You apply for renters insurance because your landlord requires it. The quote tool looks promising for a few minutes, then the screen changes. Referred. Ineligible. Call for review. Maybe you had an eviction a few years ago. Maybe your credit is bruised. Maybe you live in a building that has seen water losses before. Suddenly a basic policy feels hard to get.

That's the moment a lot of renters decide they're stuck. They aren't.

Renters insurance for high-risk tenants is harder to place, but it's usually a placement problem, not a dead end. The key is knowing how insurers look at your file, what information matters, and which paths still work when standard online quotes keep rejecting you.

Finding Renters Insurance When You've Been Labeled High-Risk

One of the most common calls in this situation starts the same way. A tenant has a lease in hand, move-in is close, and the landlord wants proof of insurance. The tenant has already tried a few websites and maybe one big-name carrier. Each try ended with a decline, an incomplete quote, or a premium that didn't make sense.

That doesn't mean the tenant is irresponsible. It usually means the application hit one or more underwriting triggers. Carriers use those triggers to sort applicants quickly, and online systems are blunt. They're built for clean files. If your situation is messier, you often need a different carrier and a more hands-on submission.

There's a real cost to going without coverage. According to MoneyGeek data summarized here, approximately 45% of U.S. renters lack renters insurance coverage, and a single covered claim can repay 10 to 50+ years of premiums. That matters even more when you're already financially stretched and can't easily absorb a theft loss, a kitchen fire, or a liability claim from a guest injury.

Practical rule: “High-risk” is an underwriting label, not a final verdict on whether you can get insured.

What high-risk usually means in real life

For renters, the label often shows up when an insurer sees a pattern it doesn't like. That can include prior claims, poor credit, missed payments, an eviction record, a dog breed some carriers avoid, smoking in the unit, or a property in an area with theft, water, storm, or flood concerns.

Sometimes the tenant isn't the main issue at all. The building is. Older plumbing, prior water losses, roof age, or neighborhood crime patterns can tighten options before your name even comes into play.

The right mindset

If you're worried, focus on one question. What exactly caused the decline?

Once you know that, the process gets more practical. You stop guessing, stop filling out quote forms that were never going to work, and start building a file a real agent can place.

Decoding Your High-Risk Tenant Profile

Insurers rarely reject renters insurance applications for vague reasons. They usually reject them because something in the file suggests a higher chance of claims, payment problems, or incomplete information. If you want better results, learn how they're reading your application.

According to Experian's overview of why renters insurance rates are rising, insurers use a step-by-step underwriting process for high-risk tenants that can include automated screening through CLUE reports, credit scores below 600, eviction history, high-crime ZIP codes, and manual review with surcharges of 20% to 50% for certain risks. That process helps explain why one tenant gets an instant quote and another gets stopped for review.

Claims history

A CLUE report shows prior insurance claims tied to you and, in some cases, the property. If the report shows repeated losses, underwriters assume future claims are more likely.

The red flag isn't always one claim. It's often the pattern. Multiple water, theft, or liability losses make a standard carrier nervous because renters claims can repeat in similar living situations.

If you're not sure what's on your insurance history, ask before you apply again. Don't wait for a denial to tell you what was already in the file.

Credit and payment behavior

Many tenants are surprised by how much credit matters. Insurers don't use it because they're judging character. They use it because they're pricing the chance of nonpayment, policy lapse, and claim behavior.

A score below 600 can move you out of preferred pricing or out of eligibility altogether, based on the carrier. Late payments and collection activity can also push an application into manual review, especially if the carrier already sees other concerns.

For a simple explanation of how negative items can affect insurance longer than people expect, the way traffic violations can linger is a useful parallel in this article on how long traffic tickets affect insurance.

Evictions and rental history

Evictions matter because carriers and landlords both read them as evidence of housing instability. Even if the eviction happened during a rough stretch you've already moved past, the application may still get tagged for review.

A clean recent rental history can help. So can proof that the old issue was resolved. Underwriters respond better to a clear story with documentation than to a blank spot they have to interpret on their own.

The fastest way to look riskier is to make an underwriter guess.

Property and location risks

Your ZIP code can affect eligibility even if your personal history is fine. A unit in a high-theft area, a flood-prone zone, or a building with old systems may get fewer carrier options from the start.

This is common in parts of the Southeast. Coastal exposure, frequent water losses, and older multifamily buildings all create friction in the quote process. In those cases, the carrier may still write the policy, but with tighter terms, a higher deductible, or added underwriting questions.

Occupancy details that trigger surcharges

Some details don't kill the application, but they can change the premium or carrier choice quickly:

- Pets with liability concerns can push you out of one market and into another.

- Smoking in the unit raises fire concerns and may trigger a surcharge.

- Subletting or roommates not listed clearly can complicate occupancy review.

- Home business activity can create exposures a standard renters form wasn't meant to handle.

When people get denied repeatedly, it's often because they keep submitting the same problem in slightly different places. Better results start when you identify the exact issue and address it head-on.

Strengthening Your Application to Improve Your Odds

Most renters try to shop first and prepare second. For high-risk applications, that order usually backfires.

The better approach is to build a submission package before anyone runs your information. That doesn't guarantee approval, but it makes your application easier to place and reduces the chance that a carrier assumes the worst.

Build your file before you request quotes

Start with the documents an underwriter is most likely to ask for. Keep them in one folder so you can send them quickly.

- Photo ID and current address details. Make sure the address, unit number, and move-in date are consistent everywhere.

- Proof of income or recent bank statements if your file may get manual review.

- A short written explanation for prior claims, lapses, evictions, or collections. Keep it factual and brief.

- Lease documents that show occupancy, required liability limits, and pet information if applicable.

- Receipts or a home inventory list for higher-value belongings, especially electronics, jewelry, tools, or collectibles.

If a debt was paid off or a landlord dispute was resolved, include evidence. Underwriters don't reward long emotional explanations. They respond to clean documentation.

Fix the easy underwriting problems first

Some risk factors are hard to change quickly. Others are not. Start with the changes that can improve the file right away.

A water leak detector, monitored alarm, deadbolt confirmation, or proof of smoke detectors can all help support the story that you take loss prevention seriously. If a carrier asks whether the unit has protective devices, you want the answer to be complete and accurate.

A higher deductible can also help open doors. It won't solve every issue, but it tells the carrier you're not looking to file small nuisance claims.

What works: documented improvements, clear occupancy details, and realistic coverage choices.

What doesn't: hiding a pet, guessing at property values, or leaving prior losses unexplained.

Risk factors and mitigation strategies

| Risk Factor | What Insurers See | Your Action Plan |

|---|---|---|

| Prior claims | Possible repeat losses | Gather claim dates, causes, and resolution details. Show what changed since the loss. |

| Poor credit | Payment and underwriting concern | Pay down active issues where possible, avoid new missed payments, and prepare for manual review. |

| Eviction history | Housing instability | Provide proof of current stable tenancy, income, and any documentation showing the old matter was resolved. |

| Pet ownership | Liability exposure | Disclose the pet early, confirm breed and bite history accurately, and ask upfront which carriers are pet-friendly. |

| Smoking | Fire risk | Be honest. If smoking has stopped, say so clearly and provide accurate occupancy details. |

| Subletting or roommates | Unclear occupancy | Make sure the lease and application match. List who lives there and who is responsible under the lease. |

| Older or loss-prone building | Property hazard concern | Ask the landlord about recent plumbing, electrical, roof, or safety upgrades and keep that information ready. |

| High-theft or storm-exposed area | Greater chance of claim activity | Ask about alarm systems, secured entry, and water shutoff devices. These details can matter in placement. |

Choose coverage that helps you, not just the lease

A lot of tenants focus only on getting the cheapest proof-of-insurance document for the landlord. That's understandable, but it can leave you underinsured.

Think about three buckets. Your belongings, your liability, and your temporary living expenses if the unit becomes unlivable after a covered loss. If you understate your belongings badly, you can end up with a policy that satisfies the lease but doesn't do much when you need it.

For liability, don't skimp just because your furniture isn't worth much. Liability claims are the part many renters underestimate.

Don't create a credibility problem

If a quote form asks about prior losses, pets, business use, or smoking, answer it cleanly. A bad answer can lead to a better-looking quote today and a bad claim dispute later.

One honest application to the right carrier beats five rushed applications that conflict with each other.

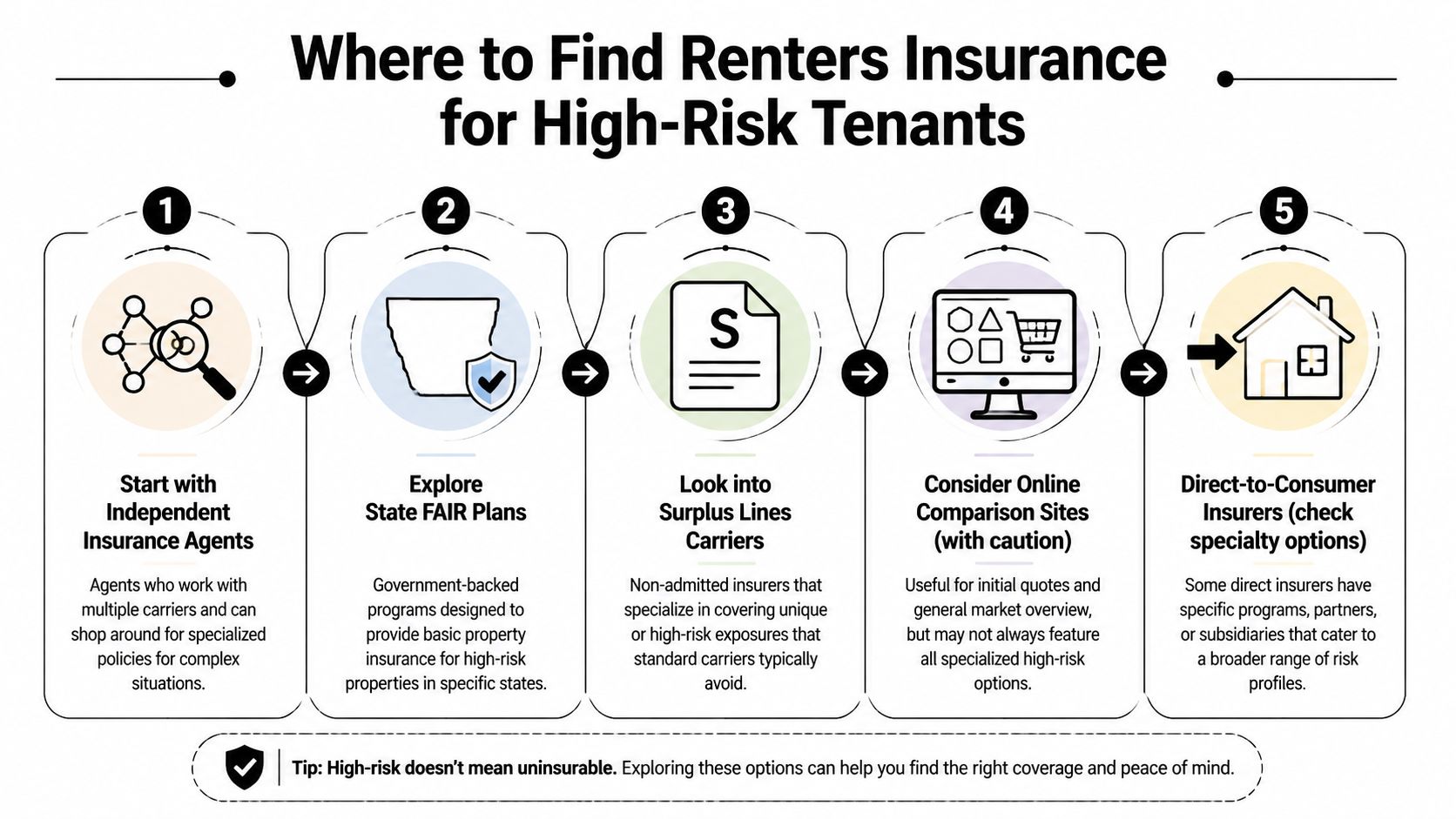

Where to Find Renters Insurance for High-Risk Tenants

Once your file is ready, the next question is where to take it. Not every channel is built for high-risk business, and many renters waste time because of this.

The three main paths are independent agents, direct access to non-standard or specialty markets, and landlord-provided plans when tenant-purchased coverage is hard to secure.

Independent agents

This is usually the most efficient route when you've already been declined. Independent agencies can approach multiple carriers, including markets that don't spend much money advertising to the general public.

That matters because standard online forms often reject risks that a non-standard carrier will still consider after a human review. A good independent agent also knows how to present the file. That's a major difference. A difficult application isn't just about where it goes. It's about how it's packaged.

If you're not familiar with how that shopping process works, this explanation of what an independent insurance agency does lays out why one agency can access more than one carrier relationship.

Specialty and surplus lines markets

Some risks don't fit admitted standard carriers well. That's where specialty markets and surplus lines may come in.

These carriers are built for harder placements. They may have tighter terms, more exclusions, or higher deductibles, but they can still provide a path to coverage when standard options disappear. For tenants with prior losses, difficult property characteristics, or layered risk factors, this can be the market that keeps the move-in on track.

This isn't always a do-it-yourself shopping project. Specialty carriers often require more complete submissions, and the wording matters.

A high-risk placement succeeds when the risk is described accurately and sent to a carrier that already expects complexity.

Landlord-provided plans

There's also a lesser-known option when individual renters policies are difficult to obtain. According to this discussion of the renters coverage gap and landlord alternatives, Tenant Protector Plan® and similar landlord-provided arrangements can cover tenant-caused losses without requiring tenant qualification.

That option won't replace every benefit of a full renters policy. It may be narrower, and the exact protection depends on the plan. But for a tenant who keeps hitting underwriting walls, it can be a practical fallback, especially when the landlord is mainly trying to manage property damage exposure.

Quick comparison of the three paths

| Option | Best for | Trade-off |

|---|---|---|

| Independent agent | Tenants with denials, mixed risk factors, or limited time | Requires a conversation and document sharing, not just instant online checkout |

| Specialty or non-standard carrier | Harder risks that standard carriers avoid | Terms may be less broad and pricing may be tougher |

| Landlord-provided plan | Tenants who can't qualify for individual coverage | May not provide the same personal property and liability structure as a full renters policy |

What usually wastes time

A lot of tenants bounce between comparison sites hoping one more quote form will produce a miracle. Sometimes it does. Usually it doesn't.

If you've already been declined more than once, stop feeding the same file into more public quote engines. Move to a channel built for exceptions.

Renters Insurance Costs in FL, GA, AL, NC, SC, TN, and VA

Pricing across the Southeast isn't uniform, and high-risk tenants feel that quickly. The premium depends on more than your credit or claims history. The building, ZIP code, and local weather patterns all matter.

Industry data summarized by IBISWorld's renters insurance market overview shows that renters in high-risk states pay substantially more for coverage, and Alabama renters face some of the highest average premiums. The same source also notes a critical issue for many Southeastern renters: standard renters policies do not cover flood damage, so tenants in flood-prone areas may need separate NFIP contents coverage up to $100,000.

Why Southeast pricing feels different

Florida and the coastal Carolinas bring hurricane and water concerns. Alabama and Tennessee often deal with severe storm exposure. Older apartment stock in many cities adds plumbing and electrical concerns that carriers price into the policy even when the tenant has never filed a claim.

Georgia and Virginia can look more moderate on one block and much tougher on the next, depending on crime patterns, prior building losses, and local catastrophe modeling. That's why two tenants with similar backgrounds can see very different options based on address alone.

What raises the premium for a high-risk tenant

The premium usually moves up when several issues stack together. A carrier may tolerate one concern. It gets stricter when the file shows multiple concerns at once.

Common cost drivers include:

- A difficult ZIP code with theft, fire, or weather-related loss patterns

- A building with older systems or prior water problems

- A prior claim history that suggests repeat exposure

- Credit challenges or payment concerns

- Added liability exposures such as certain pets or smoking

The flood issue many renters miss

A standard renters policy can still be useful in the Southeast, but it has to match the actual exposure. Flood is the big gap.

If you're renting in a coastal or flood-prone area, don't assume “water damage” and “flood” mean the same thing. They don't. That's why renters looking for whether renters insurance covers hurricane damage need to separate wind-related questions from flood-related ones.

If your apartment could take on rising water from outside the building, ask about flood separately. Don't assume your base renters policy handles it.

How to budget realistically

For high-risk tenants, the cheapest quote is often not the best quote. A policy with the wrong terms can create trouble later, especially around water, liability, or limited personal property amounts.

A smarter approach is to set a monthly budget range, decide what risks matter most at your address, and compare quotes based on actual protection. In this market, clear coverage beats a low headline price.

Common Questions from High-Risk Tenants

Will one small claim automatically get me denied

Not always. One claim doesn't automatically make a renter uninsurable. What matters is the type of claim, how recent it was, whether there are multiple claims, and whether the carrier sees other concerns in the file.

A single older claim is usually easier to work around than a cluster of recent losses.

Should I keep applying online until something sticks

Usually no. If you've already had repeated declines or referrals, more online quote attempts often waste time and create frustration.

At that point, your better move is to gather your documents, identify the likely issue, and submit through a person or channel that handles non-standard placements.

I don't own much. Do I really need renters insurance

Maybe more than you think. Even tenants with modest belongings can face real liability exposure if a guest is injured or if they accidentally cause damage that spreads beyond their unit.

The belongings matter. Liability often matters more.

What if my landlord requires coverage and I still can't qualify

Ask whether the landlord accepts alternatives, including a landlord-provided protection plan if one is available. Some landlords mainly want proof that there is some structure in place to address tenant-caused loss.

If the lease is strict, ask exactly what wording, liability limit, and additional insured or interested party language they require. Sometimes the issue is not inability to insure. It's that the policy and lease requirements don't match.

Should I hide a pet or old eviction if I think that's what caused the denial

No. That can create a bigger problem than the original underwriting issue. A policy issued on incomplete or inaccurate information can become a claim dispute later.

Give the full picture early and let the placement strategy fit the truth.

What should I do today if I need coverage fast

Take these steps in order:

- Pull together your basic file with ID, lease, address details, and any documents that explain prior issues.

- Write a short factual summary of anything likely to trigger underwriting review.

- Confirm the landlord's exact insurance requirement so you don't buy the wrong policy.

- Ask about flood separately if the property is in a flood-prone area.

- Stop chasing generic quote forms if you've already been declined and move to a channel that handles harder risks.

Renters insurance for high-risk tenants is rarely about finding a magic website. It's about matching the actual risk to the right market, with honest information and a clean submission.

If you need help sorting through denials or finding a carrier that will review a tougher file, Select Insurance Group, Inc. can compare options across multiple carriers for renters in Alabama, Florida, Georgia, North Carolina, South Carolina, Tennessee, and Virginia. Their team works with standard and non-standard markets, offers bilingual support, and can help you move from “declined” to a realistic path forward with a free, no-obligation quote.