You open the mail, or your inbox, and see the kind of notice Florida homeowners dread. Your premium jumped again. Or worse, your carrier isn't renewing at all. You haven't filed a major claim, you maintain the property, and you still feel like the rules changed overnight.

That reaction is normal. The home insurance Florida market doesn't feel stable to most homeowners because it often isn't. What shows up in headlines as a statewide “crisis” usually lands in a very personal way: a closing delayed, a lender asking questions, a roof inspection you didn't expect, or a quote that blows up your monthly budget.

The good news is that this market is still navigable if you know what insurers care about, where standard policies stop, and how inland risk differs from coastal risk. That's where most generic advice falls short. A homeowner in Orlando with an older roof and aging electrical has a different problem than a homeowner near the Gulf dealing with wind exposure and flood layering. Both need a plan. It just won't be the same plan.

Table of Contents

- Welcome to the Florida Home Insurance Puzzle

- Florida Home Insurance 101

- Decoding Your Policy Coverages and Exclusions

- Florida's Triple Threat Wind Flood and Sinkholes

- Why Is Florida Home Insurance So Expensive

- Your Action Plan for Finding Affordable Coverage

- Partner with a Pro to Simplify Florida Home Insurance

Welcome to the Florida Home Insurance Puzzle

A lot of homeowners think they did something wrong when the quote comes back high or the renewal disappears. In Florida, that usually isn't the reason. The market itself has changed in ways that hit ordinary homeowners, including people with clean claims histories and homes outside the beach towns.

Florida's homeowners policy non-renewal rate reached 2.99% in 2023, the highest in the nation, and that represented a 280% increase over five years. The same wave pushed over 1.3 million policyholders onto Citizens Property Insurance Corporation, according to Central Florida Public Media's reporting on Florida non-renewal rates.

That matters because it reframes the problem. If you received a non-renewal, a painful premium increase, or a demand for new inspections, you're not dealing with an isolated glitch. You're dealing with a market that has become stricter, more selective, and much less forgiving.

What that feels like on the ground

One homeowner gets told the roof is “too old” for a preferred policy, even though it isn't leaking. Another learns their home needs updated plumbing documentation before a carrier will even consider binding. An inland buyer assumes they're safe from the worst of Florida insurance problems, then finds out older housing stock can narrow options just as fast as coastal wind exposure.

Practical rule: In Florida, insurers don't just insure location. They insure condition, documentation, and how easy your house is to classify inside their underwriting rules.

That's why broad advice like “shop around” often disappoints people. Shopping only works when the file is complete and the property is presented correctly. If your roof age is unclear, your electrical system isn't documented, or your flood exposure hasn't been separated from your wind exposure, many quotes either won't appear or won't be useful.

What works better than panic shopping

Start by accepting two realities. First, affordable coverage in Florida often comes from preparation, not luck. Second, your strategy should match where and how the home sits.

A coastal homeowner usually needs to think hard about wind, flood, and deductibles. An inland homeowner may need to focus more on age of systems, local drainage issues, housing stock condition, and whether private carriers will accept the home at all. Those aren't the same problem, so they shouldn't get the same advice.

Here's the practical mindset: stop looking for one magic policy and start building a workable protection plan. That plan may include homeowners coverage, separate flood coverage, better inspections, mitigation proof, and a higher deductible if your budget requires it.

Florida Home Insurance 101

Home insurance Florida is a financial protection contract for two big categories of risk. One category covers the house and your belongings. The other covers your legal and financial exposure if someone gets hurt or you damage someone else's property.

The most common policy type for owner-occupied homes is often called an HO-3 policy. You don't need to memorize the label. What matters is what it does.

Think of the policy as a financial fortress

The first wall protects the physical property. That includes the house itself and, depending on the policy terms, other structures and personal belongings. If a covered event damages the structure, this part of the policy is what responds.

The second wall protects your assets from liability claims. If a visitor is injured on your property and you're legally responsible, liability coverage may help with defense costs and damages up to the policy limits.

A third piece often gets overlooked until after a loss. If the home becomes unlivable because of a covered claim, many policies include coverage for temporary living expenses.

Open perils and named perils in plain English

These phrases confuse people because they sound technical. The practical difference is simpler than it looks.

- Open perils for the dwelling: The house is generally covered unless the cause of loss is excluded.

- Named perils for personal property: Your belongings are usually covered only for causes specifically listed in the policy.

- Exclusions still control: Flood and certain ground-related losses are common examples where homeowners make costly assumptions.

That's why reading only the declarations page isn't enough. The declarations page tells you limits, deductibles, and premium. It doesn't tell you the full story of where the holes are.

If you want a plain-English walkthrough of what happens after a loss, this expert home insurance claim advice is useful because it helps homeowners think about documentation and process before they're under stress.

The basic job of your policy

A solid homeowners setup should answer these questions clearly:

| Question | Why it matters |

|---|---|

| What structure is insured | You need to know what part of the property falls under the main dwelling coverage. |

| What belongings are protected | Limits, categories, and exclusions can leave gaps if you assume too much. |

| What liability limit you carry | Lawsuits and injury claims can put savings and future income at risk. |

| What deductible applies | A policy that looks affordable can still leave a painful out-of-pocket burden after a loss. |

A good policy isn't the cheapest one on the screen. It's the one that still makes sense when the claim is real.

Decoding Your Policy Coverages and Exclusions

The declarations page tells you the premium, deductible, and headline limits. The core substance sits in the coverage sections and exclusions. If you don't know how those parts work, it's easy to think you're protected when you're only partially protected.

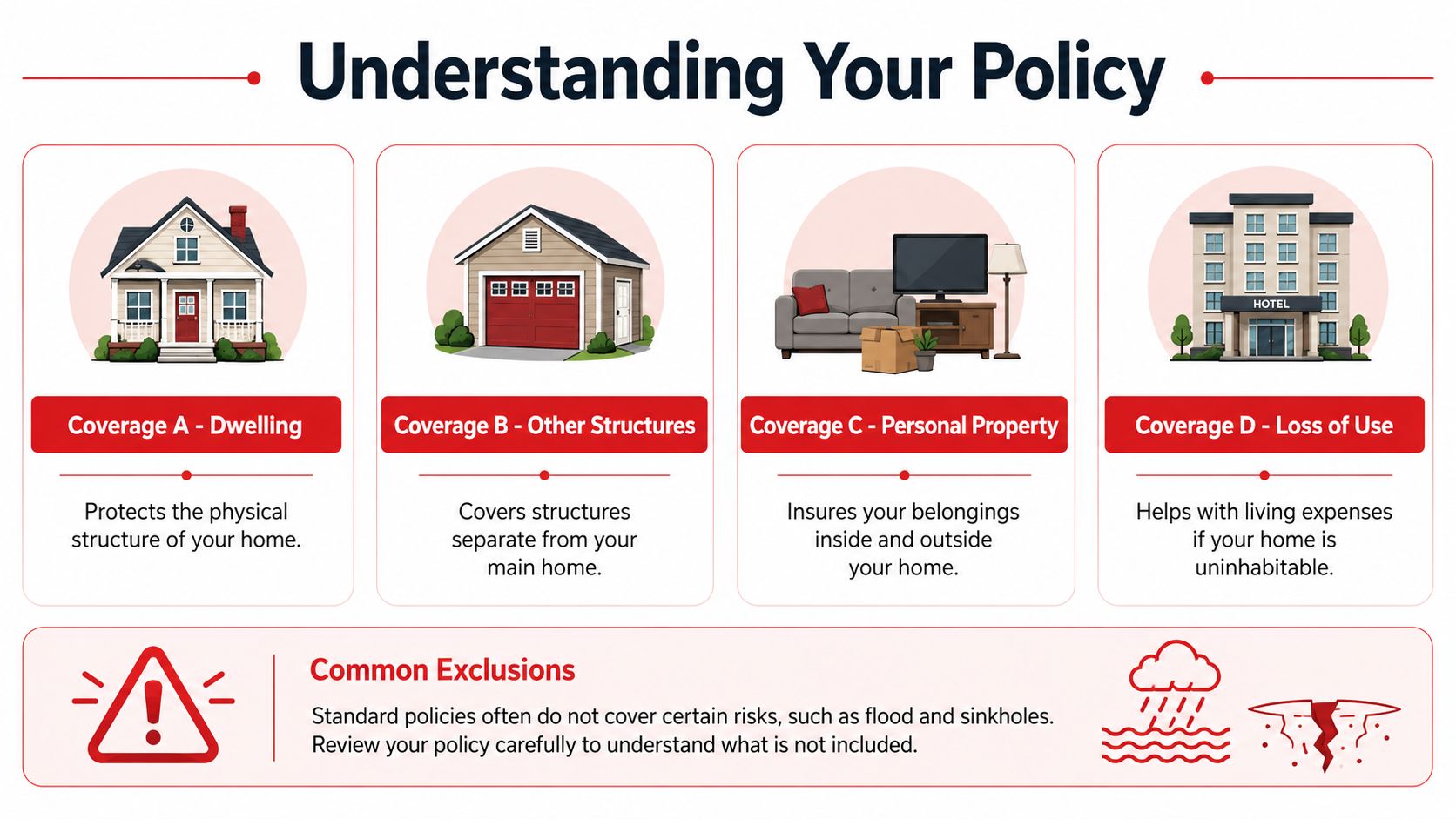

The four buckets most homeowners need to know

Coverage A, Dwelling is the main structure. Think roof, walls, attached garage, and the physical building itself. If a covered event damages the house, this is usually the core coverage that responds.

Coverage B, Other Structures handles structures separated from the main home. A detached garage, fence, shed, or standalone workshop often falls here. Homeowners miss this all the time and assume every structure on the lot shares the same protection automatically.

Coverage C, Personal Property covers belongings such as furniture, clothing, electronics, and household items. But this section often has sublimits and specific rules. High-value items may need extra attention.

Coverage D, Loss of Use helps with temporary living expenses if a covered loss makes the home uninhabitable. Hotel stays, short-term rental costs, and related living expenses can become a major issue if repairs drag on.

A practical way to review your policy is to test each bucket against a real example from your life. Detached workshop. Backyard fence. Family laptop. Temporary housing after major roof damage. If you can't tell which section would answer each one, you need a closer review.

Why older Florida homes get extra scrutiny

Florida carriers don't underwrite older homes casually anymore. Insurers increasingly require four-point inspections for homes built before 2002, focused on the roof, HVAC, plumbing, and electrical. The same market analysis notes that coastal property loss ratios can exceed 100% when wind, water damage, and litigation costs are factored in, as described in the Florida insurance market report.

That inspection requirement frustrates buyers, but it has a clear purpose. The carrier wants to know whether the systems most likely to cause a serious claim are aging out, improperly maintained, or already showing trouble.

Here's what usually triggers problems:

- Roof age and condition: Missing documentation, visible wear, or prior patchwork repairs can shrink your options fast.

- Electrical concerns: Older panels, unsafe wiring conditions, or a lack of updates can stop a quote before it starts.

- Plumbing risk: Older supply lines and drain systems raise concern because water losses can be expensive and disruptive.

- HVAC condition: Aging systems can create both maintenance and habitability issues.

When you hire contractors for repairs or updates tied to underwriting, it also helps to understand the difference between licensing, bonding, and insurance. This overview from HomeProBadge explains bonded vs insured in a way homeowners can use when vetting vendors.

The best underwriting file is boring. Clear roof age, clear updates, clear photos, clean inspection notes.

Exclusions that surprise homeowners

Standard homeowners insurance often does not cover every major Florida hazard. Flood is the classic example, but it's not the only one. Certain water losses, ground movement issues, and maintenance-related damage can also fall outside standard protection.

That's why “I have homeowners insurance” and “I'm fully protected” are not the same statement.

Florida's Triple Threat Wind Flood and Sinkholes

The most expensive misunderstanding in Florida is assuming one home policy covers one storm from start to finish. It usually doesn't. A hurricane can bring wind, wind-driven rain, rising water, and ground issues. Those don't always fall under the same coverage.

Wind is not the same as flood

If wind rips shingles off your roof and rain enters because the roof was damaged by a covered wind event, that may fall under homeowners coverage, subject to your policy terms and deductible. If water rises from the ground, storm surge enters the home, or surface water floods the structure, that is usually a flood issue, not a standard homeowners issue.

That distinction matters most after hurricanes because homeowners often describe the event as one storm, while the policy responds based on the specific cause of damage. The claim question is not “Did a hurricane hit?” It's “What caused this specific damage?”

For many properties, separate flood coverage is what closes that gap. If you're sorting out whether it's required, recommended, or prudent based on your home's location, this guide on flood insurance requirements in Florida helps frame the decision.

A homeowner can be right about the storm and still wrong about the coverage.

Coastal and inland homes face different versions of risk

Coastal homeowners usually think first about wind exposure, hurricane deductibles, and flood layering. That's appropriate. Their risk is often obvious, and insurers price for it aggressively.

Inland homeowners make a different mistake. They assume distance from the coast means they can safely skip flood coverage or relax about water risk. But inland losses often come from drainage failures, prolonged rain, ponding water, and older neighborhoods where grading, code history, or stormwater infrastructure don't perform as expected.

The practical split looks like this:

| Home location | Main insurance focus |

|---|---|

| Coastal | Wind exposure, separate flood coverage, stricter underwriting, stronger mitigation file |

| Inland newer home | Drainage and water entry review, policy exclusions, deductible fit, flood decision based on actual exposure |

| Inland older home | System age, insurability, roof condition, plumbing and electrical updates, plus flood review |

Roof design and roof condition also shape how underwriters view wind risk. Homeowners looking at upgrade options sometimes research more durable assemblies and coatings, including spray polyurethane roofing, as part of a broader conversation with licensed roofing professionals and insurers about resilience and insurability.

Sinkhole assumptions cause expensive mistakes

Florida homeowners often use “sinkhole” as a catchall term, but policies may draw distinctions that matter. Some ground collapse scenarios receive limited treatment under standard forms, while broader sinkhole protection may require optional coverage or may be harder to find depending on the property and carrier.

That means you shouldn't assume cracks, settling, or depression-related concerns automatically trigger broad sinkhole benefits. The policy wording matters. So does the cause of loss.

Here are the practical questions to ask before you bind coverage:

- What ground-related events are included by default

- What events require optional coverage

- What evidence would the carrier require to confirm the cause

- Whether the home's location or loss history affects availability

For coastal owners, the biggest blind spot is often flood. For inland owners, it's often the belief that “not coastal” means “not exposed.” In Florida, both assumptions can cost you.

Why Is Florida Home Insurance So Expensive

Florida doesn't have high premiums for one reason. It has high premiums because several expensive forces stack on top of each other, and all of them flow into your quote.

For a standard $300,000 dwelling policy, Florida's average annual premium is about $6,300, compared with the national average of $2,868, according to the National Association of Realtors report on states where home insurance costs are surging. That same report says one projection estimates Florida's average could approach $15,460 annually by 2025, and it clearly labels that as a projection rather than a current statewide average.

The price problem starts before your quote reaches you

Most homeowners think pricing starts at the kitchen table when they request a quote. It starts much earlier.

Insurers buy their own protection in the reinsurance market. In plain language, that's insurance for insurance companies. When reinsurance gets more expensive, carriers pass those costs through to policyholders.

Florida also has a history of severe storm exposure, expensive claim severity, and underwriting pressure on older properties. Put all that together and the base cost of offering coverage rises before your individual property details are even reviewed.

Another pressure point has been litigation. The Florida market report described earlier noted that Florida's share of all U.S. homeowners insurance litigation reached 76% during a peak period, which helps explain why carriers became more restrictive in pricing and eligibility.

Why the same house can price differently from one year to the next

A homeowner may ask, “Why did this house insure fine last year but not this year?” Usually, one of these things changed:

- Carrier appetite changed: A company may still write in Florida but pull back from certain roof ages, ZIP codes, or construction types.

- Reinsurance costs shifted: The cost of backing the insurer's book changes, and homeowners feel it at renewal.

- Underwriting tightened: A home that once passed with limited documentation may now need fresh proof of updates and inspections.

- Your deductible or coverage fit changed: Sometimes the policy available at renewal isn't structured the same way as the old one.

The hard part is that some of these changes have nothing to do with you personally. The useful part is that some do. Roof documentation, wind mitigation details, inspection quality, and layered coverage choices are still variables you can influence.

High premium does not always mean overpricing. Sometimes it means the carrier is one of the few still willing to write that specific risk.

For inland homeowners, cost often comes from age-of-home issues and scarce private-market appetite rather than obvious beach exposure. For coastal homeowners, cost is more directly tied to wind and water exposure plus stricter catastrophe pricing. Different inputs, same sticker shock.

Your Action Plan for Finding Affordable Coverage

A Florida homeowner often loses money before the first quote even comes back. The file is incomplete, the roof paperwork is vague, the wind mitigation form is outdated, and the carrier prices the uncertainty. If you want a better result, start by making the house easier to underwrite.

Start with the house not the quote

Shopping first feels productive, but in Florida it often creates bad comparisons. One carrier assumes an older roof with no documentation. Another assumes updates were never completed. A third declines until it sees inspection details. The homeowner ends up comparing numbers that were built on different assumptions.

A cleaner file usually gets cleaner pricing.

Before you shop, gather what an underwriter is likely to ask for:

Proof of roof age and condition

Permits, invoices, inspection reports, and clear photos all help. If roof age is uncertain, many carriers treat that as added risk.Wind mitigation documents

If the home has impact-rated openings, roof-to-wall connections, secondary water resistance, or other protective features, make sure they are documented on a current form.Records of major system updates

Electrical, plumbing, and HVAC updates matter. Keep receipts, permits, and inspection records in one place so the carrier does not have to fill in the blanks.Prior inspection reports

Four-point and full home inspections can answer questions before they turn into pricing problems or declinations.

For inland homeowners, this paperwork often matters more than people expect. The problem may be age, maintenance, or construction details rather than beach exposure. For coastal homeowners, the same documentation still matters, but wind exposure and storm-driven water usually drive more of the pricing pressure.

Know when Citizens fits and when it does not

Citizens Property Insurance can be a practical fallback for homeowners who cannot place coverage in the private market or who meet the state's eligibility rules, as explained in this overview of Florida homeowner protection and Citizens eligibility. That makes it useful. It does not make it automatic.

The right question is whether Citizens solves your actual risk problem at a price you can carry.

Some homes need a fallback market because private carriers will not accept the roof age, claim history, location, or construction type. In that case, Citizens may be the path that keeps coverage in force. But homeowners still need to review deductibles, exclusions, and whether separate flood protection is needed. Coastal owners usually know to ask about flood. Inland owners should ask too, especially near lakes, rivers, low-lying areas, or neighborhoods with poor drainage.

Liability is another blind spot. A standard home policy may not be enough for a household with savings, rental property, teenage drivers, a pool, or higher future earnings. In those cases, a personal umbrella policy for asset protection in Florida can add another layer above the home and auto policies.

Use a tighter shopping checklist

A rushed quote process usually costs more. A disciplined one gives you a better chance of finding a policy that is both usable and affordable.

Ask these questions before you choose:

How is the roof being evaluated?

Ask whether the quote is based on verified age, remaining useful life, or a simple year-built assumption.What deductible structure applies?

A lower premium may come with a hurricane deductible that feels manageable on paper but hurts after a real loss.What is excluded or limited?

Ask for plain-English explanations of water damage limits, screen enclosure rules, roof settlement terms, and cosmetic damage restrictions if they apply.Should flood coverage be paired with this policy?

Coastal and inland homes face different water risks, but both can have serious uncovered losses without a separate flood policy.What documents will the carrier require after binding?

A cheap quote is not much help if the policy is likely to be canceled after inspection because the file was incomplete.Is this property better handled through an independent agency?

Homes with older roofs, mixed updates, prior claims, unique construction, or coastal exposure often need broader market access. Select Insurance Group, Inc. is one example of an agency model that compares quotes across a broad carrier range rather than relying on a single company appetite.

One final point is blunt but important. Dropping coverage or carrying too little coverage because the premium feels painful can turn a hard bill into a financial disaster. In Florida, one major wind, water, or liability loss can exceed what many households can pay out of pocket.

Partner with a Pro to Simplify Florida Home Insurance

A lot of Florida homeowners reach the same point. The online quotes look close enough, the forms ask for details that seem minor, and then an inspection, roof question, or flood issue changes the whole result. At that point, insurance is less about finding a cheap number and more about fitting the policy to the house.

A good agent solves matching problems

Florida policies can look similar at first glance and work very differently after a claim. Carrier rules change. Inspection findings matter. A home three miles inland can have a different insurance strategy than a home on the coast, even if the sale price is similar. That is one reason many new buyers feel lost.

An independent agent helps sort out the parts that cause trouble later, not just the premium shown on page one. That includes documentation before quoting, whether a private carrier is still realistic, when a last-resort market may need to be considered, and whether separate flood or umbrella coverage makes sense for the property and the household balance sheet.

More Florida owners are trimming coverage, accepting bigger gaps, or going without protection to cut costs, as noted earlier. I understand why. Premium shock is real. But I have also seen one bad wind claim, one water loss, or one liability suit wipe out years of savings.

If you want help from a local independent agency, support from a Florida insurance agency that works through multiple coverage options can make the process easier, especially for homes with older roofs, mixed updates, prior claims, coastal exposure, or other underwriting complications.

If you need help sorting through home insurance options in Florida, Select Insurance Group, Inc. can provide a no-obligation quote review and help you compare practical coverage options based on your home's location, condition, and risk profile.