Workers' compensation insurance is built to cover medical care and partial wage replacement when an employee is hurt or becomes ill because of work. It also commonly covers rehabilitation, permanent disability, and death benefits, making it a basic financial safety net for both the worker and the business.

If you're a small business owner, you're probably not reading this because insurance is exciting. You're reading because you hired someone, payroll is growing, or a certificate request landed on your desk, and now you're trying to answer a practical question: What does workers compensation insurance cover, and what does it mean for my business if someone gets hurt?

The short version is that workers' comp is meant to keep a workplace injury from becoming two separate crises at once. One crisis is human: an employee needs treatment and may not be able to work for a while. The other is financial: the business needs a clear, legal way to respond without spiraling into confusion, conflict, or a lawsuit over every accident.

That sounds simple until you get into the details. Does it only apply to sudden accidents? What about repetitive stress? Who counts as an employee if you use part-time help, family members, or subcontractors? And if you have workers' comp, are you automatically protected from employee lawsuits?

Those are the questions that matter in real life, so let's unpack them in plain English.

Table of Contents

- What Is Workers Compensation and Why Is It Required

- The Four Core Benefits Workers Comp Covers in Detail

- Who Is Covered and What Are Common Exclusions

- Navigating a Claim The Employer Responsibility Guide

- Does Workers Comp Protect My Business from Lawsuits

- State-Specific Rules for Business Owners in the Southeast

- Protect Your Team and Your Business Today

What Is Workers Compensation and Why Is It Required

Workers' compensation is easiest to understand if you think of it as a pre-agreed deal between employer and employee.

An employee gets hurt doing the job. Instead of having to prove the employer was negligent in order to get help, the employee can access benefits through a no-fault system. In exchange, the employer usually gains protection from many workplace injury lawsuits. New York's workers' compensation board describes this framework as a no-fault benefit system that covers medical treatment, income replacement, permanent disability, and death benefits, while the worker gives up the right to sue in most cases for workplace injuries under that arrangement (New York workers' compensation overview).

The basic idea behind the system

This is why insurance people sometimes describe workers' comp as a kind of "grand bargain." It isn't charity, and it isn't a general health plan. It's a work-injury system with rules, defined benefits, and a tradeoff built into it.

For a business owner, that matters because it changes the question from "Who caused this?" to "What does the policy require us to do next?"

Practical rule: Workers' comp is designed to respond to work-related injury or illness without waiting for a blame fight.

That makes accidents more manageable. If a warehouse worker strains a back lifting inventory, or an office employee develops a repetitive-stress injury from daily computer work, the claim process is supposed to start from the work connection, not from a courtroom-style argument over fault.

Why states require it

Most employers don't buy workers' comp because it sounds nice. They buy it because state law usually requires it, and because running a business without it can leave both the employee and the company exposed.

The system also sits inside the broader cost of employing people. The CDC notes that workers' compensation is built to pay for medical care and partial wage replacement when an employee is injured or becomes ill because of the job. It also points out that workers' comp is one of the legally required benefits included in the employer benefits system, and the Bureau of Labor Statistics reported employer costs for private industry workers averaged $13.79 per hour worked in benefits in December 2025 (CDC overview of workers' compensation).

That doesn't mean every dollar of that amount is workers' comp. It means workers' comp belongs in the same category as the non-optional costs of employing people.

A good way to think about it is this:

- For employees: They need a reliable path to treatment and wage support after a work injury.

- For employers: They need a structured system that can handle claims without turning every incident into open-ended legal exposure.

- For the business itself: It creates a repeatable process. That's often the difference between a contained problem and a disruptive one.

If you're reviewing options, workers' compensation coverage for businesses is one place to see how this policy fits into a broader commercial insurance plan.

The Four Core Benefits Workers Comp Covers in Detail

When business owners ask what does workers compensation insurance cover, they usually mean, "What bills does it pay when something goes wrong?" That's the right question.

At the claim level, workers' comp generally breaks into four buckets: medical treatment, income replacement, permanent disability, and death benefits. Those categories come from the same no-fault structure described by New York's workers' compensation board, which also notes that coverage can include emergency care, surgery, prescriptions, rehabilitation, ongoing care, wage replacement during time away from work, compensation for lasting impairment, and funeral or death benefits for survivors after a fatal work injury or illness.

Medical treatment

Medical coverage is the part generally understood first.

If an employee slips on a wet floor in a stockroom and fractures a wrist, workers' comp may respond to the ambulance ride if needed, the emergency room visit, imaging, follow-up appointments, casting, medication, and later physical therapy if the employee needs help regaining motion.

That list matters because "medical bills" is broader than a single doctor visit. It can include treatment that unfolds over time.

- Immediate care: Emergency treatment after the injury.

- Corrective treatment: Surgery, specialist visits, or prescribed care.

- Follow-up care: Therapy, rehab, medication, and ongoing monitoring.

A lot of owners underestimate this part. They picture a one-time clinic bill when the actual claim may involve a chain of treatment decisions over weeks or months.

Income replacement and disability

The second bucket is wage support. If the employee can't work while recovering, workers' comp can replace part of lost income. The key word is part.

It usually doesn't function like full payroll. Instead, it helps bridge the gap while the worker is temporarily out, working reduced duty, or dealing with a lasting impairment that affects earning ability.

The practical purpose isn't to make the employee financially whole in every possible way. It's to keep a work injury from cutting off income entirely while recovery is underway.

This category can also overlap with disability questions. If the injury leaves lasting limitations, the claim may move beyond short-term missed work and into compensation tied to permanent impairment.

Rehabilitation and return to work

This is one of the most overlooked parts of coverage.

When people think about workers' comp, they think of treatment and checks. But rehabilitation is often what gets the employee back into a productive routine. That can mean physical rehabilitation, ongoing care, or support tied to returning to work in a safe way.

A simple example: a technician injures a shoulder and can't immediately return to the same lifting demands. The claim isn't only about paying the first medical bill. It's also about supporting recovery so the employee can resume work, whether in the same role or with adjusted duties.

Death benefits

This is the hardest category to discuss, but it belongs in any honest explanation.

If a worker dies because of a job-related injury or illness, workers' comp can provide benefits to survivors. That may include funeral or death benefits and support for dependents.

This is part of why the policy matters so much. Workers' comp is designed for situations that are minor, serious, and tragic. The same framework that pays for a stitched hand can also respond when a workplace event permanently changes a family's life.

Here's the cleanest way to remember the four categories:

| Benefit category | What it generally addresses |

|---|---|

| Medical treatment | Care needed because of the work injury or illness |

| Income replacement | Partial wage support during time away from work |

| Permanent disability | Compensation when impairment lasts |

| Death benefits | Financial support to survivors after a fatal work-related event |

Who Is Covered and What Are Common Exclusions

One of the biggest mistakes small business owners make is assuming "employee" only means full-time staff on a simple payroll setup. Real life is messier than that.

The definition of employee is wider than many owners expect

Virginia's workers' compensation commission notes that covered workers can include part-time workers, seasonal workers, temporary workers, minors, trainees, immigrants, and family members, and that contractor or subcontractor headcount can affect whether coverage is required at all (Virginia employer guidance on workers' compensation).

That should get your attention if you run a business with flexible staffing.

A landscaping company may bring on seasonal help. A family restaurant may have a relative on payroll a few days a week. A contractor may use a mix of direct employees and subs. A retail shop may add temporary staff for holiday periods. In those situations, the legal question often isn't "Do I consider this person a real employee?" It's "How does my state classify this worker for workers' comp purposes?"

If someone works in your business, under your direction, and inside your operations, don't assume their label answers the coverage question.

Independent contractors can be a source of trouble for owners. Calling someone a contractor doesn't automatically make workers' comp disappear. If the state views that person differently, your paperwork label may not protect you.

Where owners get tripped up

The safest mindset is to treat worker classification as a compliance issue, not just a payroll preference.

Common problem areas include:

- Part-time help: Fewer hours doesn't always mean fewer legal obligations.

- Seasonal labor: Short-term work can still trigger coverage requirements.

- Family members: Informal family arrangements still need formal insurance thinking.

- Subcontractor setups: Headcount and job structure can affect whether coverage is required.

- Trainees or minors: Inexperience doesn't remove exposure.

Now, what about exclusions? This is where nuance matters. Workers' comp covers work-related injuries and illnesses, but that doesn't mean every injury in or around work is covered in every situation.

In plain terms, disputes often arise when the injury falls outside job duties, outside work-related activity, or involves conduct that breaks the rules of the system. Owners also get confused because a claim can be denied without meaning the entire policy is useless. It may mean the facts didn't fit the coverage trigger.

A practical way to think about boundaries:

- Likely inside the system: An employee strains a knee unloading goods, develops carpal tunnel from repetitive work, or becomes ill because of job-related exposure.

- Likely disputed: An injury with a weak connection to the job, conflicting facts, or activity that wasn't part of work duties.

- Needs careful review: Contractor-heavy operations, family-run businesses, and businesses with mixed roles.

The modern version of workers' comp isn't just about what the policy pays for after an injury. It's also about making sure the right people are inside the policy before an injury ever happens.

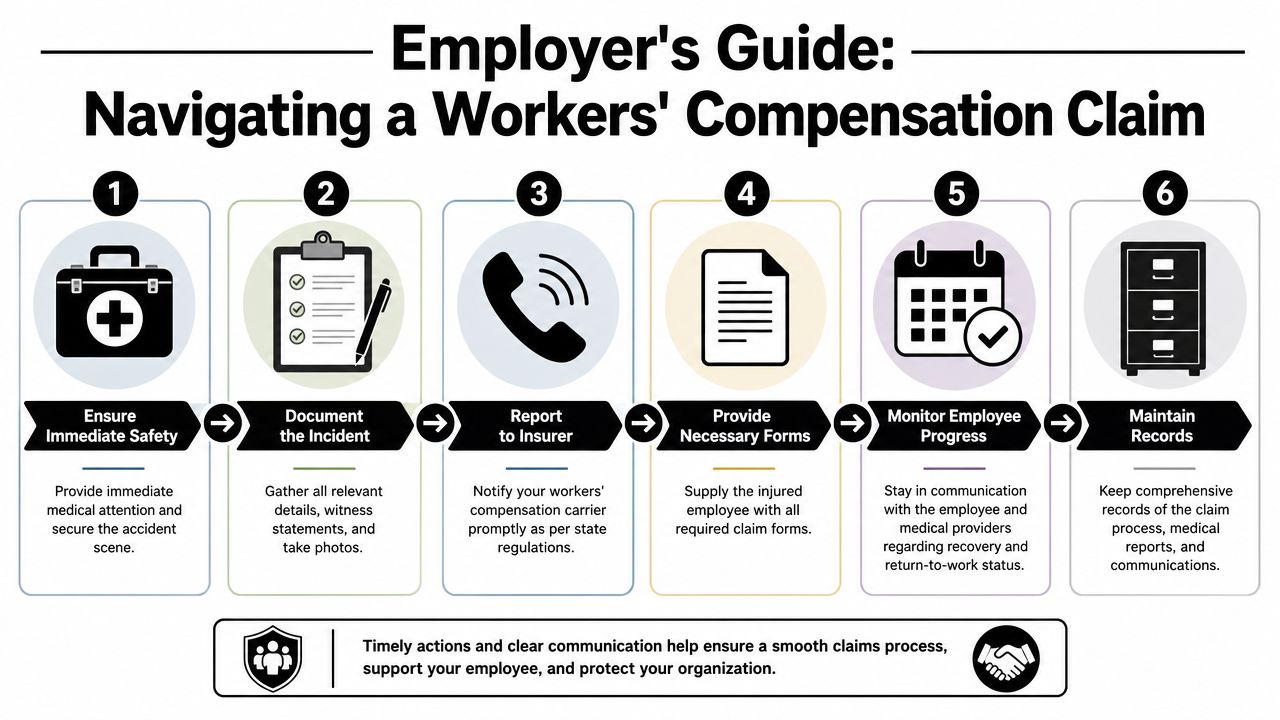

Navigating a Claim The Employer Responsibility Guide

Once an injury is reported, clarity matters more than speed for its own sake. Employers need to act quickly, but they also need to act in the right order.

Coverage isn't limited to dramatic accidents. It can also include occupational disease and repetitive-stress injuries such as carpal tunnel syndrome, and state thresholds for when coverage is required vary. The Hartford notes that many states require coverage starting with at least one employee, though thresholds differ. It gives examples including Florida, which requires workers' comp for construction employers with one or more employees and for non-construction employers with four or more employees.

The first moves matter most

When someone gets hurt, use a simple checklist.

Make sure the employee is safe. Get emergency care if it's needed. If the situation isn't an emergency, still take the injury seriously and direct the employee to appropriate medical attention under your state's process.

Stabilize the scene. If equipment, materials, or conditions contributed to the injury, secure the area so no one else gets hurt.

Write down the facts early. Record what happened, when it happened, where it happened, who saw it, and what work the employee was doing at the time.

Report the claim promptly. Contact your carrier and follow the required reporting steps. If you need a starting point, report a workers' compensation claim through the designated claim support process tied to your policy.

What good claim handling looks like

Many claim headaches come from small gaps in communication.

- Speak with the employee: Keep the tone calm and factual. You don't need to argue about fault.

- Collect witness details: Memories fade quickly, especially after a stressful event.

- Keep records organized: Save forms, notes, medical updates, and communication logs in one place.

- Track work status: Know whether the employee is out, restricted, or cleared for some duties.

A well-handled claim usually looks boring on the surface. The paperwork is complete, the timeline is clear, and nobody has to reconstruct the story later.

Don't limit this process to obvious accidents. A repetitive-stress complaint, an exposure-related illness, or a gradually worsening condition can require the same discipline. If an employee says, "My hand has been going numb for weeks," that's still a workers' comp conversation, not something to ignore because there wasn't a single dramatic incident.

Does Workers Comp Protect My Business from Lawsuits

This is the question many articles skip, and it's one of the most important ones.

Why the answer is usually but not always

Workers' comp is often described as the employee's exclusive remedy for job-related injury. In everyday terms, that means the employee typically uses the workers' comp system instead of suing the employer over the injury.

That protection is a major reason the system exists. But it isn't always automatic or complete in every situation.

A key coverage gap can arise in monopolistic states, where standard workers' comp may cover employee benefits yet still leave the employer exposed to employee negligence suits unless stop-gap or employers liability protection is added. This gap is described as distinct and important in industry guidance on stop-gap coverage.

That means you shouldn't assume "I have workers' comp" automatically equals "I'm fully shielded from every employee injury lawsuit."

Where stop-gap and employers liability enter the picture

Think of workers' comp benefits and employer lawsuit protection as two related layers.

The first layer pays the injured worker's covered benefits. The second layer helps address the employer's legal exposure in situations where the standard workers' comp structure doesn't fully close the loop.

If your business operates across state lines, uses unusual staffing arrangements, or works in states with different insurance frameworks, this question matters even more. The compliance side of hiring, classification, documentation, and policy design also affects how exposed your business may be after an injury. For a broader operational view, this essential HR compliance guide is a useful companion resource because workers' comp problems often start as people-process problems before they become insurance disputes.

A good rule for owners is simple:

- Don't assume every workers' comp policy solves every liability issue

- Ask whether employers liability is included

- If you operate in a monopolistic state, ask specifically about stop-gap coverage

That one question can reveal a gap that many owners don't know exists until after a claim turns legal.

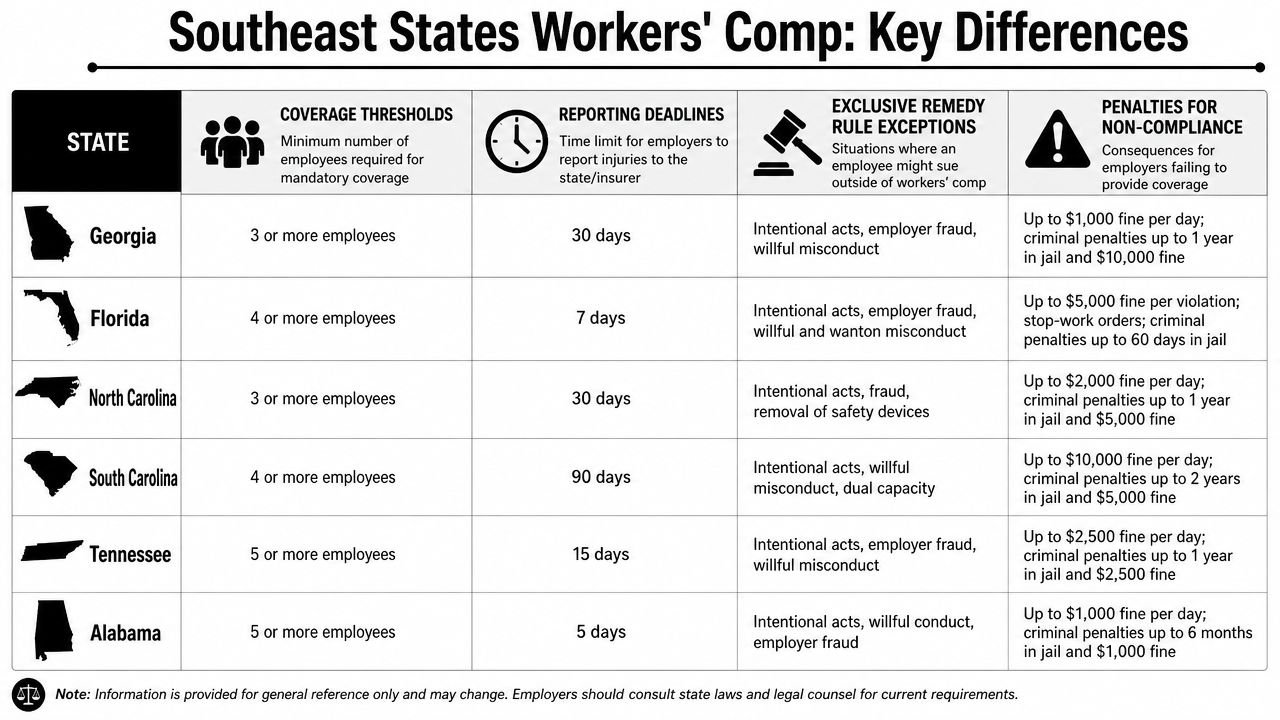

State-Specific Rules for Business Owners in the Southeast

If you operate in more than one Southeastern state, workers' comp can feel like driving through counties where the speed limit changes every few miles. The basic concept stays the same, but the trigger points and practical rules don't.

A practical comparison for regional employers

The visual below highlights how state-by-state differences matter to owners with regional operations.

Here's a practical comparison table focused on the Southeast.

| State | Employee Threshold (Non-Construction) | Employee Threshold (Construction) | Notes |

|---|---|---|---|

| Alabama | Varies by state rule | Varies by state rule | Review current state requirements before hiring growth changes your obligation |

| Florida | Four or more employees | One or more employees | Verified threshold example from the Hartford source linked earlier |

| Georgia | Varies by state rule | Varies by state rule | Construction and subcontractor arrangements deserve extra review |

| North Carolina | Varies by state rule | Varies by state rule | Headcount changes can shift your compliance duties |

| South Carolina | Varies by state rule | Varies by state rule | Multi-location employers should confirm state-specific treatment |

| Tennessee | Varies by state rule | Varies by state rule | Contractor-heavy businesses should review worker classification carefully |

| Virginia | State guidance describes coverage as mandatory based on employer and worker status rules | State guidance also considers contractor and subcontractor headcount | Virginia explicitly notes that part-time, seasonal, temporary workers, minors, trainees, immigrants, and family members can count for coverage analysis |

Only Florida's threshold details were provided in the verified material, so it's better to stay qualitative for the other states than to pretend the rules are identical or to guess at numbers.

How to use the table without overcomplicating it

A small business owner usually needs three answers:

- At what headcount does my state require coverage?

- Does construction get treated differently?

- Do subs or family members change the answer?

If your company operates across state lines, those answers can change even when the work itself looks the same. A roofing crew, restaurant group, or small delivery business may have one staffing model but several legal environments.

State rules don't just affect whether you buy the policy. They affect who must be included, when coverage is triggered, and how fast a problem can grow if you guessed wrong.

For businesses that work across the region, a multi-state insurance agency serving Florida, South Carolina, and North Carolina can help sort out how policies and state requirements line up when your workforce doesn't stay neatly inside one border.

Protect Your Team and Your Business Today

Workers' comp is easy to underappreciate until the day you need it.

At that moment, the value becomes very concrete. An employee needs care. Pay may be interrupted. Questions about job status, reporting, and legal responsibility all arrive at once. A well-structured workers' comp setup gives you a playbook for that moment.

The key takeaways are straightforward:

- It covers more than doctor bills. Medical treatment, partial wage replacement, rehabilitation, permanent disability, and death benefits can all be part of the picture.

- Who counts as an employee isn't always obvious. Part-time staff, seasonal workers, family members, and contractor-related headcount can all matter.

- Lawsuit protection may have limits. In some situations, employers liability or stop-gap protection is the missing piece.

This is also why general state summaries are useful as background, especially if you're comparing obligations or reviewing hiring plans. If you want a broader reference point, this 2026 guide on workers' comp state rules can help you frame questions to bring back to your agent or legal advisor.

For business owners who want a practical next step, Select Insurance Group, Inc. offers workers' compensation insurance as part of its commercial coverage options, including support for businesses operating in multiple Southeastern states.

The right policy does more than satisfy a requirement. It helps you protect the people who keep your business running, while reducing the odds that one injury turns into a much larger business problem.

If you're reviewing your current workers' comp policy, hiring your first employee, or expanding into another state, Select Insurance Group, Inc. can help you compare coverage options and understand how workers' compensation fits your broader business insurance plan. Reach out for a free, no-obligation quote and get clear answers before a claim forces the issue.