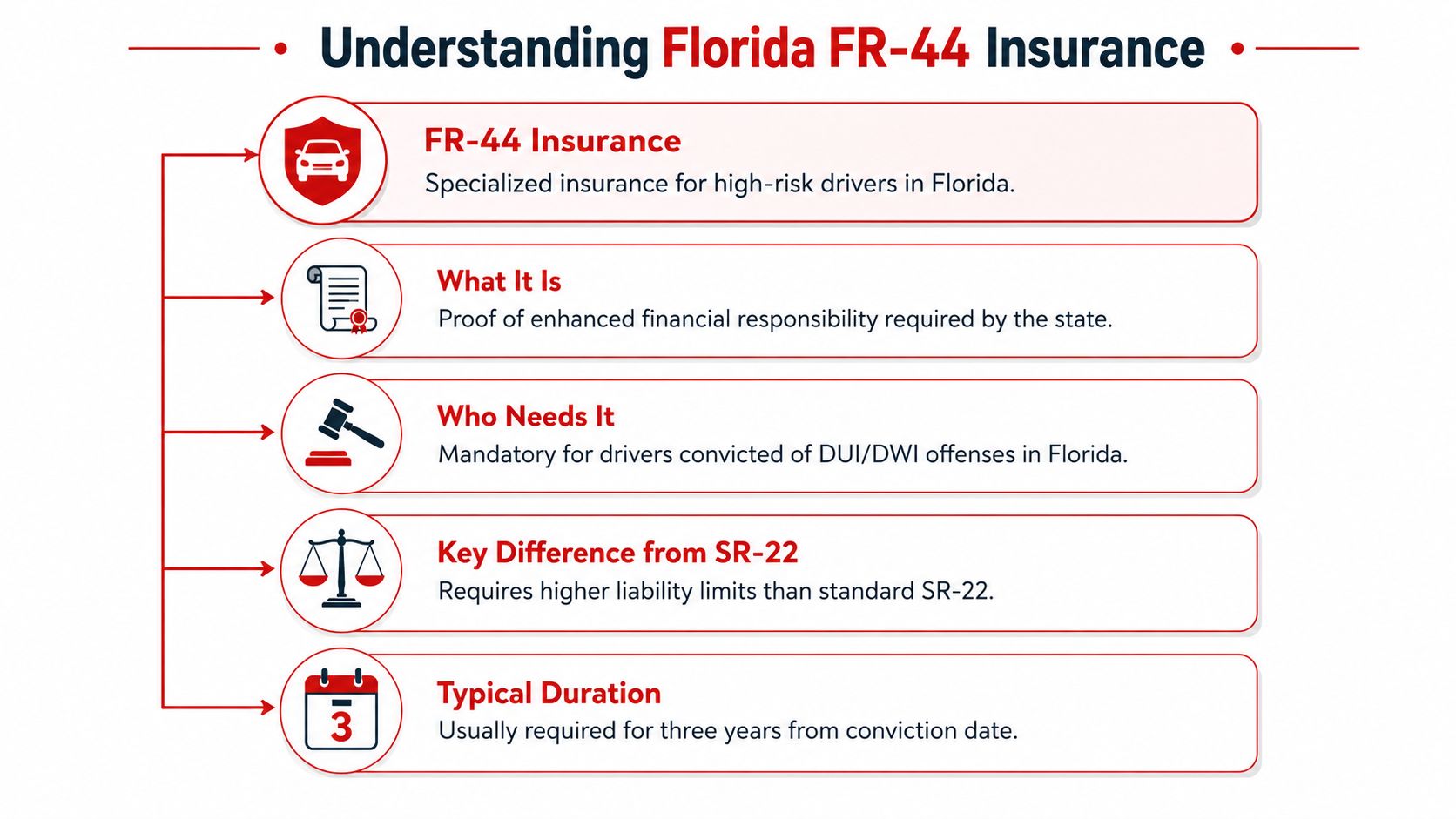

An FR-44 isn't insurance itself. It's a certificate proving you carry Florida's required 100/300/50 liability limits after a DUI, and you'll usually need to keep that coverage in place for three years. The filing fee is small, but the premium increase usually isn't, so the main challenge is finding a carrier that will still write the policy at a price you can manage.

If you're reading this, you're probably dealing with the part no one warns you about. The court side may be moving one way, the license reinstatement side another, and then an insurer tells you they won't file the form or they quote a price that feels impossible. That's common.

Most guides stop at definitions. What drivers need is a way to get compliant without wasting days calling companies that don't write this kind of business anymore. In Florida's tighter insurance market, availability matters almost as much as price. The right move isn't just “buy FR-44 insurance.” It's knowing what the state requires, which carriers still participate, how to avoid a lapse, and how to compare the quotes that are realistic.

Table of Contents

- What Is Florida FR-44 Insurance Actually

- Understanding FR-44 vs SR-22 in Florida

- The Real Cost of FR-44 Insurance After a DUI

- How to Get and File Your FR-44 Certificate

- Common Pitfalls to Avoid with Your FR-44

- Your Next Steps with Select Insurance Group

What Is Florida FR-44 Insurance Actually

The term throws people off because it sounds like a special insurance product. It isn't. FR-44 is a filing, and your insurance company sends it to the state to prove you're carrying the liability coverage required after a DUI.

Think of it as a financial responsibility report card for the DMV. The state isn't asking whether you bought “FR-44 insurance” as a separate policy. It's asking your insurer to certify that your policy meets the higher standard tied to your license reinstatement.

Think of FR-44 as a report card for the state

Florida created the FR-44 requirement by statute for DUI-related cases, and it took effect on February 15, 2008. It applies to drivers convicted of DUI after that date under the cited guidance. The filing proves you carry $100,000 bodily injury per person, $300,000 bodily injury per accident, and $50,000 property damage per accident, often shortened to 100/300/50. That summary comes from Bankrate's explanation of Florida FR-44 rules.

If you're still sorting out the basic terminology, this primer can help you understand FR-44 auto insurance before you start quote shopping.

Practical rule: If the state requires FR-44, the filing only works if the underlying policy already carries the correct liability limits.

What 10030050 means in plain English

Those numbers matter because they define how much liability protection your policy must carry.

- $100,000 bodily injury per person: This is the maximum available for injuries to one person if you cause an accident.

- $300,000 bodily injury per accident: This is the total available for all injured people in one accident.

- $50,000 property damage per accident: This applies to damage you cause to vehicles, structures, or other property.

That's why this filing changes your insurance so much. You're not just adding paperwork. You're moving into a much higher-liability policy requirement than many Florida drivers carry under ordinary minimum standards.

From a practical standpoint, the takeaway is simple. If an insurer says they can “file the FR-44,” that only helps if they're also willing to issue a policy with those limits and keep that filing active with the state.

Understanding FR-44 vs SR-22 in Florida

A lot of bad advice starts here. People hear “proof of insurance filing” and assume FR-44 and SR-22 are basically the same. In Florida, they're not.

The difference that matters

An FR-44 is the filing Florida uses for DUI-related cases. An SR-22 is generally associated with other serious driving issues, not the DUI filing discussed here. If your reinstatement paperwork says FR-44, an SR-22 won't satisfy it.

That distinction matters because people sometimes call around asking for the wrong thing. Once that happens, they get quotes that look cheaper, but they're for the wrong filing or the wrong liability structure. That wastes time and can delay reinstatement.

If you don't own a vehicle and you're trying to understand how filings can work in a non-owner situation, this guide on getting SR22 insurance without a car helps clarify the general filing concept.

FR-44 vs SR-22 in Florida at a Glance

| Attribute | FR-44 (The "DUI Insurance" Filing) | SR-22 (For Other Violations) |

|---|---|---|

| Primary trigger | DUI-related cases in Florida | Other qualifying violations or suspensions |

| Liability requirement | 100/300/50 | Lower than FR-44 in Florida |

| Cost impact | Usually higher because required limits are much higher | Usually lower than FR-44 |

| Practical shopping issue | Fewer willing carriers in some cases | Often easier to place than FR-44 |

| State purpose | Proves enhanced financial responsibility after DUI | Proves financial responsibility for other cases |

The filing names may sound similar, but using the wrong one won't fix your license problem. Match the filing to the exact reinstatement requirement.

The cleanest way to handle this is to read your paperwork carefully and use the state's exact wording when you request quotes. “I need an FR-44 filing in Florida” is very different from “I need high-risk insurance.” Precision saves time.

The Real Cost of FR-44 Insurance After a DUI

You usually feel the cost before you understand the rule. A driver gets the license issue sorted out, starts shopping, and then sees quotes that are far above what they paid before. That sticker shock is common with FR-44.

According to this Florida FR-44 cost overview, the FR-44 usually must be maintained for three years after reinstatement. Premiums often rise sharply after a DUI, while the filing fee itself is typically only about $15 to $25. In practice, the expensive part is the policy required to support the filing, not the filing form.

Why premiums increase so much

A DUI changes the account in more than one way. The insurer is pricing a higher-risk driver, and Florida also requires much higher liability limits for FR-44 than many drivers carried before. On top of that, some carriers are less willing to write this business at all, which matters if you are trying to find something both available and affordable.

That last point gets overlooked. In a tighter market, fewer willing carriers usually means fewer workable quotes, stricter payment terms, and less room for error if your budget is already stretched.

If you want added context on how pricing behaves statewide, this guide to Florida car insurance rates helps explain why FR-44 quotes can vary so much from one carrier to another.

Build your budget around the policy, not just the filing

The practical budget has three parts:

- The premium itself: This is usually the largest expense by far.

- The filing charge: Small, but still part of getting the policy issued correctly.

- The payment structure: Some carriers handling FR-44 business may require more money upfront or tighter billing terms than you are used to.

That third item matters more than many drivers expect.

A lower monthly number is not automatically the safer choice if the company requires a large down payment or uses billing terms that make a missed payment more likely. If the policy cancels, your filing can fall off with it, and that can create a new license problem fast. Affordable coverage is coverage you can keep in force for the full requirement period.

If you are also lining up the license side while budgeting for insurance, this article offers expert advice on Florida license reinstatement and can help you understand the timing.

How to Get and File Your FR-44 Certificate

The mechanics matter here. A driver can do everything right in court and still get stuck because the insurance side wasn't handled in the right order.

The hardest part today often isn't the filing form. It's finding a carrier that still wants this business. Public guidance points out that not every insurer files FR-44s, and that tightening underwriting can make these policies harder to obtain. That same overview notes that Florida FR-44 pricing can range from $162 to $318 per month, which is why quote comparison matters so much in practice. Those details are summarized in Insurify's Florida filing overview.

If you're also dealing with the license side of the problem, this article offers expert advice on Florida license reinstatement and can help you line up the paperwork sequence.

The fastest path is usually the least complicated one

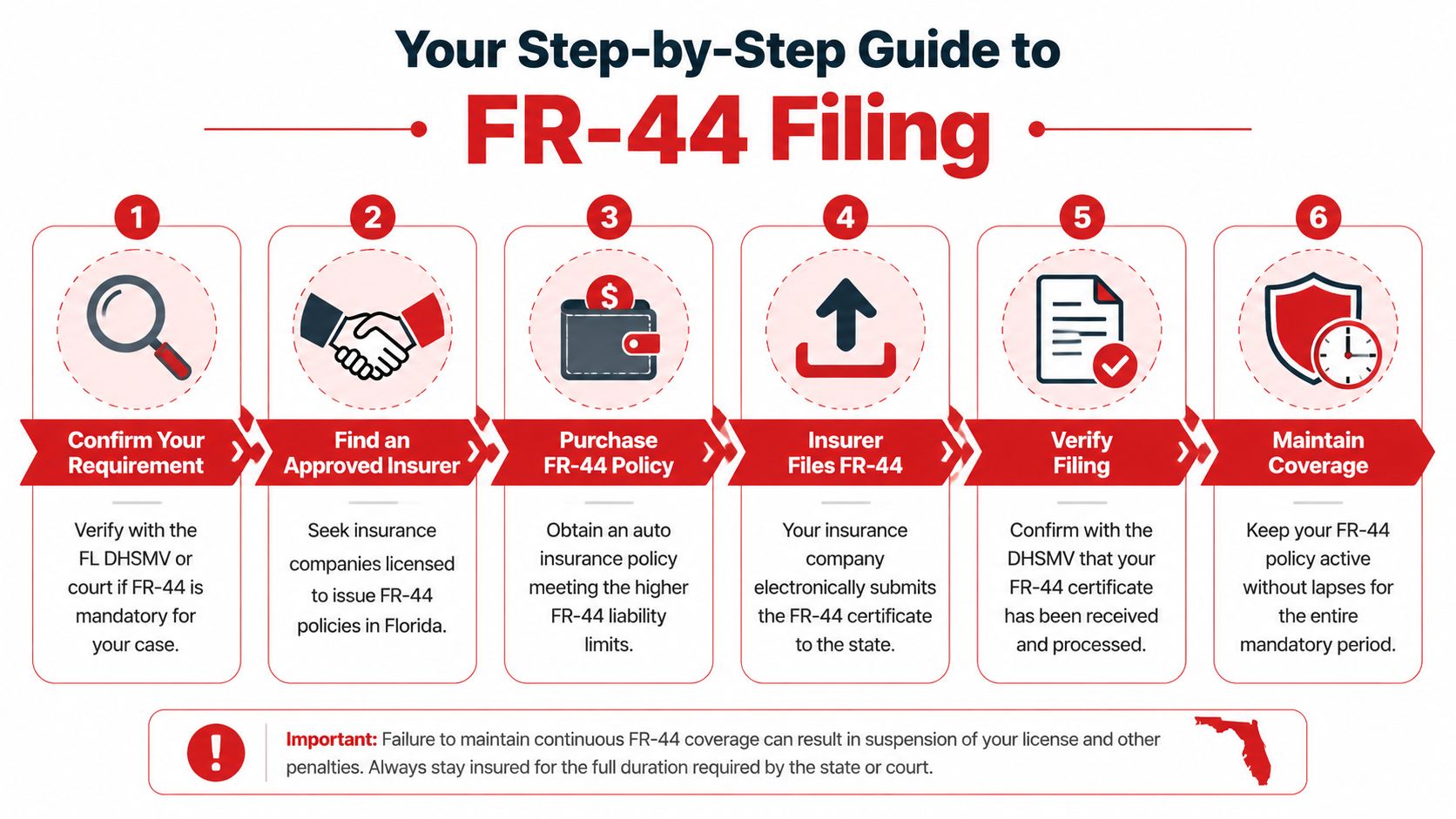

In practice, the cleanest route looks like this:

- Confirm exactly what the state requires. Check your notice, court paperwork, or DHSMV instructions. Don't guess between FR-44 and SR-22.

- Ask upfront whether the insurer files FR-44 in Florida. Don't spend time discussing optional coverages first.

- Verify the policy limits before payment. The filing only works if the liability limits meet the state requirement.

- Make sure the insurer submits the filing. Buying the policy alone doesn't complete the process.

- Confirm that the filing was received. Administrative delays happen. Verification matters.

That order avoids the most common delay, which is assuming coverage and filing are the same event. They're connected, but they aren't identical.

A practical filing checklist

Use this checklist before you pay anything:

- Requirement match: The carrier confirms this is an FR-44 filing for Florida, not another filing type.

- Correct limits: The policy shows the required liability limits before the filing is sent.

- Named driver details: Your license information and personal details are accurate. Small errors can slow processing.

- Payment plan clarity: You know whether the insurer expects a down payment, full payment, or tighter billing terms.

- Proof path: You know how you'll confirm the filing reached the state.

If an insurer sounds unsure about FR-44 procedure, keep shopping. With this filing, uncertainty usually turns into delay.

What works is simple and not glamorous. Use a carrier or agency that handles these filings regularly, verify the limits, confirm the filing, and keep records of every step.

Common Pitfalls to Avoid with Your FR-44

A lot of drivers get the policy in place, make the first payment, and assume the hard part is over. In practice, the bigger risk is keeping the FR-44 active month after month in a market where some carriers are selective, billing terms can be strict, and one preventable mistake can put your license status back in trouble.

The lapse problem is the one I warn people about first. If your policy cancels for missed payment, bad card information, or a failed renewal, the state filing can fall with it. By the time you plan to fix it, you may already be dealing with a new suspension issue and another round of reinstatement headaches.

The expensive mistakes usually look ordinary at first:

- Treating FR-44 like standard auto insurance: Standard shopping habits can fail here. A cheap quote does not help if the carrier will not keep the filing in force under your payment setup.

- Choosing the lowest monthly number without reading the billing terms: Some policies look affordable until you see the down payment, installment fees, or short grace period.

- Waiting too long to replace a declining or non-renewing policy: Availability is tighter than many drivers expect. If one carrier backs away, you need time to find another that will accept the risk and file correctly.

- Changing vehicles or addresses without checking the policy impact: Routine updates can create problems if they are handled carelessly or if underwriting changes the policy.

- Ignoring mail, email, or text notices from the insurer: Cancellation warnings often arrive before actual damage happens. Missing those notices is avoidable.

Here is the trade-off that matters. The lowest price is not always the best FR-44 option. A policy that costs a little more but has billing terms you can realistically maintain is often the safer choice.

That is why I tell clients to judge affordability by durability. Can you keep this policy active for the full filing period without scrambling every due date? If the answer is no, keep shopping.

A few habits make a real difference:

- Put every payment on a calendar with early reminders. Give yourself time to fix a card issue or bank transfer problem before the due date.

- Save proof of everything. Keep your declarations page, ID cards, filing confirmation, receipts, and any state notices in one folder.

- Call before making changes. New car, new address, driver change, or policy rewrite. Ask how it affects the filing before you approve it.

- Ask direct retention questions. “What happens if my payment is one day late?” is more useful than a broad question about customer service.

- Get help from an agency that can check more than one market. If your current option is too expensive or unavailable, start with a Florida car insurance quote for FR-44 needs and compare workable choices.

The goal is simple. Keep the policy active, keep the filing attached, and avoid gaps. That is how you protect your license and avoid paying more to clean up a problem that started with one missed detail.

Your Next Steps with Select Insurance Group

Finding Florida FR44 insurance for DUI convictions takes more than a generic online quote form. You need carriers that are still willing to write the policy, guidance on the filing itself, and a process that reduces the chance of a costly mistake.

Why this process goes smoother with the right agency

Select Insurance Group, Inc. is an independent agency with access to 20 to 40 carriers, which matters when market availability is tight. Instead of relying on a single company's appetite for high-risk business, you can compare multiple options in one place.

The agency also brings over 30 years of experience, bilingual support, and local service in the Orlando to Tampa metro area and beyond. For FR-44 shoppers, that combination matters because this isn't just a pricing exercise. It's a compliance exercise with real consequences if the filing or payment setup goes wrong.

What to do now

If you need to get moving, keep the process simple:

- Gather your paperwork: License information, vehicle details, and any state or court notice tied to reinstatement.

- Request quotes from multiple carriers: Independent access proves helpful here.

- Review payment terms carefully: Don't focus only on the lowest starting number.

- Confirm the filing process: Make sure the agency or insurer explains how the FR-44 gets submitted and how you'll know it was accepted.

You can start by requesting a Florida car insurance quote today and comparing realistic options based on your situation.

If you need help with Select Insurance Group, Inc., the fastest next step is to reach out for a quote review and filing guidance. Their team can compare multiple carriers, explain your options in plain English or Spanish, and help you find a Florida FR-44 policy you can keep in force.