Renters insurance costs about $14 per month on average in the U.S. If you're wondering how much renters insurance is monthly, that number is a solid starting point, but your own price can land lower or higher depending on a few key details.

That's what surprises most first-time renters. They expect something closer to a big household bill, when renters insurance is usually one of the smallest protections in a monthly budget. The trick isn't just knowing the average. It's understanding which parts of the price are in your control, which parts aren't, and how to shape a policy that protects your stuff without paying for coverage you don't need.

A simple way to think about it is this: your premium is built from two buckets. One bucket holds things you can change, like your deductible and coverage limits. The other holds things you can't easily change, like your state, ZIP code, and local risk profile. Once you separate those two buckets, renters insurance gets much easier to understand.

Table of Contents

- Your Guide to Monthly Renters Insurance Costs

- Why Is Renters Insurance So Affordable

- How Location Shapes Your Monthly Premium

- Sample Renters Insurance Scenarios and Monthly Costs

- The 4 Key Levers That Determine Your Premium

- 4 Proven Strategies to Lower Your Renters Insurance Bill

- Get a Fast and Free Renters Insurance Quote Today

Your Guide to Monthly Renters Insurance Costs

A typical renters insurance policy often costs about as much per month as a couple of takeout coffees, which is why many first-time renters are surprised by how manageable it can be.

That starting point helps answer a common question, how much renters insurance is monthly, without making it sound like every renter should expect the exact same bill. The average is a reference point. Your actual premium is built from a mix of choices you control and conditions you do not.

For budgeting, renters insurance usually fits into the same steady category as your phone bill or streaming subscription. If you are trying to identify recurring costs in your budget, this is usually one of the easier expenses to plan for.

The part that confuses many renters is simple. Two people can rent similar apartments and still get different quotes.

Insurance companies look at fixed factors such as your location, local claim patterns, and state rules. You usually cannot change those. They also look at choices you can change, especially your coverage limits and deductible. Those are your main pricing levers, and they matter because they let you raise protection, lower cost, or find a middle ground that feels comfortable.

A deductible works like the amount you agree to handle yourself before the policy starts paying on a covered claim. A higher deductible often lowers your monthly premium, but it also means you need more cash set aside if something goes wrong. Coverage limits work like the size of the safety net. Larger limits usually cost more, but they protect more of what you own.

That is why the smartest way to shop is to ask, “Which part of this price can I adjust safely?” not just “What is the cheapest quote?”

You can also review common policy features through a home and renters insurance resource center before you buy. A little preparation makes quotes easier to compare and helps you avoid paying for more coverage than you need, or worse, buying too little and finding out after a claim.

Why Is Renters Insurance So Affordable

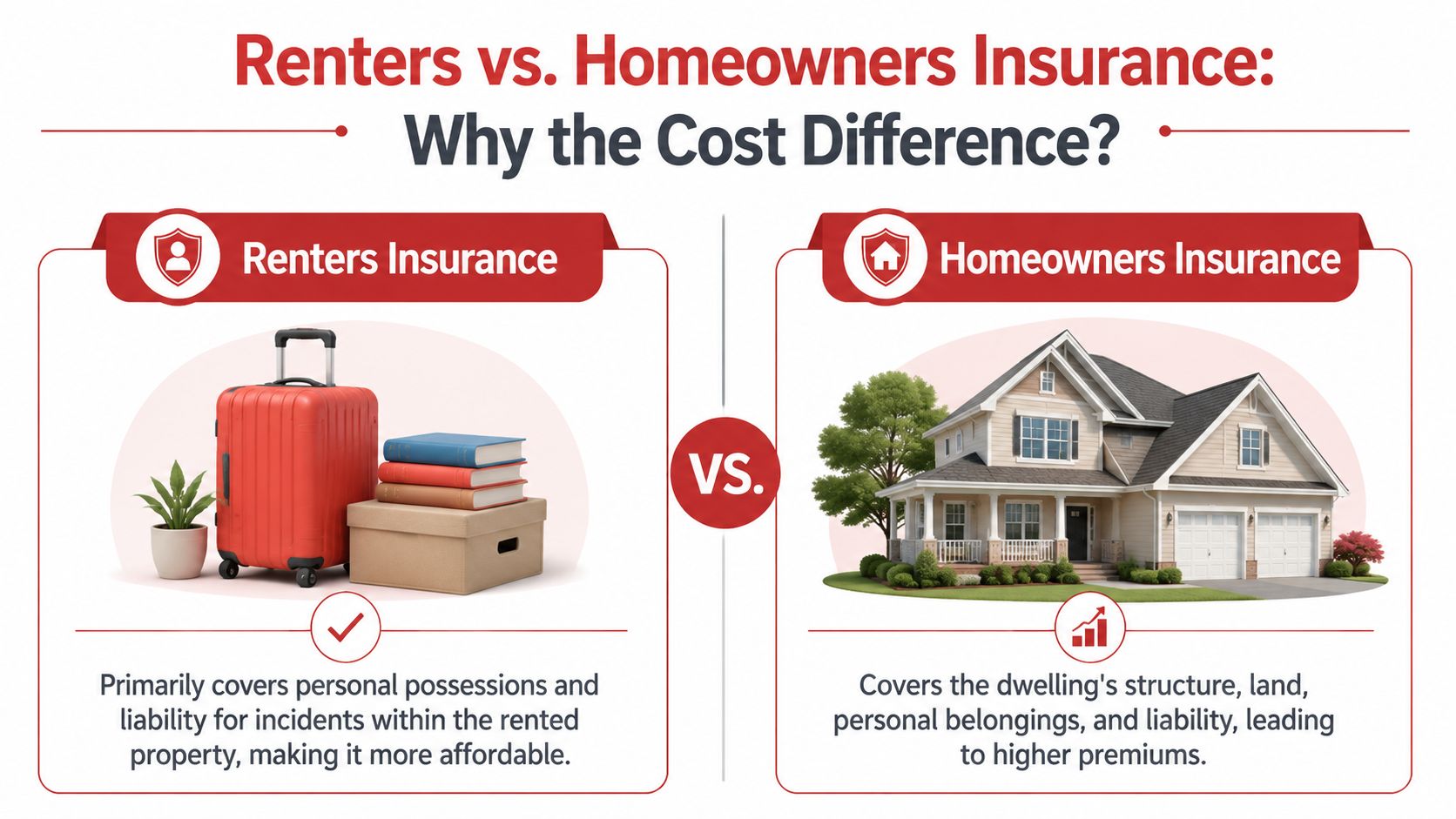

For many renters, this is one of the lowest-cost insurance policies they will ever buy. The main reason is simple. Renters insurance covers a smaller part of the total risk than homeowners insurance.

A homeowners policy has to account for the house itself, including major structural repairs or a full rebuild after a severe loss. A renters policy does not. Your landlord insures the building. You insure your belongings, your personal liability, and certain living costs if a covered claim forces you out for a while.

That narrower job keeps premiums lower.

What your premium is paying for

A renters policy is built around life inside the unit, not the structure around it. In plain terms, you are paying for protection in three main areas:

- Personal property: Items like clothes, furniture, electronics, cookware, and small appliances.

- Liability protection: Coverage if someone gets hurt and you are legally responsible, or if you accidentally damage someone else's property.

- Loss of use: Help with extra costs, such as a hotel or temporary meals, if a covered event makes your rental unlivable.

This is also where your choices matter. If you raise your personal property limit or choose a higher liability amount, your premium can go up. If you choose a higher deductible, your monthly cost often goes down because you agree to handle more of a smaller claim yourself. Those are the parts you can control.

Other price factors sit outside your control. Local weather risk, theft patterns, and insurer claim history in your area can all affect the base price before you make any policy choices. If you rent in a storm-prone area, it also helps to review how renters insurance covers hurricane damage so you know what is and is not included.

A simple way to picture the difference

A helpful comparison is this: renters insurance covers the contents and everyday risks tied to your rented space, while homeowners insurance also covers the building itself.

That difference matters more than many first-time renters realize. Replacing a sofa, laptop, mattress, and clothes after a fire is expensive. Paying for a roof, walls, wiring, and major reconstruction is far more expensive. Since your policy stops well short of covering the building, the monthly premium stays much lower.

Your policy protects your life inside the home, not the full property.

Low cost can make renters insurance easy to overlook. It should not be treated as a throwaway purchase, either. The goal is not just to find a cheap policy. The goal is to choose limits and a deductible that fit what you own, what you could afford out of pocket, and how much protection would help you sleep better at night.

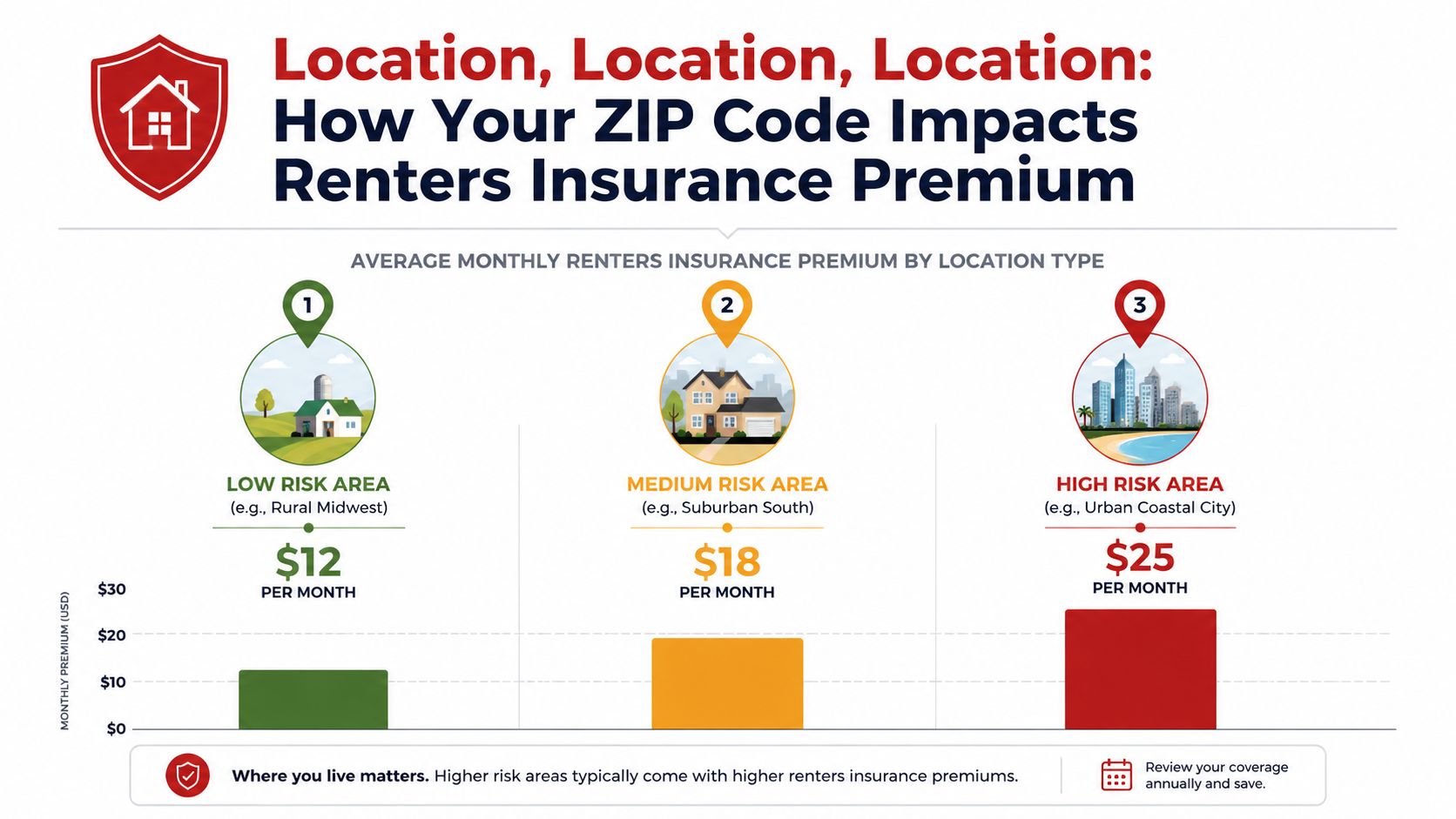

How Location Shapes Your Monthly Premium

Where you rent has a direct effect on what you pay. Two renters with similar belongings can get noticeably different quotes because they live in different states, cities, or ZIP codes.

State averages tell part of the story

NerdWallet's 2026 analysis found a national average of about $13 per month. The same analysis showed higher state averages in Georgia at about $18 per month, Alabama at about $17 per month, and Louisiana at about $22 per month, while some of the cheapest states came in around $8 to $10 per month, including Alaska at $101 per year and North Dakota at $117 per year (NerdWallet renters insurance state cost analysis).

If you rent in states served across the Southeast, that matters. A renter in Georgia or Alabama may already be starting above the national average before making any policy choices at all.

Why two renters in the same state can still pay different prices

Insurers price local risk, not just state names. They look at patterns like weather exposure, theft risk, claim frequency, and rebuilding or replacement conditions in the area. A coastal area, a storm-prone region, or a dense urban neighborhood can all push the monthly cost in different directions.

For renters in storm-prone areas, it also helps to understand what your policy does and doesn't include. If you live in a hurricane-exposed region, this guide on whether renters insurance covers hurricane damage can help you spot gaps before you buy.

Here's the key distinction. Location is mostly not in your control. If your ZIP code brings more risk, you probably won't “shop your way” out of that entirely. What you can do is avoid overreacting. Don't slash coverage just because the local rate runs higher than the national headline number.

Instead, use location as context:

- If your area runs high: Be careful and deliberate with deductibles and limits.

- If your area runs low: Don't assume the cheapest quote is automatically enough.

- If you're moving: Ask for a fresh quote before signing the lease, because a short move can change pricing.

A higher quote doesn't always mean the insurer is overcharging. Sometimes it means your location carries more risk.

That's one of the biggest misunderstandings around how much renters insurance is monthly. People often assume price differences are random. Usually, they reflect local conditions more than personal choice.

Sample Renters Insurance Scenarios and Monthly Costs

Averages are helpful, but they don't always feel real until you match them to an actual renter profile. The examples below show how your monthly price can shift based on the amount of stuff you own, the liability protection you want, and the deductible you choose.

These are not fixed market quotes. They're simple planning examples based on common renter situations, using the verified national and state benchmarks discussed earlier.

Scenario one, the student renter

A student renting a room or a small apartment often owns the basics: clothes, a laptop, textbooks, a phone, bedding, and some modest furniture. This renter may want a lean policy with enough personal property coverage for essentials and a standard liability limit.

A higher deductible can help keep the monthly bill lower, but only if that deductible is an amount the renter could realistically pay after a claim.

Scenario two, the young professional

A young professional in a city apartment usually has more furniture, more electronics, and a little more financial exposure. Think couch, bed, television, kitchen items, work equipment, and nicer personal belongings.

This renter might choose somewhat broader protection and a deductible that balances affordability with a reasonable out-of-pocket cost.

Scenario three, the small family renter

A small family renting a townhouse or suburban home tends to have the highest amount of personal property among the three examples. More beds, more furniture, more clothing, more household goods. Liability concerns may also feel more important if guests visit often.

In this case, a lower deductible can offer peace of mind, though it may raise the monthly premium compared with a higher-deductible option.

| Renter Profile | Personal Property | Liability Coverage | Deductible | Estimated Monthly Premium |

|---|---|---|---|---|

| Student renter | Lower coverage need | Standard liability | Higher deductible | Around the lower end of typical averages |

| Young professional | Moderate coverage need | Standard or somewhat higher liability | Mid-range deductible | Around the national average or somewhat above it |

| Small family renter | Higher coverage need | Higher liability | Lower deductible | Often above the national average |

The point of these examples isn't to pin an exact dollar amount to your life. It's to show the pattern. More belongings usually means more property coverage. More liability protection can raise the premium. A lower deductible often raises the monthly bill, while a higher deductible can lower it.

If your situation is unusual, such as prior claims, underwriting issues, or a tougher rental profile, it helps to review options built for renters insurance for high-risk tenants.

A lot of renters make one of two mistakes here. They either buy too little because they think “I don't own much,” or they overinsure because they never stopped to estimate what they own. A quick home inventory, even a simple phone note by room, usually brings more clarity than guessing.

The 4 Key Levers That Determine Your Premium

If you want to control your renters insurance cost, focus on the levers that move the quote. Four matter most.

Personal property coverage

This is the cap for replacing your belongings after a covered loss. The more value you insure, the more the policy may cost.

People often guess wrong here. They think only about big-ticket items like a television or laptop and forget the pile-up effect of everyday things. Clothes, shoes, cookware, bedding, furniture, small electronics, and household basics add up fast.

A good approach is to estimate by category, not by memory. Walk room to room and write down what you'd have to replace if everything vanished tomorrow.

- Bedroom items: Bed, mattress, dresser, linens, clothing, shoes

- Living area items: Couch, chairs, tables, lamps, television

- Kitchen and bath items: Dishes, cookware, small appliances, towels

- Portable items: Phone, laptop, headphones, bags

Liability limits

This part of the policy protects you if someone gets hurt or if you accidentally cause damage that leads to a claim against you.

Renters sometimes overlook liability because it isn't as visible as a stolen laptop or damaged furniture. But liability can be the part of the policy that saves you from a much bigger financial problem. If a guest is hurt in your rental or you accidentally cause damage that affects another unit, that protection matters.

The choice here is less about replacing things and more about protecting your finances.

A steady rule of thumb: Don't choose a liability limit just because it makes the quote look smaller. Choose one that fits the level of financial risk you could reasonably face.

Deductible choices

Your deductible is the amount you pay out of pocket before insurance starts paying on a covered claim. This is one of the clearest price levers you control.

Usually, a higher deductible lowers your monthly premium, while a lower deductible raises it. That sounds simple, but the smart decision depends on your emergency savings.

If you raise the deductible to cut the monthly bill, make sure the number still feels manageable on a bad day. Saving a little each month doesn't help much if you'd struggle to cover the deductible after a fire or theft claim.

A practical way to decide is to ask yourself one question: “If I had a covered loss next month, could I comfortably pay this amount without going into panic mode?”

Credit and claims history

This is the lever many renters don't expect, because it doesn't feel directly connected to the apartment or their belongings. But it can affect pricing in a meaningful way.

A NerdWallet analysis for New York found that renters with poor credit pay about $185 per year, compared with a statewide average of $125 per year (NerdWallet New York renters insurance analysis). That shows how personal rating factors can push the cost well above a headline average.

Claims history can matter too, though the exact effect will vary by insurer and situation.

Here's the control breakdown:

- Mostly in your control: Coverage amount, deductible, how carefully you review your quote

- Partly in your control: Credit profile over time, claim behavior

- Mostly outside your control: State, ZIP code, building risk, local claim trends

That split is what makes renters insurance feel less mysterious. Not everything is adjustable, but enough of it is.

4 Proven Strategies to Lower Your Renters Insurance Bill

A lower premium usually comes from adjusting the right levers, not from stripping the policy down until it barely helps. Renters insurance works a lot like a phone plan. You want to cut extras you do not need, while keeping the parts you would regret losing the moment something goes wrong.

Start with the factors you can control. Your deductible, your personal property limit, and whether you bundle policies are usually the biggest places to adjust price. Your ZIP code and local claim trends still affect the quote, but those are not knobs you can turn. Focusing on the parts you can change keeps the decision simpler.

Here are four practical ways to lower your bill without leaving yourself exposed:

Bundle if you already have another policy. If you have auto insurance or another personal policy, ask whether putting them with the same insurer reduces the total cost. This is often one of the easiest discounts because it does not require lowering your protection.

Raise your deductible only to a number you could actually pay. A higher deductible often lowers the monthly bill. The tradeoff is simple. You keep more money each month, but you take on more of the cost if you file a claim. If $1,000 would be hard to cover after a theft or fire, choosing that deductible could create more stress than savings.

Ask which safety features qualify for discounts. Deadbolts, smoke detectors, fire extinguishers, burglar alarms, and gated access can help in some cases. The savings may be modest, but this is an easy question to ask because the answer can lower your premium without changing your coverage.

Compare quotes using the same settings. This is where many first-time renters get tripped up. One quote may look cheaper only because it has a higher deductible or lower property limit. Line up the same personal property amount, liability coverage, and deductible before deciding which policy is actually the better value.

Be especially careful about cutting personal property coverage too far. That choice can make a cheap policy feel expensive later. If your clothes, laptop, furniture, and kitchen basics had to be replaced after a covered loss, the limit should be high enough to make that possible without putting you in a financial hole.

It also helps to review your policy once a year. If you moved, bought new electronics, sold expensive items, or picked up a roommate, the policy you chose last year may no longer fit your life now.

If comparing policies feels confusing, an independent insurance agency can help you review options across multiple carriers.

Get a Fast and Free Renters Insurance Quote Today

A monthly renters insurance price can shift for two simple reasons. Some parts of the price are in your hands, and some are set by where you live and how the insurer views that risk.

That is why getting your own quote matters so much. A national average is like a store sign that says "prices start here." It gives you a rough idea, but it does not tell you what your cart will cost once your choices are added.

A good quote process should feel straightforward. You enter your address, share a few details about the rental, estimate what you own, and choose the deductible and liability limits that fit your budget. Then you can see which parts of the premium come from your decisions and which parts come from things you cannot change, such as location.

If this is your first renters policy, focus on four practical steps:

- Estimate your belongings with care. A quick room-by-room list usually works better than a guess.

- Pick a deductible you could pay out of pocket. Lower premiums only help if the deductible is manageable after a claim.

- Keep liability coverage in the conversation. It protects you from costs that can be much larger than the value of your stuff.

- Review quotes line by line. The cheapest monthly number is only a good value if the coverage settings match.

That approach gives you a real answer to "how much is renters insurance monthly." Your quote should reflect your apartment, your belongings, and the coverage choices you control.

If you want help reviewing a personalized renters insurance quote, Select Insurance Group, Inc. can walk you through your options and explain how your location, property limits, and deductible affect the monthly premium.