in business operations. Think of it as your business's road-use policy. It helps protect the company when a car, truck, or van is involved in an accident, damage claim, or liability situation tied to work.

It isn't only for large fleets. In practice, many of the businesses that need it most are smaller operators with one vehicle, one owner-driver, or a few employees who drive as part of the job.

What counts as business use

The easiest way to think about it is purpose. If the trip supports the business, the exposure changes.

That can include:

- Delivering products to customers

- Transporting tools or equipment to a job site

- Driving clients or employees for work-related reasons

- Traveling between locations as part of daily operations

- Using a branded or business-owned vehicle for company activity

If you're also evaluating trailers, enclosed haulers, or specialized transport setups, National Car Transport's equipment guide can help you think through how the vehicle itself affects business use and insurance conversations.

Who usually needs it

The contractor

A contractor's truck often carries ladders, power tools, materials, and employees. That's not the same risk as a personal commute. The vehicle is part of the job, and a claim can involve equipment, passengers, or site-related schedules.

The delivery business

A florist, bakery, or meal-prep company may only run local routes, but frequent stops, tight schedules, and customer-facing deliveries raise exposure. One distracted turn in a parking lot can create both vehicle damage and liability issues.

The sales or service team

A business may not own a fleet at all. Maybe it has two account managers visiting customers or a field technician making service calls in a company car. If driving is part of the workday, commercial auto insurance belongs in the conversation.

The owner using a personal vehicle for work

Many small businesses stumble at this point. You might think, “It's my own car, so my personal policy should handle it.” Sometimes that assumption creates the very gap that causes trouble later.

A good test is simple. Ask, “If this trip didn't help the business, would I still be making it?” If the answer is no, the business use matters.

When owners should pause and review coverage

Use this quick checklist:

- Business ownership: Is the vehicle titled or leased in the business name?

- Employee driving: Do staff members drive for errands, visits, or deliveries?

- Tools or inventory: Do vehicles carry items your business depends on?

- Customer activity: Are you transporting goods, products, or people?

- Regular work travel: Do you cross county or state lines for jobs?

If any of those sound familiar, commercial auto insurance is worth reviewing now, not after a denial letter.

Decoding Your Commercial Auto Coverage Options

A commercial auto policy works like a suit of armor. Each piece protects against a different type of loss. If one piece is missing, the exposed area is usually the one that hurts the most after an accident.

You don't need to memorize every insurance term. You do need to know what problem each part solves.

Liability is the front line

Liability coverage helps when your business vehicle causes injury to someone else or damages someone else's property. This is usually the coverage that keeps a single crash from becoming a business-threatening event.

Think of it as the part of the armor facing outward. It protects your business from what your driver, vehicle, or operation may owe others after a crash.

Liability often includes:

- Bodily injury liability: For injuries to other people

- Property damage liability: For damage to another car, fence, building, or other property

Physical damage protects your vehicle

This part focuses inward, on the vehicle your business depends on.

It usually breaks into two common categories:

| Coverage | What it usually responds to |

|---|---|

| Collision | Damage from hitting another vehicle or object |

| Comprehensive | Damage from events like theft, fire, or weather-related loss |

If your business can't operate without that truck, van, or service vehicle, physical damage coverage matters because downtime costs money even when no one sues you.

Medical and uninsured motorist protections

Some policies also include protection for medical costs involving the driver or passengers. Uninsured or underinsured motorist coverage can matter when another driver causes the crash but doesn't carry enough insurance.

This area often confuses owners because they assume the other driver's policy will take care of everything. In real life, recovery can be uneven and slow. These coverages can help fill that gap.

Don't judge a policy by the declarations page alone. A low premium with thin coverage can cost much more once a vehicle is out of service or a claim turns legal.

Why commercial limits look higher than personal auto

One reason owners get sticker shock is that commercial auto insurance doesn't answer to just one rulebook. It's shaped by state law, federal regulation for some operations, and private contract requirements. For example, Texas has a minimum liability requirement of $30,000/$60,000/$25,000, while many private contracts require a $1,000,000 combined single limit before they'll issue a certificate of insurance for jobs or freight loading, as explained in this commercial auto requirements overview.

That last piece matters a lot for contractors, truckers, and service businesses. You may be legally allowed to carry one limit, but a customer, broker, or job contract may require something much higher before you can start work.

Read the policy like an owner, not just a buyer

When you review a quote, look past the premium and ask:

- Whose vehicles are covered

- Who counts as an insured driver

- Whether physical damage is included

- What liability limit applies

- Whether endorsements change the scope of protection

If policy wording feels dense, a plain-English guide to navigating auto insurance can help you ask smarter questions before you bind coverage.

Commercial auto insurance isn't just “more insurance.” It's a set of protections designed around how work vehicles create risk in actual situations.

Essential Endorsements and Overlooked Risks

A standard policy can leave dangerous holes. That's the part many owners don't hear until after a claim. They bought commercial auto insurance, assumed they were covered, and later learned the policy didn't extend where they thought it would.

One of the biggest blind spots is non-owned auto exposure.

The personal car problem businesses ignore

Here's the common assumption: “If my employee uses their own car, their own insurance handles it.”

That sounds reasonable, but it skips an essential question. What if the business is also pulled into the claim because the employee was running a work errand? That's where hired and non-owned auto coverage, often shortened to HNOA, becomes so important.

According to this discussion of rising commercial auto risks, 70% of small businesses allow employees to use personal cars for work, but only 35% carry specific hired and non-owned auto endorsements, and businesses without explicit coverage face a 40% higher rate of claim rejections in 2025 compared to fleets with explicit coverage.

That's not a technical detail. That's a real lawsuit problem.

What HNOA does

HNOA is designed to protect the business when vehicles it doesn't own are used for business purposes. Common examples include:

- An employee's personal sedan used to deposit checks, pick up supplies, or visit a client

- A rented vehicle used briefly for company operations

- A manager's own SUV used for business travel on a workday

For a deeper look at how this works in practice, this guide to hired and non-owned automobile coverage is a useful starting point.

If your answer to “Do employees ever use their own cars for work?” is anything other than a hard no, ask about HNOA in writing.

Other endorsements that can matter

Not every business needs the same add-ons. The right endorsement depends on what the vehicle carries, where it goes, and how your operation works.

Cargo-related protection

If your vehicle hauls products, materials, or customer goods, you may need cargo-related coverage. A basic auto policy may insure the vehicle itself but not what's inside it.

Trailer concerns

Some trucking and hauling operations rely on trailers they don't own full time. In those cases, trailer-related endorsements may be important. Without them, one damaged trailer can create a costly dispute over who pays.

Equipment and specialty use

Service bodies, attached equipment, refrigeration units, racks, or permanently installed tools can change the exposure. The more customized the vehicle, the less safe it is to assume a standard form handles everything properly.

A better way to review hidden risk

Instead of asking only, “Do we have commercial auto insurance?” ask these questions:

- Vehicle ownership: Do we ever use vehicles the business doesn't own?

- Driver mix: Do employees, temporary staff, or owners use personal cars for business?

- Cargo exposure: Are we carrying business property, tools, or customer goods?

- Contract exposure: Do job agreements require endorsements before we can work?

A policy can look complete and still miss one of those areas. Endorsements are how you turn basic coverage into practical protection.

How Your Commercial Auto Premiums Are Calculated

Commercial auto pricing feels mysterious until you see how underwriters look at risk. They aren't guessing. They're asking how often your vehicles are exposed, how severe a claim could be, and how predictable your operation looks on paper.

That's why two businesses with the same number of vehicles can pay very different premiums.

Why business auto usually costs more

Commercial auto insurance is commonly priced higher than personal auto because the exposure is different. In Texas, the average annual premium is $6,884 for commercial auto versus $3,910 for personal auto, and the gap is tied to factors such as higher annual mileage, multiple drivers, heavier vehicles, higher liability limits, operating radius, motor vehicle records, loss history, and endorsements such as HNOA, according to this commercial automobile insurance definition and pricing overview.

That same logic applies across many business types in the Southeast. A work vehicle is often on the road more, carries more weight, involves more drivers, and creates a bigger liability target.

What underwriters usually examine

Vehicle class

A small sedan used by one office employee is one thing. A loaded work truck or cargo van is another. Heavier and more specialized vehicles typically signal greater repair cost and claim severity.

Operating radius

A business that stays within a local service area presents one type of risk. A business that regularly crosses counties or states presents another. More road time and more jurisdictions often mean more complexity.

Driver records

Underwriters pay close attention to motor vehicle records, often called MVRs. A clean driving history helps. Multiple violations, recent accidents, or a mixed group of drivers can raise concern quickly.

Loss history

Past claims matter because they show patterns. If a business has repeated backing accidents, cargo-related losses, or frequent windshield claims, underwriters notice.

What you can control and what you can't

This is the part owners appreciate most. Some pricing factors are fixed. Others are manageable.

| Factor | Can you influence it? | How |

|---|---|---|

| Vehicle type | Sometimes | Choose practical vehicles for the job, not oversized ones by habit |

| Driver quality | Yes | Screen drivers, check records, set clear expectations |

| Operating habits | Yes | Limit unnecessary trips, define routes, track use |

| Claims history | Yes, over time | Build safer procedures and respond early to small issues |

| Contract-required limits | Usually not much | Review contracts before signing so insurance needs don't surprise you |

Practical ways to lower pressure on your premium

You can't make commercial risk disappear, but you can present a cleaner account.

- Tighten driver selection: Don't hand keys to anyone without reviewing driving history.

- Create a vehicle use policy: Spell out who can drive, what counts as business use, and how incidents must be reported.

- Separate personal and business use clearly: Blurry usage tends to create both underwriting and claims problems.

- Match endorsements to actual exposure: Extra coverage should solve a real risk, not just pad the policy.

- Review your fleet before renewal: Remove unused vehicles and outdated driver listings.

If you're looking for operational ideas that support safer driving habits, this article on how to reduce fleet insurance costs offers a practical checklist mindset.

Insurance pricing isn't only about what happened last year. It's also about whether your business looks organized, disciplined, and insurable going into the next term.

Navigating Southeast State Requirements

If your business stays in one state, insurance is already a compliance issue. If you cross state lines in the Southeast, it becomes a moving target. Contractors, delivery companies, trucking operations, and service businesses often discover that the route matters almost as much as the vehicle.

The challenge is that legal minimums and real-world requirements aren't always the same thing.

Quick reference for the Southeast

Below is a simple legal reference table using the state minimum structure discussed in the verified guidance. Where specific state numbers were not provided in the verified data, they're marked for direct confirmation with your agent or state filing requirements.

| State | Bodily Injury Liability per person | Bodily Injury Liability per accident | Property Damage Liability per accident |

|---|---|---|---|

| Alabama | Confirm by state filing | Confirm by state filing | Confirm by state filing |

| Florida | Confirm by state filing | Confirm by state filing | Confirm by state filing |

| Georgia | Confirm by state filing | Confirm by state filing | Confirm by state filing |

| North Carolina | Confirm by state filing | Confirm by state filing | Confirm by state filing |

| South Carolina | Confirm by state filing | Confirm by state filing | Confirm by state filing |

| Tennessee | Confirm by state filing | Confirm by state filing | Confirm by state filing |

| Virginia | Not legally mandated in all cases. Confirm route and filing requirements | Not legally mandated in all cases. Confirm route and filing requirements | Not legally mandated in all cases. Confirm route and filing requirements |

Why multi-state fleets get complicated fast

A lot of owners assume they can insure to their home state and be done. That can be a costly mistake.

According to this commercial auto FAQ discussion, Virginia and New Hampshire do not legally mandate commercial auto insurance in the same way many other states do, yet interstate fleets can still face uninsured motorist liability claims exceeding $1.2 million, and 60% of multi-state premiums are driven by the highest state minimum rule rather than accident frequency.

That means your policy often needs to reflect where you operate, not just where you're based.

What this means for Southeast businesses

For small businesses in the Southeast, multi-state exposure is common:

- A Georgia contractor may take projects in South Carolina.

- A North Carolina service company may dispatch crews into Virginia.

- A Florida business may send vehicles into neighboring states for deliveries or events.

In those situations, the question isn't just “What's my state minimum?” The better question is “What requirements follow my routes, contracts, and filings?”

For broader regional context, this overview of commercial insurance across the Southeast can help frame the compliance conversation.

A simple approach to staying compliant

Map your actual driving territory

List where your vehicles really go, not where you think they usually go. One recurring out-of-state job can change the insurance conversation.

Review contracts before jobs begin

A customer requirement can exceed the legal minimum. If your team starts work before the policy matches the contract, you can end up scrambling for a certificate or endorsement.

Recheck policy design as routes change

Businesses grow unevenly. A local fleet becomes a regional one without anyone updating the insurance structure. That's when gaps form.

Businesses that operate across Southeast state lines need a policy built around routes, vehicle types, and contract demands. A home-state assumption isn't enough.

Get the Right Quotes and the Best Protection

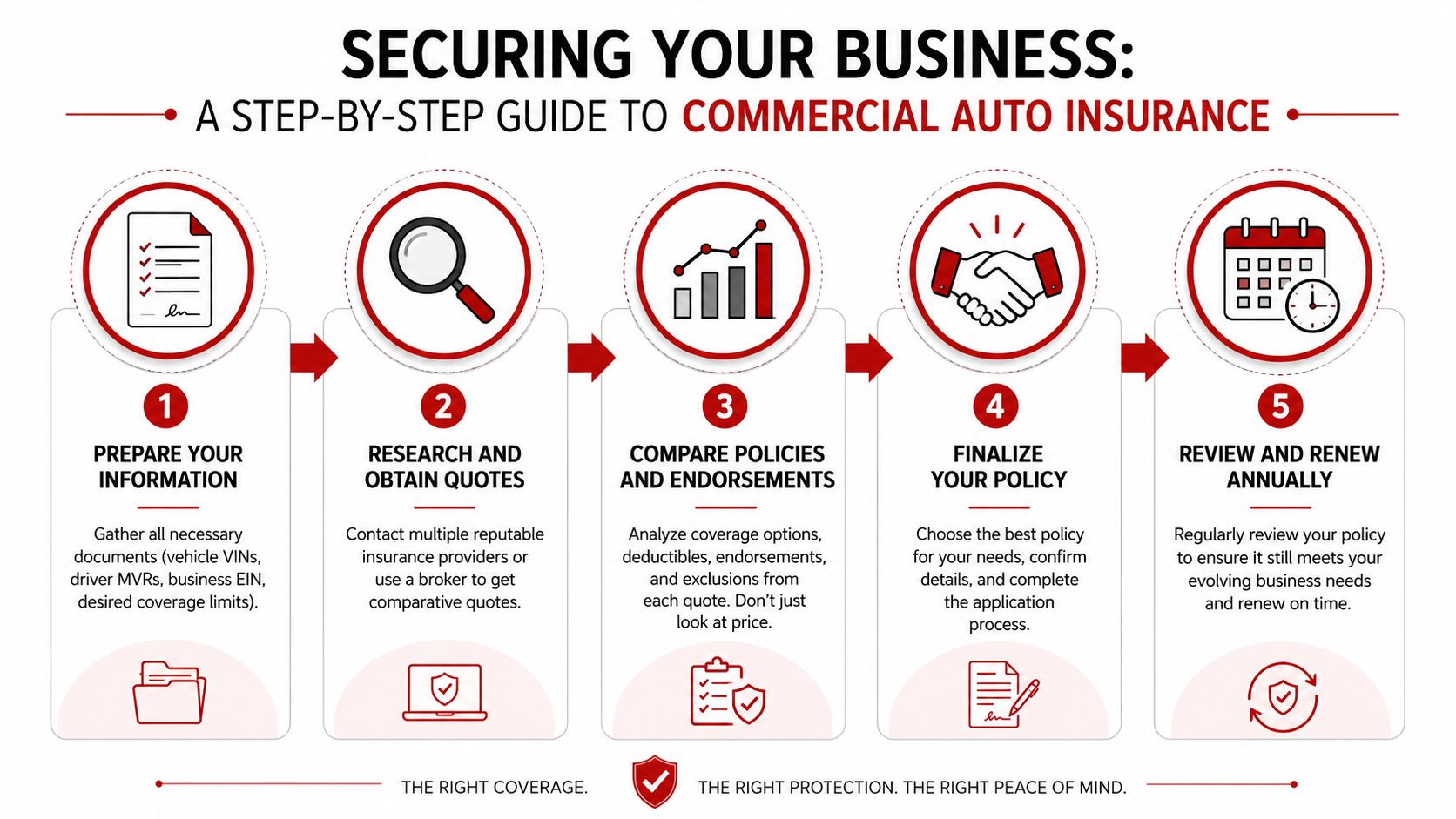

Shopping for commercial auto insurance gets easier when you treat it like a business process, not a last-minute purchase. Good quotes depend on clean information, clear questions, and an honest picture of how your vehicles are used.

If you rush the application, the quote may look fine but fail under scrutiny later.

Start with the documents that matter

Before you ask for quotes, gather the details carriers usually need:

- Vehicle information: VINs, year, make, model, and how each vehicle is used

- Driver information: Names, license details, and any known driving issues

- Business information: Entity name, address, operations, and where vehicles travel

- Coverage needs: Liability limits, physical damage needs, and any contract requirements

- Use details: Whether employees drive personal cars, whether tools or goods are transported, and whether routes cross state lines

The process is easier to visualize here:

Compare quotes the right way

Price matters, but it's not the first thing to compare. Start with scope.

Look at these items side by side:

| What to compare | Why it matters |

|---|---|

| Liability limits | Low limits can fail contract requirements or leave major exposure |

| Physical damage coverage | A cheaper quote may leave your vehicles unprotected |

| Driver listing rules | Some policies are stricter about who is covered |

| Endorsements | HNOA and other add-ons may be the difference between covered and denied |

| Exclusions | This is where unpleasant surprises usually live |

Ask every agent the same question set. That's the only way to compare policies fairly.

Questions worth asking before you bind

Does this quote match how my business really uses vehicles

A policy should reflect your actual operation, not a simplified version that makes the application easier.

Are there gaps involving personal vehicles or rented vehicles

If your staff ever uses personal cars for work, ask directly about non-owned auto exposure.

Will this satisfy my contracts or certificates

A low quote that can't produce the certificate your customer requires isn't a savings. It's a delay.

When an independent agency helps

Many business owners prefer working with an independent agency because it can compare options across multiple carriers instead of forcing one company's form onto every situation. If you want a plain-English explanation of that model, this overview of what an independent insurance agency is lays it out clearly.

In the Southeast, some agencies also understand the local patterns that generic quote systems miss, such as cross-border jobs, bilingual service needs, and the difference between a true fleet account and a small business with mixed vehicle use. Select Insurance Group, Inc. is one example of an independent agency that works with business customers in Alabama, Florida, Georgia, North Carolina, South Carolina, Tennessee, and Virginia.

The best protection usually comes from better questions

The strongest commercial auto insurance purchase isn't the cheapest quote. It's the quote that correctly matches your vehicles, drivers, routes, and contracts.

When you review options, slow down enough to confirm:

- Who is driving

- What is being transported

- Where the vehicles go

- Whether personal vehicles create business liability

- What proof of insurance your customers require

That's how you avoid buying a policy that only looks good until the first claim.

If your business uses cars, trucks, or vans for work, now's a good time to review whether your coverage matches the way you operate. Select Insurance Group, Inc. helps businesses in the Southeast compare commercial auto insurance options, review liability gaps like non-owned auto exposure, and sort through multi-state requirements before those issues become claim problems.