The envelope shows up, or the email lands, and everything narrows fast. Your license is suspended. You're not sure whether you're supposed to stop driving immediately, call the DMV, call your insurer, or do both before the end of the day. If you don't own a car, the confusion gets worse. Why would you pay for auto insurance when you legally can't drive?

That question is usually where the panic starts. It's also where bad decisions happen. Drivers cancel coverage to save money, assume they can “fix it later,” or buy the wrong policy because someone told them they “just need an SR-22” without explaining what that means.

The practical answer is this: in many cases, you're not paying for the right to drive right now. You're paying to satisfy a legal requirement, protect your path to reinstatement, and avoid making an already expensive problem harder to fix. If you're also dealing with a related charge, it can help to review Miles Hansford Law defense strategies so you understand the legal side as clearly as the insurance side.

Table of Contents

- Your Guide Through License Suspension

- Why You Still Need Insurance Without Driving Privileges

- Decoding Your Three Main Insurance Options

- State-Specific Reinstatement Rules and Filings

- What to Expect for Costs and Surcharges

- Your Step-by-Step Guide to Getting Back on the Road

- How Select Insurance Group Makes This Process Easier

Your Guide Through License Suspension

A suspension notice rarely arrives at a convenient time. Most drivers are already juggling work, family, court paperwork, or a recent lapse in coverage when they find out their license status changed. Then the insurance questions pile up all at once.

The hardest part is that the words on the notice often don't answer the actual question you need answered. They tell you what happened. They don't tell you what to buy, what to file, whether you should keep insurance on a car you own, or what to do if you don't own one at all.

You can usually solve this faster once you separate the problem into two tracks: the legal reason for the suspension, and the insurance proof needed to clear it.

That distinction matters. A suspended license creates two different issues that people often blend together. One is whether you're allowed to drive today. The other is what the state wants to see before it will restore your driving privileges later.

A practical path usually looks like this:

- Read the notice closely: Find the reason for suspension, any compliance deadline, and whether the state mentions a filing such as SR-22 or FR-44.

- Check whether you own a vehicle: That single fact changes the insurance structure more than most drivers expect.

- Avoid unnecessary cancellations: Dropping a policy without understanding the filing requirement can create a second problem.

- Solve the paperwork in order: The right filing attached to the wrong policy, or the right policy without the filing, still leaves you stuck.

Drivers looking for auto insurance for drivers with suspended licenses usually don't need more jargon. They need a calm process. That starts with understanding that insurance in this situation is often about compliance first, driving second.

Why You Still Need Insurance Without Driving Privileges

If your license is suspended, your first reaction may be simple. Stop driving, cancel coverage, wait it out. In many cases, that backfires.

A suspended license doesn't automatically prevent you from obtaining auto insurance, but many standard insurers will decline a new policy. Insurers often require an SR-22, which is a financial-responsibility filing confirming the policy meets state minimums, and common compliance periods are 3 to 5 years depending on the violation and state, as explained in Progressive's overview of insurance with a suspended license.

Insurance and legal compliance are not the same thing

Many drivers often get confused. Insurance usually makes people think about crashes, repairs, and liability on the road. During a suspension, the more urgent issue is often financial responsibility.

Think of an SR-22 as a DMV compliance signal. It isn't the insurance policy itself. It's the filing your insurer sends to show the state that you carry the required liability coverage. You may not be driving, but the state may still require that proof to keep your reinstatement path open.

Practical rule: If your notice or reinstatement requirements call for an SR-22 or FR-44, paying for that policy is often what keeps your case moving forward. It is not wasted money just because you're off the road temporarily.

What you're actually paying for

For many suspended drivers, the payment covers one or more of these needs:

- DMV compliance: The state wants proof that you carry required liability coverage.

- Future reinstatement: You may need active coverage on file before your license can be restored.

- Vehicle protection structure: If you own a car, it may still need the right policy setup even if someone else is the primary driver.

- Gap prevention: A lapse can create fresh underwriting problems when you try to come back.

That's especially important if you're still sorting out fault or legal exposure from an accident. For a plain-language explanation of how uninsured claims issues can unfold, even when fault is disputed, the guidance from Pacin Levine, P.A. is useful background.

The key question to ask

Don't ask only, “Can I drive with this policy?” Ask, “Does this policy satisfy the state requirement tied to my suspension?”

Those are different questions. The right answer depends on whether you own a car, whether your state requires an SR-22 or FR-44, and whether another licensed household member needs to remain insured on the vehicle.

Decoding Your Three Main Insurance Options

Most suspended drivers aren't choosing from dozens of realistic paths. In practice, there are three main insurance setups, and each solves a different problem.

SR-22 and FR-44 filings

An SR-22 or FR-44 is not a standalone policy. It's a filing attached to an insurance policy. The state requires it when it wants formal proof that the driver carries at least the required liability coverage.

Who is this for? Drivers whose suspension or violation triggered a filing requirement.

What problem does it solve? It gives the DMV documented proof of financial responsibility.

What it does not do by itself: It does not insure a car. It does not automatically reinstate your license. It does not mean you're allowed to drive before the state clears you.

That last point matters. Drivers often say, “I bought the SR-22.” What they usually mean is that they bought a policy and paid for the insurer to file the form. That may be exactly what they need, but only if the policy type underneath it is correct.

Non-owner coverage for drivers without a car

This is the most misunderstood option, and for many people it's the right one.

If you don't own a car, but your state requires proof of liability coverage tied to reinstatement, a non-owner policy may be the practical fit. It can sometimes be paired with the required filing so the state sees continuous liability evidence without you insuring a vehicle you don't own.

A major blind spot in most discussions is the driver who needs compliance but has no vehicle. State rules and insurer underwriting can diverge, and in Georgia, a lapse of insurance triggers a penalty and suspension notice, which makes non-owner coverage an important compliance tool in some situations, as noted by the Georgia Department of Revenue insurance lapse guidance.

If you want a plain-English breakdown of how this type of policy works in real life, this simple guide to non-owner car insurance helps clarify when it fits and when it doesn't.

If you don't own a car, the question isn't “Why would I insure a vehicle I don't have?” The question is “What policy format will the state and insurer accept as proof while I work toward reinstatement?”

Non-owner coverage is often useful when:

- You need a filing but own no vehicle

- You regularly borrow cars after reinstatement

- You want to avoid a compliance gap while off the road

It usually does not make sense if you have regular access to a household vehicle that should be insured under an owner policy, or if the car is titled to you.

High-risk owner policies

If you own a car and need insurance tied to that vehicle, you may need a high-risk auto policy. That's a standard auto policy in structure, but it's written for a driver profile that insurers consider more difficult to underwrite because of suspension history, serious violations, or prior lapses.

This option works best when:

- You own the vehicle

- You need liability attached to that vehicle

- A licensed household member drives the car

- Your state requires a filing and the vehicle still needs active coverage

Some insurers can also use variations such as excluded-driver arrangements or limited-use structures depending on the facts. The main point is to match the policy to the actual ownership and driving setup. A cheap policy that doesn't fit your legal or household situation can create claim problems later.

State-Specific Reinstatement Rules and Filings

State rules are where suspended-license cases stop being theoretical. The filing type, how long it has to stay on file, and what reinstatement costs look like all depend on where the suspension happened.

South Carolina provides one of the clearest examples of how administrative penalties work. The state requires an SR-22 for three years from the date of suspension, and if insurance verification is not received within 20 business days after a lapse notice, a driver's privilege, plate, and registration can be suspended. Reinstatement can cost up to $400. Pennsylvania also lists a $94 driver's-license restoration fee along with other penalties, according to the South Carolina DMV uninsured driving facts page.

For drivers trying to sort out filings without owning a vehicle, this guide to getting SR22 insurance without a car can help frame the insurance side correctly.

If your case is in Georgia and you're also trying to understand the licensing process from the state side, this resource on how to navigate Georgia license reinstatement is a helpful companion to the insurance conversation.

State SR-22 and reinstatement requirements 2026

| State | Filing Type | Required For | Typical Filing Period | Estimated Reinstatement Fee |

|---|---|---|---|---|

| Alabama | Varies by case | Check state notice or court order | Varies by case | Varies by case |

| Florida | Often case-specific, sometimes FR-44 or SR-22 depending on offense | Check state notice or court order | Varies by case | Varies by case |

| Georgia | Often SR-22 in applicable cases | Check state notice or DMV notice | Varies by case | State penalties can apply after lapse |

| North Carolina | Varies by case | Check state notice or court order | Varies by case | Varies by case |

| South Carolina | SR-22 | Suspension and uninsured-driving related compliance | 3 years | Up to $400 |

| Tennessee | Varies by case | Check state notice or court order | Varies by case | Varies by case |

| Virginia | SR-22 or FR-44 depending on violation | Serious violations and financial-responsibility cases | Varies by case | Varies by case |

Alabama

For Alabama drivers, the notice from the state or court is the document to trust first. Don't assume a friend's experience applies to your file. The cause of suspension often determines whether a filing is needed and how the policy should be written.

A common mistake is shopping for “cheap insurance” before confirming whether the state needs proof filed directly by the insurer.

Florida

Florida cases often create confusion because drivers may hear both SR-22 and FR-44 discussed. The right filing depends on the violation. What matters operationally is not the label alone, but whether the policy underneath it meets the liability level required for that filing.

Georgia

Georgia drivers need to pay special attention to lapse issues. A loss of coverage can trigger penalties and suspension activity, so keeping the right policy active matters even when you're not currently driving.

North Carolina

North Carolina drivers should confirm whether the suspension is tied to insurance compliance, court action, or another administrative issue. Those details change what an agent should quote and what the state will accept.

South Carolina

South Carolina is one of the clearest reminders that this problem isn't only about premium price. It's also about preserving registration, tags, and your timeline for reinstatement.

Missing a compliance deadline can turn one suspension issue into several separate administrative problems.

Tennessee

Tennessee drivers should verify whether the suspension created a filing requirement or a reinstatement task after another issue is resolved. That difference affects whether you need a policy immediately or only after a specific court or DMV step.

Virginia

Virginia deserves special attention because the filing type can shift based on violation severity. Some drivers need an FR-44, which is treated differently in underwriting than an ordinary policy situation. That can affect both availability and price.

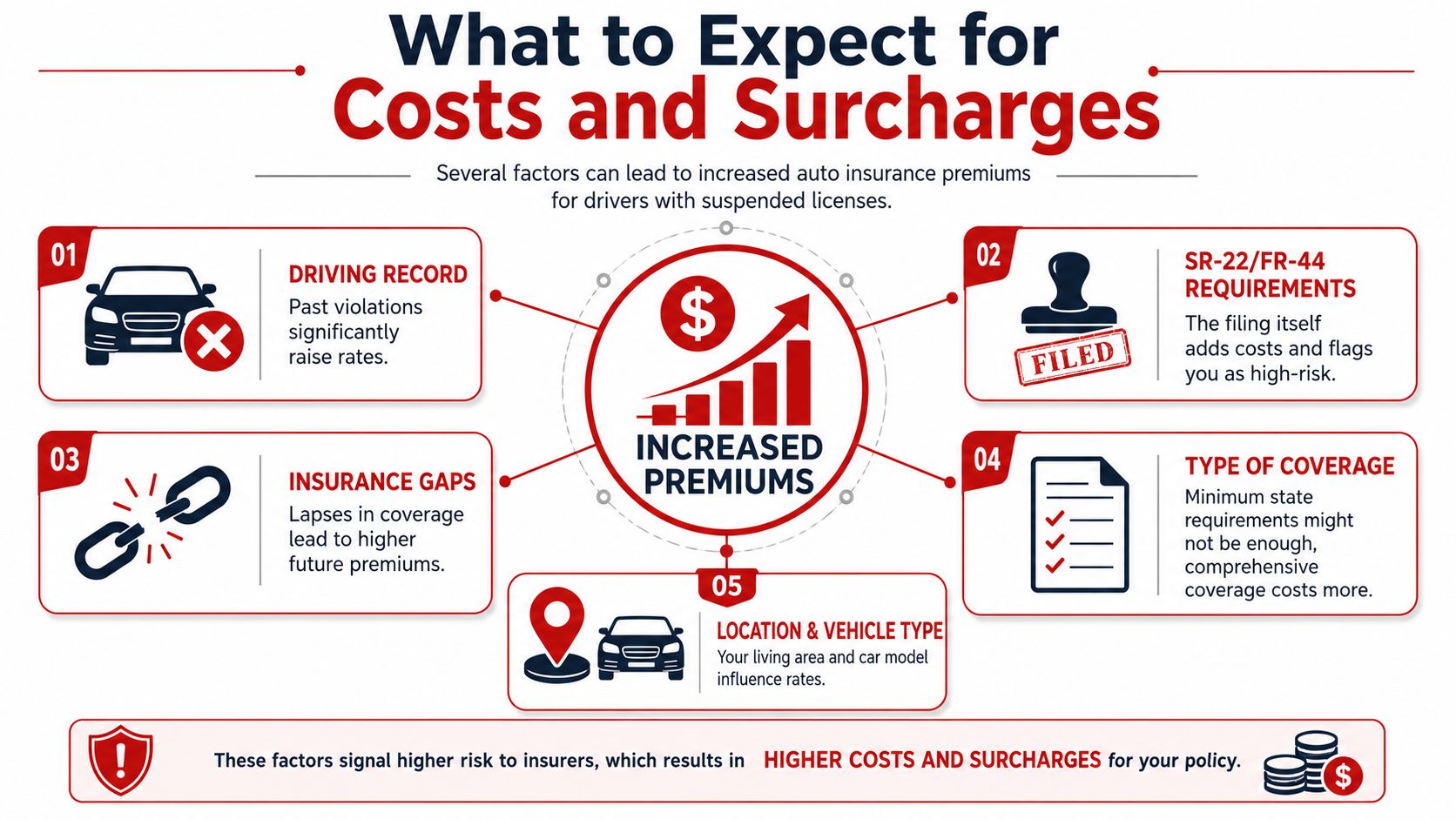

What to Expect for Costs and Surcharges

The price jump after a suspension feels personal, but from the insurer's side it's underwriting math. A suspended license tells the carrier that the file has compliance issues, violation history, or both. That pushes the policy out of the clean standard market and into a higher-risk category.

Why insurers charge more after a suspension

A Virginia-focused legal guide notes that insurers may raise premiums after suspension and that suspensions can remain on a driving record for several years. The same source reports that a minor moving violation can raise premiums by 13%, more serious violations requiring an FR-44 can double rates, and high-risk drivers may see increases of up to 90%, according to this Virginia suspension and insurance analysis.

Those increases don't happen because an insurer is charging for the suspension notice itself. They happen because the suspension often comes bundled with risk signals such as violations, uninsured periods, filing requirements, or a restricted underwriting profile.

What the price range can look like

Independent market data cited by Insurify shows that high-risk drivers with suspension-related history can face average full-coverage quotes in the $226 to $269+ per month range, as summarized in this suspended-license insurance cost review.

That figure is useful as a reality check, not a promise. Your actual quote depends on factors such as vehicle ownership, state filing requirements, coverage level, and whether there was a lapse.

A practical budgeting approach is:

- Plan for the filing requirement: The policy has to stay active for the full compliance period required in your case.

- Expect fewer standard-market options: Some insurers will not open a new file for a suspended driver.

- Treat lapses as expensive: Canceling too soon can cost more than keeping a basic compliant policy in place.

- Review how long violations affect pricing: This overview of how long traffic tickets affect insurance is useful when you're trying to estimate how long the pressure on rates may last.

Budget for compliance first, then optimize price. Drivers who reverse that order often end up buying the wrong policy twice.

Your Step-by-Step Guide to Getting Back on the Road

The fastest recoveries usually come from doing the boring steps in the right order. When drivers skip ahead, they often buy coverage that doesn't match the reinstatement requirement.

Start with the suspension notice

Read the notice line by line. You need four facts before you shop for anything:

Reason for suspension

A lapse, an uninsured-driving violation, a serious traffic offense, and a court-related suspension don't point to the same insurance solution.Whether the state requires a filing

If the notice mentions SR-22 or FR-44, write that down exactly.Who owns the vehicle

If the car is titled to you, that usually pushes you toward an owner policy structure. If you don't own a vehicle, the path may look very different.What must happen before reinstatement

Some drivers need more than insurance. They may also need to resolve fines, court obligations, or other administrative issues first.

Match the insurance to your actual situation

Once you know the requirement, get quotes for the policy type that fits your life, not the one someone casually recommended.

- If you own a car: Ask for an owner policy that can handle the required filing.

- If you don't own a car: Ask whether a non-owner policy is acceptable for your state requirement.

- If someone else drives your vehicle: Make sure the licensed driver arrangement is disclosed and properly rated.

- If you're unsure: Ask the agent to explain whether the policy is for active vehicle use, compliance filing, or both.

That distinction saves time. Many delays come from using the right filing on the wrong policy form.

Keep the policy active until the requirement ends

This part is where people sabotage their own reinstatement. They get the filing submitted, pay one month, then cancel after they think the state has “already seen it.”

Don't do that. Filing requirements are usually continuous. If the policy cancels, the insurer can notify the state, and you may be back in the same loop.

Use a simple checklist:

- Set autopay if possible

- Open every insurer notice

- Confirm the filing was accepted

- Don't replace the policy without coordinating the filing transfer

- Ask for proof of current coverage and filing status

If you're frustrated, that's normal. The process is repetitive, but it is manageable when each step matches the state requirement.

How Select Insurance Group Makes This Process Easier

Suspended-license insurance is difficult for one reason more than any other. The policy you need has to satisfy both underwriting rules and state compliance rules at the same time. That's where many drivers get stuck.

An independent agency can help sort that out by checking whether you need an owner policy, a non-owner policy, or a filing attached to either one. In Select Insurance Group, Inc.’s case, the agency states that it compares quotes from 20 to 40 carriers and has over 30 years of experience serving drivers across multiple Southeastern states, according to the publisher information provided for this article.

What matters in practice is speed and accuracy. A suspended driver usually needs someone to answer a few specific questions clearly:

- Do I need a filing, and which one?

- Can I get coverage if I don't own a car?

- Will this policy satisfy the DMV requirement?

- What happens if I switch policies later?

Those aren't sales questions. They're process questions. When the answers are clear, the path forward gets much less stressful.

If you need a policy for a suspended license, a non-owner setup, or an SR-22-related filing, Select Insurance Group, Inc. can help you review the requirement, check available policy structures, and request a free, no-obligation quote so you can start the reinstatement process without guessing.