If you're trying to insure an older house in North Carolina right now, you're probably running into the same frustrating pattern. One carrier declines. Another offers a policy that strips out key protections. A third gives you a premium that makes you wonder whether the house itself is the problem.

In many cases, the house isn't the problem. The mismatch between an older home and standard underwriting is.

North Carolina homeowners insurance for older homes is harder to place because carriers don't just look at charm, square footage, or neighborhood. They look at systems, rebuild complexity, storm exposure, and whether the home fits a modern policy form. Once you understand those moving parts, the options get clearer. The right answer often isn't "get a standard policy at any cost." It's choosing the policy structure that fits the property, then documenting the upgrades that make underwriters more comfortable.

Why Insuring an Older North Carolina Home Is So Difficult

Most carriers in North Carolina treat a home as "older" somewhere in the 30 to 50 year range, with 40 years serving as a common benchmark. That aging profile is one reason the state's average annual homeowners premium reaches about $3,025 for $400,000 in dwelling coverage, which is 21% above the national average, according to Allen Insurance Agency's overview of home insurance and aging properties.

That benchmark surprises a lot of homeowners. They hear "older home" and think of a century-old farmhouse or a historic downtown property. Underwriters often mean something much more ordinary, like a house built decades ago with systems that may still be original or only partially updated.

Underwriters read your house like a maintenance record

A useful way to think about it is a used car. Two cars can be the same age, but one has complete service records, new brakes, a recent transmission check, and updated tires. The other still runs, but no one knows when major work was last done. Insurers view older houses the same way.

Four areas trigger the most concern:

- Roof condition and material: An older roof creates obvious claim risk. Leaks, wind damage, and harder-to-match materials all make losses more expensive to settle.

- Electrical system: Older wiring types and outdated panels raise concern because they can increase the chance of fire or repeated repair issues.

- Plumbing system: Aging supply lines and drain systems create a steady risk of interior water damage, which can become a large claim quickly.

- Foundation and structure: Homes built to older standards may not perform as well when wind, water, or settling puts stress on the structure.

A home can be beautifully maintained and still trigger underwriting questions if those systems haven't been modernized. That's the gap many owners miss.

Practical rule: Insurers don't price nostalgia. They price repair difficulty, claim frequency, and uncertainty.

Older materials create claims friction

Older homes also carry a rebuild problem. Some materials are discontinued. Some methods of construction are uncommon now. Some repairs require specialty labor. That matters because a carrier isn't just asking, "Will this house have a claim?" It's also asking, "How difficult will this claim be to resolve?"

This is one reason standard policy eligibility narrows as homes age. Carriers may still insure the property, but they may require inspections, updates, endorsements, or a different policy form entirely.

Storm exposure makes that harder in North Carolina. Hurricanes and wind-driven rain don't only affect coastal homes, and they can expose weak points fast. If you're also trying to understand how wind and named-storm claims work in related policy settings, this overview of renters insurance and hurricane damage gives a useful parallel on how policy wording shapes real-world protection.

What usually doesn't work

Homeowners often make two mistakes.

First, they assume loyalty to one brand will solve the issue. It usually won't if the home falls outside that carrier's appetite.

Second, they ask for "the cheapest policy" before they know which policy type the house can support. For an older property, that approach often produces a bad fit rather than a bargain.

Understanding Your NC Insurance Policy Options

Once a standard homeowners quote gets difficult, many owners think they're out of options. They're not. They just need to stop thinking in terms of one policy form.

For older homes in North Carolina, the main choices usually fall into three buckets: HO-3, HO-8, and a dwelling fire policy such as DP-3. Each solves a different problem.

The core difference is how broad the coverage is and how claims are paid

A standard HO-3 is what most homeowners want because it's familiar and broad. If the house qualifies, it's usually the cleanest fit for an owner-occupied primary residence.

An HO-8 is often the workaround when the home's age, condition, or rebuild characteristics make standard underwriting uneasy. It keeps the owner in a homeowners-style form, but with modified terms built for older properties.

A DP-3 or another dwelling fire form comes into play when a standard homeowners policy isn't available. As the Kenan Institute explains in its discussion of North Carolina's insurance pressures, dwelling fire policies such as DP-1 or DP-3 are critical alternatives for older homes that can't be insured under a standard HO-3, and they often use actual cash value, which reflects depreciation.

Home Insurance Policy Comparison for Older NC Homes

| Feature | HO-3 (Standard Policy) | HO-8 (Modified Policy) | DP-3 (Dwelling Fire) |

|---|---|---|---|

| Best fit | Owner-occupied homes that meet standard underwriting | Older homes that need modified homeowners coverage | Homes that don't fit standard homeowners underwriting |

| Coverage style | Broad homeowners form | Modified homeowners form for aging or historic-style risks | Dwelling fire form, often used as an alternative |

| Claim settlement | Often structured more favorably than ACV-based alternatives, depending on carrier terms | Depends on carrier and endorsements | Often Actual Cash Value, especially on older structures |

| Perils approach | Broader than limited named-perils forms | More tailored and narrower than standard HO-3 | Often named perils coverage |

| Liability | Typically included | Typically included | May need careful review depending on form and setup |

| Good for | Homes with updated systems and strong eligibility | Homes with charm but tougher underwriting characteristics | Homes where replacement economics or condition push carriers away from HO-3 |

Replacement cost and actual cash value aren't the same

This difference matters more than homeowners expect.

- Replacement Cost Value (RCV): Pays based on what it costs to repair or replace with like kind and quality, subject to policy terms.

- Actual Cash Value (ACV): Pays after depreciation is applied.

If your older roof, plaster, trim, or built-in features are already aged, an ACV settlement can leave a much larger out-of-pocket gap. That's why a cheaper premium can become expensive at claim time.

A policy that fits the house is better than a broader policy you can't keep. But a lower premium isn't a win if the settlement method leaves you underinsured after a loss.

Which option usually makes sense

A practical way to decide:

- Choose HO-3 if the home qualifies and the systems are updated enough to satisfy underwriting.

- Choose HO-8 when you need a homeowners-style policy for an older house with unique rebuild or age concerns.

- Choose DP-3 when standard homeowners coverage isn't available and you need a workable path to insure the dwelling.

The policy type isn't a status symbol. It's a tool. The right one depends on the home's condition, not the owner's preference alone.

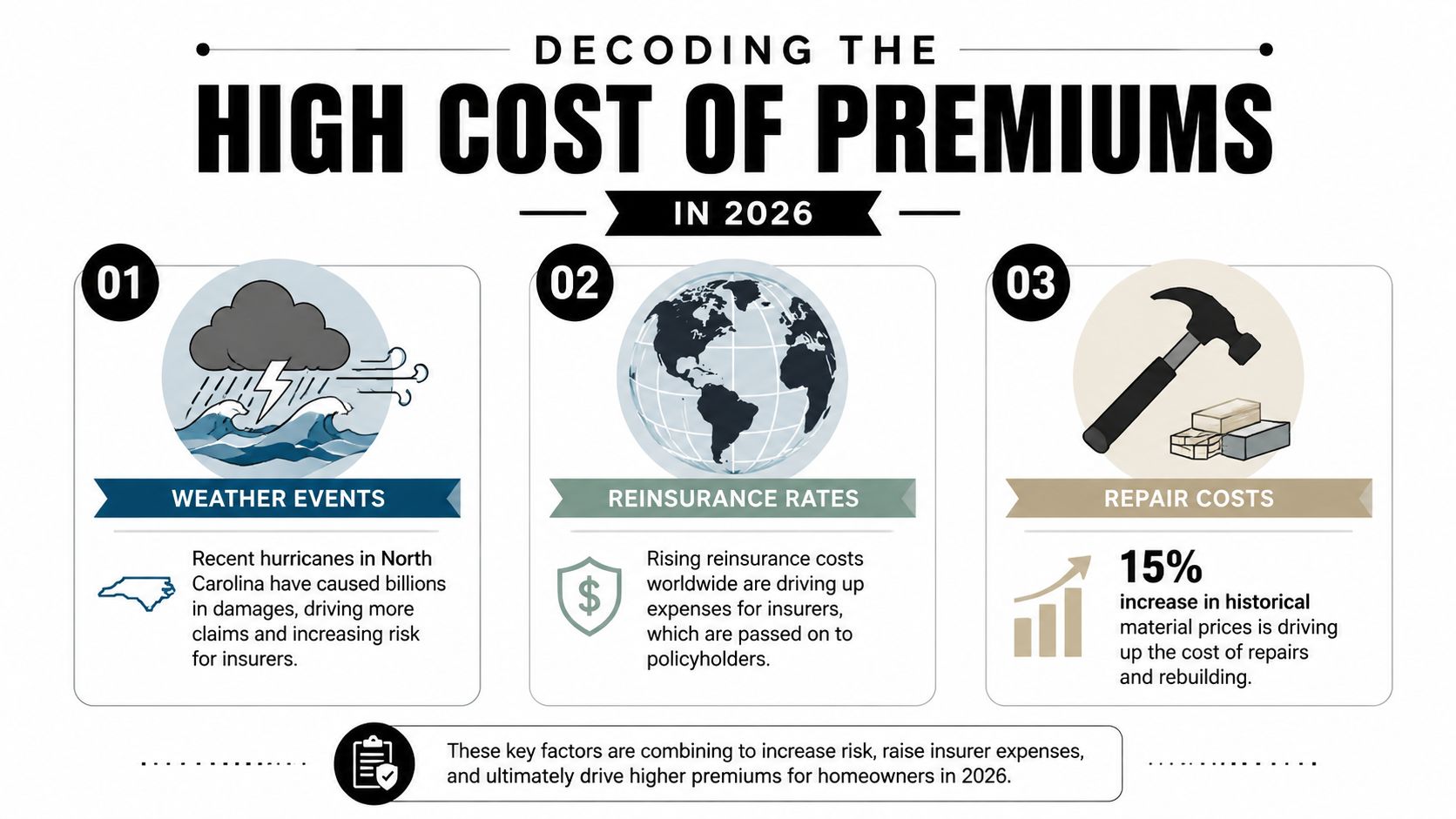

Decoding the High Cost of Premiums in 2026

The price pressure many North Carolina homeowners feel didn't come from one bad renewal cycle. It's part of a larger climb.

According to Guardian Service's review of North Carolina's 2025 rate increase, homeowners insurance rates in the state rose 44.4% from 2020 to mid-April 2025. After negotiations, a 7.5% statewide average increase took effect on June 1, 2025, and another 7.5% is slated for 2026.

Those statewide figures don't mean every home moves the same way. Older properties often feel the increase more sharply because they stack multiple concerns at once: age, repair complexity, and weather vulnerability.

Why the market is pushing premiums up

Three forces are hitting the same policy at the same time.

First, North Carolina has seen repeated storm pressure. Carriers price not only past claims, but also the actual chance of future wind and water losses.

Second, reinsurance costs matter. Insurers buy protection for their own catastrophic losses, and when that cost rises, policyholders feel it downstream.

Third, repairs on older homes are rarely simple. Matching materials, finding skilled labor, and addressing hidden problems once walls or roofs are opened all make claims less predictable.

Older homes get priced for uncertainty

A newer home with updated wiring, plumbing, and roof may still be expensive to insure in the current market. An older home with open underwriting questions gets priced for uncertainty on top of that.

That's why two houses on the same street can produce very different quotes. One home shows recent upgrades with clear documentation. The other has patchwork repairs, aging systems, or an inspection report full of deferred maintenance. The premium reflects more than location.

Market reality: A high premium doesn't always mean the quote is bad. Sometimes it means the carrier is one of the few still willing to write the risk.

How to judge a quote in a hard market

Don't evaluate the number first. Evaluate the structure.

Use this checklist:

- Look at the policy form: Is it HO-3, HO-8, or DP-3?

- Check settlement basis: Will major dwelling losses be handled on ACV or more favorable replacement terms?

- Review deductibles: Make sure wind or hurricane deductibles won't create an unpleasant surprise.

- Read exclusions and endorsements: Water backup, ordinance or law, and service line issues matter more in older houses.

- Confirm rebuild assumptions: If the home has unusual features, ask how the dwelling amount was estimated.

That context helps you separate a competitive quote from one that only looks cheaper because it gives up important protection.

Proven Upgrades to Lower Your Insurance Bill

Carriers don't reward every renovation equally. A new backsplash won't move underwriting much. A documented roof replacement or electrical overhaul can.

The best strategy is to focus on the systems most likely to cause claims or trigger eligibility problems. Think in terms of Good, Better, Best. You don't always need a full gut renovation, but targeted upgrades can improve both insurability and price.

Start with roof, wiring, and plumbing

These are the systems that underwriters ask about first because they generate expensive claims.

- Good: Repair obvious defects, replace missing shingles, fix active leaks, and gather invoices for prior work.

- Better: Replace aging materials before they fail, update an obsolete panel, and remove known plumbing weak points.

- Best: Complete the upgrade and keep dated permits, contractor receipts, and photos ready for underwriting review.

Roof work often has the fastest impact because roof age and condition are central to wind and water exposure. For homeowners comparing replacement decisions in the Triangle, these Triangle area roofing insurance insights offer a useful explanation of why roof condition affects premiums and eligibility so directly.

Storm hardening can help older homes compete better

For North Carolina homes exposed to hurricane and wind risk, mitigation matters. The challenge isn't only preventing damage. It's showing a carrier that the home is less fragile than its build year suggests.

Some upgrades to consider:

- Roof attachment improvements: Ask your contractor what can be documented for insurer review.

- Opening protection: Shutters or stronger protection for vulnerable openings can make a difference in underwriting comfort.

- Garage door reinforcement: A weak garage door can become a major pressure point during wind events.

- Water management: Gutters, drainage correction, and attention to grading won't solve every issue, but they reduce recurring loss triggers.

Documentation matters almost as much as the work itself

Homeowners often spend money on upgrades and still don't get underwriting credit because they can't prove what was done.

Keep a simple file with:

- Contractor invoices

- Permit records if applicable

- Before-and-after photos

- Material specifications

- Inspection reports showing the updated condition

If you're trying to compare pricing strategies more broadly, this article on cheap homeowners insurance is a useful reminder that "cheap" usually comes from fit, discounts, and risk improvement, not from cutting core protection.

The best insurance upgrade is the one an underwriter can verify. If it isn't documented, it may not count.

What usually gives the weakest return

Cosmetic remodeling rarely helps much on its own. Carriers care far more about hidden systems than visible finishes. A renovated kitchen paired with old wiring and aging pipes still looks risky in underwriting.

If the budget is limited, put money into what prevents fire, water, and wind claims first.

Your Step-by-Step Guide to Securing Coverage

When an older home is involved, insurance shopping goes smoother when you prepare like you're going into underwriting, not just asking for a quick quote.

The process becomes much easier if you gather the right paperwork before you apply. That matters because recent data points to a 28% surge in non-renewals for pre-1980 homes in North Carolina, while some carriers still write HO-3 coverage for homes up to 50 years old if owners can document retrofits such as a new roof, which may earn a 10% to 15% discount, according to Liberty Mutual's North Carolina homeowners insurance page.

Step one is building your underwriting file

Before you ask anyone to quote the home, pull together:

- Year built and basic property details

- Roof age and material

- Electrical update records

- Plumbing update records

- HVAC replacement dates

- Any inspection reports you've already done

- Photos showing current condition

This changes the conversation immediately. Instead of saying, "It's an old house, but we've done some work," you can say, "The roof was replaced, the panel was updated, and here's the documentation."

Expect a 4-point inspection discussion

For older homes in the Southeast, carriers often want a 4-point inspection or similar underwriting review. It focuses on four systems:

- Roof

- Electrical

- Plumbing

- HVAC

The purpose isn't to fail you. It's to reduce unknowns. If the report shows those systems are in solid shape, it can open up policy options that might otherwise be unavailable.

If the inspection reveals issues, don't panic. Many homes still get insured after repairs, policy adjustments, or placement with a carrier that handles older-property risk more comfortably.

Bring the inspection mindset to the property before the inspector does. Fix obvious hazards, trim back preventable issues, and organize proof of upgrades.

Compare quotes like an underwriter, not just a shopper

Once quotes come in, line them up by substance.

Ask these questions:

- What policy form is this?

- How is the dwelling settled after a loss?

- Are wind or named-storm deductibles separate?

- Is ordinance or law coverage included or optional?

- Are water backup or service line endorsements available?

- Will the carrier require repairs after binding?

The goal isn't just to get approved. It's to avoid binding a policy that creates trouble later, either through required repairs, weak settlement terms, or a renewal the carrier doesn't want to keep.

A clean submission, good documentation, and realistic expectations make a major difference for older homes.

The Independent Agent Advantage for Older Homes

Older homes expose the limits of one-company shopping fast. If a captive agent represents a single carrier and that carrier doesn't like aging roofs, legacy wiring, or unusual rebuild profiles, the conversation ends there.

That doesn't mean the house is uninsurable. It means that carrier isn't your match.

An older home needs market access, not just a quote button

The practical advantage of an independent agent is choice. With an older property, choice matters because underwriting appetites vary sharply from one carrier to another.

One company may decline the home based on age alone unless every major system is recently updated. Another may consider the same property if the roof is newer and the plumbing has been replaced. A third may steer the home toward HO-8 or DP coverage without treating it as a dead end.

That flexibility is why older-home owners often get better results working with someone who can move across multiple markets rather than forcing one carrier to fit.

A good independent agent also frames the risk correctly

Placing older homes isn't just about submitting an address online. It often comes down to how the home is presented.

A strong submission package includes the facts that calm underwriting concerns:

- Which systems have been updated

- When the work was completed

- What documentation exists

- Whether prior issues were fully repaired

- Which policy form best matches the home

That kind of packaging can change the response from "decline" to "let's review."

If you're not familiar with how this model works, this explanation of what an independent insurance agency is gives the basic structure behind why independent representation matters so much for hard-to-place risks.

A standard house can survive a standard process. An older house usually can't.

What this looks like in real life

A homeowner with a beautifully maintained older property often assumes the market will see what they see. Underwriting usually doesn't. It sees roof age, electrical questions, prior water exposure, and rebuild uncertainty.

An independent agent can take that same home and reframe the file around documented upgrades, acceptable policy alternatives, and carriers that write this type of risk. That's not magic. It's market knowledge.

For North Carolina homeowners insurance for older homes, that difference is often the line between no workable option and a policy that makes sense.

Frequently Asked Questions About Older Home Insurance

Is knob-and-tube wiring an automatic dealbreaker

Not always, but it often creates a serious underwriting problem. Some carriers won't accept it at all. Others may consider the home only after updates or additional review. If the house still has any legacy wiring, assume the insurer will ask questions and be ready with an electrician's documentation.

Does being in a historic district change my options

Yes, sometimes. Historic district rules can affect how repairs and rebuilds must be handled, especially if specific materials or methods are expected. That can make replacement more complicated and can influence whether a carrier prefers HO-8, a dwelling fire form, or added endorsements. Owners of historic homes should pay close attention to settlement terms and rebuild assumptions.

What is ordinance or law coverage

This coverage helps when a damaged older home must be repaired or rebuilt to current building codes, not just restored to its prior condition. That matters because an older house may have legal, permitted features that no longer meet today's code. Without ordinance or law coverage, the policy may help with the direct damage but leave you paying for code-required upgrades out of pocket.

Can I get flood insurance on an older home

Yes. Standard homeowners insurance generally doesn't cover flood damage, and that gap matters for older homes because water losses can be especially destructive to aging materials and systems. Flood coverage is a separate conversation and should be reviewed alongside the homeowners policy, especially if the property has any history of water exposure or sits in an area with known flood concerns.

Will a new roof really make a difference

Often, yes. Roof condition affects both eligibility and pricing because it ties directly to wind and water losses. A roof replacement also gives you one of the easiest upgrades to document for underwriting. Keep the invoice, installation date, and material details.

Should I accept an HO-8 or keep pushing for HO-3

That depends on the home's condition and your realistic options. If the house qualifies for HO-3 on solid terms, that's often attractive. If pushing for HO-3 means repeated declines or a poor-fit policy, an HO-8 may be the smarter solution. The better question is not "Which form sounds better?" It's "Which form protects this specific house in a way I can keep and afford?"

Is a dwelling fire policy only for landlords

No. While dwelling fire policies are often associated with rental property, they can also be a practical fallback for older homes that don't fit standard homeowners underwriting. The details matter a lot, especially liability setup and how claims are settled, so this isn't a policy to buy casually.

What's the biggest mistake older-home owners make

They wait until renewal or closing to start the process. Older homes need more preparation. The best results usually come when you gather documentation early, fix obvious underwriting issues first, and shop the property based on fit rather than brand loyalty.

If you're trying to insure an older house and the market keeps giving you mixed answers, Select Insurance Group, Inc. can help you compare real options across multiple carriers. Their team works with homeowners who need practical guidance, fast quoting, and a clearer path through a difficult market, especially when a standard policy isn't the obvious fit.