If you're splitting time between Florida and the Carolinas, insurance gets messy fast. One car may be garaged in one state, a rental may sit in another, and a small business may cross state lines every week. What looks simple on paper turns into separate agents, different renewal dates, conflicting advice, and coverage gaps that nobody catches until there's a claim.

That's why choosing a multi-state insurance agency for FL, SC, and NC should be a strategy decision, not just a convenience decision. The right agency doesn't just collect policies under one roof. It coordinates how those policies work together across different state rules, different carriers, and very different market conditions.

Why You Need One Agency for Florida and the Carolinas

A common scenario goes like this. Someone lives in North Carolina, owns a condo in Florida, and has a college-age driver spending part of the year in South Carolina. Another business owner keeps personal coverage in one state, registers vehicles in another, and sends employees across all three. They often end up with different agents handling different pieces.

That setup creates blind spots. One agent may know your Florida property well but miss how your North Carolina auto use affects underwriting. Another may quote a South Carolina policy correctly but never ask how your household is structured across state lines. When each policy sits in its own silo, nobody is responsible for the full picture.

A single multi-state agency fixes that by centralizing the questions that matter. Where is the vehicle really garaged? Which address is primary for underwriting? Which state's rules apply to the driver, property, or business operation? Those answers affect policy design more than most buyers realize.

What a coordinated agency actually changes

The practical benefit isn't just fewer phone calls. It's better coverage alignment and cleaner account management.

- One account review: A good agency reviews your auto, property, umbrella, and business risks together instead of treating each policy like a separate transaction.

- One renewal strategy: When policies renew through different offices with different timelines, discounts and coverage reviews often get missed.

- One service team: Claims documents, lender requests, ID cards, endorsements, and billing questions move faster when one agency can see the entire relationship.

If your household or business generates a steady flow of certificates, policy changes, and follow-up tasks, operational support matters too. Larger agencies often rely on strategic insurance BPO solutions to keep service moving when back-office demand spikes, especially for document handling and routine policy servicing.

For readers who want the short version of the agency model itself, this explanation of what an independent insurance agency does is a useful starting point.

Practical rule: If your life or business crosses state lines, don't shop each policy in isolation. Shop for an agency that can manage the relationship as one account.

Confirming Your Agency Is Licensed to Practice

Before you compare premiums, confirm that the agency and the producer are properly licensed for the states where they're advising and placing business. This is not a formality. If the licensing side is sloppy, everything else should concern you too.

For multi-state work, the dependable workflow is simple. The producer first secures a resident license in the home state, then files for non-resident authority in each target state through the state DOI or NIPR, as outlined in this guidance on getting licensed in multiple states. The mistake agencies make is assuming reciprocity works the same everywhere. It doesn't.

What to verify before you buy

Ask for the full legal name of the agency and the individual producer's name. Then verify both.

Use this checklist:

Check the individual first

Make sure the person giving advice holds authority in the state where your policy is being discussed or sold.Check the agency entity

Some buyers verify only the agent. The agency itself may also need proper registration or licensing status depending on the state setup.Confirm line of authority

Personal auto, homeowners, commercial auto, general liability, and trucking don't always sit under the same practical workflow. Make sure the person handles the line you're buying.Ask about renewal tracking

A serious multi-state agency keeps a state-by-state license matrix and appointment process. If the answer sounds vague, keep looking.

Questions worth asking directly

A legitimate agency won't be offended by direct compliance questions. Ask these plainly:

- Are you licensed as a non-resident producer in Florida, North Carolina, and South Carolina?

- Who on my account is licensed in each state I need help with?

- If my risk changes mid-term, who checks whether another state's rules now apply?

- Do you track appointments and renewals internally, or is that handled ad hoc?

A clean license record doesn't prove the agency is skilled. But an unclear answer on licensing is enough reason to walk away.

An agency that can't explain its authority to practice across state lines usually won't be strong on policy detail either. Start with legality, then move to coverage design.

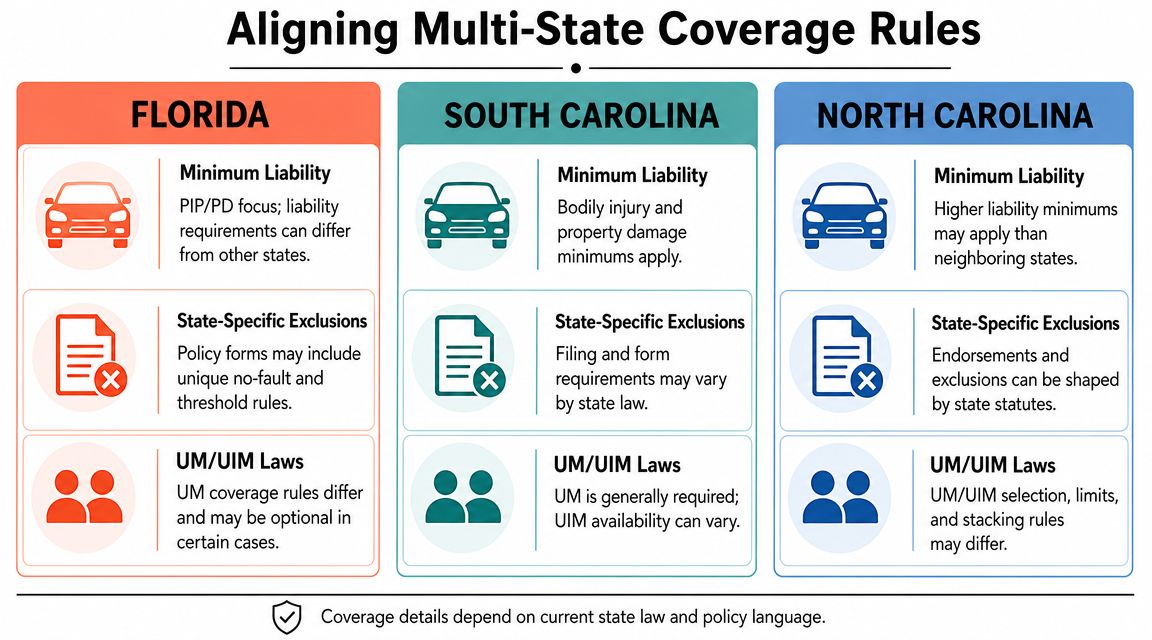

Aligning Coverage Across Different State Rules

The biggest mistake buyers make is assuming a multi-state setup means they can copy one policy approach across all three states. That rarely works.

Florida's personal auto market is structurally different from North Carolina and South Carolina. Florida is a no-fault/PIP state, while North Carolina and South Carolina are at-fault states. Premiums reflect those differences too. Bankrate's 2024 analysis using Quadrant data put average annual full-coverage auto premiums at about $3,941 in Florida, $1,771 in North Carolina, and $1,589 in South Carolina in this discussion of state-by-state auto pricing and rule differences.

Why one-size-fits-all advice fails

An agent who treats these states as interchangeable usually gives generic advice like "just match your current limits." That sounds easy, but it skips key underwriting and claims issues.

Here's where mismatches happen:

| Area | Florida | North Carolina and South Carolina | What the buyer should watch |

|---|---|---|---|

| Auto claim framework | No-fault/PIP structure | At-fault structure | Medical payment handling and liability planning differ |

| Policy design | Often needs different conversations around injury protection and deductibles | Often centers more directly on liability structure and driver profile | Limits should be reviewed by state, not copied |

| Pricing pressure | Higher volatility and cost pressure | Usually a different quote environment | Carrier access and comparison matter more in harder markets |

Where coordinated review helps most

The right agency looks for overlap points, not just separate quotes.

- Households with multiple addresses: If a driver rotates between states, the garaging and usage details must be accurate.

- Rental and seasonal property owners: The property policy and the auto policy should reflect how often you're physically present in-state.

- Contractors and service businesses: Vehicles, tools, and liability exposures often change depending on where work is performed.

A lot of buyers also miss how weather-related exposure changes the property side of the account. If you're balancing renters or property decisions in coastal areas, this overview of whether renters insurance covers hurricane damage is a useful example of why state and peril details matter.

The best multi-state account isn't the one with matching policy language everywhere. It's the one where each policy fits the state and still works together as a package.

That takes more work on the agency side. It also prevents the expensive problem of finding out after a loss that each policy was technically valid, but poorly coordinated.

Evaluating Carrier Access and Local Expertise

An independent agency is only as useful as the carriers it can reach. That matters in every state, but it matters most in Florida because the market is larger, more concentrated, and more difficult to manage than many buyers expect.

The Insurance Information Institute lists 218.6 insurers or market presence units for Florida, 83.2 for North Carolina, and 28.2 for South Carolina in its state insurance market data. That difference tells you something important. A multi-state agency in these three states isn't managing one regional market. It's managing three markets with different depth, competition, and placement challenges.

What to look for under the hood

Carrier count alone isn't enough. Ask which types of carriers the agency uses for your kind of risk.

A strong agency should be able to explain:

- Which carriers write standard risks in each state

- Which markets handle tougher property or driving profiles

- How they pivot when a carrier tightens underwriting

- Whether they have regional options, not just one or two national names

Florida especially tests this. Catastrophe exposure changes availability and underwriting appetite. Agencies that only have a thin carrier bench often run out of options quickly. Agencies with broader access can reroute the account instead of telling you to accept a bad fit.

Local expertise still matters

A big call center can quote fast. That doesn't mean it understands your street, your county, or how local habits affect placement.

Local expertise shows up in the questions an agent asks:

- Is the home owner-occupied, seasonal, or tenant-occupied?

- Is the vehicle used mostly for commuting, service calls, or mixed business use?

- Does the business cross state lines regularly, or only occasionally?

- Is the property in a location where storm exposure changes carrier appetite?

One practical option in this market is Select Insurance Group, Inc., which operates as an independent agency across Florida and the Carolinas and compares multiple carriers for personal and commercial lines. That model matters more than branding. What you want is an agency that can match local knowledge with real market access.

Assessing Service Quality Digital Tools and Bilingual Support

The first quote is only the start of the relationship. The true test comes later, when you need a policy change, proof of insurance, a claim document, a mortgagee update, or help understanding why one option is cheaper but weaker.

Service quality shows up in small moments. Can you upload documents securely without chasing email threads? Can you request ID cards or certificates without waiting on hold? Can you text a question and get a useful answer instead of a generic response? Those details save time, but they also reduce mistakes.

Digital tools that solve actual problems

A good agency's digital setup should make routine tasks easier, not push you into self-service confusion.

Look for these basics:

- Document upload and e-sign support: Useful when you're binding quickly or sending lender and registration paperwork

- Payment and billing access: Especially helpful when policies are spread across more than one carrier

- Claims assistance: Not just a carrier phone number, but someone who can tell you what to send and when

- Policy change workflows: Address changes, vehicle swaps, driver updates, and certificate requests should be straightforward

If an agency still handles everything through voicemail and scattered email chains, expect delays when timing matters.

Why bilingual support matters beyond translation

The U.S. Hispanic population reached 68 million in 2023, and a J.D. Power study found 49% of insurance customers were unaware of at least one available discount, as noted in this discussion of bilingual insurance access and discount awareness. That matters in Florida, South Carolina, and North Carolina because many households don't just need a translated quote. They need someone who can explain coverage choices clearly.

What works in practice: Bilingual service is most valuable when the agent can explain deductibles, exclusions, endorsements, and discount opportunities in plain language, not just switch languages.

That distinction matters for families and business owners alike. A bilingual agent should be able to explain why one deductible creates more out-of-pocket risk, why a landlord policy differs from a homeowners policy, or why a commercial auto schedule needs cleanup before renewal.

An agency that combines useful digital tools with bilingual guidance usually performs better over the life of the account. The quote may look similar at the start. The difference shows up when something changes.

Hiring Tips for Commercial Fleet and Trucking Insurance

Commercial clients need a stricter hiring standard for agents than personal lines buyers do. If your company has service vans, dump trucks, box trucks, or an interstate trucking operation, the question isn't whether the agency can quote. The question is whether it can keep the account compliant as the business grows.

Florida alone had 40,030 insurance sales agents in May 2023, according to the Bureau of Labor Statistics reference cited in KFF context on insurance market competition and employment scale. For a business owner, that means choice isn't the problem. Screening is.

Questions to ask before you appoint an agent

Don't ask, "Do you write trucking?" Ask sharper questions.

How do you handle vehicles that operate in more than one state?

You want an answer that mentions garaging, radius, operations, and filings, not just "we can insure that."What information do you need before quoting my fleet?

A serious commercial agent asks for driver lists, VINs, loss runs, business description, travel territory, and contract requirements.How do you deal with policy changes mid-term?

Fleets change constantly. Drivers come and go. Units are added, sold, or down for repair. Slow service creates uninsured days and certificate issues.What filings or endorsements should I expect for my operation?

Interstate work often requires more than a standard commercial auto conversation. The agent should be comfortable discussing filings and contract-driven insurance requirements.

What separates a vendor from an advisor

A weak agent shops the premium and disappears. A strong one notices account problems before the carrier does.

If the agent doesn't ask where your trucks actually travel, what contracts require, and how drivers are hired, the quote is incomplete.

This matters for flatbed, contractor, and owner-operator risks in particular. Cargo type, tie-down exposure, route patterns, and subcontractor relationships all affect placement. Business owners comparing agencies may also find operational context in this 2026 guide to flatbed operations, especially if they're evaluating how equipment use and freight type affect insurance conversations.

One more practical check. Ask the agent to explain the difference between broad protection and bare compliance in plain English. If you also want a quick refresher on policy structure before that conversation, this breakdown of full coverage vs liability is useful.

For commercial accounts, hire the agent the way you'd hire a controller or safety manager. You're not buying a quote sheet. You're hiring judgment.

If you need help comparing personal or commercial coverage across state lines, Select Insurance Group, Inc. can review your current setup, identify where Florida, North Carolina, and South Carolina rules may conflict, and help you quote coverage through multiple carriers with bilingual support when needed.