A lot of Lake Norman owners are in the same spot right now. The boat is fueled, the kids want to tube, somebody brought a wakeboard, and there's already a plan to tie up for lunch at a crowded restaurant dock. Most days, that's exactly what boating here should be.

The trouble starts when a normal lake day turns sideways in one fast moment. A guest falls hard on a wakeboard run. Your bow swings a little too wide near the dock and catches another boat. A summer storm rolls in while your boat is still in the slip. Or a stranger clips your PWC and then you learn they don't have usable coverage.

That's why Boat and PWC insurance Lake Norman NC isn't something to treat like an afterthought. A standard homeowners policy usually doesn't cover watercraft losses beyond very small, low-powered craft, and that leaves real gaps for people who spend time on a busy lake. The risk isn't theoretical either. Recreational boating incidents still produce hundreds of fatalities and thousands of injuries annually, and alcohol remains a leading factor, as noted by H Cutt Insurance's overview of boat insurance gaps.

Your Guide to Worry-Free Boating on Lake Norman

A good Lake Norman policy should match the way people use the lake. That means more than “coverage for the boat.” It means thinking through the moments that trigger claims here: docking in tight spaces, towing a rider, leaving gear on board overnight, or dealing with another boater who causes damage and can't pay for it.

Why generic advice misses the real problems

Most online guides talk in broad terms. They'll mention collision, theft, and liability, then stop there. That's not enough for Lake Norman, where one Saturday can include open-water cruising, pulling a wakeboarder, docking at a marina, and trailering home after dark.

Three practical questions matter more:

- Who gets paid if your guest is hurt: Not just in a major crash, but after a towing incident or a hard fall during normal recreation.

- What happens if another boater causes the damage: Especially if they're uninsured, underinsured, or disappear into weekend traffic.

- Where the loss happens: At the dock, on the trailer, in storage, or on the water.

Practical rule: If your policy only makes sense while the boat is moving in open water, it probably has gaps.

The local mindset that works

Owners who have the fewest surprises usually treat insurance like part of the boating setup, the same way they treat maintenance, registration, and safety gear. They don't buy a policy just to satisfy paperwork. They buy one that fits how they launch, store, tow, dock, and entertain.

That approach matters more on Lake Norman because the exposure changes by the hour. Calm morning cruise. Midday congestion. Afternoon storms. Evening docking when everyone is tired and in a hurry.

When people ask what works, the answer is simple. Buy coverage for the day you hope not to have, not the day you planned.

Is Boat Insurance Required in North Carolina?

The legal answer is straightforward. North Carolina doesn't require boat insurance for registration. The practical answer on Lake Norman is different.

This lake is a major boating hub. It's described as North Carolina's largest man-made lake with over 520 miles of shoreline, and that scale matters because more shoreline means more ramps, more docks, more marinas, and more chances for property damage and liability claims, according to On The Water Marine's North Carolina boat insurance guide.

Where insurance becomes a real requirement

A lot of owners hear “not required by the state” and assume insurance is optional. That usually falls apart the moment they try to use the boat the way most active owners do.

Actual gatekeepers are private parties:

- Marinas: Slip agreements and storage arrangements often require proof of coverage before they'll let you in.

- Lenders: If the boat or PWC is financed, the lender usually wants the asset insured.

- Yacht clubs and organized facilities: If you want access, they often want proof of insurance first.

That's why, in day-to-day Lake Norman boating, insurance works like a de facto requirement even when the state doesn't demand it for registration.

Optional on paper, necessary in practice

People get tripped up at this point. They compare boat insurance to something discretionary, like adding a cosmetic upgrade. It's closer to keeping a trailer roadworthy. You might technically own it without doing certain things, but your real-world use gets limited fast.

A boat without workable insurance is hard to finance, hard to berth, and harder to recover from after a claim.

There's another practical point. On a smaller, lightly used body of water, some owners can get away with bare-minimum thinking for a while. Lake Norman isn't that kind of environment. The lake's size and activity level create more interaction with docks, marina staff, other boaters, rented spaces, and service providers.

Who can gamble and who really can't

If you keep an older, low-value boat on private property and only use it occasionally, you may feel comfortable carrying less protection. That's a personal choice.

But if any of these apply, insurance stops being optional in any meaningful sense:

| Situation | Why coverage matters |

|---|---|

| Financed boat or PWC | The lender usually wants proof of insurance |

| Marina slip or dry storage | The facility may require liability and physical damage coverage |

| Frequent guest use | Passenger injury exposure goes up quickly |

| Towing skiers or wakeboarders | Liability exposure changes compared with simple cruising |

| Restaurant and marina docking | Close-quarters property damage becomes more likely |

The practical takeaway is simple. On Lake Norman, boat insurance isn't a luxury add-on. It's part of responsible ownership.

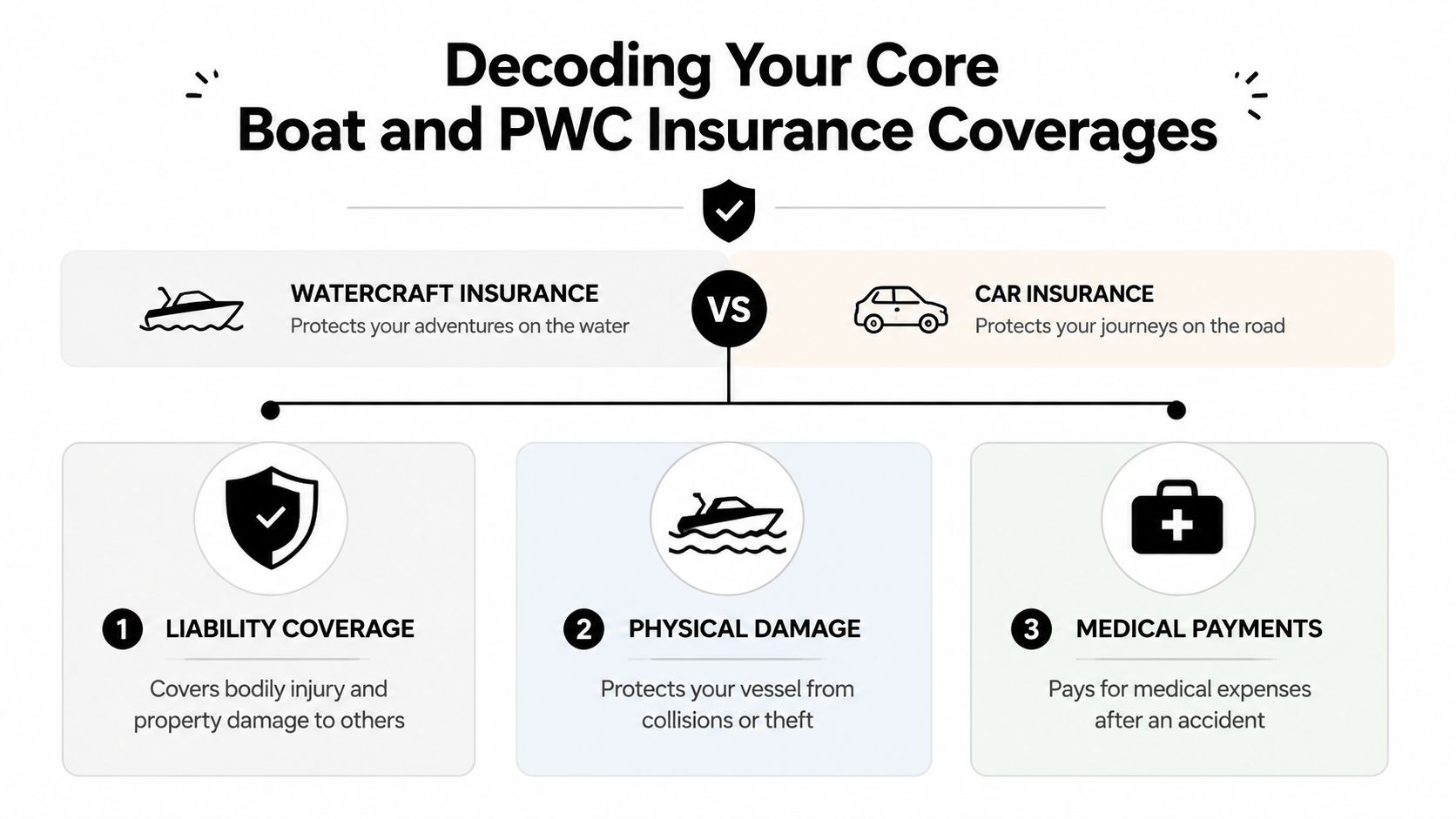

Decoding Your Core Boat and PWC Insurance Coverages

Most boat and PWC policies make more sense once you compare them to auto insurance. You're usually dealing with three main buckets: physical damage, liability, and medical payments. North Carolina's Department of Insurance frames boat policies around those same core pieces, and it notes that liability can cover damage to another craft, dock, or property, plus bodily injury or death caused by negligence, including injuries to towed skiers, in its North Carolina boat insurance consumer guidance.

Physical damage covers your boat or PWC

Think of this as the part that protects your machine. If the hull is damaged, the outboard is hit, the craft is stolen, or the trailer incident causes covered damage, this is the section people look to first.

On Lake Norman, physical damage claims often aren't dramatic movie-scene wrecks. They're more ordinary and more common:

- backing into a piling

- rubbing another boat during docking

- storm damage while moored

- vandalism or theft

- trailer damage during transport or storage

For PWC owners, this coverage matters because repairs can get expensive quickly even after what looks like a minor hit.

Liability pays when you harm someone else

This is the part many owners underbuy. They focus on the boat's value and forget that the largest loss might have nothing to do with the boat itself.

A few Lake Norman examples make the point:

- You misjudge a crowded restaurant dock and damage another owner's vessel.

- Your rider gets injured during a wakeboarding run and claims operator negligence.

- You hit a private dock, marina structure, or moored watercraft.

- A guest passenger gets hurt during a sudden maneuver.

If you want a quick comparison with land-based insurance, this breakdown of full coverage vs liability helps frame the same trade-off. Protecting your own property and protecting yourself from what you may owe others are two different jobs.

Don't choose liability limits based on what your boat is worth. Choose them based on the biggest injury or property-damage claim you could realistically cause.

Medical payments helps with immediate injury costs

Medical payments is often misunderstood. It's not the same thing as liability. It can help with covered medical expenses after an accident involving people on your boat, regardless of whether a lawsuit follows.

That can matter when a friend slips boarding the boat, a passenger is hurt during a sharp turn, or someone gets banged up during a towing activity. It doesn't solve every injury issue, but it can take some heat out of the first round of expenses.

What works better than buying “the cheapest policy”

The best setup is usually boring in a good way. Adequate liability. Solid physical damage terms. Medical payments that aren't an afterthought.

What doesn't work is buying the lowest-priced policy without checking how it handles:

- Guest passengers

- Wakeboarding or tubing

- Dock and marina incidents

- Trailer-related losses

- Proof-of-insurance requirements for storage or financing

A good policy should read like it was built for the way you boat, not for a fictional owner who cruises alone on an empty lake.

Essential Add-Ons for Your Lake Norman Policy

Core coverage gets you into the game. The add-ons decide whether a bad day becomes a manageable inconvenience or a drawn-out mess.

On Lake Norman, the most useful endorsements are the ones that solve common local headaches. Not flashy options. The practical ones.

On-water towing and assistance

This is one of the easiest coverages to appreciate after the fact. If your boat won't restart or your PWC leaves you stranded well away from your launch point, towing can turn from “annoying” to “expensive” fast.

People often assume roadside-style help is built in. Sometimes it is not. That's worth checking before you need it.

Best fit for:

- boats that run far from the launch area

- owners who anchor out or spend long days on the water

- PWC operators who ride away from familiar coves and docks

Uninsured or underinsured boater protection

This is one of the most overlooked parts of Boat and PWC insurance Lake Norman NC. It matters because not every person who hits you has usable coverage, enough coverage, or any interest in making your life easier.

A common scenario on busy lakes is straightforward. Someone damages your boat, injures a passenger, or causes a crash, and then you find out their insurance situation is weak or nonexistent. That's where this coverage earns its keep.

If you can picture a stranger ruining your weekend, you should picture their insurance being inadequate too.

Trailer coverage and off-water exposure

A lot of losses happen before the boat reaches the lake or after it leaves. Tires fail. A trailer gets clipped in a parking lot. Gear disappears while the boat is stored at home or at a marina. Owners who only think about on-water collisions miss a big slice of their real exposure.

This is especially important for people who tow often, store outside, or keep a PWC on a trailer for part of the year.

Personal effects and equipment

Some owners keep the boat fairly bare. Others carry fishing gear, electronics, safety equipment, coolers, anchors, and accessories that add up quickly after a theft or vandalism loss.

It's helpful to inventory items that remain on board. If replacing those items out of pocket would sting, ask how the policy handles personal effects and onboard equipment.

Fuel spill and cleanup concerns

This one doesn't get enough attention. After certain incidents, cleanup obligations can become part of the problem, not just the physical damage itself. Owners who dock regularly, keep larger fuel loads, or spend time around marinas should ask whether the policy addresses that exposure clearly.

A simple add-on checklist

Use this before you buy or renew:

- Ask about towing: Is it included, optional, or excluded?

- Ask about uninsured boaters: If another operator causes the accident, how does your policy respond?

- Check trailer language: Don't assume your trailer is protected just because the boat is.

- Review stored gear: Electronics and equipment need clear treatment in the policy.

- Confirm marina expectations: Some facilities want proof of specific coverages, not just any policy number.

The best add-ons are the ones tied to your real habits. If you tow riders, dock in crowded places, trailer often, or leave the boat in a slip, build around that.

How Much Does Boat and PWC Insurance Cost on Lake Norman?

The honest answer is that cost depends on the vessel, the operator, the storage setup, and the coverage choices. There isn't one “Lake Norman rate,” and anyone who quotes one without details is guessing.

What you can count on is the underwriting logic. Insurers look at the type of boat or PWC, the value, the horsepower and performance profile, who operates it, where it's stored, how it's used, and how much liability protection you want.

Why PWCs often price differently

PWC insurance often surprises people. The craft is smaller than a pontoon or runabout, so they assume the premium should automatically be lower. That's not always how it works.

The underwriting community treats PWCs as a distinct category for a reason. There are nearly 1.4 million registered PWCs in the U.S., and North Carolina requires a minimum of $300,000 in insurance on each PWC rented to the public, which shows regulators recognize the higher risk profile involved, according to the Water Sports Foundation's U.S. PWC market information.

That rental benchmark doesn't set your personal premium. But it does tell you something important. These machines create liability concerns that insurers take seriously.

The factors that usually move the price

Some rating factors are predictable:

- Boat type and performance: A pontoon, a fishing boat, a wake boat, and a high-performance runabout won't be viewed the same way.

- Operator history: Prior claims, driving history, and experience can affect pricing.

- Storage: A boat in a secured setup is a different risk than one left exposed at a dock or on an open trailer.

- Use pattern: Towing riders, frequent weekend use, and guest operators can all matter.

- Deductible and limits: Higher deductibles may lower premium, while stronger liability limits usually cost more.

If you want a broad consumer-oriented reference point for how marine premiums are commonly discussed, the Better Boat guide on marine insurance costs is a useful supplement. It won't replace an actual quote, but it can help you understand why two owners with similar-looking boats may get very different numbers.

A better way to shop than chasing the lowest quote

The cheapest quote often leaves out something important. Maybe towing isn't included. Maybe the liability limit is too thin. Maybe the trailer treatment is weak. Maybe the policy is fine for simple cruising but not ideal for wakeboarding or regular marina docking.

That's the same mistake people make in other recreational vehicle markets. Comparing insurance only by premium usually backfires because usage style changes the risk. The logic is similar to what you see in the best RV insurance companies comparison, where storage, travel habits, and equipment change what “good coverage” really means.

What to have ready before requesting quotes

You'll get a cleaner quote faster if you have these details ready:

| Information to gather | Why it matters |

|---|---|

| Year, make, model, and value | Forms the base of the physical damage rating |

| Horsepower and modifications | Affects performance and risk profile |

| Storage location | Marina, home, covered, uncovered, trailer, or slip |

| Operator details | Age, experience, loss history, and driving history |

| Usage details | Cruising, fishing, towing riders, seasonal use, guest use |

One practical note. If you want a fast side-by-side comparison, an independent agency such as Select Insurance Group, Inc. can compare multiple carrier options rather than forcing you into one company's appetite and pricing model.

Top Risks for Lake Norman Boaters and How to Prepare

Lake Norman losses usually don't happen because someone forgot the word “insurance.” They happen because owners didn't connect a local risk to the right coverage before something went wrong.

The biggest trouble spots here are easy to recognize if you spend time on the lake. Crowded restaurant docks. Busy holiday traffic. Sudden summer weather. Gear left on board. PWCs and high-performance boats operating close to slower family craft.

Four scenarios owners on this lake recognize fast

A common one is the restaurant dock claim. You come in hot because the wind pushes you, there's a crowd watching, and the space is tighter than it looked from the water. That's how another hull gets scraped, a dock post gets cracked, or a passenger twists a knee trying to fend off.

Then there's the quick afternoon storm. Inland-lake owners increasingly face storm-related losses from severe convective storms and hail, which can damage docked boats and stored PWCs. At the same time, high-performance boats and PWCs are disproportionately represented in claims, which is part of why insurers price them differently, as discussed in Watson Insurance's Charlotte-area boat insurance overview.

A third scenario is equipment theft. It's not always the whole boat. Sometimes it's electronics, gear, or accessories that disappear while the boat sits at a marina or behind a lakeside home.

The fourth is the one many owners never plan for. A transient boater hits you and their insurance turns out to be missing, disputed, or nowhere near enough.

Crowded water changes small mistakes into insurance claims faster than open water does.

Common Lake Norman Risks & Your Insurance Shield

| Lake Norman Risk | Potential Consequence | Key Coverage Solution |

|---|---|---|

| Docking at a crowded marina or restaurant | Damage to another boat, dock, or passenger injury | Liability coverage, medical payments |

| Wakeboarding or tubing with guests | Injury claims involving a rider or passenger | Liability coverage, medical payments |

| Sudden hail or severe storm while docked | Damage to hull, upholstery, electronics, or PWC bodywork | Physical damage coverage |

| Theft from boat, dock, or storage area | Out-of-pocket replacement of gear or equipment | Physical damage, personal effects coverage |

| Breakdowns far from launch point | Costly recovery and interrupted day on the water | On-water towing assistance |

| Hit by an uninsured or underinsured boater | Repair bills and injury costs with weak recovery options | Uninsured or underinsured boater coverage |

| Trailer problem during transport or storage | Damage to trailer, vessel, or related equipment | Trailer coverage and physical damage coverage |

Preparation that actually reduces claims

Insurance matters most after the loss. Preparation matters before it.

A few habits reduce trouble significantly:

- Practice docking when it's quiet: Don't make a busy fuel dock your training ground.

- Watch the weather early: Summer cells move fast. Leaving ten minutes sooner beats filing a hail claim later.

- Secure gear and document upgrades: Keep photos and receipts for electronics, accessories, and custom additions.

- Treat the trailer like part of the risk: For a practical maintenance refresher, this checklist of essential trailer care steps is worth reviewing before peak season.

- Review guest use: If different family members or friends operate the boat, say so up front when you buy coverage.

The best insured boaters on Lake Norman usually do two things well. They carry the right policy, and they don't rely on the policy to compensate for bad habits.

Get Your Fast and Free Lake Norman Boat Insurance Quote

Boat and PWC insurance Lake Norman NC should do one job well. It should protect the way you actually use the lake. Not a generic boat owner on a brochure. You.

That means looking beyond a basic quote and checking whether the policy matches your real exposures. Guest passengers. Towed riders. Docking claims. Marina requirements. Trailer losses. Storm damage. Uninsured boaters. Those are the issues that decide whether your coverage feels solid or flimsy when something goes wrong.

What to ask before you bind coverage

When you request quotes, ask direct questions:

- Will this policy fit how I store the boat or PWC?

- Does it handle guest operators and guest passengers clearly?

- How does it respond to towing activities like wakeboarding or tubing?

- What proof of insurance will my marina or lender want?

- What's included versus optional for towing, trailer damage, and uninsured boaters?

A local conversation usually beats a generic online application because Lake Norman use patterns are specific. Docking habits, storage choices, and weekend traffic all shape what a smart policy looks like.

Why an independent agency model helps

If you've never worked with an independent agency, it helps to understand the difference. An independent agent can compare multiple carrier options instead of quoting one company's single answer. This overview of what an independent insurance agency is explains that model well.

That matters for boats and PWCs because pricing appetite can vary a lot based on vessel type, performance, storage, and how you use the watercraft.

If you want a quote, gather your boat or PWC details, where it's stored, who operates it, and any financing or marina requirements. That makes the process faster and the comparison more accurate.

If you want help sorting through Boat and PWC insurance for Lake Norman, Select Insurance Group, Inc. can provide a fast, free, no-obligation quote and compare options across multiple carriers. Call or text for pricing, coverage review, or help matching a policy to your boat, PWC, marina requirements, and how you use the lake.