You're changing addresses, opening a second location, adding vehicles, or hiring across state lines. That's usually when people discover an uncomfortable truth. Insurance doesn't automatically “come with you” just because your life or business does.

A driver moving from one state to another may need a new policy setup, updated registration details, and different coverage requirements. A homeowner buying in a new region may face different property risks and policy forms. A business expanding into a neighboring state can end up juggling separate agents, different renewal calendars, and conflicting advice. That's how coverage gaps happen. Not because people are careless, but because the system is fragmented.

A good multi state insurance agency solves that fragmentation. It gives you one place to manage change, one team that understands how state lines affect insurance, and one process for keeping personal or business coverage aligned while your situation shifts.

Table of Contents

- Your Insurance Should Move With You

- What Is a Multi State Insurance Agency

- Navigating the Complex World of State Regulations

- Key Benefits for Every Type of Customer

- How to Choose the Right Multi State Agency

- Simplifying Your Insurance Future

Your Insurance Should Move With You

Most moves don't fail because the boxes weren't packed. They fail because the details were left for later. Insurance is one of those details.

A family relocates for work. The moving truck is booked, the utility transfer is in motion, and school enrollment is underway. If they're planning a stress-free Boston interstate relocation, they're already dealing with enough logistics. The last thing they need is to call one agent for auto, another for renters or homeowners, and then start over again after crossing a state line.

The same thing happens in business. An owner opens an office in a neighboring state and assumes the existing insurance arrangement will stretch to fit. Sometimes it does. Often it doesn't. The business may need updated liability structures, different vehicle handling, new workers' compensation coordination, or revised property schedules. If nobody is managing that transition centrally, small mistakes pile up fast.

A multi state insurance agency is often most valuable when life is changing quickly, because that's when disconnected policies create the most risk.

The broader market explains why this matters. As of 2026, the United States has over 226,000 insurance agencies, but the number of independent agencies is down 2.5% since 2022 to about 39,000, according to U.S. insurance agency statistics. In practical terms, that means strong agencies tend to be the ones that can support more operational complexity, especially in dense markets where clients need speed, options, and real coordination.

One relationship instead of repeated restarts

Working with a multi state insurance agency means you don't have to rebuild your insurance life from zero every time something changes.

That convenience matters when you're:

- Moving households and need auto, home, or renters coverage updated together

- Buying property in another state and want one point of contact

- Expanding a company and need coverage to keep pace with operations

- Managing multiple drivers or locations without multiple agencies creating confusion

The best version of this setup feels simple on your end, even when the work behind it isn't.

What Is a Multi State Insurance Agency

A multi state insurance agency is a centralized insurance resource that serves clients across more than one state. The easiest way to understand it is this. It works like a universal remote for your insurance.

Instead of calling one office for your car, another for your house, and a different agency when you move or expand operations, you work through one team that can coordinate coverage across state lines. That doesn't make insurance identical everywhere. It makes the process manageable.

One agency, many moving parts

A strong multi-state agency keeps your policies organized around your life or business, not around agency boundaries.

That usually means it can help you manage:

- Personal coverage together such as auto, home, renters, motorcycle, or RV

- Business protection in one place such as liability, property, workers' compensation, or commercial auto

- Policy changes during transitions when addresses, vehicles, payroll, operations, or locations change

- Renewal timing and service requests through a single relationship instead of scattered contacts

For clients, the biggest benefit is continuity. You don't lose context every time you need help.

Independent agency versus captive setup

Many people struggle with this point. Not every agency works the same way.

A captive setup generally represents one insurance company. If that company fits your situation, great. If it doesn't, your options narrow quickly. A multi-state independent agency has a different role. It shops among multiple carrier relationships and helps match coverage to the state, the property, the vehicle, or the business exposure in front of it.

If you want a deeper explanation of how that model works, this overview of what an independent insurance agency is is a useful starting point.

Independence matters more when your needs aren't standard. Moving, expanding, adding drivers, or insuring multiple locations rarely fits a one-size-fits-all process.

What clients should expect

A true multi state insurance agency shouldn't just say, “Yes, we write in your state.” It should be able to coordinate service, explain what changes when state rules differ, and keep coverage aligned as your situation evolves.

That's the practical difference. You're not buying geography. You're buying organized insurance management across geography.

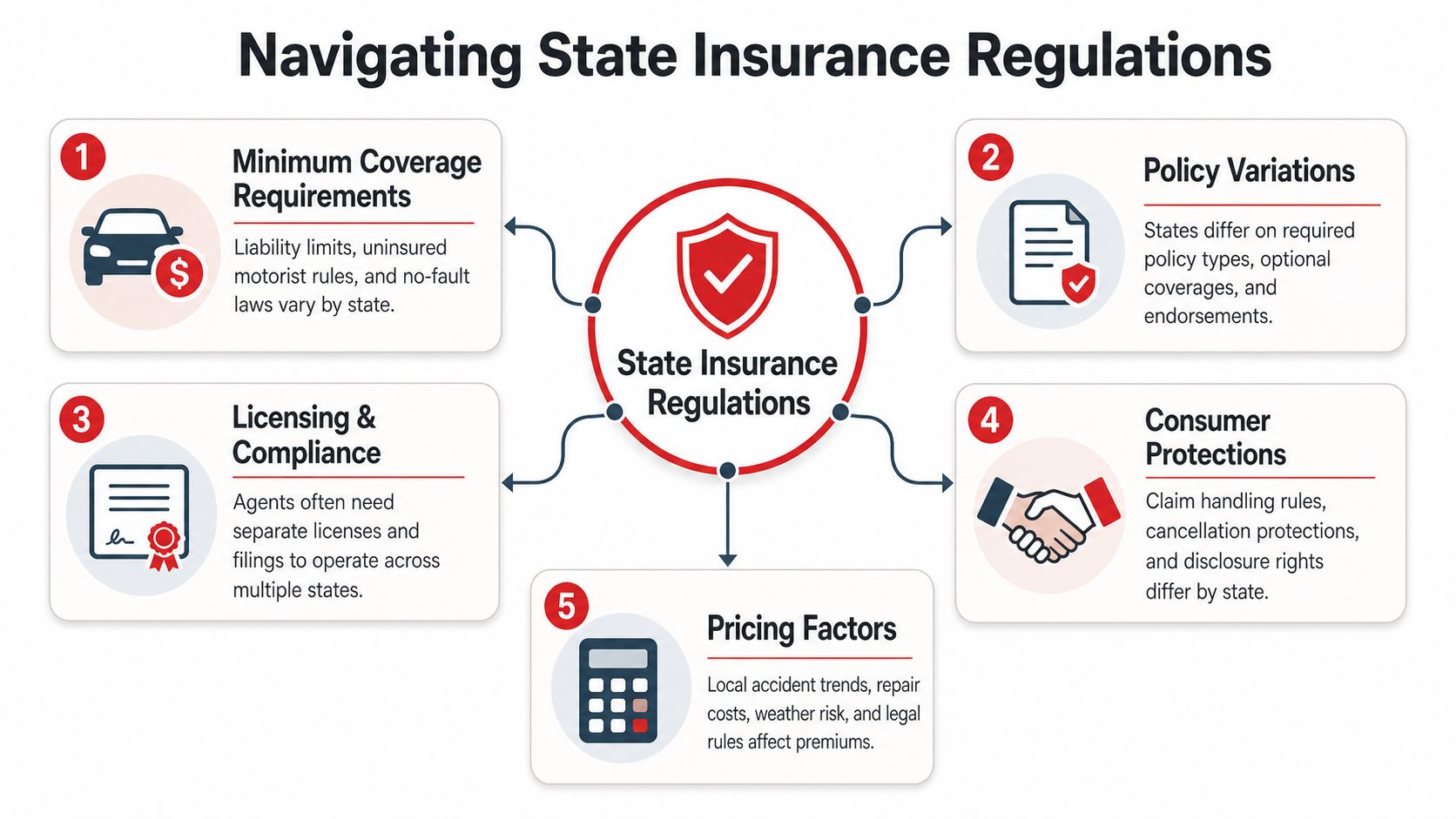

Navigating the Complex World of State Regulations

Insurance is regulated state by state. That sounds technical until it affects your coverage, your paperwork, or your claim.

A driver may move and discover different vehicle requirements. A homeowner may face a different underwriting approach because the new property sits in a region with very different loss patterns. A business may expand into another state and find that the agency relationship that worked well at home now leaves service gaps, delays, or inconsistent advice.

A capable multi state insurance agency earns its keep here. It handles the regulatory differences behind the scenes so the client doesn't have to become an expert in state insurance administration.

Every state changes the workflow

The public usually sees insurance as a policy and a payment. Agencies see the moving parts behind it.

Those moving parts include:

- Licensing rules that determine which agents can work in which states

- Policy forms and endorsements that can vary by jurisdiction

- Marketing and communication rules that affect what can be used where

- Service routing so a client reaches someone authorized to help in that state

One of the clearest realities in multi-state operations is that agencies must treat each state like its own line of business. According to guidance on ACA state exchanges and multi-state agency compliance, agencies must maintain state-specific marketing materials and make sure agents are properly registered for that state. A common failure happens when a call is routed to an agent who isn't authorized in the caller's state.

That might sound like an agency problem, but it becomes a client problem fast if advice is delayed, paperwork stalls, or the wrong person handles a state-specific issue.

Why this matters for businesses in particular

Businesses feel state complexity more sharply because they carry more policy layers. One expansion can trigger changes across general liability, property, workers' compensation, commercial auto, and contractor or fleet needs.

If your company operates across the Southeast, for example, a regional view matters. Insurance needs in one state won't always line up cleanly with the next. Agencies that regularly manage commercial insurance across the Southeast are built for that kind of coordination.

Practical rule: If an agency can't explain how it handles state-specific compliance internally, it probably won't make interstate insurance feel simple for you externally.

What actually works

The agencies that handle multi-state business well usually do three things consistently.

- They build state-by-state processes. They don't assume one script, one form set, or one service path works everywhere.

- They centralize communication. Clients shouldn't have to guess who handles which state issue.

- They review changes before problems surface. Moves, new locations, vehicle additions, and staffing changes should trigger policy review, not wait for renewal.

That's what turns a complicated regulatory map into a manageable client experience.

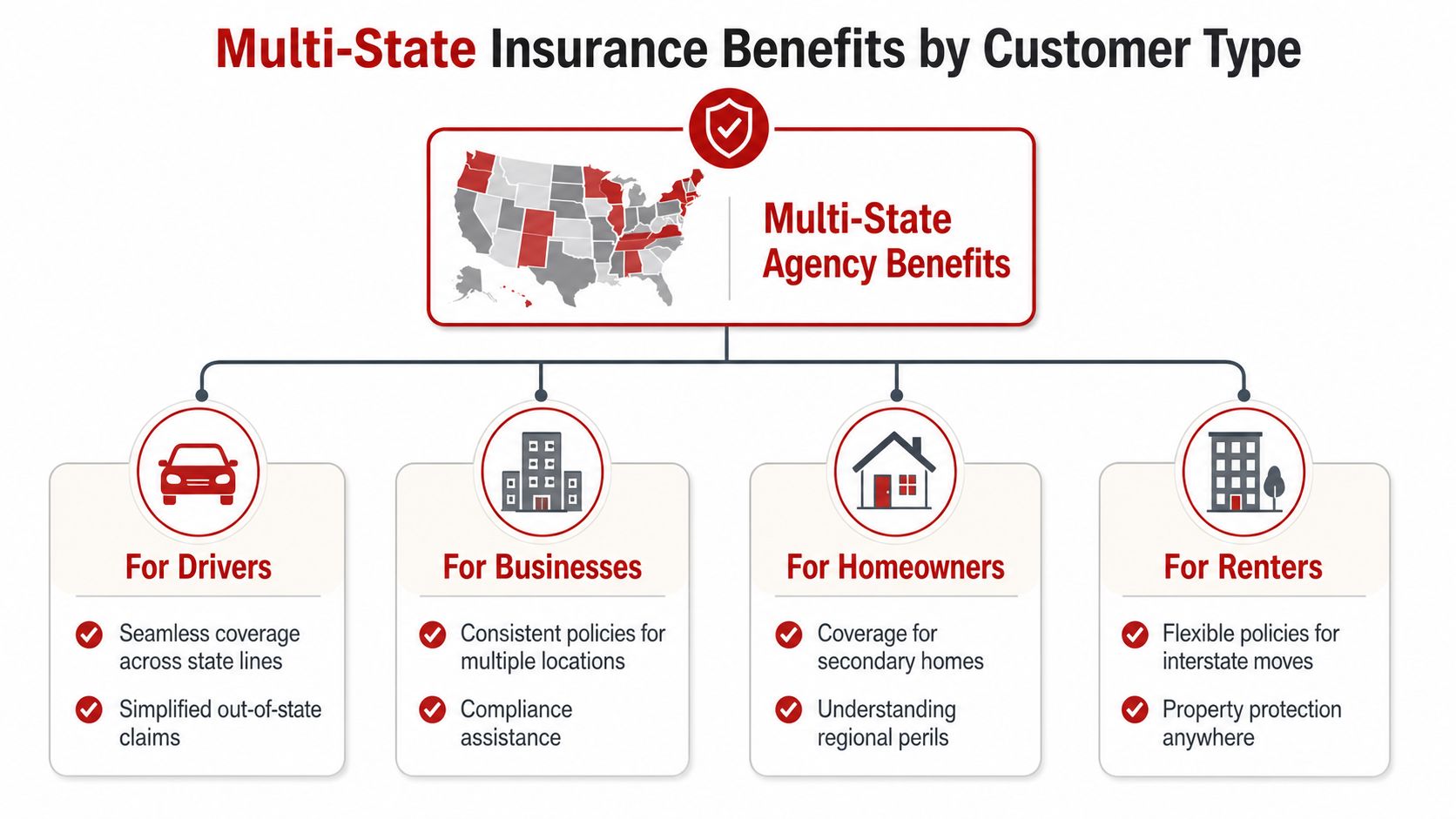

Key Benefits for Every Type of Customer

The appeal of a multi state insurance agency isn't abstract. It shows up in ordinary situations where people need coverage to stay intact while their circumstances change.

For Drivers

Drivers usually feel the benefit first because auto changes happen fast. A move, a new garaging address, a teen driver, a title transfer, or an added vehicle can all require action.

A single-state agency often works fine until your address or daily driving pattern crosses a border. Then the process gets clunky. A multi-state agency helps coordinate the update without forcing you to go shopping from scratch with no continuity.

That matters for families too. If parents, children, or shared vehicles are tied to different addresses during a transition, keeping everything organized under one agency relationship reduces confusion.

For Homeowners

Homeowners don't just move houses. They move into different risk environments.

The insurance approach that made sense for one property may not fit another. Construction type, lender requirements, regional weather exposure, occupancy patterns, and secondary-home questions can all change the conversation. When one agency can help you transition from one state to another without breaking the service relationship, the move feels far more controlled.

Good insurance service during a move isn't just about replacing a policy. It's about carrying forward the details that shouldn't be lost in the shuffle.

For Small Businesses

Small business owners benefit the most when operations stop fitting neatly in one zip code. A second storefront, a neighboring-state client base, equipment storage in another jurisdiction, or employees working across state lines all complicate insurance.

A multi-state agency helps keep that complexity from turning into fragmented coverage.

Common advantages include:

- Consolidated oversight so liability, property, and auto decisions don't happen in separate silos

- Cleaner renewals when one team is tracking changes across locations

- Better issue spotting because service staff can see how one policy change affects another

- Less wasted time when owners don't have to retell the same business story to multiple agencies

For Fleets and Commercial Vehicles

Commercial vehicles create practical headaches fast. Where a vehicle is based, where it operates, who drives it, and how it's titled all matter.

A multi-state agency is useful here because fleet management is already detail-heavy. If your insurance is split among separate offices, every update takes longer than it should. Centralized handling gives owners and office managers one place to report vehicle additions, driver changes, certificates, and claim questions.

For Spanish Speaking Customers

Insurance gets harder when the explanation is unclear. That problem gets worse during a move or business expansion.

Clients who prefer bilingual service often want more than translation. They want continuity. They want the same agency relationship to stay intact while addresses, policies, and paperwork shift. A multi-state setup with reliable bilingual support makes that possible and reduces the chance that important details get missed because communication changed along the way.

How to Choose the Right Multi State Agency

Not every agency that says it serves multiple states is built the same way. Some can write business broadly but service it unevenly. Others have licenses in place yet can't deliver useful options where you need them.

The right question isn't only whether the agency can take your call. But the question is whether it can carry your insurance smoothly through change.

What good agencies handle well

Start with the basics. The agency should be able to explain which states it serves, how service works when you move or expand, and how it keeps policy changes from slipping through the cracks.

Then ask the question most buyers overlook. An expert recommendation from a licensing and compliance playbook for growing across state lines is to ask not only whether the agency is licensed in your state, but which of its 20 to 40 carriers are appointed and can write your policy there. That carrier-availability check matters because licensing alone doesn't guarantee useful market access.

The best agencies answer operational questions clearly. The weak ones answer in generalities.

If you're evaluating agencies in a state with a busy market, it helps to review a local example of a Florida insurance agency and notice whether the service model looks built for ongoing support or only for initial sales.

Checklist for Choosing a Multi State Agency

| Evaluation Criteria | What to Look For |

|---|---|

| State licensing footprint | Clear confirmation that the agency and relevant agents are authorized where you live or operate |

| Carrier access | A direct answer about which carriers can actively write your policy in the states you need |

| Personal and commercial capability | Ability to manage more than one policy type if your needs overlap |

| Transition handling | A defined process for moves, new locations, added vehicles, or business changes |

| Service model | One consistent contact path for billing questions, policy updates, and claims support |

| Digital convenience | Secure tools for documents, signatures, payments, and routine service requests |

| Bilingual support | Reliable communication if your household or staff prefers service in Spanish |

| Regional familiarity | Practical knowledge of the states where you actually need coverage |

Red flags worth noticing

Some warning signs show up early:

- Vague answers about who can service which state

- No discussion of carrier appointments beyond basic licensing

- Fragmented communication where personal lines, commercial lines, and service all feel disconnected

- Reactive advice that only appears after a problem surfaces

The right agency should make interstate insurance feel simpler, not more mysterious.

Simplifying Your Insurance Future

A multi state insurance agency does one job exceptionally well. It reduces friction when your life or business doesn't stay inside one state boundary.

That convenience matters more than people realize. One point of contact, organized policy management, better continuity during moves, and clearer handling of state-specific issues all reduce the odds that something important gets missed. For households, that can mean fewer gaps during a relocation. For businesses, it can mean steadier protection while operations expand.

The best agencies also save you from false confidence. They know that “licensed in your state” isn't the same as “ready to serve you well there.” They coordinate the details that most clients never see, and that's exactly the value.

If you're moving, buying property in another state, growing a company, or just tired of juggling separate insurance relationships, this model is worth serious attention. Insurance should keep up with where you're going.

If you want help from an independent agency that serves customers across Alabama, Florida, Georgia, North Carolina, South Carolina, Tennessee, and Virginia, Select Insurance Group, Inc. offers personal and commercial coverage with quotes from 20 to 40 carriers, bilingual support, and a service model built for people and businesses in transition.