You're probably here because you typed “universal insurance company” into Google and got a messy mix of results. Some pages talk about a Florida homeowners insurer. Others talk about a public policy idea called “universal insurance.” That's a problem if you're just trying to figure out whether this carrier is worth trusting with your home.

Here's the straight answer. Universal Property & Casualty Insurance Company is a real property insurer tied to Universal Insurance Holdings. It is not the same thing as the broader idea of “universal insurance.” If you own a home in Florida or another coastal market, that distinction matters because this company should be judged like a property carrier, not like a catchall insurance concept.

Table of Contents

- An Introduction to Universal Insurance Company

- Analyzing Financial Strength and Company Ratings

- A Guide to Universal's Insurance Products

- Navigating the Universal Claims Process

- How Universal Determines Your Insurance Premiums

- Is Universal Insurance the Right Choice for You

- Compare Universal and Find Your Best Rate Today

- Frequently Asked Questions About Universal

An Introduction to Universal Insurance Company

Your mortgage company needs proof of homeowners insurance. You start searching for "Universal Insurance Company" and run into two different ideas at once. One is a Florida-based insurer. The other is the generic phrase "universal insurance," which people often use loosely and sometimes confuse with other insurance products entirely.

Clear that up first. Universal Insurance Company usually refers to Universal Property & Casualty Insurance Company, the insurer homeowners are shopping for. It sits under Universal Insurance Holdings, Inc., the parent company. The parent was originally incorporated as Universal Heights, Inc. in November 1990, and company filings state it writes business across 19 states (corporate filing details).

That distinction matters.

If you are comparing quotes, the operating insurer is what affects your policy forms, underwriting, claims handling, and the financial backing behind the contract. The parent company matters too, but the name on the actual policy is what you should verify before you buy.

Universal gets attention for a simple reason. It has long focused on property coverage in a tough coastal market, especially Florida. That makes it more relevant for homeowners worried about wind, hail, roof restrictions, and catastrophe exposure than a carrier trying to be everything to everyone.

My view is straightforward. Universal is worth a serious look if you own a home in Florida or another higher-risk property market and you want a carrier with a long operating history in that space. It is not a name you should choose just because it sounds broad or familiar.

One more point, because this confusion is common. "Universal Insurance Company" is not the same thing as the broad idea of "universal insurance." And it has nothing to do with health coverage unless you are reading about a completely different product. If your search drifted into medical coverage, use this health insurance guide for 2026 to sort out the basics before you compare policies that solve completely different risks.

Analyzing Financial Strength and Company Ratings

A storm claim is the worst time to learn what your insurer is made of. If you are looking at Universal Property & Casualty Insurance Company, start with the balance sheet and the rating agencies, not the brand name. That matters even more here because some shoppers confuse Florida-based Universal Insurance Company with the general idea of "universal insurance," which is not a carrier evaluation at all.

Universal Property & Casualty Insurance Company holds an A- (Excellent) financial strength rating from AM Best with a Positive outlook as of September 26, 2025. The same AM Best disclosure says the company serves more than 800,000 policyholders and is a leading property writer in Florida (AM Best rating profile).

What the AM Best rating tells you

An A- (Excellent) rating is a good sign. It means AM Best views the insurer as having a strong ability to meet ongoing insurance obligations on the rating date.

For homeowners, that usually means three practical things:

- Better claims-paying confidence: In hurricane and severe weather markets, financial strength matters more than polished advertising.

- More credibility with lenders and agents: Ratings affect how the carrier is viewed by the people involved in your transaction.

- Meaningful operating scale: A carrier with a large property book in Florida is dealing with real catastrophe exposure, not testing the market.

That does not mean Universal is the right fit for every property owner. It means the company clears the first serious screening step. I would not buy a home policy in a catastrophe-prone state from any carrier with weak financial backing, regardless of how low the quote looks.

Why reinsurance matters here

For a Florida-focused property insurer, reinsurance is part of the business model. It is the layer of protection that helps absorb losses after major storm events.

Universal's publicly stated reinsurance utilization measure is 30% to 40% of premium, based on company information referenced by Demotech (reinsurance and company profile details).

Here is my read. That level of reinsurance use shows the company is structured for catastrophe exposure, which is what you want in this market. It also means profitability can get squeezed when reinsurance prices rise, and that pressure can affect rates and underwriting.

So the rating is good. The reinsurance dependence is normal for this type of insurer. The smart conclusion is not blind confidence or automatic rejection. It is this: Universal makes the most sense for property owners who want a carrier built for coastal risk and who understand that Florida insurance pricing reflects storm exposure, not just the insurer's name.

If your insurance needs are tied to freight rather than residential property, this cargo insurance guide for trucking companies covers a completely different type of risk.

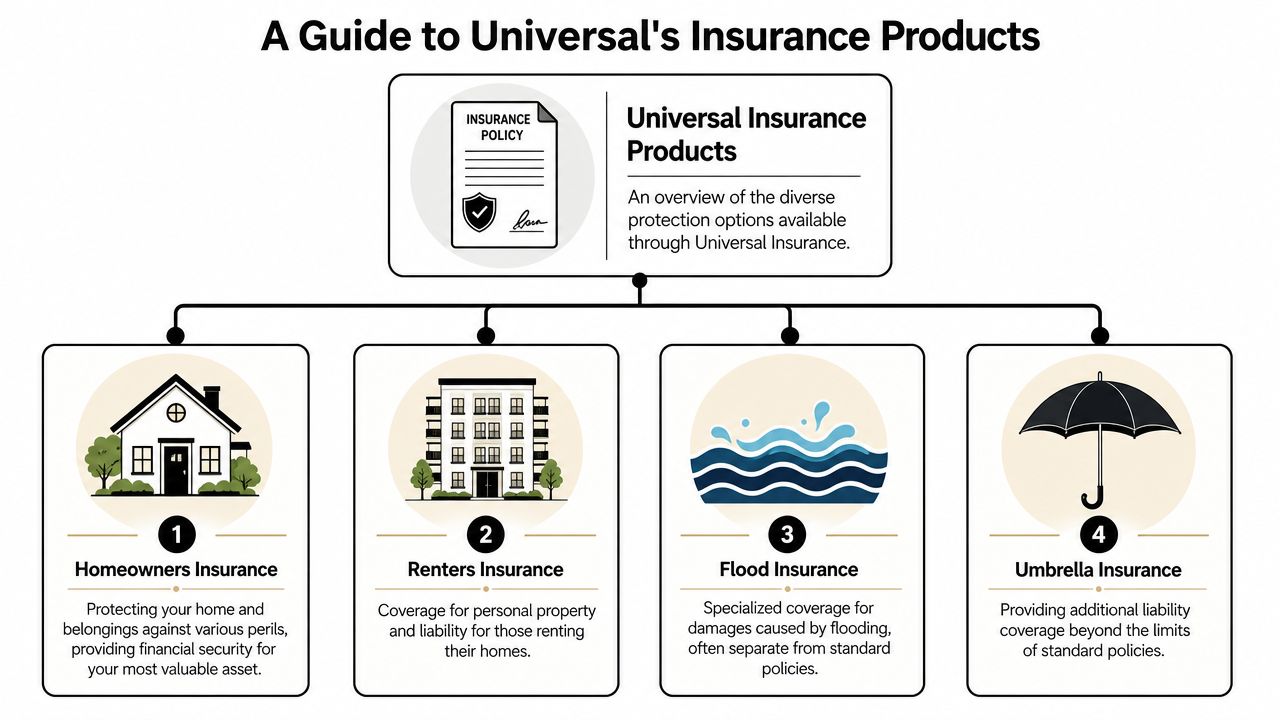

A Guide to Universal's Insurance Products

Universal isn't the place to start if you want a one-stop giant that handles every possible personal and commercial line under the sun. That's not the value here. The value is property focus.

The company is best understood as a carrier built around home-related risk. That means the right question isn't “Do they insure everything?” The right question is “Do they fit the kind of property I need to protect?”

Where Universal fits best

Universal is most relevant for people insuring residential property exposure. Think homeowners, condo owners, landlords with dwelling coverage needs, and people who may need related liability protection tied to a residence.

A simple way to frame it:

| Property situation | Policy focus |

|---|---|

| You own a single-family house | Standard homeowners coverage is usually the starting point |

| You own a condo unit | Condo-style coverage usually focuses more on your interior, personal property, and liability |

| You own a rental dwelling | A landlord or dwelling-type policy is often the better fit |

| You're worried about a liability claim that exceeds basic limits | Umbrella coverage may make sense |

How to think about the main policy types

People get tripped up by policy forms, so keep it simple.

- Homeowners coverage: This is your broad home protection policy. It's designed for owner-occupied houses and usually combines dwelling, other structures, personal property, liability, and loss-of-use features.

- Condo coverage: This is more like insuring the part of the home you own inside the walls. The building association often insures common elements, while you insure your interior exposure and belongings.

- Dwelling or landlord-style coverage: If the property is rented out, don't assume a standard owner-occupied policy works. Occupancy matters.

- Flood protection: Standard homeowners policies generally don't cover flood damage. If flood is part of your risk, treat that as a separate buying decision.

Buy the policy that matches how the property is used. Don't try to force an owner-occupied form onto a rental property or assume condo coverage works like house coverage.

If your insurance needs stretch into commercial hauling, don't mix that up with residential property insurance either. A business owner looking into freight exposure needs a different framework altogether, and this cargo insurance guide for trucking companies is useful for that separate risk category.

Navigating the Universal Claims Process

A policy looks good on paper until you have to use it. That's when details matter. The claims process for a property loss is usually straightforward in outline and frustrating in practice, especially after a wind event when everyone in your area is filing at once.

A realistic claim example

Say a storm tears shingles off your roof and rain gets inside. You discover staining on the ceiling, wet insulation, and damage to flooring in one room. Your job is to move quickly and document everything.

Start with the basics:

- Prevent further damage. Tarp the roof if it's safe and reasonable to do so.

- Report the claim promptly. Delays can complicate inspections and payment discussions.

- Photograph the damage before cleanup. Take wide shots and close-ups.

- Save repair receipts and emergency mitigation invoices.

- Meet the adjuster and ask direct questions about scope.

That last step matters more than is commonly appreciated. A claim dispute often starts because the homeowner thinks the carrier is paying for “the whole problem,” while the adjuster is paying for a narrower, documented scope.

Exclusions that trip people up

Homeowners often get blindsided. Standard property policies often exclude some major risks or limit how they're handled.

Common trouble spots include:

- Flood damage: Rising water is usually not covered under a standard homeowners policy.

- Neglect or maintenance issues: Insurance covers sudden accidental loss, not long-term wear.

- Earth movement: This is often outside normal homeowners coverage.

- Code upgrades: Some policies limit what's paid unless you carry added protection.

If your roofer or contractor finds missing items in the adjuster's estimate, handle that carefully and with documentation. For a cleaner look at that process, these tips for roofing insurance supplements can help you understand how line-item disputes usually develop.

The fastest way to create a bad claim outcome is to assume coverage before you read the exclusions.

How Universal Determines Your Insurance Premiums

Two houses can sit on the same street and still get different premiums. That isn't random. Property insurers price risk based on the structure, the location, and the loss profile they think you bring to the table.

Universal also uses outside analytics to sharpen that process. According to Verisk, Universal Property uses Verisk's ecosystem for advanced underwriting and claims analytics to improve risk selection and pricing in catastrophe-prone markets (underwriting and claims analytics announcement).

The biggest pricing drivers

From an agent's perspective, these are usually the pressure points:

- Location: Coastal exposure, local weather patterns, and claim environment matter.

- Roof characteristics: Age, shape, material, and condition can move the quote a lot.

- Construction type: Masonry, frame, and other features affect expected loss severity.

- Claims history: Prior losses can change both pricing and eligibility.

- Coverage choices: Deductibles, limits, endorsements, and optional protections all affect cost.

Here's a simple reference table:

| Factor | Why it matters |

|---|---|

| Roof age and condition | Older or worn roofs often produce more underwriting scrutiny |

| Distance to coast or storm exposure | Higher catastrophe risk usually raises rates |

| Prior property claims | Repeated losses can signal higher expected future cost |

| Protective devices | Alarms and other safeguards may improve the risk profile |

Why data and analytics affect your quote

Analytics help a carrier standardize decisions across a large book of business. That can be good for you if your home is well-maintained and fits the underwriting appetite. It can also hurt if the data flags characteristics associated with higher loss potential.

This is why I tell clients not to argue in the abstract about whether a premium is “fair.” Break it into components. Ask what the carrier is seeing in the roof, claims history, construction, and hazard profile. Then fix what you can.

And don't confuse property pricing with auto pricing. If you're sorting through how violations affect personal auto rates, this guide on how long traffic tickets affect insurance covers a very different rating system.

Is Universal Insurance the Right Choice for You

Universal is a serious option for the right homeowner. It is not the right carrier for everyone.

If you want a property insurer with clear experience in tough coastal markets, Universal deserves a look. If you want broad product variety or you expect every carrier to price aggressively in high-risk areas, adjust your expectations.

Good fit for

- Florida and coastal homeowners: Universal has meaningful presence and property focus in storm-sensitive regions.

- People who value insurer strength: The company's AM Best rating and large policyholder base support confidence in its position.

- Owners with straightforward property needs: If your main concern is home-related coverage, a specialist can make more sense than a generalist.

Not a great fit for

- Shoppers who only care about the cheapest premium: In hard markets, disciplined carriers may not be the lowest quote.

- People looking for every insurance line under one roof: Universal's appeal is property concentration, not universal product breadth.

- Homeowners with unusual risk features: Older roofs, prior claims, or complex occupancy issues can make placement harder.

My opinion: Universal is strongest when you need a carrier that understands residential property exposure in a difficult market and you're willing to judge the policy on coverage quality and carrier discipline, not just sticker price.

If you're not sure how to evaluate that tradeoff, it helps to understand what an independent insurance agency does when comparing carriers and coverage structures.

Compare Universal and Find Your Best Rate Today

Getting one quote from Universal won't tell you whether Universal is the best fit. It only tells you what Universal is willing to offer. That's not the same thing.

A smart buyer compares coverage, deductible structure, exclusions, and price side by side. If you don't, you can end up choosing a lower premium that creates a worse claim outcome later.

Here's my recommendation. Compare Universal against other available options at the same time, with the same property details, and with enough scrutiny to catch meaningful coverage differences. Price without context is noise.

If you're changing carriers during that process, read this short guide on how to switch auto insurance companies so you don't create an accidental lapse on another policy while reorganizing your insurance.

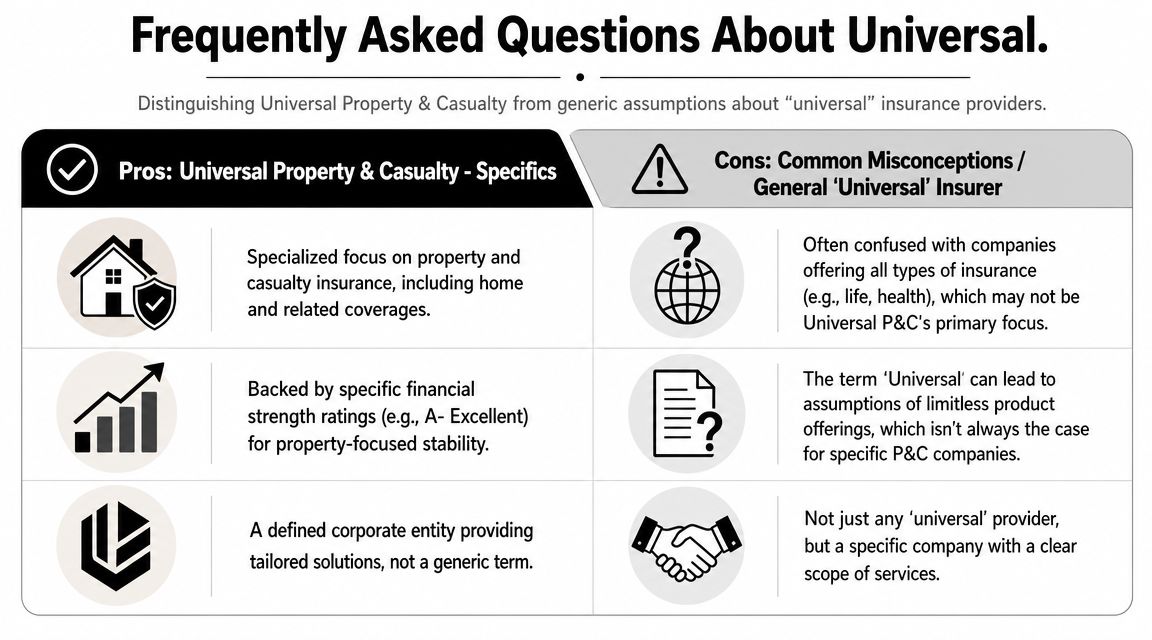

Frequently Asked Questions About Universal

Is Universal Insurance Company the same as universal insurance

No. This is the biggest point of confusion.

Universal Insurance Holdings refers to a specific Florida-based insurer group. Universal insurance can also refer to a social policy model discussed in public policy circles. Search results often blur the two, which is why people land on the wrong type of article in the first place, as noted in this discussion of the difference between Universal Insurance Holdings and universal insurance as a policy concept.

Is Universal a strong option for Florida homeowners

It can be. I think it's most compelling for homeowners who want a property-focused carrier with real scale in a difficult market. Florida isn't a place where I'd choose a carrier casually. I'd look hard at underwriting discipline, financial strength, and how the policy handles the property's specific risk profile.

Does Universal offer every type of insurance

Don't assume that from the name. Universal is best understood as a property-focused insurer, not a company that automatically covers every personal and commercial need.

Should you buy from Universal without comparing quotes

No. Never buy a homeowners policy that way. Even if Universal looks strong on paper, coverage terms and pricing have to be compared against other available options for your exact address, roof, occupancy, and deductible preference.

If you want help reviewing Universal Insurance Company against other available carriers, Select Insurance Group, Inc. can do the comparison work for you. As an independent agency serving customers across the Southeast, their team can shop multiple options, explain coverage differences in plain English, and help you choose the right balance of protection and price without guesswork.